Introduction

Over the past 25 years, the cost of employer sponsored health insurance premiums has increased at almost triple the growth rate for workers’ earnings, in large part because of the underlying escalating prices for hospital care. The previous and current Trump administrations aimed to help consumers by issuing executive orders requiring health care providers and insurers to disclose their negotiated prices, so that consumers can readily compare providers based on costs.

President Donald Trump’s first executive order led to rules requiring each U.S. hospital to provide clear, accessible pricing information online about the items and services they provide starting on Jan. 1, 2021. A recent issue brief attempted to compare prices at some of the Texas Medical Center’s largest hospitals using price transparency data posted on their websites. However, the data were so incomplete, that a rigorous comparison across three or more hospitals — or a full analysis of rates negotiated by two major insurers — was not possible.

The price transparency executive orders also created rules requiring insurers to publicly report their negotiated prices with all hospitals for all services and treatments. Insurer data requirements began in July 2022, about a year and a half after the introduction of hospital price transparency data. This issue brief examines insurers’ price files to compare the cost of receiving care at Baylor St. Luke’s Medical Center, Houston Methodist Hospital, and Memorial Hermann-Texas Medical Center.

Methods

Outlined below are the methods used to examine hospital price transparency data for this brief:

- Insurers’ price transparency files were accessed using the Signal platform built by Serif Health, a private company that scans, aggregates, and standardizes insurers’ websites nationwide data on a monthly cadence.

- Negotiated prices were searched using Medicare Severity Diagnosis Related Group (MS-DRG) codes or Common Procedure Terminology (CPT) codes — the two primary coding systems used in insurer-hospital price negotiations.

- The Signal platform was searched for prices for the 50 most common MS-DRG codes — for overnight stays in the hospital — in the U.S. in 2021, as indicated in the Agency for Healthcare Research and Quality HCUPnet database.

- The Signal platform was also searched for prices for 51 common outpatient procedures reported for California in 2024 because no federal reporting of the most common CPT codes exists.

- Prices were sought for both a Preferred Provider Organization and Health Maintenance Organization (or Accountable Care Organization) plan for Aetna, Blue Cross Blue Shield Texas (BCBSTX), Humana, and United Healthcare. Missing data for certain plans, hospitals, and service codes limited the number of services that could be compared across the three hospitals.

Results

BCBSTX provided the most complete set of prices negotiated with all three hospitals; their prices are presented in Table 1. The mean price for an overnight stay in the hospital for patients with BCBSTX coverage was highest at Memorial Hermann, second highest at Houston Methodist, and lowest at Baylor St. Luke’s. As one would expect, the mean price of a hospital stay was higher for the PPO plan (Blue Choice PPO) than the HMO plan (Blue Essentials) at Baylor St. Luke’s and Memorial Hermann. However, BCBSTX negotiated identical rates for its PPO and HMO plans with Houston Methodist. The 44 DRG codes that could be compared across the three hospitals are listed in Appendix Table A.

Table 1 — Average Prices Negotiated by BCBSTX with 3 TMC Hospitals for 44 Common Diagnosis Related Groups

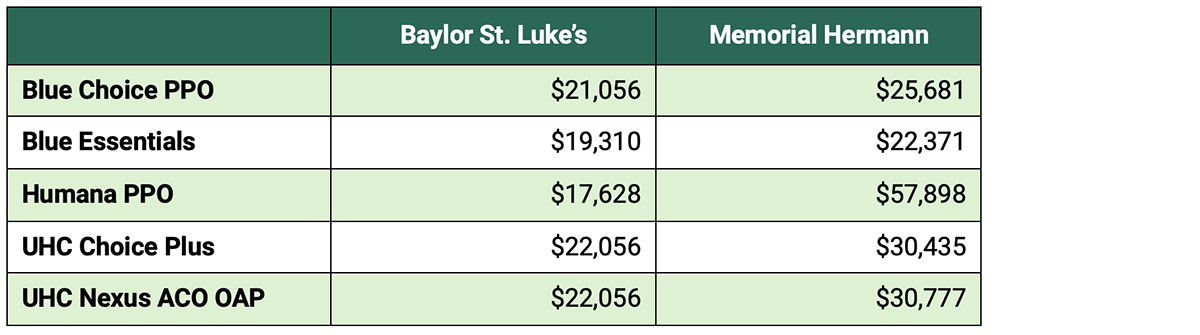

Three insurers reported prices that they negotiated with Baylor St. Luke’s and Memorial Hermann — but not Houston Methodist — for the same 44 MS-DRG groups reported in Table 1; their prices are compared in Table 2. The DRG prices that the three insurers negotiated with Baylor St. Luke’s were relatively similar, with the Humana PPO having the lowest mean price across the 44 DRG codes.

In contrast, the three insurers all paid higher mean prices for patients requiring an overnight stay at Memorial Hermann, and there was substantial variation across insurers. The mean price for Humana PPO patients at Memorial Hermann was 88% higher than the next highest plan — $57,898 versus $30,777 for a UHC Accountable Care Organization plan.

Table 2 — Average Prices Negotiated by Insurer with 2 TMC Hospitals for 44 Common Diagnosis Related Groups

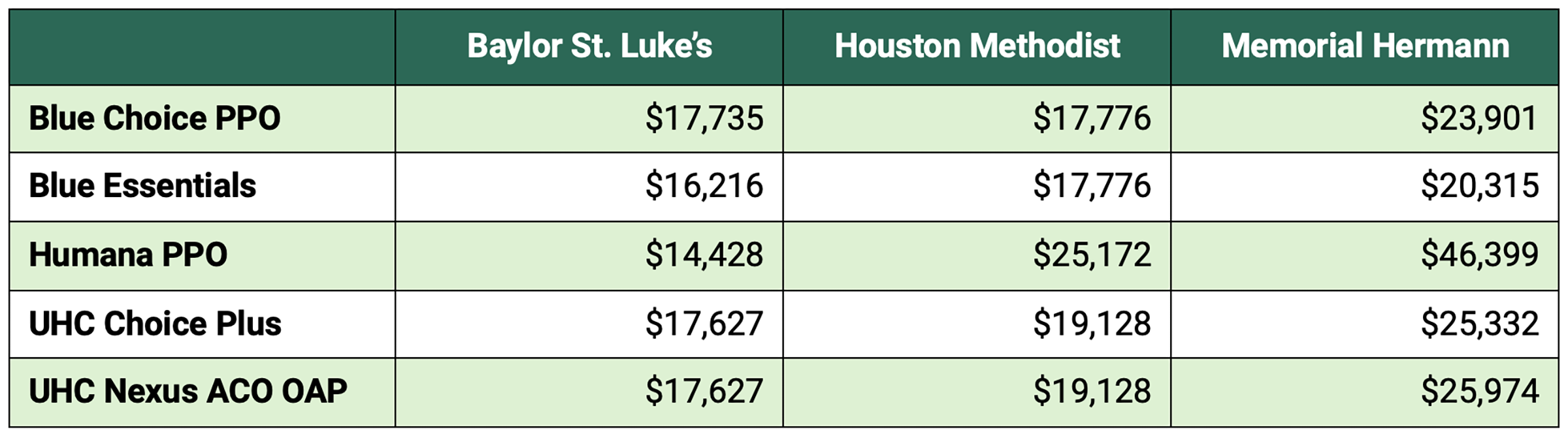

It was only possible to compare DRG prices across all three insurers and all three hospitals for 10 DRGs. These 10 DRGs are marked with an asterisk in Appendix Table A. Mean prices for these 10 DRGs for all three insurers reported in Table 3 displayed the same pattern observed in Table 1, with prices being highest at Memorial Hermann, second highest at Houston Methodist, then lowest at Baylor St. Luke’s. The ordering of mean prices across insurers was similar to Table 2, with prices for BCBSTX plans being lower than those for UHC plans. The Humana PPO plan had the lowest mean negotiated DRG price at Baylor St. Luke’s, but remarkably high mean prices at Memorial Hermann.

Table 3 — Average Prices Negotiated by Insurer with 3 TMC Hospitals for 10 Common Diagnosis Related Groups

BCBSTX also provided the most complete set of CPT prices negotiated with all three hospitals; these data are presented in Table 4. The mean price for outpatient care for 55 CPT codes was similar for patients with Blue Choice PPO coverage at all three hospitals, ranging from a low of $1,701 at Memorial Hermann to a high of $1,792 at Baylor St. Luke’s. In contrast, mean prices for outpatient care were substantially lower at Memorial Hermann for patients with HMO coverage with BCBSTX ($1,445 for Blue Essentials) relative to patients receiving care at Baylor St. Luke’s or Houston Methodist ($1,667 and $1,702 respectively). The 55 CPT codes that could be compared across the three hospitals are listed in Appendix Table B.

Table 4 — Average Prices Negotiated by BCBSTX with 3 TMC Hospitals for 55 Common CPT Codes

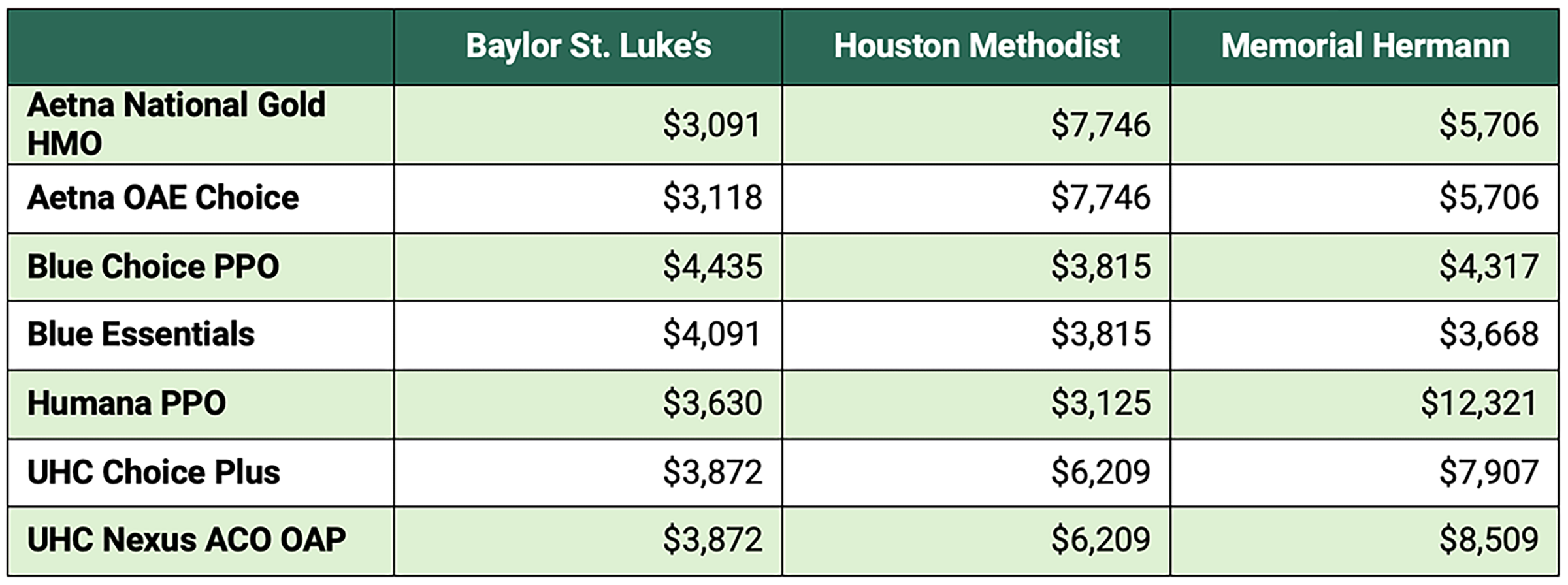

Due to missing prices for insurers other than BCBSTX for multiple CPT codes, the comparison of mean CPT prices across multiple insurers was limited to just 18 codes. These 18 codes — marked with an asterisk in Appendix Table B — were almost all for surgical services, leading to generally higher mean prices in Table 5 than for Table 4.

The mean prices in Table 5 reveal that no insurance plan negotiated the lowest prices across all three hospitals. Moreover, no hospital was consistently the lowest-cost option across the seven insurance plans compared. However, the negotiated prices for patients treated at Baylor St. Luke’s were substantially lower than those at Memorial Hermann, except for the BCBSTX plans, which had only slightly higher mean prices at Baylor St. Luke’s.

Table 5 — Average Prices Negotiated by BCBSTX with 3 TMC Hospitals for 18 Common CPT Codes

Discussion

The findings of this analysis indicate that other than BCBSTX, major insurance companies covering Houston residents have posted negotiated price lists with significant gaps in information for at least one major hospital in the TMC. It may be the case that some insurers are using coding schemas other than MS-DRGs and CPT codes to negotiate the price of services. To address this concern, searches were also performed using APR-DRGs and revenue codes that are similar to the MS-DRG and CPT codes used in the analysis.

In the few cases where prices were found, the comparable code often had a broader definition than the original code, impeding reliable price comparison. Nevertheless, insurers have reported considerably more price information than hospitals, providing consumers and employer purchasers with valuable information for choosing between insurers and benefits packages.

Choosing Lower-Priced Hospitals Saves Money for Patients & Their Employers

The differences in mean prices across hospitals for consumers with the same insurance plan are striking. For 44 common DRG codes requiring an overnight stay in the hospital, a patient with Blue Choice PPO insurance faces a mean treatment price of $21,056 at Baylor St. Luke’s versus $25,682 at Memorial Hermann. A patient with UHC Choice Plus coverage would face a mean price of $22,056 for these 44 DRG codes at Baylor St. Luke’s, but a much higher mean rate of $30,777 at Memorial Hermann. Patients with Humana PPO insurance face the widest price differential. These patients face a mean price of $17,628 if they seek care at Baylor St. Luke’s, but a mean price of $57,898 if they are treated at Memorial Hermann.

Houston employees with Humana PPO coverage could pay substantially more out-of-pocket if they were admitted to Memorial Hermann versus Baylor St. Luke’s for treatment. According to the KFF Employer Benefits Survey, 59% of workers with employer-sponsored health insurance in 2024 had plans requiring them to pay coinsurance for each hospital admission. The average coinsurance rate for these workers was 21%.

Therefore, the mean out-of-pocket payment for a worker with Humana PPO insurance seeking care at Baylor St. Luke’s could be $3,702 versus $12,159 at Memorial Hermann. KFF survey data indicates that most PPO beneficiaries have an out-of-pocket maximum on their plan that would protect them from having to pay $12,000+ for care. Nevertheless, 63% of employees nationwide with PPO coverage faced an out-of-pocket maximum of $3,000+, 45% faced a $4,000+ maximum, and 22% faced a $6,000+ maximum.

The price differentials across hospitals also have important implications for employers. The KFF survey determined that in 2024, 63% of insured workers were in plans that are self-funded by their employer. For the 44 DRG codes compared across five insurance plans (Table 2), the smallest price difference between the two hospitals was 16%, and the largest was 228%.

Thus, steering more employers to choose hospital admission at Baylor St. Luke’s versus Memorial Hermann could yield substantial savings for self-insured employers, which they could translate to lower insurance premiums for workers in the subsequent year. Both hospitals are nationally ranked in multiple specialties by USNews, so differences in quality matter much less than price differences in most cases.

Employers can also achieve significant savings by steering workers toward hospitals with lower prices for outpatient care. Among the seven insurance plans that reported negotiated prices for the same 18 outpatient procedure codes in the three hospitals being studied (Table 5), the median price difference between any two hospitals was 36%. Major insurers have begun to offer health plans that steer patients toward lower cost, high quality providers, and employers who adopt such plans could achieve substantial savings. These plans set low copays or eliminate them for doctors and hospitals that charge lower prices and/or achieve higher quality ratings.

Employer Spending Varies Widely by Insurer Choice

Employers can save themselves and their workers significant amounts by choosing insurers that have negotiated lower prices with the different TMC hospitals. In Table 2, both the BCBSTX PPO and HMO insurance plans show lower mean negotiated prices than the two comparable UHC plans for 44 common diagnoses requiring admission at the two hospitals. The lower mean price for BCBSTX plans reflects generally lower prices for individual DRG codes versus the UHC plans. For example, the negotiated PPO price with BCBSTX versus UHC insurance was lower for 38 out of 44 individual DRGs requiring a hospital admission at Baylor St. Luke’s.

Both Aetna plans have lower mean negotiated prices at Baylor St. Luke’s and Memorial Hermann than the two UHC plans for 18 common outpatient procedures or tests (Table 5). The Aetna plan prices at Houston Methodist are higher than those at UHC, so there are important cost differences for employers using these two plans, depending on where the majority of their workers seek care. Similar tradeoffs exist for employers using BCBSTX plans to cover their workers.

The BCBSTX negotiated prices for outpatient care are noticeably lower at Houston Methodist and Memorial Hermann relative to most other insurers. The negotiated BCBSTX prices at Baylor St. Luke’s are higher than their competitors, but the hospital remains a relatively low-cost option in general. Again, the noticeable differences in prices suggest that there are significant opportunities for employers to achieve cost savings for their workers by steering patients to lower-cost alternatives for care.

Stronger Rule Enforcement Can Improve Transparency

Significant price differentials were identified across TMC hospitals and insurance plans, based on an analysis of prices for multiple common DRG codes used for overnight stays, as well as outpatient procedure codes. However, only BCBSTX reported enough of their negotiated prices in a format that allows comparison across most of the codes examined. In many cases, the other insurers posted no prices for common DRG and procedure codes. In other cases, insurers would report the negotiated price as a percentage of charges, but they failed to report the dollar value of those charges.

The Centers for Medicare and Medicaid Services (CMS) are responsible for enforcing the Transparency in Coverage regulations that originated from Trump’s first executive order involving price transparency. The CMS website explicitly states that insurance plans must disclose “rates for all covered items and services between the plan or issuer and in-network providers.”

With the exception of BCBSTX, none of the major insurers examined disclosed rates for all the services used by their members. However no known enforcement actions or fines have been issued by CMS in response to these omissions. Unless the federal government fulfills its responsibility to hold insurers responsible for price transparency, employers cannot take fully informed action to lower health care costs for their workers.

Conclusion

As the cost of health care coverage continues to grow far more quickly than workers’ earnings, employers and the federal government can take steps to reign in rising costs. Hospital spending accounts for nearly one-third of health expenditures in the U.S., and the analysis reveals that there are wide variations in prices for common illnesses and treatments across high-quality hospitals in Houston. Employers can use the price data made available by the price transparency executive order to redesign their health care benefits, guiding employees toward high quality, lower cost hospitals for care.

Although the price files released by insurers are complex, there are multiple companies — including the one used in this analysis — that have gained expertise with these files, and benefit consultants can help employers design benefit plans with tiered pricing or variable copayments to encourage more cost-effective use of health care. Employers may be concerned that redesigned insurance plans increasing copays for higher-priced providers may upset some workers. However, the potential cost savings are so significant, that employees are likely to accept the benefit changes as long as their employers share the resulting savings with them through lower insurance premiums in subsequent years.

CMS should strengthen enforcement of price transparency rules to ensure employers and patients can easily access comprehensive information on the prices of all providers offering care in the local market. Insurers may appear to have complied with rules when price files are available for download from their websites. However, when one attempts to use these files to compare competing hospitals in a local market, important gaps in reporting for common diagnoses and for major hospitals become apparent.

Unlike most developed countries, the U.S. has chosen to let the private sector provide health insurance coverage to workers and their families. Healthy private sector competition among health care providers and insurers requires price transparency for customers. Unless CMS compels insurers to improve their price transparency, the current cost trajectory for private health insurance will make this system unsustainable.

Appendix

Table A — Top 50 Medicare Severity-Diagnosis Related Group (MS-DRG) Ranked by Number of Discharges, 2021

View Appendix Table A (PDF).

Table B — Top Outpatient Current Procedural Terminology (CPTs) in California, 2024

View Appendix Table B (PDF).

This publication was produced on behalf of Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by external experts prior to its release. Any errors are the responsibility of the author(s) alone.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.