Author(s)

Russia’s Military Potential Follows Its Oil Production

Russia’s era of easily accessible oil from Western Siberia appears to be coming to a close. This creates a fiscal constraint that Moscow is unlikely to offset through conflict or narrative engineering. Over time, the country’s diminished oil production capacity is expected to weaken its ability to hold geopolitical influence. In the next five years, however, it may have the opposite effect — raising the risk of conflict if the Kremlin decides to act militarily beyond Ukraine before its financial advantages erode further.

Resisting geological decline does not quite capture the same media attention as the ongoing war in Ukraine. Russian operations in Siberian, Volga, Caspian, and Arctic oilfields often lack the perceived newsworthy quality regulated to combat. Whether covered in the media, barrels from those fields, or the lack thereof, will likely be a primary driver of Russia’s strategic decision-making, military capacity, and global influence.

Yet trends in the country’s oil production do not appear to be in Moscow’s favor. The rector of the Almetyevsk State Technology University’s Higher School of Oil noted in a March 2025 interview, “Yes, the era of easy oil is over. …There will be no more ‘gushers.’” This decline carries direct fiscal implications. Echoing Marcus Tullius Cicero’s observation that “the sinews of war,” require “a limitless supply of money,” the Kremlin’s financing efforts can be distilled into either the direct sale of oil or its indirect monetization through loans-for-oil deals. Thus, less money equals less military power over time.

National leaders typically approach acts of war on the basis of a risk-reward assessment that combines ambition and emotion with financial and industrial calculations, including how a campaign could be conducted and sustained. Four and a half years into the Russia-Ukraine war, President Vladimir Putin remains committed to the conflict, despite its significant financial costs and domestic risks. That said, sustaining military options and preparing for the future both require long-term, substantial money inflows.

Therefore, oil production is perhaps the most critical metric for assessing Russia’s capacity to exert international influence, maintain its war effort, and rebuild for further strikes on Ukraine, and potentially, future actions against Poland, the Baltic States, and parts of Central Asia.

How Oil Affects Russia’s Influence

Russia produced roughly 9 million barrels per day of crude oil in 2024 — equating to 11% of the global supply in that year — with a population less than half that of the United States and an economy about 15% smaller than Texas’. As such, a large portion of its oil supply is allocated to exports, which situates Russia as a systemically important supplier with both commensurate income, which approximates to $120 billion U.S. dollars in oil revenues in 2024, and geopolitical influence.

Influence flows from the fact that oil pervades modern life. It remains the world’s most widely traded commodity, with an annual global turnover exceeding $2 trillion at a volume of 100 million barrels per day and an average price of $60 per barrel — more than three times the value of all semiconductors sold worldwide in 2024. Oil is also highly fungible. After Russian tanks crossed into Ukraine in February 2022, Urals oil that would have been sold to European buyers was easily redirected to China, India, and other alternative markets.

Significant discounts driven by reputational risks and sanctions made Russian oil more attractive to customers in the Global South, although the same buyers continue purchasing shipments even as the price gap with global benchmark crude grades narrows. In short, if Russian producers can deliver barrels to a port or through an export pipeline, a buyer will likely pay for them. However, trends related to Russia’s oil production capacity suggest that fewer barrels will be available in the coming years.

Factors Shaping Russia’s Oil Production Capacity

Geological fatigue — the gradual depletion of oil reservoirs — is currently unfolding in the Russian oil patch. Despite persistent efforts, Russia’s oil production is weakening. Oil producers are drilling at levels not seen since the late 1980s. Furthermore, the proportion of horizontal wells — used to access more of an oil-bearing formation from a single wellbore — has risen from approximately 15% in 2011 to nearly 60% in 2025. This shift marked a decline from a 68% horizontal well share in 2024, likely due to capital shortages and a shift to cheaper, less tech-intensive vertical wells. Yet oil production still declines.

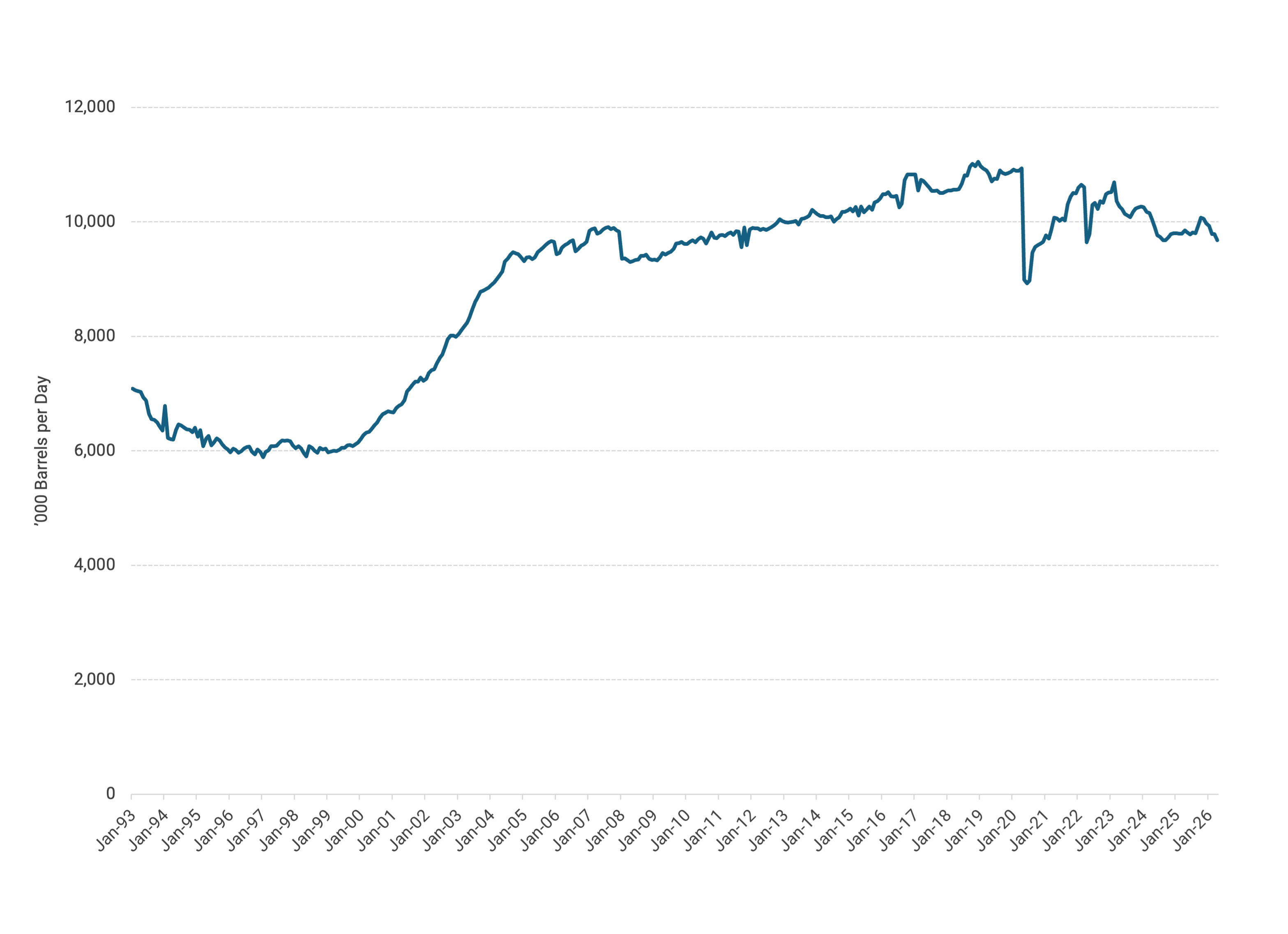

Russia is transitioning from a resource superpower to a resource depletion manager. In Russia’s oil heartland of Khanty-Mansiysk in Western Siberia, which accounts for approximately 40% of the country’s output, production has steadily declined since 2009. From 2019 to 2024, output in Khanty-Mansiysk fell by more than 14% while the rest of Russia also saw oil production decline by nearly 9% (Figure 1). Russian companies have located additional oilfields in Eastern Siberia and the Caspian Sea area, but not on a scale that would be sufficient to offset declining production in the Western Siberia fields.

Figure 1 — Russian Production of Crude Oil, January 1993–April 2026

Note: The figure’s calculations include lease condensate.

Could these declines be reversed? Oil production is typically a product of the following formula: a dynamic multiplication of geology, technology, capital, and oil prices collectively equals output. Russia still has significant geological potential, as attested to by at least one large American oil company’s confidential talks with Russian state champion producer Rosneft that the Wall Street Journal covered in August 2025. However, oil prices are largely beyond its control.

That leaves technology and capital as factors over which the country can have greater influence. For Russia, access to technology and capital are functions of geopolitics, as Moscow’s interventions into neighboring countries, including Ukraine, have constrained the availability of such resources. Western sanctions have progressively limited access to both technology and capital in the wake of Moscow seizing Crimea in 2014, supporting a war in Eastern Ukraine from 2014–22, and launching a full-scale invasion of Ukraine in 2022, which has resulted in a nearly five-year war that is still ongoing.

Capital

Capital enables drilling at the scale and pace needed to offset natural production declines and maintain, or when possible, grow production. In the first decade of the shale boom, U.S. producers spent over $1 trillion in capital investment. If one assumes oilfield services spending equals two thirds of total capital expenditures — roughly the ratio for Russia — the data suggested North American oil and gas producers spent approximately six times what Russian producers did in 2024, in terms of U.S. dollars. Even accounting for the attenuating impacts of ruble-devaluation on local service costs in Russia, the gap remains substantial.

Russian oil producers’ ability to self-fund investments at a level necessary to maintain production are likely to be limited. Based on the author’s estimates, Russian official disclosures of comprehensive oil production costs suggest that the margin after operating, capital, and other costs are paid is on the order of 30–40%. Wartime financial stresses coupled with the cost of repairing damage caused by Ukrainian strikes on refineries and other infrastructure could bring the gross margin on exported oil and refined products closer to 25%.

With annual crude oil and product exports earning around $120 billion in gross revenues, a 25% gross margin would mean $30 billion. If the Russian government were to impose wartime levies that absorbed half the margin’s estimated amount — which is a highly plausible prospect — then the remaining $15 billion per year in additional funds could be used for reinvestment in future oil production. Shareholders would not receive dividends or other regular payback, but given the wartime mobilization of Russia’s economy, they would likely accept this deprivation. Yet even with more funds, recent years’ efforts have demonstrated that drilling more holes and putting more steel in the ground have not been able to revive oil production in Russia.

Technology

In the case of technology, it amplifies the impact of the capital deployed, especially when older oilfields and more complex deposits are involved, which is the current situation Russian producers are facing in Western Siberia. When functioning successfully, technology’s ability to increase returns on capital then stimulates investment in developing and improving the technologies deployed for drilling and production. This is why H&P, a leading American drilling company, can by itself drill in 2023 about 70% of the footage that all the producers and drillers in Russia achieved in a similar timeframe, but with one seventh as many rigs.

Technology related to oil production is vital not only onshore but also for challenging Arctic offshore projects that the Kremlin sees as potentially offsetting declines in Western Siberian production. For example, estimates for the Vostok Oil project, located over 1,700 miles northeast of Moscow, are 2 million barrels per day of oil at peak output. However, it is projected to cost as much as $130 billion to develop. Could Moscow self-fund the project’s development to its full potential? Perhaps, but constraints on access to technology would introduce substantial barriers, and the project’s high price tag would create significant opportunity costs by requiring funds to be diverted from other activities.

Russia’s capacity to self-finance its projects matters because foreign capital is unlikely to be available. When the Russia-Ukraine war ends, many companies may hesitate to invest in Russia given that the country could begin another conflict, expropriate assets, or impose new fiscal terms once foreign investors have sunk capital into a project.

Finally, any potential Russian oil production asset, assuming a durable ceasefire in Ukraine, would be competing for capital with other assets around the world. Oil deposits in Argentina, Guyana, Iraq, the Persian Gulf region, and other areas across the Americas would all largely present profiles with less aboveground risk than those located in a geopolitically unstable Russia.

Global Impacts of Russia’s Reduced Oil Production

Declining Russian oil output will affect China, India, Canada, the U.S., European NATO members, and Middle East oil producers but will be particularly acute for Russia’s post-Soviet neighbors.

For China and India, Russia will likely appear as a less attractive partner if its oil production continues to wane. For Canada, every lost Russian barrel is an additional market space for heavier, high-sulfur crude from the Alberta oilsands. For the U.S. and European NATO members, if Russia maintains less oil revenue over time, Moscow would likely be a persistent threat, but at the same time, see its ability to pay for military personnel and hardware eroded. For Middle East producers, a diminishing number of Russian barrels may potentially lead to increased demand for exports from the Gulf region. The ongoing Iran war and Strait of Hormuz disruptions presently obscure this underlying strategic reality, but as bypass routes are built, multiple Middle Eastern suppliers will have established a more robust market presence.

Notably, for Russia’s post-Soviet neighbors, Russia’s reduced oil capacity could mean a heightened period of volatility in the next five years, particularly if Russian leaders conclude their window for military actions is closing due to structural oil revenue declines. However, decreased oil production and revenues could also facilitate deterrence efforts and set the stage for a future that finds Moscow with substantially less capacity to translate territorial aspirations into military actions.

Diminished Oil and Increased Risk

Russia’s resolve should not be underestimated. Oil largely underpins Putin’s domestic political viability and Russia’s global position. Drilling activity attaining or even surpassing Soviet-era records in the next three years is highly plausible. Higher oil prices could also provide temporary respite — as evinced by the Strait of Hormuz closure.

Moreover, Russia has other resources — gas, metals, coal, nuclear fuel sales, and military equipment — but the combination of these funds is not expected to equal the country’s prewar oil revenues. Additionally, the war with Ukraine has significantly diminished Russia’s arms sales potential, as potential buyers are concerned about Western sanctions and are also watching a range of NATO and Ukrainian indigenous weapons outperform Russian-made systems.

The country’s most accessible oil reserves are depleting without clear replacement. The remaining barrels are also more difficult and expensive to produce. All else held equal, this suggests Russia’s ability to convert resource wealth into military power will face increasing constraints. Two key strategic insights result:

- Oil revenue constraints will likely intensify at the expense of Russia’s longer-term comprehensive national power.

- Short-term risks are expected to rise as Moscow may perceive that it has a limited window for credibly employing military actions against other post-Soviet states and NATO neighbors.

Due to constraints on oil production and revenue generation, Russia may increasingly resemble a giant Eurasian North Korea — highly nuclearized, structurally isolated, and economically vulnerable — rather than the military powerhouse many perceived it to be before the Russia-Ukraine war. The next decade will be a dynamic period of adjustment, with commensurate strategic risk and deterrence requirements. NATO thus could be facing one of its most challenging set of tasks since perhaps the early 1980s.

Acknowledgments

This brief draws on the author’s piece, “Russia’s Oil Production Decline Is a Geopolitical Clock,” and other previously published research available through publicly accessible personal platforms.

This publication was produced by Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by outside experts prior to release. Any errors or omissions are solely the responsibility of the author(s).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.