Kuwait’s Energy Strategy

In 2025, Kuwait Petroleum Corporation (KPC) announced a production increase that was significant not only in scale but also in precedent. KPC plans to invest up to $10 billion U.S. dollars per year to raise oil production capacity by 25%, from 3.2 million barrels per day (bpd) in 2025 to 4 million bpd by 2035. Alongside more oil, KPC seeks to triple gas production to 2 billion cubic feet per day by 2040.[1] At the same time, Kuwaiti authorities pledged to eliminate carbon dioxide emissions from the oil sector by 2050, a decade ahead of the country’s national target.[2]

For some wealthy oil producers, these goals would seem ambitious, though straightforward. However, the institutional environment in Kuwait could complicate achieving such investment targets. Kuwait’s energy sector implementation has historically been constrained by institutional barriers including limiting legal architecture, ministerial turnover, political impasses, independent regulatory deficiencies, and lack of cross-sector coordination. While Kuwait’s policy ambitions are well established, delivering on such plans will be a complex venture, both politically and economically.

This report builds on discussions at a Middle East Energy Roundtable held in Kuwait City in December 2025. However, by the spring of 2026, the Iran war following joint U.S.-Israeli strikes on Feb. 28 has added further challenges to Kuwait’s energy ambitions. The conflict has significantly disrupted its oil export economy and led to physical attacks on infrastructure, including damage to refineries and production shut-ins that have halted exports. Thus far, the country has also experienced its sharpest decline in oil production since the 1990 Iraqi invasion of Kuwait following Iran’s blockage of export routes through the Strait of Hormuz in response to the conflict. Output fell by more than 76% from January 2026 levels to an average of 600,000 bpd in April.[3]

At the same time, recent political developments have created an opportunity to reduce policy gridlock. The May 2024 suspension of Kuwait’s National Assembly for up to four years, which was still in place at the time of writing, could enable the enactment of more ambitious energy and investment plans than previously considered achievable. However, whether these plans can move forward given the ongoing conflict among the U.S., Israel, and Iran and institutional uncertainty remains unclear.

Limiting Legal Architecture

Kuwait’s energy sector continues to operate within a largely rigid legal framework that has not been substantially reconfigured to reflect the evolving structure of the industry since the 1990s. While this framework has historically been effective in consolidating state control over hydrocarbons, it has proven to limit Kuwait’s opportunities for the forms of investment, contracting, and sector organization associated with large-scale energy development in neighboring Gulf states.

This constraint is most evident in the structuring of foreign participation in upstream oil and gas. The Kuwaiti Constitution prohibits foreign ownership of natural resources and limits the granting of concessions for resource exploitation, narrowing the legal instruments for international cooperation.[4] At the statutory level, the country’s oil sector remains centered on Law No. 6 of 1980, which established KPC as the unified national oil company with exclusive rights over the exploration, production, and marketing of hydrocarbons.[5] Thus, Kuwait has not yet established an updated petroleum act that would permit private sector access to licensing or operating upstream oil fields. International oil companies (IOCs) continue to be regulated to “technical service contracts or international joint ventures rather than equity participation.”[6]

Additionally, the suspension of Project Kuwait in 2005 illustrates the implications tied to outdated legal architecture. The project sought to involve IOCs in the development of northern oilfields but was ultimately unsuccessful, in part because proposed arrangements largely misaligned with prevailing constitutional interpretations and also proved politically difficult.[7] Similar constraints have consistently hindered IOC participation, even as each major strategy cycle since the mid-1990s identified IOC participation as a necessary prerequisite for energy development.[8]

Such legal rigidity has also led to reduced oilfield-level outcomes. In the Saudi Arabia-Kuwait neutral zone, production is divided between areas managed by KPC subsidiaries and those operated through partnership with the major U.S. oil corporation, Chevron. Oil sector experts from these adjacent fields point to differences in operational responsiveness and maintenance timelines; the Chevron-operated side showed faster intervention and greater efficiency in similar geology when compared to KPC operations.[9] The comparison reflects Kuwait’s limited access to combined international operating models and expertise, despite its robust domestic technical capability.[10] Outside the neutral zone, the Kuwaiti legal system could also restrict the accommodations necessary for such international and private partnerships.

These constraints extend beyond upstream oil production. Kuwait has sought to expand private sector participation in the electricity sector and develop new capacity through alternative financing structures. Here, too, legal frameworks tended to create barriers to policy objectives. Kuwait has enacted legislation for public-private partnerships (PPPs) in power generation, notably through Law No. 39 of 2010 — also known as the Independent Water and Power Projects (IWPP) Law — and Law No. 116 of 2014, with the latter establishing the Kuwait Authority for Partnership Projects (KAPP).[11] Under this framework, KAPP is mandated to structure, tender, and supervise projects involving PPPs, including independent power producer (IPP) and IWPP developments.

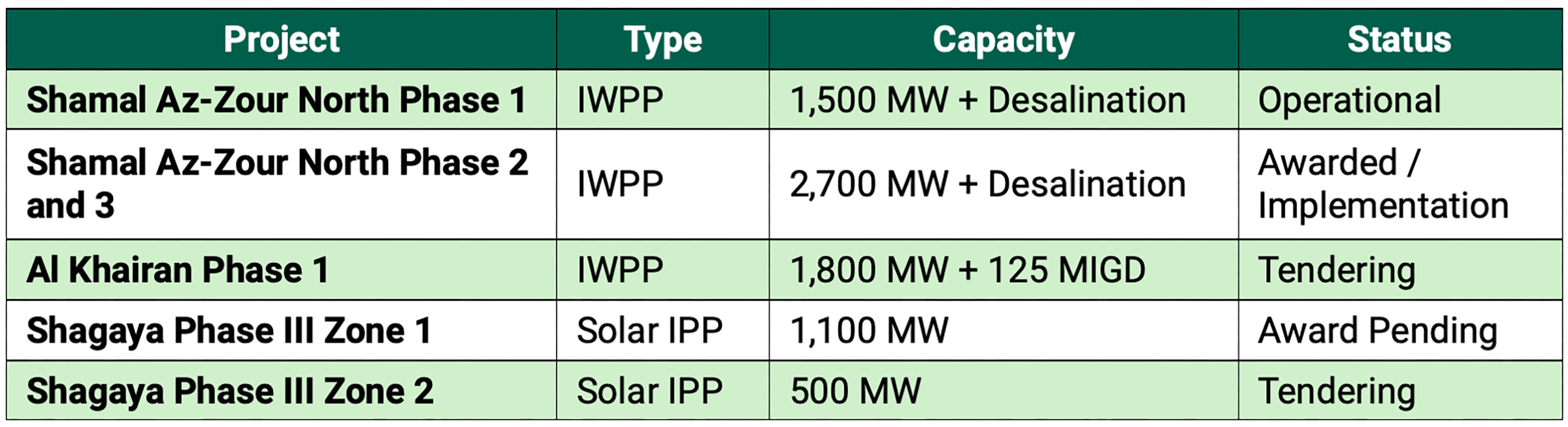

Yet these laws have produced only a partially developed market framework, which has led to slowed progress, as Shamal Az-Zour Phase 1 is the only completed and fully operational IPP/IWPP project to date (Table 1).[12] Across the Gulf region, IPP models have been supported by legal systems capable of defining contractual obligations and allocating risk in a consistent manner. For example, in Saudi Arabia, projects such as the Rabigh 2 IPP expansion have been tendered through the Saudi Power Procurement Company under long-term power purchase agreements.[13]

Table 1 — Current and Future IPP and IWPP Projects in Kuwait

Note: MW refers to megawatts; MIGD refers to millions of imperial gallons per day.

More broadly, Kuwait’s legal framework continues to channel energy development projects through public-sector contracting structures rather than through instruments tailored to large-scale, capital-intensive energy projects.[14] This approach affects project timelines, contractual design, and the ability to structure long-horizon investments. While expanding energy investments and developments remain clear policy directives, such goal’s implementation is required to pass through rigid legal channels that can cause delays.

These limitations are becoming more consequential as Kuwait seeks to expand into gas, renewables, and lower-carbon energy pathways. Renewable projects continue to rely on existing IWPP and PPP frameworks rather than a targeted renewable energy law.[15] Altogether, one of Kuwait’s primary challenges is to build legal frameworks capable of more fully and effectively accommodating its energy policy goals.

Ministerial Turnover and Political Impasses

The capacity of Kuwait’s energy sector for further development and expansion is largely constrained not only by its institutional design but also by the lack of continuity within those institutions. Ministerial turnover has been one of the most persistent features of the Kuwaiti system, particularly within agencies central to energy governance. Between 2000 and 2024, Kuwait cycled through 22 individual cabinets, which equates to an average lifespan of just over one year per government. Across that same period, voters went to the polls 12 times to elect new National Assemblies. More specifically, institutional continuity has been least sustained in agencies mainly responsible for long-horizon infrastructure planning and project execution, and the significant turnover rate has also resulted in tense relations between the executive and legislative branches.

Recent energy leadership rotations illustrate this pattern. When Saad Al-Barrak was appointed minister of oil in June 2023, he was the eighth holder of the post in as many years, and he was in office for seven months, while his successor was replaced after nine months, before the current incumbent, Tareq Sulaiman Al-Roumi, was appointed as minister in October 2024.[16]

Leadership changes have occurred through resignations, interim appointments, and cabinet rotations. Recent reporting has described the ministry as experiencing a “revolving door” of leadership, demonstrating a broader trend rather than a short-term disruption.[17] The rapid turnover of oil ministers in Kuwait presents a marked divergence from other Gulf states where oil and energy ministers often remain in post for years, even decades, and are able to impart policy continuity and decision-making predictability. Significantly, Kuwait’s current oil minister is an oil sector veteran, having joined the Kuwait Oil Company in 1976, and tensions with the presently suspended National Assembly that marked his predecessor’s tenures have not factored into his role as of yet.[18]

Ministerial uncertainty is rooted in the structural features of Kuwait’s political system. Kuwait’s National Assembly typically exercised extensive oversight powers, which opened ministers to questioning — or as the Kuwaiti Constitution states, “interpellation” — and sustained political pressure.[19] As a result, resignations, rotations, and cabinet reconfigurations became recurring features of governance. For example, Kuwait underwent four elections and three parliamentary suspensions from 2020 to 2024.[20] Over the longer period of 1963–2020, 149 interpellations occurred with nearly 62% of them initiated by individual members of parliament (MPs) rather than organized blocs.[21] In fact, 11 of Kuwait’s 18 legislative terms were suspended before completing their full term, mainly due to interpellations or motions of confidence, and the 2016–20 Parliament was the first to serve its full four-year term in its entirety since the session of 1999–2003.[22]

The pattern of ministerial turnover functions as a structural rather than an episodic issue. Kuwait combines permissive, partial oversight procedures with a highly individualistic, nonpartisan political system; interpellations can be advanced by individual MPs at any time, without fixed limits on frequency, while the wider party system remains inadequately institutionalized. The result is a setting in which oversight tools are available in principle for accountability, but in practice, they can often generate delay, stagnation, and recurring legislative-executive impasses.[23]

For example, in September 2016, Parliament strongly opposed government efforts to impose austerity measures — at a time when oil prices and government revenues were declining — which included the lifting of subsidies on water, electricity, and fuel. In response, the emir dissolved Parliament that October, but voters’ criticism toward the austerity measures led to opposition candidates winning nearly half the seats in the National Assembly in the election held in November 2016.[24]

However, parliamentary pressure only partially covers issues related to institutional continuity. Turnover is also occurring within the operating state-owned companies themselves. Policies within KPC subsidiaries require senior staff to retire after extended service periods — 35 years — with strictly limited extensions in cases of critical expertise or until the employee turns 60 years old.[25] While intended to renew the workforce and expand opportunities for younger national talent, these measures have also led to a more rapid loss of accumulated technical experience. As a result, continuity in training and expertise is weakened at both the leadership and operational levels.

Workforce coherence is particularly significant in the energy sector, where reform requires sustained technical oversight and multiyear implementation; thus, these measures largely resulted in a pattern of strategic repetition without cumulative learning. Subsequently, production targets set in 2005 for achievement in 2020 have not been met, and the same targets, though modestly revised, are now set for 2035 in Kuwait’s New Vision.[26]

While recent political developments, such as the National Assembly’s suspension in May 2024, may serve to ease short-term legislative pressure, it does not by itself sustainably address this administrative issue of recurring turnover in important ministerial and state-owned company positions.[27] Overall, institutional continuity will be determined by whether Kuwait can learn from policy lessons, stabilize leadership in key institutions, and create structures that allow reform to continue beyond individual appointments. Officials have a time-bound window to deliver tangible reforms before the National Assembly is scheduled to be reinstated by May 2028.

Independent Regulatory Deficiencies

Another matter related to Kuwait’s primary institutional deficiencies is the lack of an independent regulatory authority for its electricity sector. The leadership position within the Ministry of Electricity, Water, and Renewable Energy combines policymaking, service provision, and sector oversight within a single framework. As a result, Kuwait’s private power generators are managed by separate state agencies rather than a dedicated sector regulator.[28] Also, tariff-setting, market participation, and project development does not receive the same level of supervision as distinct regulatory anchors found in more developed power markets.

The absence of a separate regulatory authority for the electricity sector continues to shape decision-making on prices, contracts, and system planning, which remain embedded within government ministries. As such, the sector is vulnerable to administrative turnover and short-term political pressures. One defining feature of the current structure is that the residential electricity tariff has remained at 2 fils per kilowatt-hour since 1966 and covers only 5% of the government’s cost of provision.[29] In this case, the lack of an institutional framework capable of sustaining tariff adjustments over time has led to stagnant pricing and oversight. Without a regulatory body with a clear mandate and operational independence, pricing reform and private sector participation will likely remain difficult.

In areas where Kuwait has already identified reform priorities, similar constraints still persist. IPP models, which have mainly supported capacity expansion across the Gulf, require consistent regulatory frameworks capable of structuring long-term agreements, allocating risk between public and private actors, and providing tariff clarity. As Kuwait’s current regulatory bodies are under ministerial positions with broad reach and extensive turnover, it has largely been unable to provide IPP projects with similar structural support in terms of tariff-setting, contractual consistency, and long-term risk allocation. Also, the availability of suitable land for large-scale projects is limited in Kuwait, which is a separate but important structural constraint.

In a similar vein, efforts to introduce more cost-reflective tariffs remain restricted due to these same regulatory limitations. Pricing reform requires not only political will, but institutions capable of enforcement. For Kuwait, where the same entity is responsible for both service provision and price setting, price reform’s credibility and durability tend to be more difficult to sustain, even when the economic rationale for doing so is well established.

Thus, the absence of a dedicated independent regulator for the electricity sector affects more than the perceptions of investment risk, as it also hinders the passing of reforms that Kuwait has historically identified as necessary. Strengthening the country’s regulatory architecture should therefore be treated as a precondition for broader sectoral change. This, in turn, would support the legal and regulatory reforms needed to create an electricity sector more welcoming to foreign investment and project implementation.

Lack of Cross-Sector Coordination

Coupled with these dynamics, Kuwait’s energy system currently lacks a single authority capable of aligning policy across oil, gas, power, and climate. Kuwait’s government comprises more than 80 state agencies operating within the energy and environmental sectors, yet these sectors’ management and oversight remain dispersed across separate institutions that function individually rather than in a unified manner.[30]

For example, electricity and water services, including billing and tariff administration, sit within the Ministry of Electricity, Water, and Renewable Energy. Oil and gas strategy is managed through KPC and its subsidiaries. Climate and environmental oversight, meanwhile, falls to the Environment Public Authority, which serves as Kuwait’s primary agency on climate-related matters. Thus, without a single agency responsible for aligning policy goals and implementation, the result is a fragmented governance landscape in which decisions made in one part of the system could potentially conflict with priorities in another.

Given the scale of Kuwait’s energy agenda, with the transition framed as a $389 billion opportunity, the repeated emphasis on coordination in discussions of Kuwait’s future points toward the importance of establishing a cross-sector body to ensure consistency and transparency.[31] Government, the public sector, private investors, and international partners should be linked within a common implementation framework if the country’s ambitious energy investment plans are to be effectively realized.

Policy Recommendations

Kuwait’s energy policy challenges require a sequencing of action rather than a diagnosis. The core components of reform have been identified frequently across the government’s successive strategy cycles: increasing investment in expanded upstream oil capacity; introducing structured forms of external participation in energy projects; rationalizing domestic energy consumption; and diversifying power generation sources. The persistence of these recommendations alongside their limited delivery suggests that both policy design and government institutional frameworks are key target areas for reform.

Previous reform efforts have often implemented individual components of this agenda in isolation. However, in practice, these components are interdependent. Pricing reform is unsustainable without a regulatory body capable of setting, enforcing, and revising tariffs. Private sector participation depends on legal and contractual frameworks that Kuwait has not yet fully developed, and infrastructure expansion requires consistent, thorough cross-institutional coordination.

Historically, where these enabling conditions have been largely absent in Kuwait, reforms have also often been delayed, diluted, or reversed. The central policy task is therefore to establish a sequence of policy changes in which early interventions create the conditions necessary for subsequent reforms. The following policy recommendations should be implemented in such a sequence to improve institutional consistency and support the country’s energy policy objectives:

- Governance architecture updates: Establish a unified Ministry of Energy with a clear legal mandate to align oil, gas, electricity, and renewable policy within a single decision-making framework. This should be paired with the creation of an independent electricity regulator, either through a new institution or by converting the Ministry of Electricity, Water, and Renewable Energy into a regulatory authority. Together, these institutions would provide the governance architecture required to anchor tariff reform, support private sector participation, and sustain policy implementation across the nation’s entire energy landscape.

- Legal and contractual reforms: Develop a modern energy law to provide a clear statutory framework for the energy sector, alongside project-specific contractual mechanisms capable of accommodating external participation within constitutional limits. Where appropriate, key contracts could be ratified through the National Assembly, following its reinstatement, to provide further resilience to political oppositions. Procurement and project-execution rules should also be updated in parallel with the new law to more fully reflect the requirements of large-scale energy infrastructure.

- Domestic demand and tariff revisions: Introduce a phased approach to electricity pricing reform, beginning with smart-meter deployment, improved billing enforcement, and peak demand management. These measures should be combined with tiered tariffs and a targeted citizen-account mechanism to allow gradual increases in prices while managing potential political sensitivities. Reforms should focus on reshaping energy consumption incentives over time rather than attempting to enact immediate full cost recovery.

- Economic and energy diversification goals: Position diversification as an outcome of earlier reforms rather than a starting point. With clear, consistent governance structures established, legal frameworks strengthened, and domestic demand more effectively managed, Kuwait would be well positioned to support the expansion of gas, downstream, and related sectors. Additionally, creating a more predictable operating environment would improve the conditions for private sector participation and sustained investment across these areas.

Conclusion

Kuwait has produced several effective energy strategies, and many of the core priorities have remained consistent across its planning cycles. Yet progress on these plans has been mostly uneven, slowed by legal rigidity, weak continuity, and an institutional framework that has struggled to enact reforms across sectors. As this report demonstrates, the country’s institutional shortcomings, whether legal, regulatory, or political, are the primary drivers of this pattern.

Kuwait should prioritize strengthening the governance and institutional bodies that will oversee how its energy ambitions are implemented and regulated. If these foundations are established and if reforms are sequenced effectively, Kuwait would be better equipped to translate their policy ambitions into sustained delivery across its energy system and advance the fulfillment of Vision 2035, especially once the disruptions caused by the Iran war begin to dissipate.

Notes

[1] Middle East Energy Roundtable (MEER) workshop discussion held in Kuwait City in December 2025. MEER convenes workshops with a broad range of participants and discussion topics (“Middle East Energy Roundtable,” Rice University’s Baker Institute for Public Policy, https://www.bakerinstitute.org/middle-east-energy-roundtable). “Kuwait’s KPC Plans $9–10bn Annual Upstream Capex,” Middle East Economic Survey (MEES), December 12, 2025, https://archives.mees.com/issues/2140/articles/65197.

[2] Kuwait Petroleum Corporation, “A Sustainable Energy Future,” accessed June 2026, https://www.kpc.com.kw/Sustainability.

[3] “Gulf States’ Budgets Will Come Under Pressure,” Oxford Analytica, May 14, 2026; Jim Krane and Justin Alexander, “Losing Hormuz: The Costs of War for Gulf Oil Exporters,” Rice University’s Baker Institute for Public Policy, April 8, 2026, https://doi.org/10.25613/TKP5-JF69; and Alex Lawler, “OPEC Oil Output Hits New Low in April on Hormuz Export Disruption, Reuters Survey Finds,” Reuters, May 11, 2026, https://www.reuters.com/business/energy/opec-oil-output-hits-new-low-april-hormuz-export-disruption-reuters-survey-finds-2026-05-11/.

[4] Kuwait Const. art. 21 and 152 (1962), https://www.refworld.org/legal/legislation/natlegbod/1962/104436.

[5] “Law No. 6 of 1980 Establishing the Kuwait Petroleum Corporation,” International Energy Agency, July 22, 2022, https://www.iea.org/policies/12003-law-no-6-of-1980-establishing-the-kuwait-petroleum-corporation.

[6] Alex Mohammad Saleh, “Kuwait: Key Legal Developments in the Energy Sector,” Al Tamimi and Company, accessed June 2026, https://www.tamimi.com/law-update/the-energy-issue/articles/kuwait-key-legal-developments-in-the-energy-sector/.

[7] Agence France Presse, “Kuwaiti MPs Halt $8.5bn Oil Project,” Arab News, December 27, 2005, https://www.arabnews.com/node/277988.

[8] MEER workshop discussion.

[9] MEER workshop discussion.

[10] Stephen Whitfield, “Assessing Operational Readiness for Restart of Wafra Oil Field,” Journal of Petroleum Technology, January 28, 2020, https://jpt.spe.org/assessing-operational-readiness-restart-wafra-oil-field.

[11] Saleh.

[12] Saleh.

[13] “ACWA and Saudi Energy Sign $3bln PPA with SPPC for Rabigh 2 IPP Expansion,” Zawya, April 19, 2026, https://www.zawya.com/en/projects/utilities/acwa-and-saudi-energy-signs-3bln-ppa-with-sppc-for-rabigh-2-ipp-expansion-s4atp6go.

[14] U.S. Department of State, “2022 Investment Climate Statements: Kuwait,” accessed June 2026, https://www.state.gov/reports/2022-investment-climate-statements/kuwait.

[15] Saleh.

[16] Bloomberg, “Kuwait Appoints New Oil, Defence Ministers in Latest Cabinet,” Gulf Business, June 19, 2023, https://gulfbusiness.com/en/2023/kuwait/kuwait-appoints-new-oil-defence-ministers/; “Kuwaiti Emir Accepts Oil Minister’s Resignation, Appoints Finance Minister as Acting Oil Chief,” Xinhua, September 9, 2024; https://english.news.cn/20240909/0106b87bdd8c48fe86d4129a0fcc230c/c.html; and Yesar Al-Maleki, “Kuwait: New Oil Minister,” MEES, November 1, 2024, https://www.mees.com/2024/11/1/news-in-brief/kuwait-new-oil-minister/30a38410-985b-11ef-94a0-b580ec0503ce.

[17] Al-Maleki.

[18] Al-Maleki.

[19] Kuwait Const. art. 100 and 101.

[20] Luai Allarakia, “Legislative-Executive Paralysis in Kuwait,” PS: Political Science and Politics 58, no. 1 (January 2025): 115–8, 115, https://doi.org/10.1017/S1049096524000751.

[21] Allarakia, 117.

[22] Allarakia, 117.

[23] Courtney Freer, The Resilience of Parliamentary Politics in Kuwait: Rentierism, Ideology, and Mobilization (Oxford University Press, 2024), 23–5.

[24] Scott Weiner, “The Opposition’s Fight Against Austerity in Kuwait,” Carnegie Endowment for International Peace, March 9, 2017, https://carnegieendowment.org/sada/2017/03/the-oppositions-fight-against-austerity-in-kuwait.

[25] MEER workshop discussion; “KPC Mandates Retirement After 35 Years of Service for Oil Sector Officials, with Conditional Exceptions,” The Times Kuwait, August 1, 2025, https://timeskuwait.com/kpc-mandates-retirement-after-35-years-of-service-for-oil-sector-officials-with-conditional-exceptions/.

[26] “Kuwait Vision 2035 (New Kuwait),” Ministry of Foreign Affairs, State of Kuwait, accessed June 2026, https://www.mofa.gov.kw/en/pages/kuwait-vision-2035.

[27] Vivian Nereim, “Kuwaiti Emir Suspends Parliament, Citing Political Tumult,” New York Times, May 10, 2024, https://www.nytimes.com/2024/05/10/world/middleeast/kuwait-emir-parliament-suspension.html.

[28] Kuwait Institute for Scientific Research, Kuwait Energy Outlook: Sustaining Prosperity Through Energy Management, 2019, 33, https://www.kisr.edu.kw/media/filer_public/a7/d7/a7d7ecfa-242e-4c5f-a9bc-f971295b0a41/keo_report_english.pdf.

[29] Osamah Alsayegh et al., “The Distortionary Effects of Kuwait’s Cheap Electricity and the Case for a Just Reform,” Rice University’s Baker Institute for Public Policy, January 29, 2025, https://doi.org/10.25613/TR3Q-VQ96.

[30] MEER workshop discussion.

[31] “Kuwait’s Energy Transition — White Paper Executive Summary,” Kuwait Foundation for the Advancement of Sciences, 2023, https://www.kfas.org/Publications/Kuwaits-Energy-Transition---Executive-Summary.

This publication was produced by Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by outside experts prior to release. Any errors or omissions are solely the responsibility of the author(s).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.