Author(s)

Abstract

The Arab Gulf states have long relied on oil revenues to sustain their economies and labor markets, with expatriates forming a significant portion of the workforce. However, the global energy transition is expected to significantly alter the Gulf’s current economic structure by increasing alternative energy sources, intensifying hydrocarbon market competition, and limiting hydrocarbon fuel products’ demand. Thus, adapting to these economic shifts necessitates diversification efforts and labor market reforms.

This report examines the implications of the energy transition on the Gulf’s expatriate workforce, focusing on Kuwait as a case study. It examines the relationship between fluctuations in oil exports and expatriate labor dynamics, while highlighting the private sector’s reliance on the nonnational workforce and government tender projects.

Four potential labor market scenarios are analyzed. Under these scenarios, this report finds that Kuwait should consider the following to adapt sustainably to the energy transition: 1) restrict the dependence on foreign labor, where the country segments the private sector labor market, and 2) reserve certain professions for high-cost national labor and others for low-cost foreign labor. By reducing foreign labor, overall labor costs would increase. However, nationals would still retain some of the cost advantages from low-cost foreign labor.

If the private sector does not develop high-value, non-oil tradable products, Kuwait may ultimately shift toward the merging labor market model where national and nonnational workers would be integrated into a single labor market. In turn, this would likely reduce expatriate labor, public sector employment, and wages for nationals.

Introduction

The Arab Gulf states have long been synonymous with fossil fuel wealth. The discovery of oil in the mid-20th century, followed by a surge in revenues from the 1970s, marked a pivotal turning point in their economic trajectory. Oil revenues have served as the backbone of Gulf economies, funding infrastructure, social programs, public sector employment, and the foreign workforce. However, with increasing global pressure to reduce carbon emissions, the Gulf states now face a critical crossroads of balancing their historical dependence on oil with the urgent need to embrace a more diversified, resilient, and sustainable energy model. Recognizing the necessity of adapting to the global energy transition, these nations are motivated by economic diversification goals, climate commitments, and the long-term sustainability of their economies.[1]

Unlike the mainstream definition of the energy transition, which primarily advocates phasing out fossil fuels, the Gulf states have adopted an alternative approach.[2] Rather than discontinuing the production of fossil fuel resources, their strategy focuses on mitigating emissions by integrating clean technologies into the existing energy system and implementing energy demand-side management measures.[3]

Crucially, the interactions among hydrocarbon wealth, economic prosperity, and foreign labor have been a defining feature of Gulf economies. Their relatively small national populations and limited availability of skilled labor initially led the Gulf states to recruit workers from neighboring Arab countries.[4] However, as large-scale development projects expanded, the demand for labor soared, resulting in a diversification of the migrant workforce. By the mid-1980s, the composition of foreign workers had shifted significantly, with increasing numbers arriving from Asia, particularly Southeast Asia.[5]

Today, foreign labor is deeply embedded in the economic structures of the Gulf states, filling roles across various sectors, including construction, education, finance, health care, manufacturing, oil, power, and other high-skilled professions.[6] Despite ongoing workforce nationalization efforts, expatriates continue to constitute a significant portion of the labor market.[7] For nearly six decades, hydrocarbon revenues have been a primary driver of demographic shifts in the Gulf.[8]

This report examines the potential impact of the global energy transition, where declining demand for hydrocarbons may lead to decreases in Gulf states’ oil revenues, expatriate population, and overall economic performance. It explores how this transition could reshape the region’s population structure, particularly the balance between national and nonnational workers. Overall, the report assesses the extent to which Gulf economies can develop a quantitatively and qualitatively sufficient national workforce to meet their evolving labor market needs.

- Section 1 examines Gulf states’ demographics, labor markets, and nationalization policies.

- Section 2 analyzes the potential impacts of the global energy transition on the labor markets and economic sustainability, using Kuwait as a case study.

- Section 3 explores four possible future workforce structures in the Gulf, with a focus on Kuwait.

- Section 4 summarizes key findings and outlines potential implications for private sector reform to shift toward a sustainable, service-oriented economy that integrates more national workers and reduces reliance on expatriate labor.

1. Demographic Trends and Labor Market Structure

National and Nonnational Populations

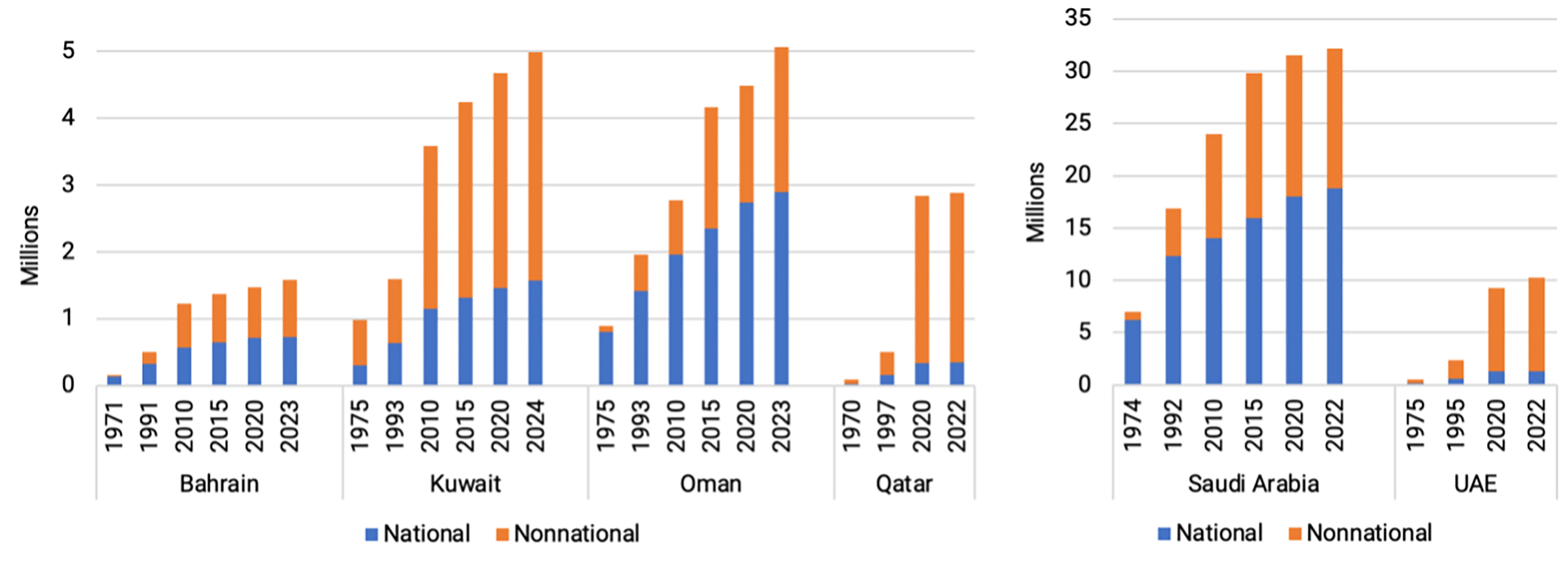

Driven primarily by oil revenues, one of the most significant transformations in the Gulf states has been rapid population growth since the early 1970s. In 1975, the region’s total population was approximately 10 million, with expatriates comprising around 2 million, or 20% of this total.[9] By 2023, the Gulf’s population had climbed to about 59 million, including 32 million expatriates.[10] Thus, the Gulf currently holds the world’s largest concentration of temporary migrant workers, equating to approximately 10% of migrant workers worldwide.[11]

The proportion of expatriates varies significantly across the Gulf states’ populations. In 2023, Qatar and the United Arab Emirates (UAE) had the highest expatriate populations, making up nearly 90% of their total residents, followed by Kuwait at around 70%. Bahrain had an expatriate share of 55%, while Oman and Saudi Arabia had the lowest proportions, with expatriates comprising about 40% of their populations (Figure 1).[12]

Figure 1 — Arab Gulf States’ Population Growth Profiles

The Arab Gulf states rely heavily on nonnationals to drive key economic sectors, reflecting their dependence on expatriate labor. Industries such as construction, hospitality, retail, and domestic services are extensively staffed by foreign workers, who often outnumber nationals in these fields.[13] Additionally, sectors such as health care, information technology, and finance also have a significant expatriate participation due to the demand for specialized expertise.[14] This reliance stems from rapid economic growth, limited local workforce availability, and policies favoring skilled migration programs.[15] As a result, nonnationals play a vital role in sustaining Gulf economies, shaping labor markets, and influencing demographic trends.

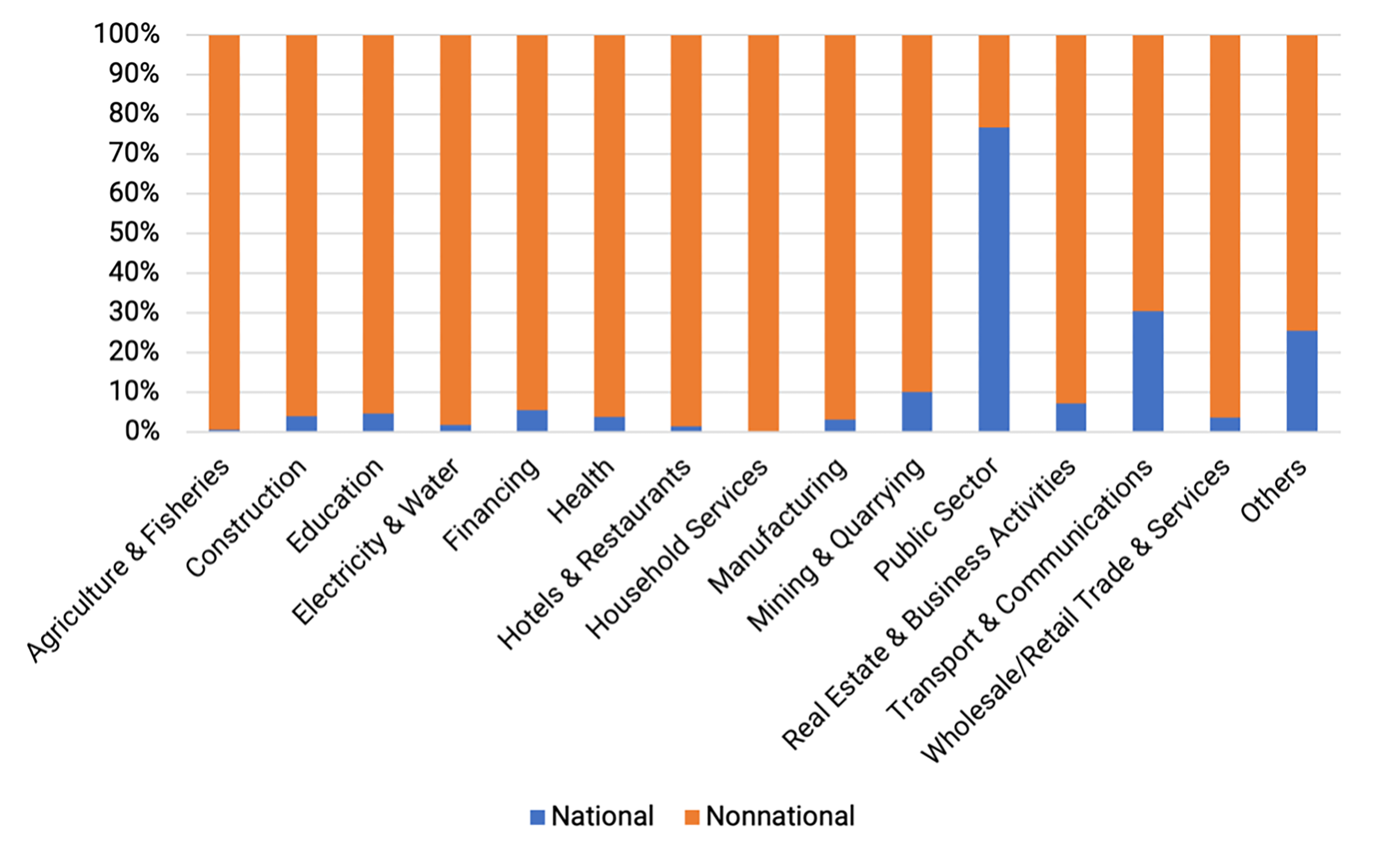

Using Kuwait as an example, its economic sectors are predominantly reliant on nonnational labor (Figure 2). Due to its financial strength, Kuwait, like other Gulf States, has the flexibility to import skilled labor as needed based on shifting economic priorities. Nonnational workers tend to be temporary residents with visas tied to their employment. Because of nonnational workers’ temporary status, Gulf governments could mitigate the potential impact of economic downturns, as they are not legally obligated to provide social welfare for expatriate workers.[16]

However, this dependence on lower-paid, highly productive foreign workers has hindered efforts to enhance national workforce productivity and skills. The prevalence of nonnational workers has also reduced the number of nationals employed by the private sector, as demonstrated in Kuwait’s case (Figure 2). To address these employment challenges, the Kuwaiti government has absorbed large numbers of nationals into the public sector, leading to significant fiscal strain. Kuwait’s 2024–25 fiscal year budget reveals that nearly 80% of government revenues are allocated to public sector salaries (Figure 2).[17]

Figure 2 — Composition of Kuwait’s Workforce by Sector and Nationality Status, 2024

Labor Nationalization Policies

As Gulf state governments aim to reduce their reliance on expatriates and create more employment opportunities for their national populations, labor nationalization policies have gained significant momentum. Several states have introduced policies that promote the hiring of nationals through employment quotas, as well as call for higher fees, increased taxes, and stricter visa regulations for the expatriate workforce.

For example, Bahrain has implemented a series of nationalization policies collectively known as “Bahrainization.”[18] In 2024, the Bahraini government established quotas to ensure a minimum percentage of Bahraini employees within private companies. The minimum percentage of Bahrainization quotas varies by sector and company size. These quotas are determined and enforced by Bahrain’s Labor Market Regulatory Authority (LMRA) and are periodically adjusted.[19]

Since the 1980s, Kuwait has adopted various strategies to promote “Kuwaitization.”[20] These include employment quotas requiring private companies to hire a specific percentage of Kuwaiti nationals, with quotas varying by industry to ensure national representation across the workforce. To encourage compliance with these nationalization goals, strategies include offering businesses financial incentives to hire Kuwaiti citizens. Furthermore, initiatives have been launched to enhance the skills of Kuwaiti nationals to align their qualifications with market needs and improve their employability across various sectors.

Despite these efforts, Kuwaitization faces challenges, particularly due to the public sector’s more attractive incentives for nationals, as it offers better salaries and job security. Additionally, some private sector employers are reluctant to hire nationals because of assumptions related to higher labor costs or mismatched skill sets, which contribute to the country’s ongoing dependence on expatriate labor.[21]

Oman’s nationalization initiative, known as “Omanization,” has been a cornerstone of the country’s economic strategy since 1999.[22] The government’s decisions to regulate non-Omani workforce recruitment include setting quotas for Omani workers in sectors such as fisheries, mining, and construction. The policies also oversee expatriate job transfers and outline conditions for hiring foreign labor in specific industries.[23] However, Omanization’s execution across the private sector has encountered difficulties. Some positions remain filled by expatriates due to lower wages offered by certain private companies compared to salaries in the public sector. Furthermore, a large portion of the Omani workforce is young and may lack the accumulated experience required for senior roles, resulting in the country’s continued reliance on foreign expertise.

In 2023, Qatar’s government cabinet approved a draft law aimed at increasing employment for Qatari nationals in various industries within the private sector. This law outlines that the government will determine which jobs within each sector will be nationalized by considering specific nationalization plans and target rates. It also proposes providing incentives, facilities, and privileges to private entities that comply with these nationalization rates, as well as offering financial incentives for Qatari workers employed in these sectors.[24]

With objectives to grow Saudi nationals’ employment rates in the private sector, Saudi Arabia’s nationalization policy, known as “Nitaqat,” sets specific quotas for companies to hire Saudi nationals, with requirements varying based on industry and firm size.[25] The government offers preferential treatment in government dealings, potential financial benefits, and other incentives to private companies that meet or exceed Saudization targets. Additionally, initiatives have been launched to equip Saudi nationals with the necessary skills to meet market demands, thereby enhancing their employability in various sectors.[26] However, like other Gulf states, Saudi Arabia’s nationalization initiative has not achieved its desired goals due to shortages of qualified national candidates for specific roles as well as its impact on business operations and overall economic efficiency, particularly in industries heavily reliant on expatriate expertise.[27]

Similarly, the UAE’s “Emiratization” efforts through its Absher program policy aim to support the employment of nationals in the private sector through job placement services, training, and partnerships with private companies.[28] However, the country has relatively less restrictive labor policies when compared to those of other Gulf states and continues to make efforts to attract skilled foreign talent.[29]

Notably, wages for expatriate workers in the Gulf are significantly lower than those of national workers, primarily due to policy distortions rather than market forces. Such policies contribute to an overpaid national workforce in public and private sector jobs.[30] A key challenge in replacing cost-efficient expatriate labor with relatively more expensive national workers lies in the productivity gap between the two groups, as expatriate workers often have a productivity advantage over nationals, especially in Saudi Arabia and Kuwait.[31]

As studies show, in well-functioning labor markets with minimal government policies focused on employment directives, higher workforce productivity tends to lead to higher wages.[32] However, in the Gulf, policies may result in high labor costs for less productive public sector jobs. Thus, the private sector, which seeks to hire less-productive local labor at lower wages, struggles to compete with the high salaries offered in the public sector.

2. Labor Market Implications of the Energy Transition

Economic Adaptations to the Energy Transition

Under its Announced Pledges Scenario, the International Energy Agency (IEA) projects global oil demand to decline from its current rate at approximately 103 million barrels per day (mb/d) to 55 mb/d by 2050.[33] In IEA’s Net Zero Emissions by 2050 Scenario, demand is expected to fall further to 24 mb/d.[34] Conversely, the U.S. Energy Information Administration (EIA) forecasts an increase in global oil production to 120 mb/d by 2050 under its Reference case, which aligns closely with estimates from the Organization of the Petroleum Exporting Countries (OPEC).[35]

Regardless of whether oil demand peaks, which is only one aspect of the energy transition, hydrocarbon-dependent economies should diversify its energy sources to remain resilient amid shifting global energy markets, geopolitical dynamics, and resource availability. This transition necessitates substantial governance reforms, with skilled labor playing a crucial role in fostering economic diversification. Furthermore, the population of citizens is likely growing faster than the availability of public sector jobs. Thus, expanding Gulf states’ non-oil sectors to generate sufficient employment opportunities is essential to support their economies, even in a world with increasing global oil demand.

Workforce dynamics under the energy transition are typically analyzed through job creation or the shift from fossil fuel industries to low-emission sectors.[36] Consequently, the energy transition’s impact on Arab Gulf states presents a unique challenge because their economies rely heavily on a predominantly nonnational workforce sustained by fossil fuel export revenues. As the transition progresses, a key question arises: Can the Gulf states sustain their large expatriate labor force while integrating more nationals into the public sector in an environment of reduced revenues? Furthermore, given their limited success in workforce nationalization over past decades, achieving this goal amid declining export revenues poses a significant challenge.

In accordance with the Solow growth model, a nation’s economic growth is driven by capital accumulation, labor development, and technological progress. In the case of the Gulf states, two of these factors — capital and labor — are largely influenced by oil export revenues.[37] While the extent of the energy transition’s impact may vary among Gulf states, the overall effect on its workforce will likely be similar, as illustrated by the Kuwait case study below.

Case Study of Kuwait

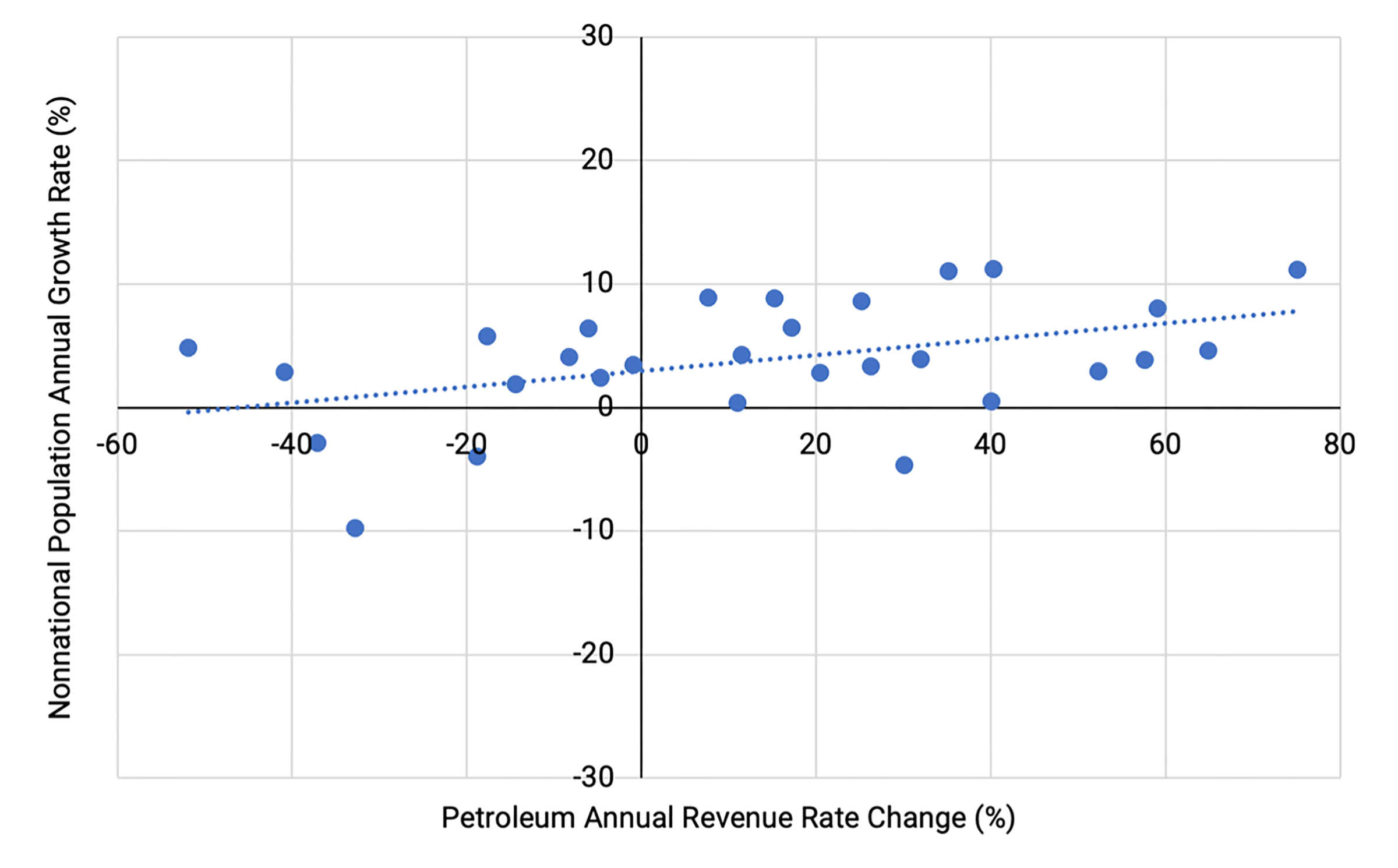

Using Kuwait as a case study, empirical data suggests a causal link between oil export revenue and the nonnational population, or ultimately the inflow or outflow of expatriate workers, as shown in Figure 3. The chart illustrates the annual percentage change in oil revenue alongside the annual percentage growth of the nonnational population. These findings suggest that the expatriate population level is affected a year later — equating to a one-year lag — by the oil revenue change. Notably, the non-oil sector or private sector, where nonnationals constitute most of the workforce, is highly dependent on oil revenues.

Figure 3 — Causal Relation of Kuwait’s Nonnational Population and Petroleum Revenue, 1993–2023

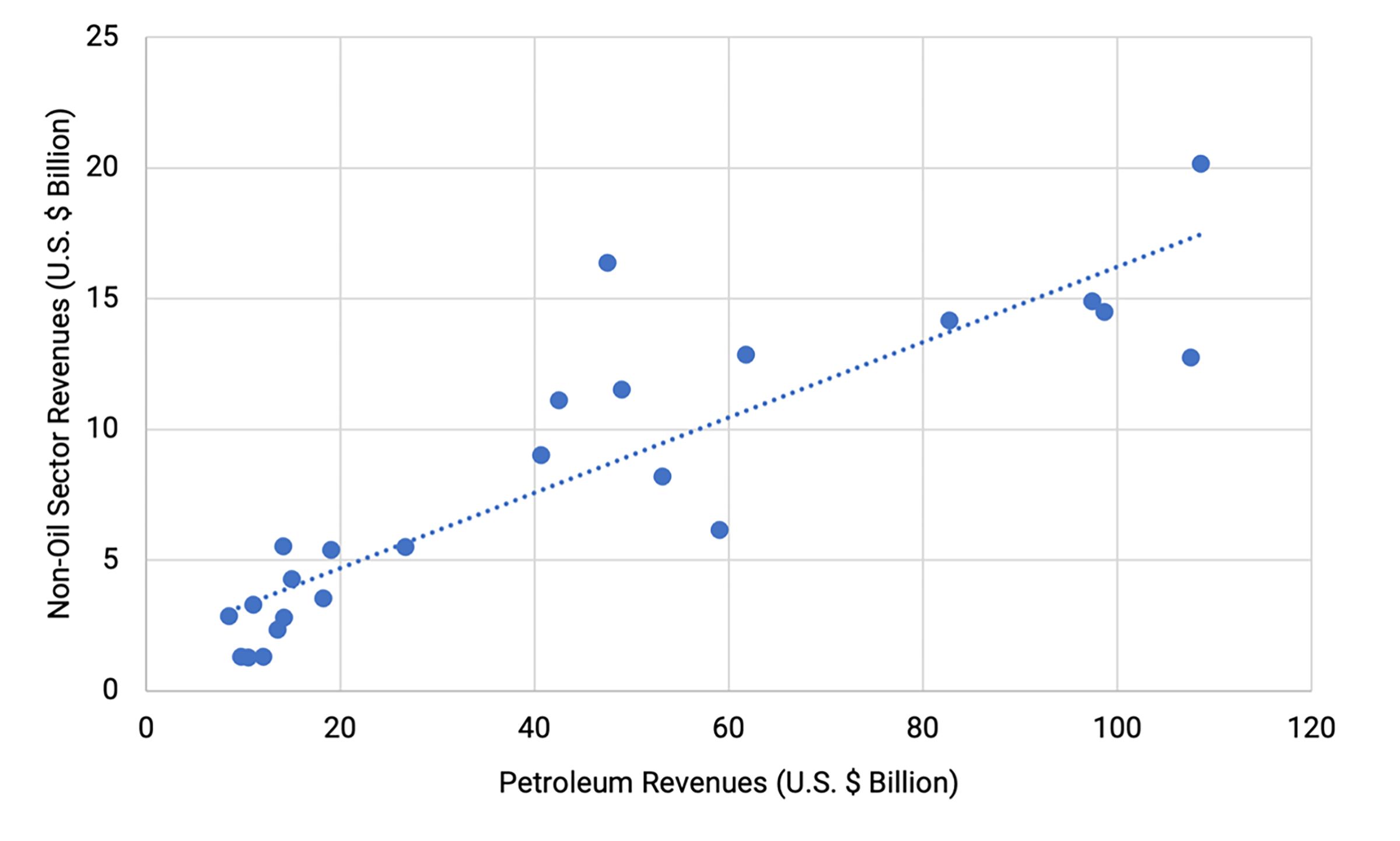

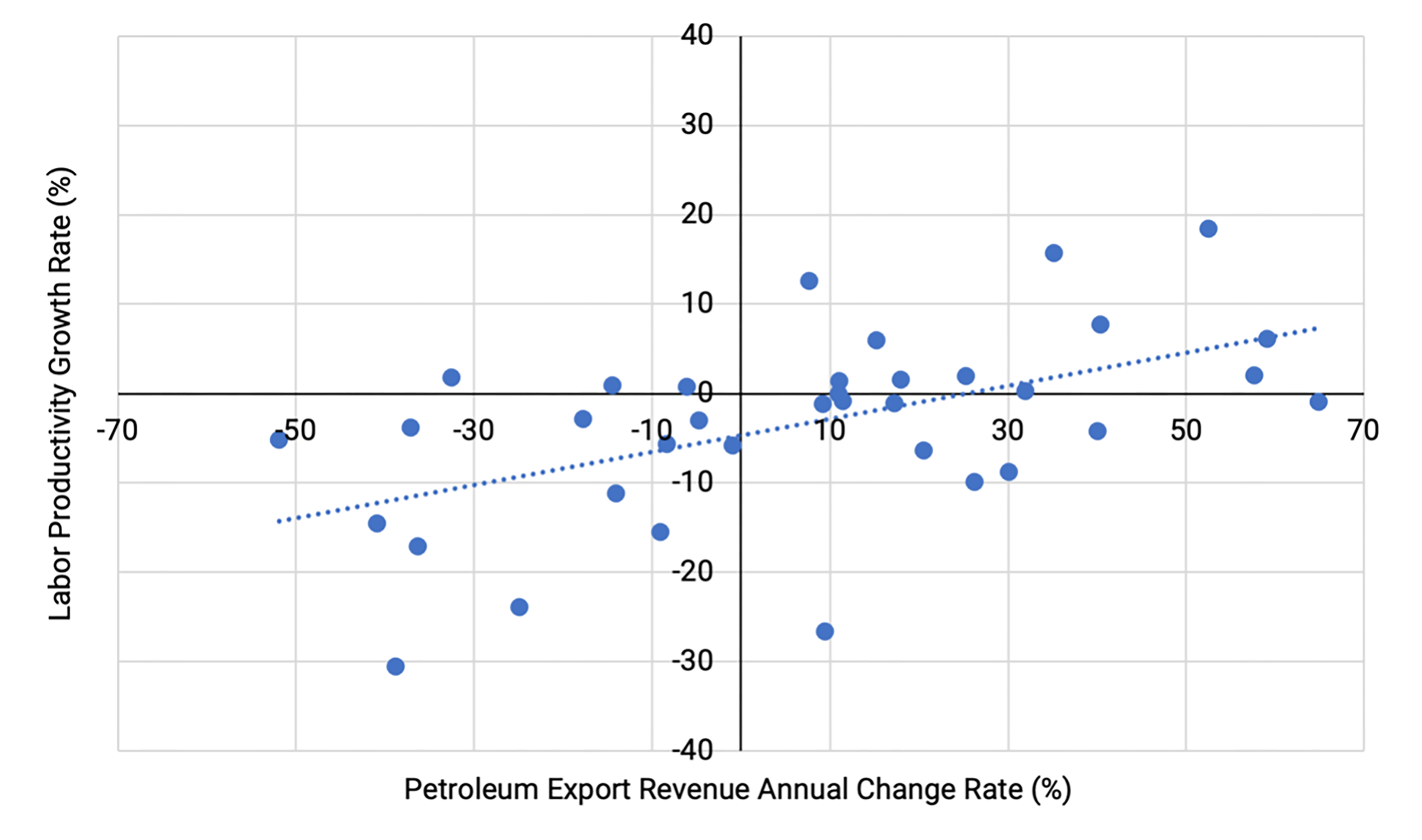

Accordingly, overall labor is influenced by oil revenue, as depicted in Figures 4 and 5.[38] These figures’ data suggests that the private sector lacks labor productivity due to its reliance on public funds, primarily through government tender projects. The labor productivity refers here to the production of tradable goods and services that generate revenues for the country, which are entirely independent of public funds and not reliant on oil export revenues.

Thus, the challenge extends beyond the dependence on oil revenue for importing expatriate labor, as it also encompasses a private sector that, even if it replaces expatriate workers with national labor, remains reliant on oil revenue. In the long run, declining oil revenues will lead to a contraction in both public and private sector outputs, and consequently, a reduction in the expatriate workforce.

Figure 4 — Causal Effect of Petroleum Export Revenues on Kuwait’s Non-Oil Sector Revenue, 1993–2023, With Lag Time of Five Years

Figure 5 — Causal Effect of Petroleum Export Revenues on Kuwait’s Labor Productivity, 1980–2018

For Kuwait’s current situation, the analysis estimates that a 1% change in annual petroleum export revenue would alter the nonnational population by 0.07% within a year (Figures 4 and 5). Additionally, an increase or decrease of $1 million U.S. dollars in petroleum export revenue is projected to raise or lower private sector revenue by US$0.15 million within five years. In summary, the decline in oil revenues results in a decrease in non-oil or private sector production, and eventually the decline of nonnational labor.

3. Potential Scenarios for Gulf Expatriate Workforce

As previously discussed, Gulf economies operate with two distinct labor markets: national workers, who are primarily employed in the public sector that is supported by oil revenues, and expatriate workers, who largely comprise the private sector that also receives contracts from the public sector. With the global energy transition’s effects — implementation of alternative energy sources, increased competition for oil market share from new producers, and mounting climate change-motivated actions — the Gulf labor market will be significantly affected.[39] The extent of workforce restructuring will vary across the Gulf states. Building on the four labor strategies explored by Michael Herb in his article, “Labor Markets and Economic Diversification in the Gulf Rentiers,” this report examines four potential outcome scenarios of the energy transition, with a specific focus on Kuwait’s labor market.[40]

Leveraging Expatriate Workforce (LEW)

In this scenario, the energy transition drives the import of a low-cost foreign workforce to support economic industries that generate tax revenue, which is then allocated to public sector jobs for nationals. This model has been implemented in Dubai, UAE, where economic diversification has significantly reduced reliance on the oil sector.

Historically, oil production accounted for 50% of Dubai’s GDP, but today it contributes less than 1% to its GDP due to resource depletion that urged a strategic shift toward other industries.[41] As a result, Dubai expanded private sectors, such as trade, tourism, aviation, real estate, and financial services, and established itself as a global business hub.[42] Maintaining this economic structure relies on a large influx of low-wage expatriate labor. The government taxes this diversified economy to fund public services and pay the salaries of the nationals who provide those services.

In Kuwait, although nonnationals comprise approximately 70% of the total population, the energy transition is unlikely to lead to adopting the Leveraging Expatriate Workforce (LEW) system for several interrelated reasons. First, the country’s abundant oil reserves and resulting rent continue to sustain a closed oligopoly as the dominant business model. Within this oligopolistic political economy, the most influential advantage that a private sector actor can have is membership in elite merchant families that dominate the business landscape, as Sophie Olver-Ellis notes.[43]

This entrenched system tends to position Kuwait as a closed, less favorable business environment. Its placement as the lowest among Gulf states in the World Bank’s Ease of Doing Business rankings reflects this perception, based on evaluations of regulatory environment, business operations, and procedures for permits and registrations.[44] Kuwait ranks 83rd out of 190 countries, significantly behind the UAE at 16th, Saudi Arabia at 62nd, Oman at 68th, and Qatar at 77th.

Merging Labor Markets (MLM)

In this scenario, the consequences of the energy transition push toward integrating national and nonnational labor markets without diminishing the role of foreign workers in the economy. Accordingly, public sector employment and wages are reduced for nationals.

Given Kuwait’s substantial oil wealth, lowering the standard of living for less skilled national workers to match the low wages of nonnational laborers is not a politically viable option. As a result, the country is unlikely to adopt the Merging Labor Markets (MLM) labor system in the foreseeable future. However, in the long term, factors such as a growing national population, global energy transition developments, and increasing fiscal constraints may ultimately necessitate limiting national employment in the public sector and reducing salaries.

National Labor Only (NLO)

This scenario would require a drastic reduction in nonnational labor, effectively forgoing a low-cost labor diversification strategy and compelling the economy to diversify by employing national labor. Given the inadequacy of national labor in both quantity and quality to sustain its economy amid the global energy transition, Kuwait is highly unlikely to adopt the National Labor Only (NLO) system. Such a shift would lead to a sharp economic decline, with the most significant impacts on construction, manufacturing, health, oil, and power sectors, which heavily rely on foreign labor.

A successful transition would require nationals to enlist in vocational jobs currently held by expatriates, a shift that has yet to materialize. According to a study by Ikhlas A. Abdalla and Moudi A. Al-Homoud, key obstacles to job nationalization can include cultural and political economy factors, such as disengaged work attitudes, reluctance to work long hours, shortage of soft skills, and a general disinclination toward vocational training.[45] Additionally, the private sector tends to perceive national workers as less deferential compared to expatriate labor.[46] Moreover, the non-oil sector, including the private sector, remains heavily reliant on state funding derived from oil revenues (Figures 4 and 5).

Restricting the Dependence on Foreign Labor (RDF)

In this scenario, the energy transition’s impacts push the country to segment the private sector labor market, reserving certain professions for high-cost national labor and others for low-cost foreign labor. This approach captures some of the benefits of the NLO system while mitigating its most significantly negative effects. By reducing foreign labor, overall labor costs increase. However, nationals still retain some of the cost advantages by benefiting from non-tradeable services provided by low-cost foreign labor.[47]

Kuwait’s current National Labor Support Program aims to increase national participation in the private sector by providing additional monthly financial support to nationals working in the private sector, with incentives ranging from US$1,860 to $2,915, depending on educational qualifications and job levels.[48] However, Kuwait has not successfully replaced expatriate labor for reasons previously discussed. In an energy transition scenario, where oil revenues decline per capita, the national population continues to grow, and the public sector becomes unable to absorb more national workers, the government is likely to intensify pressure on the private sector to apply a system similar to the Restricting the Dependence on Foreign Labor (RDF) scenario.

Findings

In sum, among the four scenarios analyzed, RDF appears to be the most probable labor system. LEW and MLM are ineffective due to economic and political constraints, while NLO is highly unlikely given the skills and workforce size gaps among nationals. When considering Kuwait’s current conditions, RDF aligns with its economic and labor market realities by gradually reducing reliance on expatriate labor without disrupting key industries.

As oil revenues per capita decline and demographic pressures grow, Kuwait will likely implement policies that promote structured labor segmentation while maintaining economic stability and social cohesion. However, if the private sector, particularly large and medium enterprises, does not significantly diversify away from government tender projects, manufacturing, and product exports, Kuwait may ultimately be closer to incorporating the MLM system as a long-term strategy.

4. Conclusion and Policy Implications

The global energy transition is a multifaceted process that affects technological, economic, social, and geopolitical developments. This report investigates the transition’s effects on economic and social aspects specifically related to the workforce structure in the Arab Gulf states with a focus on Kuwait.

Unlike other regions, the Gulf’s economies rely heavily on foreign labor, with expatriates comprising a significant portion of the workforce in the private sector, and nationals often being primarily employed by the public sector, which tends to offer generous benefits. This labor structure has been built, supported, and maintained by Gulf states’ hydrocarbon export revenues since the 1970s. In Kuwait, empirical data suggests that a 1% fluctuation in annual petroleum export revenue leads to a 0.07% direct change in the nonnational population within a year. Since expatriates are largely employed by the private sector, a rise or drop of US$1 million in petroleum export revenue is projected to increase or decrease private sector revenue by US$0.15 million within five years.

With the global energy transition, the current economic structure in the Gulf is likely unsustainable. Additionally, the impact of the transition could accelerate negative socioeconomic consequences unless comprehensive economic reforms are implemented to diversify Gulf economies, with the partial exception of Dubai in the UAE, Bharain, and Oman to some extent.

In Kuwait’s case, a national vision has been adopted to transform the country into a regional and international financial and trade hub.[49] Leveraging its strategic geographic location, Kuwait’s vision emphasizes the development of logistical infrastructure, including the expansion of seaports and airports, as well as the construction of a railway network connecting Gulf countries. If accomplished, the growth of the financial, commercial, and logistics sectors could play a key role in employing more national labor and, thus, alleviating pressure on public sector employment.

Given the four workforce structure scenarios as discussed in the previous section, the RDF labor model appears to be the most beneficial, long-term labor system for Kuwait’s economy and other similar Gulf state economic structures. Under this model, economic adaptations to the energy transition would lead to a segmented private sector labor market, reserving certain professions for high-cost national labor while others remain open to low-cost foreign workers.

However, if the private sector does not compete effectively, diversify beyond government tender projects, and secure international trade agreements that position Kuwait within major trade corridors — such as the India-Middle East-Europe Economic Corridor, China’s Belt and Road Initiative, or other emerging trade and logistics routes — the country may ultimately shift toward a MLM model. Under this model, national and expatriate workers would be integrated into a unified labor market, marking a significant departure from the current dual labor structure.

Unlike nations with economies driven by industry and manufacturing, the Arab Gulf states’ economies rely on hydrocarbon export revenues, potentially leading to limitations in both the quantity and quality of national workforce capacities due to the energy transition’s impacts. As a result, their economic diversification strategies are unlikely to center on the production of tradable goods.

Instead, the most viable path toward adapting to the energy transition and sustaining Gulf state economies likely rests on developing high-value, non-oil tradable service sectors that can generate strong productivity gains and positive spillover effects, thereby expanding and stabilizing their revenue base. Among these, the logistics sector, which supports global commercial and financial activities, presents particularly strong potential.

Notes

[1] Antonio Sanfilippo et al., “Energy Transition Strategies in the Gulf Cooperation Council Countries,” Energy Strategy Reviews 55 (September 2024): 101512, https://doi.org/10.1016/j.esr.2024.101512.

[2] International Energy Agency (IEA), Net Zero by 2050: A Roadmap for the Global Energy Sector, October 2021, https://www.iea.org/reports/net-zero-by-2050; Osamah Alsayegh, “The Arab Gulf Helps Fuel the Global Economy. What It Means for the Energy Transition,” Rice University’s Baker Institute for Public Policy, October 12, 2023, https://doi.org/10.25613/P469-G689.

[3] Alsayegh.

[4] Williams Jason Essomba, “Labor Immigration into the Gulf: Policies and Impacts,” Kuwait Program, Sciences Po, 2017, https://www.sciencespo.fr/kuwait-program/wp-content/uploads/2018/05/KSP_Paper_Award_Fall_2017_Williams_Jason_Essomba.pdf.

[5] J.S. Birks et al., “Labour Migration in the Arab Gulf States: Patterns, Trends and Prospects,” International Migration 26, no. 3 (1988): 267–86, https://doi.org/10.1111/j.1468-2435.1988.tb00649.x.

[6] Zahabia S. Gupta et al., “Expat Exodus Adds to Gulf Region’s Economic Diversification Challenges,” S&P Global, February 15, 2021, https://www.spglobal.com/ratings/en/research/articles/210215-expat-exodus-adds-to-gulf-region-s-economic-diversification-challenges-11800970.

[7] Huda Alsahi, “COVID-19 and the Intensification of the GCC Workforce Nationalization Policies,” Arab Reform Initiative, November 10, 2020, https://www.arab-reform.net/publication/covid-19-and-the-intensification-of-the-gcc-workforce-nationalization-policies/.

[8] Jon B. Alterman, “A New Revolution in the Middle East,” Center for Strategic and Internaional Studies, August 9, 2021, https://www.csis.org/analysis/new-revolution-middle-east; Chloe Cornish, “Learning to Live with 50C Temperatures,” Financial Times, August 24, 2024, https://www.ft.com/content/d5a5bc1f-e225-4397-b99f-56c62b00366d.

[9] Gulf Research Center (GRC), “Gulf Labor Markets, Migration, and Population (GLMM) Programme: Demographic and Economic Module,” accessed March 2025, https://gulfmigration.grc.net/glmm-database/demographic-and-economic-module/.

[10] GRC.

[11] Yoel Guzansky, “The Future Job Market in the Gulf States: The Challenge of Migrant Workers,” The Institute for National Security Studies, April 2021, https://www.inss.org.il/strategic_assessment/the-future-job-market-in-the-gulf-states-the-challenge-of-migrant-workers/.

[12] GRC.

[13] Udaya R. Wagle, “Labor Migration, Remittances, and the Economy in the Gulf Cooperation Council Region,” Comparative Migration Studies 12 (June 2024): 30, https://doi.org/10.1186/s40878-024-00390-3.

[14] Wagle.

[15] Abdul E. Erumban and Abbas Al-Mejren, “Expatriate Jobs and Productivity: Evidence from Two GCC Economies,” Structural Change and Economic Dynamics 71 (December 2024): 248–60, https://doi.org/10.1016/j.strueco.2024.07.007.

[16] Gupta et al.

[17] Ministry of Finance, “Summary of 25/24 Budget,” State of Kuwait, 2024, https://www.mof.gov.kw/MofBudget/PDF/BudgetPresentation25-24Eng-1.pdf; Public Authority for Civil Information, State of Kuwait, 2024, http://www.paci.gov.kw/stat/SubCategory.aspx?ID=3.

[18] Fragomen, “Bahrain: Draft Law Amending Bahrainization Policies Currently Under Review,” September 9, 2024, https://www.fragomen.com/insights/bahrain-draft-law-amending-bahrainization-policies-currently-under-review.html.

[19] Labor Market Regulatory Authority, “Bahrainization Target Rate and Minimum and Maximum Number of Foreign Workers by Economic Activity and Size of Economic Unit,” https://www.lmra.gov.bh/files/cms/shared/bahrainization-table-english8-10-2024.pdf.

[20] Passant Hisham, “Kuwaitization Policy Aims for Change, but Workforce Gap Remains a Concern,” Kuwait Times, December 10, 2024, https://kuwaittimes.com/article/22118/kuwait/other-news/kuwaitization-policy-aims-for-change-but-workforce-gap-remains-a-concern/.

[21] Mohamed Ihsan Ajwad et al., Towards a National Jobs Strategy in Kuwait, World Bank Group, 2022, https://hdl.handle.net/10986/38120.

[22] Economic and Social Commission for Western Asia (UNESCWA), “Omanization,” U.N., accessed May 2025, https://archive.unescwa.org/omanization.

[23] UNESCWA, “Ministerial Decision 115/2020 Governing the Recruitment of Non-Omani Manpower in Private Sector Establishments Operating in Cleaning Services,” March 12, 2020, https://migrationpolicy.unescwa.org/index.php/node/3743.

[24] Qatar News Agency, “Cabinet Approves Draft Law on Nationalising Jobs in Private Sector,” Gulf Times, February 8, 2023, https://www.gulf-times.com/article/655107/qatar/cabinet-approves-draft-law-on-nationalising-jobs-in-private-sector.

[25] Ministry of Human Resources and Social Development (MHRSD), “Nitaqat Mutawar Program,” Kingdom of Saudi Arabia, May 17, 2024, https://www.hrsd.gov.sa/en/knowledge-centre/decisions-and-regulations/regulation-and-procedures/832742.

[26] MHRSD.

[27] Vivian Nereim, “Saudi Businesses Are Struggling to Hire Saudi Workers,” Bloomberg News, September 19, 2018, https://www.bloomberg.com/news/articles/2018-09-19/jobs-for-saudis-plan-tests-retailers-used-to-cheap-foreign-labor.

[28] Ministry of Human Resorces and Emaritization (MOHRE), “Absher,” Government of United Arab Emirates, January 10, 2025, https://www.mohre.gov.ae/en/services/absher/about-absher.

[29] Gupta et al.

[30] Erumban and Al-Mejren.

[31] Erumban and Al-Mejren.

[32] Economic Policy Institute, “The Productivity — Pay Gap,” last modified May 15, 2025, https://www.epi.org/productivity-pay-gap/?utm_source; Edward Lazear et al., “Productivity and Wages: What Was the Productivity-Wage Link in the Digital Revolution of the Past, and What Might Occur in the AI Revolution of the Future?,” National Bureau of Economic Research, Working Paper 30734 (December 2022), https://www.nber.org/papers/w30734.

[33] IEA, The Oil and Gas Industry in Net Zero Transitions, November 2023, 19, https://iea.blob.core.windows.net/assets/f065ae5e-94ed-4fcb-8f17-8ceffde8bdd2/TheOilandGasIndustryinNetZeroTransitions.pdf.

[34] IEA, The Oil and Gas Industry in Net Zero Transitions, 19.

[35] Energy Information Administration (EIA), “EIA Projections Indicate Global Energy Consumption Increases Through 2050, Outpacing Efficiency Gains and Driving Continued Emissions Growth,” press release, October 11, 2023, https://www.eia.gov/pressroom/releases/press542.php; Organization of the Petroleum Exporting Countries (OPEC), World Oil Outlook 2045, 2023, https://www.opec.org/assets/assetdb/woo-2023.pdf.

[36] International Renewable Energy Agency (IRENA), Renewable Energy and Jobs: Annual Review 2023, September 2023, https://www.irena.org/Publications/2023/Sep/Renewable-energy-and-jobs-Annual-review-2023; Gordon H. Hanson, “Local Labor Market Impacts of the Energy Transition: Prospect and Policies,” National Bureau of Economic Research, Working Paper 30871 (January 2023), https://www.nber.org/papers/w30871.

[37] Panayotis G. Michaelides, “The Solow Growth Model,” in 21 Equations that Shaped the World Economy, Palgrave Macmillan, 2024, 185–97, https://doi.org/10.1007/978-3-031-76140-9_16.

[38] OPEC, Annual Statistical Bulletin 2024, 2024, https://publications.opec.org/asb; World Bank, “Kuwait,” accessed March 2025, https://data.worldbank.org/country/kuwait.

[39] EIA, “Petroleum Liquids Supply Growth Driven by Non-OPEC+ Countries in 2025 and 2026,” February 13, 2025, https://www.eia.gov/todayinenergy/detail.php?id=64565.

[40] Michael Herb, “Labor Markets and Economic Diversification in the Gulf Rentiers,” in The Politics of Rentier States in the Gulf, Project on Middle East Political Science, January 2019, 8–12, https://bit.ly/43rjS4Z.

[41] Matthew A. Winkler, “Dubai’s the Very Model of a Modern Mideast Economy,” Bloomberg, January 17, 2018, https://www.bloomberg.com/professional/insights/markets/dubais-model-modern-mideast-economy/.

[42] Sneha Abraham, “Oil Sector Takes a Smaller Role in Dubai,” Middle East Business Intellegence, April 20, 2015, https://www.meed.com/oil-sector-takes-a-smaller-role-in-dubai/.

[43] Sophie Olver-Ellis, “Building the New Kuwait: Vision 2035 and the Challenge of Diversification,” LSE Middle East Centre Paper Series 30, Kuwait Programme, January 2020, 7–9, https://eprints.lse.ac.uk/103198/1/Olver_Ellis_building_the_new_Kuwait_published.pdf.

[44] World Bank, “Ease of Doing Business Rankings,” accessed March 2025, https://archive.doingbusiness.org/en/rankings.

[45] Ikhlas A. Abdalla and Moudi A. Al-Homoud, “Foreign Faces in Kuwaiti Places: The Challenges of Human Capital Utilization in Kuwait,” International Journal of Business and Managment 7, no. 20 (2012): 1–12, 6, https://doi.org/10.5539/ijbm.v7n20p1.

[46] Abdalla and Al-Homoud, 6.

[47] Herb.

[48] Public Authority of Man Power, “Categories of Social Allowance Disbursement for National Workers in the Private Sector,” State of Kuwait, October 2022, https://www.manpower.gov.kw/media/CategoriesOfSocialAllowances.pdf.

[49] Ministry of Foreign Affairs, “Kuwait Vision 2035: ‘New Kuwait,’” State of Kuwait, accessed April 2025, https://www.mofa.gov.kw/en/pages/kuwait-vision-2035.

This publication was produced on behalf of Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by external experts prior to its release. Any errors are the responsibility of the author(s) alone.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.