Executive Summary

Twelve years of data show that the Affordable Care Act’s health insurance marketplace (marketplace) has helped significantly reduce the number of uninsured Texans. State and federal policy changes have helped more people in Texas obtain affordable health insurance coverage in the last four years. In 2025, policymakers have the opportunity to continue helping Texans. This brief discusses the state and federal policy changes that accelerated the growth in Texas enrollment and identifies the risks and opportunities to this trend.

Introduction

One of the primary goals of the Affordable Care Act (ACA) was to increase access to affordable health insurance for Americans. When the ACA was enacted in 2010, Texas had the highest uninsured rate (23.7%) in the country — 5.6 million people. The Texas Health and Human Services Commission (HHSC) estimated that full implementation of the ACA could cut the uninsured rate in half, with 36% (2 million people) gaining subsidized health insurance coverage through the ACA marketplace and 24% (1.3 million people) gaining coverage through Medicaid expansion.

Although Texas did not expand Medicaid coverage, the ACA marketplace has benefited Texans by enabling nearly 4 million people to obtain affordable coverage not otherwise available in the state. State and federal policy changes in the last four years have further reduced the cost of health insurance for Texans, more than doubling the number of enrollees from 2021 to 2025. This remarkable growth in coverage has helped reduce the rate of uninsured Texans from 23.7% in 2010 to 17.4% in 2023.

Policy Changes Boosted Coverage and Lowered Uninsured Rates

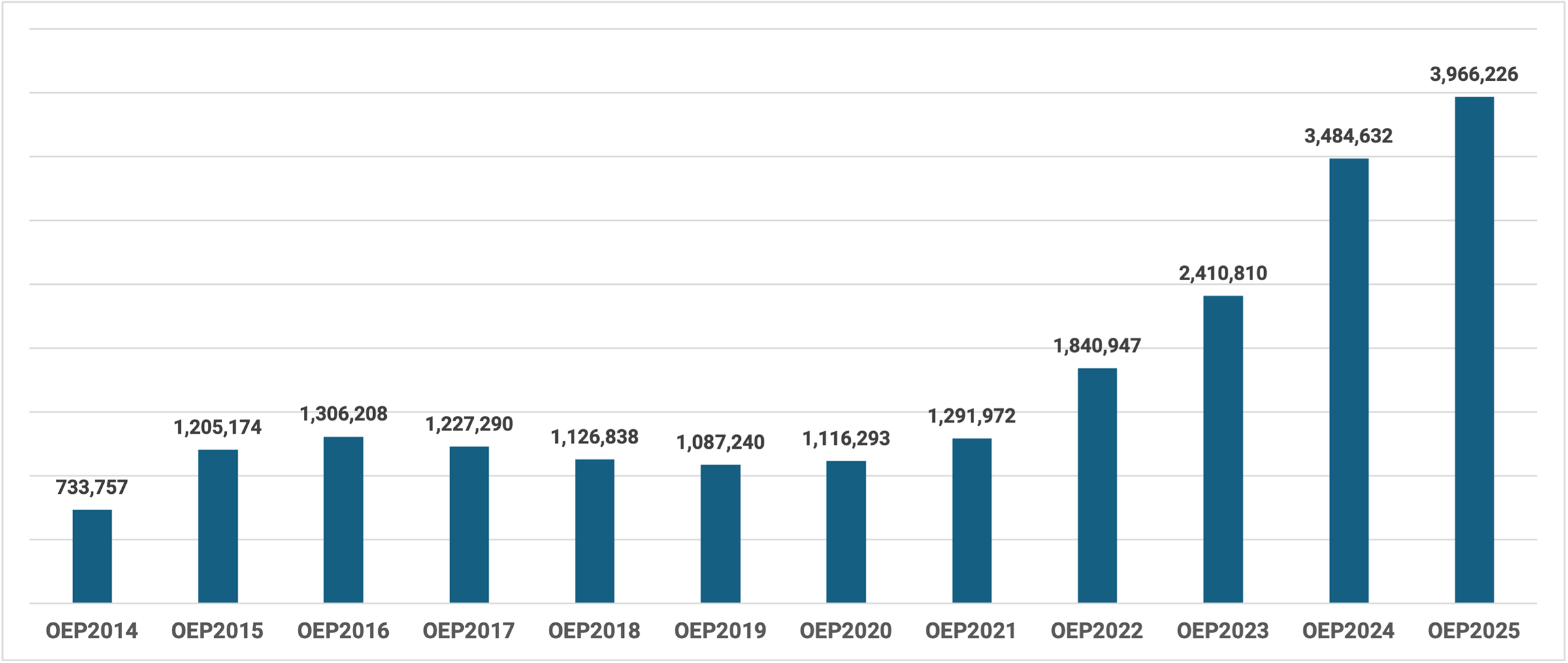

Toward the end of each year, the marketplace holds an annual open enrollment period (OEP) to enable individuals — typically those who do not have health insurance through their job, Medicare, Medicaid, or another source — to select and purchase health insurance plans. Figure 1 shows the number of Texas who enrolled in marketplace plans from 2014–25. As the chart shows, Texas enrollment increased more than five-fold over the 12 OEPs.

Figure 1 — Number of Texas Enrollees, Open Enrollment Period 2014–25

The most significant increase in enrollment occurred between the 2021 and 2025 OEPs, when Texas and U.S. policy changes were adopted that made plans more affordable:

- 2021: Enhanced premium tax credits — a federal policy change.

- 2021: Aligning state-approved premiums with federal subsidies — a state policy change.

- 2022: Fixing the “family glitch” — a federal policy change.

The following sections outline the key policy changes that drove this enrollment growth.

Enhanced Premium Tax Credits

Originally, the marketplace provided premium tax credits, or reductions in premium costs, that limited the amount paid by those with household incomes up to 400% of the federal poverty level (FPL). Individuals with income below 138% of the FPL paid no more than 2% of their income toward premiums and those with incomes between 300% and 400% FPL paid no more than 9.83%. In March 2021, Congress passed the American Rescue Plan Act (ARPA), which enhanced the premium tax credits by increasing the amount available to all purchasers. Under ARPA, those with incomes below 150% FPL were able to purchase a plan with no premium. Those with incomes between 150% to 300% were able to obtain a plan with premiums between 2% and 6% of their income. And those with higher incomes were able to obtain a plan by paying no more than 8.5% of their income. ARPA also opened a special enrollment period that enabled people to purchase plans immediately, rather than having to wait until the next OEP. In 2022, Congress passed the Inflation Reduction Act which extended the enhanced subsidies through 2025.

Aligning State-Approved Premiums with Federal Subsidies

After years of overlooking the potential benefits of the ACA, in 2021 the Texas Legislature passed SB 1296, which took effect for the 2023 OEP. This bill directed the Texas Department of Insurance (TDI) to conduct rate reviews of ACA marketplace plans to maximize the value of premium tax credits available to Texans. The rate review resulted in the reduction in premiums charged by health insurance companies offering marketplace plans, which in turn reduced the costs of plans to purchasers, enabling more to obtain a plan with no premium and some to obtain a plan with more coverage at lower prices. TDI is considering an update to its application of SB 1296, which may further increase benefits and reduce costs.

Fixing the ‘Family Glitch’

Originally, the ACA enabled people whose employers offered health insurance to receive a premium tax credit in the marketplace only if the employer’s plan was not deemed “affordable” — meaning the employee contribution was no more than 9.5% of household income. The affordability test was interpreted in a way that did not consider the cost of covering an employee’s family members, only the cost for the employee. As a result, full family coverage that far exceeded 9.5% of family income was still classified as affordable — this was often referred to as the “family glitch.” This left an estimated 5 million, mostly low-income, Americans uninsured. In 2022, the IRS updated its interpretation of “affordability,” stating that employer coverage was considered to be affordable if full family coverage did not exceed 9.5% of income. The new interpretation became effective for the 2023 OEP, enabling more people to access affordable marketplace plans.

These three policy changes are likely key factors in the growth of Texas marketplace enrollment, from 1.29 million in OEP 2021 to 3.96 million in OEP 2025 (see Figure 1) — a 206% increase.

Policy Recommendations

1. Congress should extend the enhanced premium tax credits beyond their scheduled expiry at the end of 2025.

The enhanced premium tax credits provided subsidies of $1.5 billion to 3.4 million Texans in 2024, amounting to 16% of total subsidy dollars across the U.S. Although the exact number of Texans who would have foregone health insurance without the enhanced subsidies is not known, the dramatic rise in marketplace purchases by Texans clearly coincides with the enhanced tax credits. KFF estimates that without the enhanced tax credits, Texans would experience health insurance premium increases in 2026 of 115%. The Urban Institute projects that 4 million Americans will lose coverage if the enhancements expire, with a 27% increase in the uninsured rate among Texans. Lower-income people are more likely to be impacted by the loss of enhanced credits. While the costs to the federal government of the enhancements is not insignificant, the impact of withdrawing the enhancements will increase the uninsured rate. While Republicans now talk about reforming rather than repealing the ACA, both the Republican Study Committee and the House Budget Committee have released plans that would allow the enhanced tax credits to expire.

Key Takeaway: Policymakers should reconsider this part of their health reform plans to ensure that millions of Americans do not lose affordable health insurance coverage.

2. Congress and the Texas Legislature should fund outreach plans to inform Americans about available health insurance options.

National Issues

Purchasing health insurance in the ACA marketplace can be overwhelming for consumers. Many communities have dozens of plans on offer each year, with varying premiums, co-pays, deductibles, provider networks, and level of coverage. For this reason, the ACA requires that the marketplace establish and fund knowledgeable, impartial navigators to help consumers understand their options and select the best plan for them. Navigators usually work for community-based organizations that know and are trusted by their communities.

A snapshot of Texas figures may reflect the availability of navigator funding: Marketplace health insurance enrollment in Texas increased year over year until OEP 2018, when the navigator funding was cut by 40%. Enrollment then remained at or near 1.2 million people until OEP 2022, when navigator funding was restored (and the enhanced tax credits were in place), leading to a surge in enrollment to 1.8 million Texans.

During the first Trump administration, the amount of funding for navigators was reduced from $63 million in 2016 to $36 million in 2017, and ultimately to $10 million in 2018–20. In 2024, $100 million was awarded to 44 navigator agencies across the U.S., but on Jan. 20, President Trump issued an executive order rescinding the previous administration’s order that had increased navigator funding. This may signal an intent to reduce that funding again in advance of the 2026 OEP.

National Takeaway: The new Trump administration should reevaluate this decision and Congress should enact legislation to ensure substantial funding for marketplace navigators, to help more eligible individuals and their families find the right health insurance plans.

Texas Issues

Research on the uninsured population in Texas in 2023 revealed that 47% of the uninsured were eligible for subsidized health insurance plans in the marketplace, while an additional 15% became eligible through the enhanced premium tax credits. Based on focus groups, the researchers concluded that many of the uninsured were unaware of marketplace plans that were low-cost, or, in some cases, free. The request by Texas HHSC for $300 million to upgrade its Medicaid enrollment system presents an opportunity to enhance marketplace enrollment as well by seamlessly linking systems.

Texas Takeaway: The Legislature should approve the funding requested by HHS and require that the improved Medicaid system facilitates access to ACA marketplace health insurance enrollment. This should include consumer education and assistance so that more eligible Texans can obtain marketplace plans. The state should also continue to look for opportunities to reduce costs for Texans through SB 1296.

Conclusion

Key policy measures have driven recent enrollment growth in the ACA’s health insurance marketplace and extending them will be crucial to maintain and expand affordable coverage for Texans. By renewing enhanced premium tax credits and investing in outreach efforts, policymakers can ensure continued access to health insurance for millions. The decisions made in 2025 will shape the future of health coverage in Texas, determining whether the progress achieved over the past decade is sustained or reversed.

This publication was produced on behalf of Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by external experts prior to its release. Any errors are the responsibility of the author(s) alone.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.