Author(s)

In roughly a month, the Organization of the Petroleum Exporting Countries (OPEC) will meet in Vienna for its 172nd ordinary meeting. But a new force that will influence the discussions is anything but ordinary: the rise of U.S. shale producers as global “event shapers.” The May 2017 OPEC meeting will be very different than the one in November 2014, when key oil exporters approached the table flush with cash—or, in the case of Russia, knowing that ruble devaluation could help ease the shock of a major price decline.1 Now, sentiments in OPEC capitals and Moscow are likely to have swung much further toward being willing to maintain production cuts in order to salvage their fiscal health.

Most large Middle East fields and Russia’s core fields in West Siberia can produce oil at a lower economic cost than can U.S. shale plays—a point most recently raised by Russian Energy Minister Alexander Novak and previously highlighted by various OPEC officials.2 Yet the “we are structurally lower-cost producers” view misses the most relevant strategic issue: a growing group of highly efficient U.S. shale operators now appears able to maintain production—and even expand it—at oil prices that likely are unsustainably low for many major exporters’ national budgets.

Multiple U.S. unconventional producers have leveraged a combination of service cost reductions, hedging, operational improvement, and technical innovation to dramatically lower their economic break-even costs in core plays. An important effect of this transformation is that the combined production of the Permian Basin, Eagle Ford Shale, Bakken Shale, and Niobrara Formation is now roughly equal to that of Iraq, the second-largest oil producer in OPEC, according to data from the U.S. Energy Information Administration and OPEC.

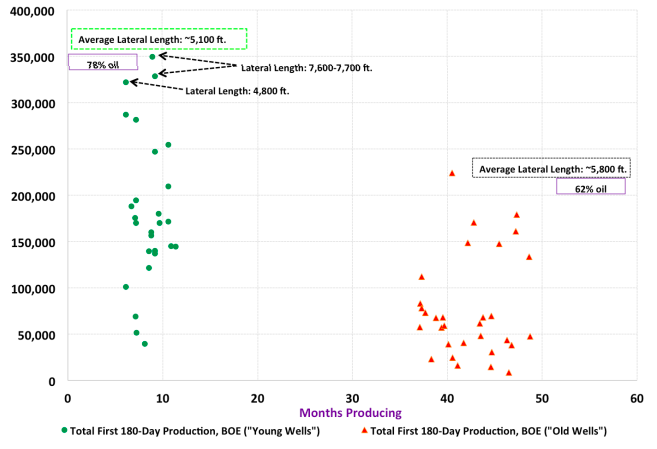

For an example of how this globally meaningful transformation has come to pass, consider the following snapshot from EOG Resources’ operations in Lea County, New Mexico, one of the 10 most actively drilled counties in the United States.3 The total sample of 202 wells analyzed show a trend of strongly increasing productivity with each year of successive completions, reflecting an evolution displayed at the company-wide level in EOG’s investor disclosures (Figure 1). EOG’s results show that top unconventional oil producers are steadily making their wells more productive.

Figure 1 — 180-day Initial Production Results for Selected EOG Resources Oil Wells in Lea County, NM4

Source New Mexico Oil Conservation Division; Baker Institute Center for Energy Studies.

Notably, EOG’s Lea County well productivity gains do not appear to have been fundamentally driven by longer laterals (i.e., physically larger wells). Generally speaking, laterals of the 2016-vintage wells are actually shorter than wells completed in the 2013 to 2014 timeframe. Yet both overall well productivity and oil as a proportion of total hydrocarbons produced have risen markedly.

Part of the volumetric production boost and higher oil content may be explained by “high grading”—i.e., drilling and completing wells on the richest geological sweet spots. Yet placing too much emphasis on high grading neglects the fact that operators almost always prioritize developing the best wells in their drillable inventory at a given time. The incentives to do so with unconventional wells are especially strong, since much of a well’s total production tends to occur early in its life.

As such, the more likely explanation for higher well productivity during the downturn comes from technical and operational improvements operators have been forced to make in order to survive.5 As noted in prior Center for Energy Studies research, a mounting body of evidence suggests that top operators are making structural improvements such as investments in water handling infrastructure, sand sourcing, pad drilling, and upsized frac completions that are likely to endure even if oil field service costs rise in the future.6

In other words, the top shale producers are month-by-month getting better at extracting more oil per dollar spent on capital expenditures (capex). Moreover, these volumetric recovery gains are fundamentally rooted in process and technology improvements that are likely to endure even if service costs rise as activity picks up. Equally important, knowledge will likely disseminate across operators over time. Innovations by skilled engineers, geologists, data scientists, and smart field personnel at larger technical leaders such as Anadarko Petroleum Corp., Apache Corp., Concho Resources Inc., Continental Resources, Devon Energy, EOG, Pioneer Natural Resources, and others will eventually be transmitted across firms and drive incremental, sector-wide productivity gains.

An additional important development is that many of the largest multinational oil producers such as BP, Chevron, ConocoPhillips, ExxonMobil, Occidental Petroleum, and Shell are now boosting their focus on unconventional resources.7 This shift marries deep balance sheets, large inventories of drillable locations, and a newcomer advantage that potentially enables these companies to immediately utilize years of horizontal drilling knowledge accumulated by multiple operators and service companies. Indeed, Occidental Petroleum reports that it has now identified nearly 12,000 horizontal drilling locations on its Permian Basin acreage and that it anticipates growing its total Permian hydrocarbons production, which is liquids oriented, at a 20% compound annual growth rate from 2017 through 2019.8

The inexorable process of iterative improvement in the U.S. oil patch, supported by rising capital deployment, should be deeply disturbing to policymakers in OPEC and Russia. OPEC is locked in a high-stakes competition with the shale drillers at least until global oil demand picks up sufficiently to accommodate growth in shale and Middle East production. Indeed, the ongoing OPEC production curbs may, on the margins, actually be reinforcing crude-on-crude competition, since Saudi Arabia is reducing output of its heavier oils and proportionally increasing exports of light, sweet crude—exactly the grade produced by U.S. unconventional producers.9

This competition is fundamentally an endurance race. And it is not a multidecade event, for which the numbers would be more on OPEC’s side. Rather, it is a short-term contest that boils down to a stark question: Can major OPEC producers, Russia, and other countries dependent on energy revenues handle 24 to 60 months of oil averaging $50 to $55/bbl and stave off financial pressures that could raise the prospect of major political concessions these predominantly autocratic governments would rather not make?

A. Many Key U.S. Light, Tight Oil Producers Can Now Operate Within Cash Flow at $50/BBL Oil

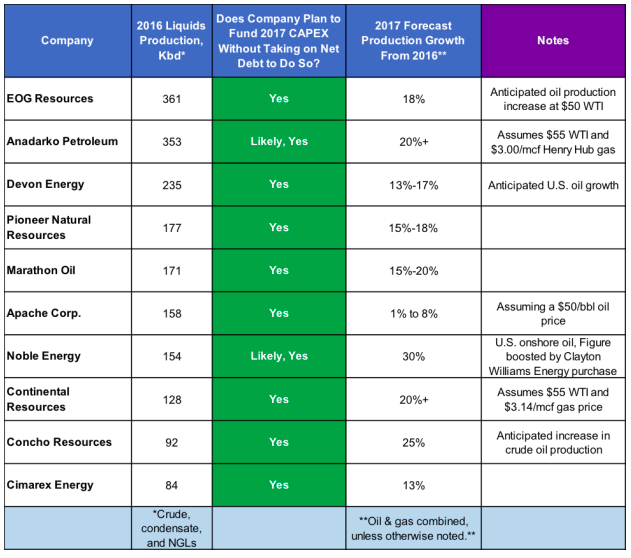

For much of the shale boom, critics have frequently pointed out that many companies could not operate without using debt to fund drilling. Yet after two years of right-sizing and cost reductions, at least 10 of the largest U.S. unconventional liquids producers now say they will be able to fund their capital expenditure programs in 2017 without taking on net debt (Figure 2). Many of them will be able to fund capex out of cash flow, while others will use a combination of cash flow, cash on hand, and cash from asset divestitures. Note that these 10 producers alone can pump 2 million bpd of total liquids.10

Figure 2 — Ten of the Largest U.S. Unconventional Liquids Producers Anticipate Being Able to Execute Capital Spending Programs Without Taking on Net Debt in 2017

B. Most Major Oil-exporting Countries Will Have to Either Run Significant Budget Deficits or Cut Spending

Shale producers adjust to lower commodity prices in large part by applying technology to become more efficient and reduce their costs for finding and extracting oil. In contrast, oil-exporting governments generally lower social break-even costs not by becoming “efficient,” but instead by reducing spending. This can be intensely problematic if budget constraints must be maintained for multiple years, because in many large oil-exporting countries, citizens have tolerated political autocracy in exchange for rulers’ willingness to provide oil-funded social benefits.11 Furthermore, oil revenues often also fund capable internal security services that act as praetorian guards for the ruling class. In the case of Russia, energy export revenues help purchase the loyalty of powerful siloviki political clans and also fund the military and security services.

Put bluntly, in many countries where 10% or more of GDP comes from energy rents, oil revenues (and gas revenues linked to oil prices) fundamentally underpin the social contract between rulers and the governed. Even weaker regimes can weather short periods of low prices, but a large, multiyear reduction in oil and gas revenues in such countries can erode the shock-absorbing capacity of adjustment mechanisms such as exchange rate devaluation and foreign exchange reserves.12

As shock absorbers lose their effectiveness, governments may increasingly face tough political choices that, if taken far enough, could force them to cede meaningful degrees of political power. Furthermore, low oil prices may create a financial challenge many OPEC countries have not faced for some time: speculative attacks on currencies. When oil was priced at $100/bbl, the idea of a speculative bet against various Gulf currencies likely would have gotten a trader booted from his portfolio manager's office. Another year of oil prices between $45 and $55/bbl and such ideas may no longer seem ridiculous. Indeed, by early 2016, at least two large hedge funds had already bet that Saudi Arabia will be forced to devalue the riyal, according to Bloomberg.13

These trades—while still very much in the minority and premised on a low-probability event—merit close attention, because as Southeast Asia countries learned in the late 1990s, once speculative momentum builds, currency pegs can rapidly become indefensible. This author suspects that Saudi Arabia would choose to defend its financial position by cutting oil production to boost prices, thereby avoiding any potential instability and political loss of face that could accompany a significant currency devaluation.

Key Oil Exporters’ Likely Strategic Response: Reduce Budget Spending and Maintain—or Maybe Deepen—Oil Production Cuts

Major oil producers’ policy responses to the current oil downturn are very different than those seen in the V-shaped 2008–09 oil price collapse. Within weeks of the initial oil price decline, OPEC began trimming production and by the end of 2008 had agreed to cuts that reduced total daily global oil supplies by nearly 5%.14 The results were substantial, with oil prices bottoming in February 2009 and nearly doubling by the end of that year.

The present oil price downturn—characterized by the moniker “lower for longer”—has played out differently, with key OPEC producers now engaging in structural internal reforms rather than simple adjustment of crude oil production volumes. Such policy responses suggest that decision-makers in key oil-exporting countries see a multi-year period of lower and more volatile prices ahead and are planning accordingly. The strategies fall into two primary categories. The first involves tactical measures. Certain major oil producers are turning to the debt markets to plug financial gaps. Saudi Arabia unleashed a $17.5 billion sovereign bond issue in October 2016, the largest emerging market debt issuance to date, while Qatar issued $9 billion of debt in May 2016.15

The second group of policy responses is potentially more transformational, but also involves greater political risks. Multiple Gulf countries are beginning to meaningfully reform their substantial subsidies for gasoline, diesel, natural gas, and water.16 Subsidy reforms mark a significant—and arguably, politically risky—departure from traditional policies, given that many citizens in these countries still expect oil-funded largesse. For instance, more than 90% of young Qataris, Omanis, and Bahrainis and 86% of young Saudis who responded to an April 2016 poll said subsidies should continue.17

In another high-impact move, Saudi Arabia now appears serious about privatizing part of Saudi Aramco. A Saudi Aramco share sale could bring several strategic benefits. In the immediate term, an influx of foreign investors to the Saudi stock market would increase demand for the riyal and, all else considered, help the kingdom maintain its peg to the U.S. dollar. In the medium term, a Saudi Aramco share listing would, in essence, also help the kingdom effectively monetize a portion of its oil reserves while they are still in the ground.18 Finally, a Saudi Aramco IPO would enable the country to inject a large chunk of capital into its Public Investment Fund (PIF), which Saudi leaders seek to make the world’s largest sovereign wealth fund, according to the kingdom’s Vision 2030 national development strategy document.19

Not all major oil exporters have the political capital to restructure social entitlements, or to reduce costs through other channels that might be even more politically risky. But all major oil exporters have a strong, singular focus at present: the need to sustain production cuts and drain global oil inventories by at least 250 million barrels, if not more. The trade-off math is clear: it is better to cut production by 2%, 5%, or even 10% and see prices sustainably rise by 20% than to resume a market share war where prices fall to a level at which no feasible amount of volume increase can generate the revenue a country needs to sustain its present political and economic structure. Expect OPEC members to maintain the current cuts at the group’s May meeting and maybe even deepen them.

Endnotes

1. For a detailed explanation of the ruble shock absorber, please see Mark Agerton, “Oil Price, Exchange Rates and the Convoluted Impact of Sanctions on Russia,” Forbes, April 27, 2015, https://www.forbes.com/sites/thebakersinstitute/2015/04/27/oil-price-exchange-rates-and-the-convoluted-impact-of-sanctions-on-russia/#2538b1c978adv.

2. “Россия не боится конкуренции с производителями сланцевой нефти” (“Russia is Not Afraid of Competition From Shale Oil”), Oilcapital.ru, March 27, 2017, http://m.oilcapital.ru/industry/297926.html.

3. The author compiled production data from the New Mexico Oil Conservation Division for EOG’s active oil wells that have been brought online in Lea County since 2011, a date by which drilling activity had (A) become intensively oriented toward seeking oil and liquids-rich wells and (B) become focused on horizontal wells completed with hydraulic fracturing.

4. The 180-day cumulative production count for a given well begins in the first month for which the company reported oil or gas production volumes greater than zero.

5. See, for instance, Erin Ailworth, “Fracking 2.0: Shale Drillers Pioneer New Ways to Profit in Era of Cheap Oil,” Wall Street Journal, March 30, 2017, https://www.wsj.com/articles/fracking-2-0-shale-drillers-pioneer-new-ways-to-profit-in-era-of-cheap-oil-1490894501.

6. Gabriel Collins and Kenneth B. Medlock, Assessing Shale Producers’ Ability to Scale-up Activity, Issue brief no. 01.17.17. Rice University’s Baker Institute for Public Policy, Houston, Texas, 2017, http://www.bakerinstitute.org/media/files/files/7bfea3e9/BI-Brief-011717-CES_ShaleScale.pdf.

7. One of the largest deals to date was ExxonMobil’s January 2017 purchase of the Bass family holdings, which more than doubled the company’s estimated Permian Basin reserve base. See “ExxonMobil to Acquire Companies Doubling Permian Basin Resource to 6 Billion Barrels,” ExxonMobil News Releases, January 17, 2017, http://news.exxonmobil.com/press-release/exxonmobil-acquire-companies-doubling-permian-basin-resource-6-billion-barrels.

8. “Oxy Permian Tour: Driving Value in the Permian,” Investor Presentation, March 10, 2017, http://www.oxy.com/investors/Documents/PermianBasin%20InvestorDayMarch2017.pdf.

9. Rania El Gamal, “Seeking higher revenues, Saudi sets out stall for light crude,” Reuters, April 4, 2017, http://www.reuters.com/article/us-opec-saudi-crude-idUSKBN17616H.

10. Based on 2016 annual report data, the precise crude oil number is somewhat difficult to ascertain due to differing production reporting formats between companies.

11. See, for instance: Jim Krane, “Guzzling in the Gulf,” Foreign Affairs, December 19, 2014, http://www.bakerinstitute.org/media/files/files/dfb15ed5/KRANE_Guzzling_in_the_Gulf_ FA_Dec2014.pdf; and Jim Krane, “The Political Economy of Subsidy Reform in the Persian Gulf Monarchies,” in The Economics and Political Economy of Energy Subsidies, ed. Jon Strand (Cambridge: MIT Press, 2016), https://mitpress.mit.edu/books/economics-and-political-economy-energy-subsidies.

12. For instance, Saudi foreign reserves declined by more than $200 billion between August 2014 and December 2016, a drop of more than 27%. If this “burn rate” continues, Saudi Arabia would exhaust its reserves by 2020, as the International Monetary Fund noted in fall 2015.

13. Katia Prozecanski, Simone Foxman, and Katherine Burton, “PointState Said to Bet Against Saudi Riyal After Oil Short,” Bloomberg, March 1, 2016, https://www.bloomberg.com/news/articles/2016-03-01/pointstate-is-said-to-bet-against-saudi-riyal-after-shorting-oil.

14. “151st (Extraordinary) Meeting of the OPEC Conference,” OPEC, December 17, 2008, http://www.opec.org/opec_web/en/945.htm; “Oil Market Report,” International Energy Agency, October 10, 2008, https://www.iea.org/media/omrreports/fullissues/2008-10-10.pdf.

15. Elaine Moore and Simeon Kerr, “Saudi Arabia’s $17.5bn bond sale has lessons for debt market,” FT, October 20, 2016, https://www.ft.com/content/92158e52-95f4-11e6-a80e-bcd69f323a8b.

16. Jim Krane and Shih Yu (Elsie) Hung, “Energy Subsidy Reform in the Persian Gulf: The End of the Big Oil Giveaway,” Issue Brief no. 04.28.16., Rice University’s Baker Institute for Public Policy, Houston, Texas, 2016, http://www.bakerinstitute.org/research/persian-gulf-energy-subsidy-reform/.

17. Vivian Nereim, “Young Arabs Wedded to State Largess Pose Test for Gulf Leaders,” Bloomberg, April 12, 2016, https://www.bloomberg.com/news/articles/2016-04-12/young-arabs-wedded-to-state-largess-pose-test-for-gulf-leaders. Nereim cites ASDA’A Burson-Marsteller’s survey of 3,500 young people in 16 Arab countries.

18. If the kingdom can satisfactorily clarify taxation policies, much of the Saudi Aramco shares’ valuation premium would derive from investors’ expectations of future oil production that comes at a lower cost, and with less geological risk, than most other large-scale global crude oil sources.

19. “Vision 2030,” kingdom of Saudi Arabia, http://vision2030.gov.sa/en.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.