Author(s)

To access the full working paper, download the PDF on the left-hand sidebar.

The Permian Challenge

The Permian Basin underlies West Texas and Southeastern New Mexico, covering an area larger than the state of South Dakota. New drilling and completion techniques have broken the Permian’s decades-long output decline, and the region now produces more oil per day than every OPEC member country aside from Saudi Arabia and Iraq. Intense oilfield activity has made communities in the basin such as Carlsbad, New Mexico, along with Midland/Odessa, Pecos, and Monahans Texas into boomtowns. Complex policy challenges are arising as “full speed ahead” resource development strains local infrastructure, including roads, schools, hospitals, housing, first responders, and others. These challenges will likely if WTI Midland realized crude oil prices remain between $55 and $65 per barrel on average over the next 3-5 years.

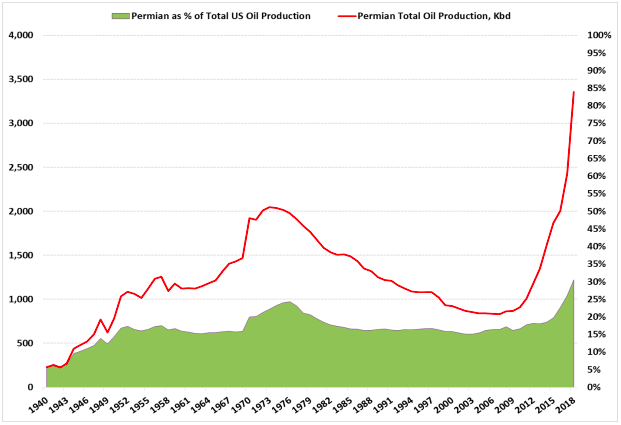

Volumetrically speaking, the Permian is in uncharted territory, as in 2018 it produced over 60% more oil than its prior historical oil production peak in 1973 and now accounts for roughly 1/3 of US oil production—itself an historical high (Figure 1). As of mid-2019, Permian oil output exceeded the maximum sustainable production capacity of Saudi Arabia’s supergiant Ghawar Field.1 Current production levels severely test the capacity and adaptability of both oilfield and community infrastructure. If community infrastructure fails to support the needs of local residents’ and E&P and oilfield service companies in the Basin, this could jeopardize the future growth prospects of the world’s largest single oil production center outside of the Middle East.

International oil & gas companies (aka “the Majors”) have a long and varied range of experience developing resources in challenging environments that initially lacked many types of supporting infrastructure. Yet the Permian generally poses a different set of challenges than Angola, Kazakhstan, Nigeria, Papua New Guinea, and other such locations. To name a few, companies are protected by rule of law, there are no armed rebel groups menacing drilling sites, local politicians generally seek to engage constructively with energy producers, there is a pre-existing pipeline network and array of service companies, and local populations have deep and robust institutional memory when it comes to the oil & gas industry.

But paradigmatic differences notwithstanding, Permian communities also face some concerns shared by their counterparts in resource-rich regions overseas; for instance, central and regional governments failing to share sufficient windfall revenues to help the producing areas offset the burden of the boom and ensure community infrastructure is sufficient to support continued robust, competitively-priced resource development. On these questions, certain Permian challenges often do correspond to themes in the broader global discourse on the “resource curse.”

Figure 1. Permian Basin Oil Production Since 1940, Annual Average (‘000 bpd)

This paper lays out and explains the core community infrastructure challenges created by the Permian oil boom, analyzes how the region’s energy producers are responding to them, and concludes by distilling the key policy lessons involved and offering suggestions on ways to fine-tune corporate engagement with local infrastructure, civil society, and political actors as Permian Basin oil & gas production remains large and continues to evolve.