In December 2017, President Donald Trump signed into the law the largest corporate tax reduction since the Tax Reform Act of 1986 passed under President Ronald Reagan. The Tax Cut and Jobs Act of 2017 (TCJA, Pub. L. 115–97) reduced the top marginal tax rate on corporate income from 35 percent to 21 percent, leading to extensive speculation on its anticipated effects.1

To project the long-term economic impact of the corporate tax cut, this issue brief presents the results of a dynamic model similar in nature to the macroeconomic models used by the Congressional Budget Office and Joint Committee on Taxation.2 The model shows a modest decline in wealth inequality due to the corporate tax cuts in the TCJA. While total wealth remains highly concentrated in the top quintile, there is a small shift toward each of the bottom four quintiles. Wages, household consumption, and corporate investment experience a modest increase, while total output remains unchanged.3

The economic variables most directly impacted by corporate tax cuts are average dividends issued and equity valuation, which increase more significantly. Total corporate tax revenue declines by about 40 percent, but nearly 20 percent of that decline is recaptured through increased personal income tax revenue.

An advantage of a dynamic model is its ability to capture behavioral changes corresponding to policy changes. The specific model used to evaluate policy in this brief simulates business decisions about hiring, investment, and dividend issuance, as well as household decisions about employment and stock ownership. Simulating these household and business decisions improves measurement of changes in key economic variables, including stock market valuation and wealth distribution.

The dynamic model is also able to capture changes in market quantities by adjusting prices until the corresponding market demand and supply reach parity. This is a critical feature of any model attempting to evaluate the effect of policy change on wages or interest rates. Because the model is entirely self-contained, every consequence of the policy reform is captured by the simulated economy.

To validate the model, several statistics are estimated from the model’s baseline economy and compared to their real-world counterparts. A close match between the model-generated and real-world values implies a satisfactory calibration of the model and establishes confidence in the model’s ability to evaluate policy reforms. The model’s baseline parameters are chosen to match current U.S. economic statistics, including firm-level values estimated from COMPUSTAT data, and household values estimated from the Survey of Consumer Finances (SCF) and derived from other studies.

The Model

Unlike most models quantifying the impact of the TCJA, this model simultaneously measures the long-run effects of tax reform on equity ownership and wealth inequality. Many models assume that the corporate income tax is simply a tax on capital. The model used here explicitly considers profits and decision-making around issuing dividends, and thus captures how tax rates can distort the choice between issuing higher dividends and investing in production.

Long-term Government Debt

Since 2000, federal government debt—both in absolute terms and as a share of the economy—has increased continuously, with acceleration in the last decade. This debt growth is not indefinitely sustainable, and the U.S. will eventually face difficult decisions that will likely require compromise on the part of all political stakeholders. Moderating debt growth and balancing the budget would require significant modification to the U.S. fiscal structure. The exact nature of any future changes will be determined by a political landscape yet to evolve.

What we do know for sure is that the TCJA permanently reduced the corporate tax rate. To that extent, this paper evaluates the tax reform while avoiding an assessment of how the budget is eventually balanced. In order to isolate the direct effects of the corporate tax reduction, the reform is evaluated on the premise that the government budget eventually reaches balance through a commensurate reduction in the government expenditures that minimally distorts economic outcomes. Further, the model assumes that the government maintains no debt in the long run.

Other Key Assumptions

It would be impossible to accurately represent all aspects of the U.S. economy; thus, the model—like all other simulations of this kind—includes some key assumptions that could affect how it measures the long-term impact of the TCJA:

• Long-term reform. Certain provisions of the TCJA are set to expire after a five-year window. While these provisions may have significant short- and medium-term consequences, these effects will eventually wash out in the long run. As a result, only the decline in the corporate tax rate is modeled.

• Closed economy. The model in this paper is a closed economy with no international factors influencing outcomes. Of course, in reality, the U.S. economy is influenced by international economic events, and foreign entities held 13.6 percent of U.S. equity in 2016.4 However, it is difficult to construct a model that takes international factors into account without making arbitrary assumptions.5

• No pass-through entities. This paper does not directly account for the effect of pass-through entities, such as Subchapter-S corporations that avoid corporate taxation altogether but depend on private investment rather than public issuance of equity. Omitting this factor is not likely to affect the results.6

• Taxation. Households in the model pay taxes directly only on labor and dividend income. The dividend tax rate is set to 20 percent, while the progressive personal income tax function is calibrated so that aggregate personal tax revenue (including dividend tax revenue) is roughly 9 percent of GDP. The baseline effective corporate tax rate is set to 20 percent and generates 5.8 percent of GDP, which is elevated compared to the 2 percent corporate tax share of GDP observed in recent decades.

Firms

Firms make decisions that maximize their current value, defined as their discounted stream of dividends. When the government reduces corporate tax rates, firms’ cash flows increase and they must choose how much of this new cash flow they will invest in production or distribute as dividends. Because prices change within the model, firms account for changes in wages, interest rates, the market valuation of their equity, and the price of their output.

Although the model does not directly account for aggregate risk, individual firms experience idiosyncratic risk corresponding to demand for their output. Each firm accounts for this risk, as well as market prices and government policy, and chooses employment and investment to maximize its value. By simulating these business decisions, the model captures a critical mechanism through which changes in the corporate tax rate affect key financial variables and the broader economy.

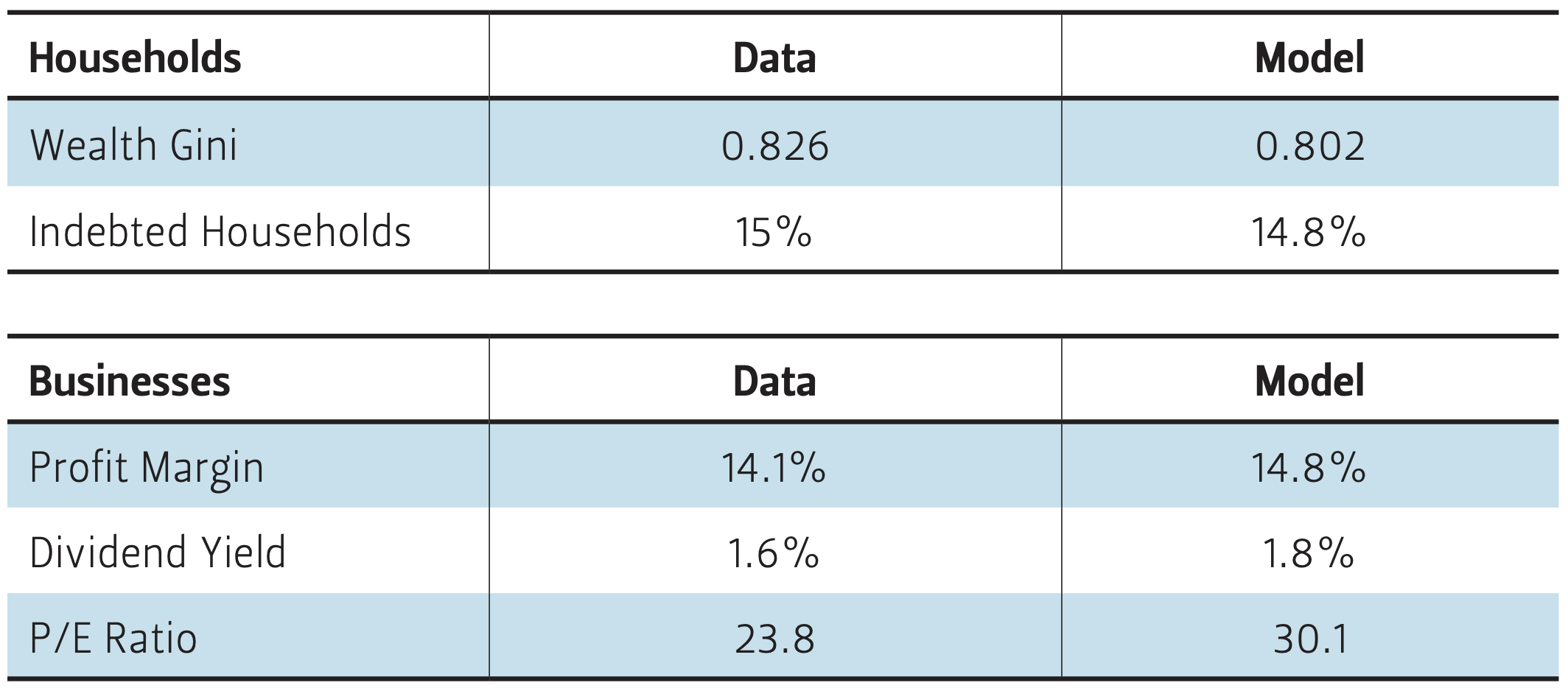

Table 1 — Survey Data and Benchmark Model Comparison

Firms’ profit margins, dividend yields, and price-to-earnings (P/E) ratios provide a comparable measure of the firms’ profits, dividends, and equity valuations. Each of these variables helps to capture how cash flows throughout a firm, beginning at the sale of its products, continuing through investment decisions, passing through the corporate tax levy, and finally ending up as dividend payments distributed to shareholders. Understanding this mechanism helps to trace the impact of a corporate tax change through corporate activity.

Table 2 — Wealth Quintiles: Data Versus Model

Households

Households in the model capture two critical behavioral distortions included in almost every dynamic macroeconomic model: responsiveness of saving and labor. Different financial circumstances experienced by households over time generate variability in household wealth. Households save to mitigate risk by holding a portfolio of equity shares that receive firms’ dividends. Households with a negative equity position are debtors. The magnitude of uncollateralized borrowing in the model is calibrated to match the percentage of individuals with negative net worth in the Federal Reserve Survey of Consumer Finances for 2016.7

Since wealth is accumulated by maintaining firms’ equity shares, it is the household variable most directly impacted by corporate tax reform. The wealth Gini coefficient (a measure of inequality), percentage of indebted households, and individual quintiles of wealth generated by the model are compared to the corresponding values from survey data for model validation in Tables 1 and 2. The wealth Gini coefficient from the data corresponds to an estimated weighted average within the time span from 2000-2015. It should be noted, however, that this value has been steadily rising over those years.

Measuring the Effects of TCJA Corporate Tax Reform

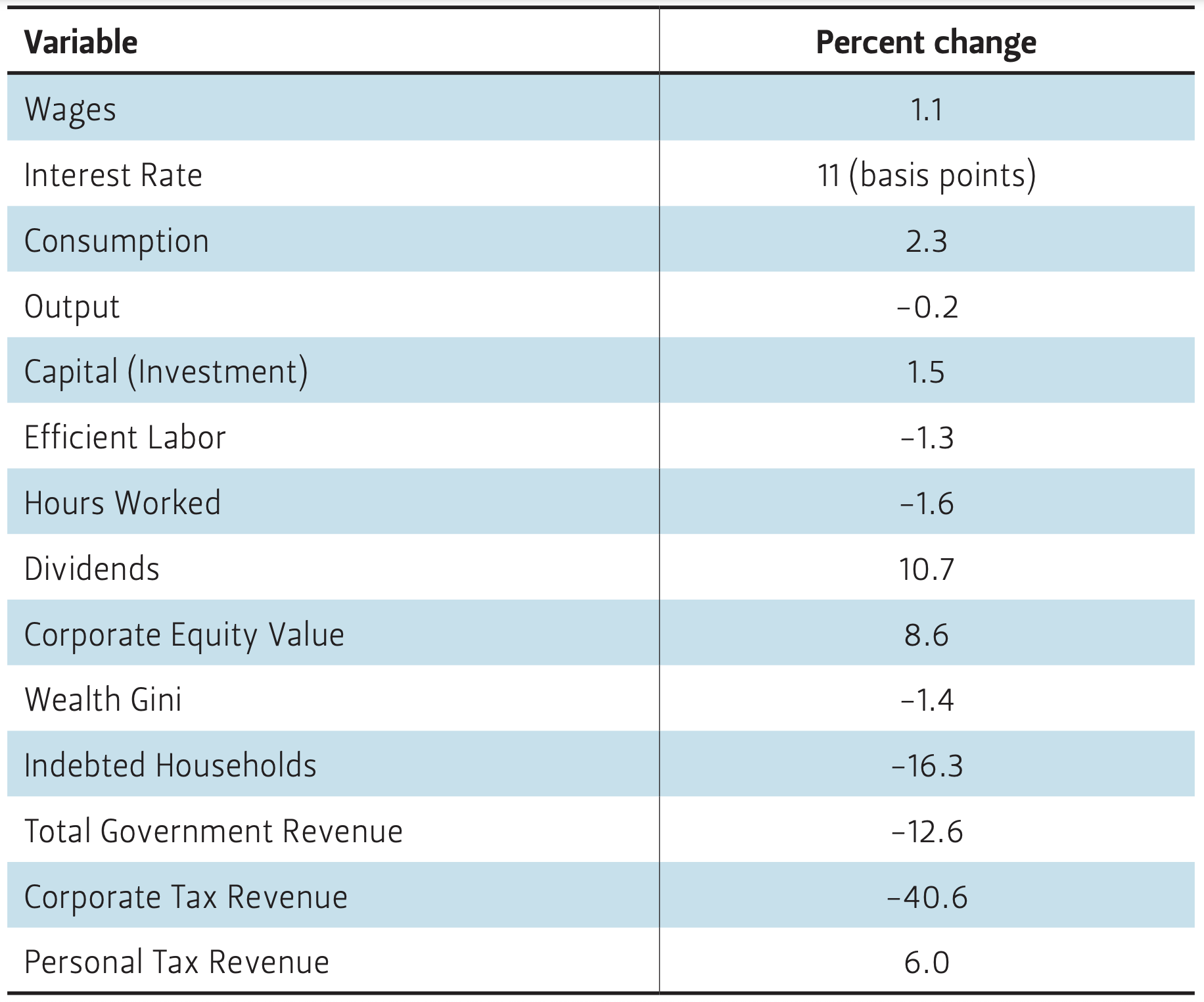

The TCJA reduced the top marginal corporate tax rate from 35 percent to 21 percent, reflecting a 40 percent decline in the rate. Since the marginal and effective tax rates are equal in the model, the corporate tax rate is reduced from 20 percent to 12 percent to reflect a proportional decline of 40 percent. The long-term impact of the simulated tax reform is summarized in Table 3. When the government reduces corporate income taxes, households receive higher dividends. Part of this increase in dividend income allows households to increase consumption, but it also allows members of those households to work less and maintain a quality standard of living. To accommodate this increased demand for consumption and compensate for the scarcity of labor, firms increase investment to accumulate capital.

Table 3 — Simulated Effects of the Corporate Tax Reduction on Key Variables

This decline in the availability of labor supply, coupled with an increase in labor demand, leads to higher market wages.

The implications of corporate tax reform on labor market outcomes depend on individuals’ preferences regarding consumption and leisure. In this model, an increase in private consumption of 2.3 percent, which approximately offsets the reduction in government expenditures, induces households to increase leisure time by reducing work hours by 1.6 percent. Consequently, the decline in work hours also reduces efficient labor by 1.3 percent. This decline in labor supply, together with increased labor demand drives up equilibrium wages by 1.1 percent.

Although capital increases by 1.5 percent, the greater impact of labor in the production process means that a decline in total labor of 1.3 percent slightly reduces total output. In a stable economy, the change in investment will equal the change in capital, since average investment is constantly just replacing depreciated capital. Higher demand for corporate equity shares slightly drives up the interest rate by 11 basis points, from 4.71 percent to 4.82 percent.

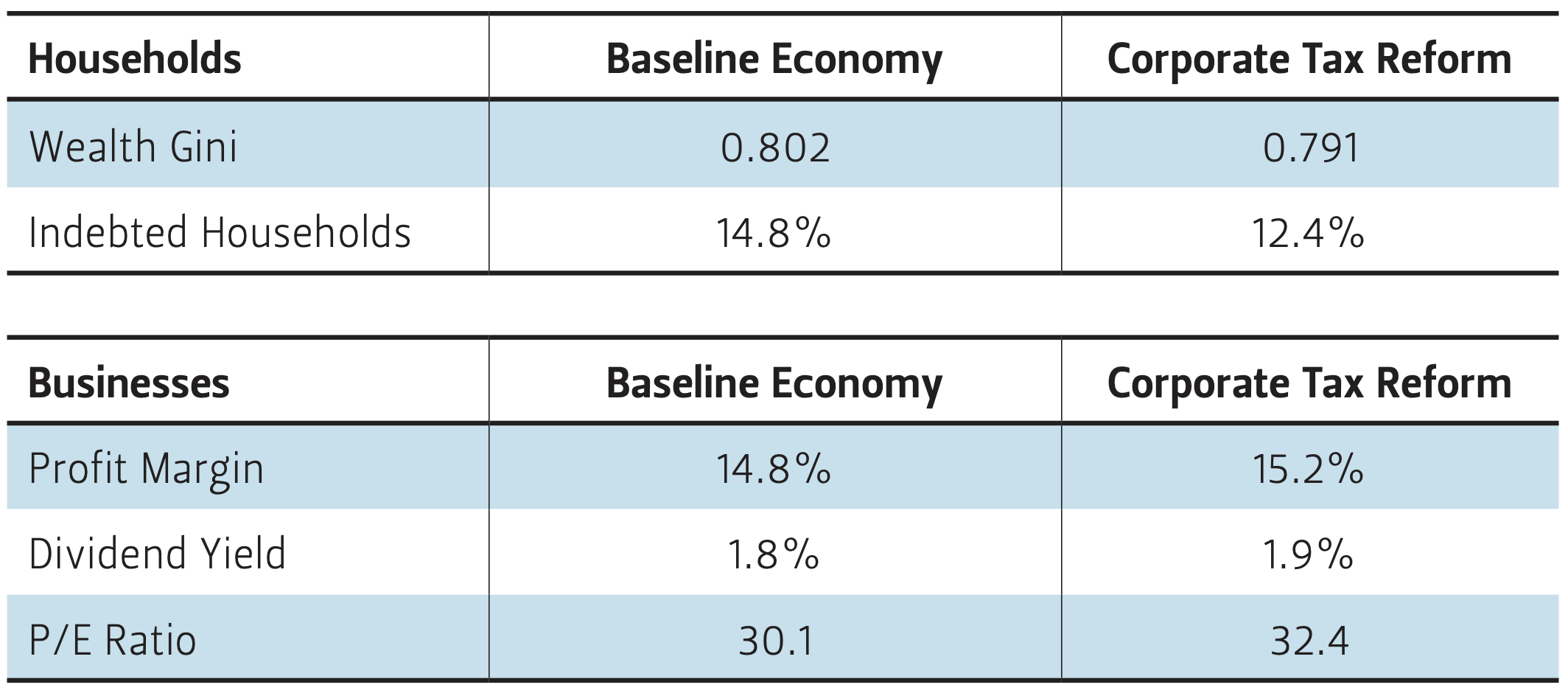

The largest impact of the corporate tax reform can be observed by the sharp increase in average dividend of 10.8 percent, which, in turn, drives up equity values by 8.6 percent. Because the interest rate increases (or, inversely, the firm’s discount factor declines), equity values fall relative to dividends, which partly explains why average dividends increase by more than average equity values. This effect increases the average dividend yield from 1.8 percent to 1.9 percent, while average profit margins and P/E ratios increase from 14.8 percent to 15.2 percent and 30.1 percent to 32.4 percent, respectively.

The decline in the corporate tax rate causes a roughly proportional decline in corporate tax revenue. Total revenue falls by 12.6 percent, which likely overstates the actual amount because of the high corporate tax revenue relative to output in the baseline model. This decline in total revenue reflects a 6.0 percent increase in personal income tax revenue, which recaptures 19.5 percent of the lost corporate tax revenue.

Perhaps one of the most surprising results of the model is the reduction in wealth inequality resulting from a reduction in the corporate income tax rate. The model shows an increase in the share of wealth held by the bottom 80 percent of the population, as well as a modest decline in the wealth Gini coefficient. Total indebted households decline by 16.3 percent, as the percentage of indebted households falls from 14.8 percent in the baseline to 12.4 percent after the tax reform. Although most of the gains from corporate tax reduction are absorbed by wealthy households, the tax reform shifts wealth concentration toward the bottom four quintiles.

Conclusion

Although the corporate tax reduction of 2017 reduces total tax revenue by less than one percent of GDP, the long-term effects will impact every part of the economy. The model’s results provided a counterintuitive projection: a decline in the corporate tax rate can reduce wealth inequality. Since the corporate tax burden is distributed evenly across each share of a firm’s equity, corporate tax reductions reduce the effective per-share tax incidence faced by all shareholders, regardless of a household’s location within the wealth distribution. A consequence of such a tax reduction is a relative improvement of the bottom 80 percent of households in the wealth distribution.

Table 4 — Baseline and Tax Reform Comparison

In addition to private consumption and savings growth, the dynamic model captured the growth in personal tax revenue resulting from the decline in corporate taxation. The model shows that almost 20 percent of the decline in corporate tax revenue is offset by an increase in personal tax revenue resulting from increased dividends to shareholders.

Table 5 — Simulated Effect of Reform on Wealth Quintiles

Although the corporate tax reduction will reduce tax revenue, the reform will also change the structure and composition of the U.S. economy. The results of this paper show that private consumption grows by the magnitude of the tax cut, likely offsetting the decline in government consumption—as long as the tax cut is eventually financed through a reduction in government expenditures.

A factor that may eventually diminish the direct impact of a corporate tax cut on the U.S. economy is the growth of government debt relative to GDP. Although the economy has shown little sign of strain from increased levels of US government debt in the periods preceding the TCJA, a decline in demand for U.S. treasury bonds may eventually place upward pressure on firms’ cost of capital.

Endnotes

1. See, for example, James B. Stewart, “Trump Tax Cuts and the Economy: Time Will Tell, Maybe,” The New York Times, February 1, 2018.

2. The model and results are described in more detail in Jorge Barro, “Long—term Macroeconomic Effects of the 2017 Corporate Tax Cuts” (research paper, Rice University’s Baker Institute for Public Policy, Houston, Texas, April 24 2018), https://www.bakerinstitute.org/media/files/files/494cac72/cpf-pub-corporate-tax-042418.pdf.

3. This finding is in contrast to a report published by the Council of Economic Advisers (CEA) in October 2017 that projected an increase in average household income from $83,143 to at least $87,520 — a 4.8 percent improvement. Cline (2017) also found lower wage increases than the CEA model, on the order of 1.4 percent. While the model in this paper applies an alternative approach, wage change estimates are similar, with the model used here projecting a 1.1 percent increase in wages. See The Council of Economic Advisers, “Corporate Tax Reform and Wages: Theory and Evidence” (Washington, D.C., October 2017), https://www.whitehouse.gov/sites/whitehouse.gov/files/documents/Tax%20Reform% 20and%20Wages.pdf; and William R. Cline, Will Corporate Tax Cuts Cause A Large Increase in Wages? (Washington, D.C.: Peterson Institute for International Economics, November 2017), https://piie.com/system/files/documents/pb17-30.pdf.

4. “U.S. Portfolio Holdings of Foreign Securities as of June 30, 2016” (Joint report from the Department of Treasury, Federal Reserve Bank of New York, and Board of Governors of the Federal Reserve System, April 2017).

5. Gravelle (2013) identifies several limitations of open economy models. See Jennifer Gravelle, “Corporate Tax Incidence: A Review of General Equilibrium Estimates and Analysis,” National Tax Journal 66, no. 1 (2013): 185.

6. Chen et al. (2017) show that reducing the corporate tax rate reduces the relative value of pass-through organization, motivating firms to access broader capital markets by filing as corporate-taxable C-corporations. The authors show that reducing the corporate tax rate to 20 percent causes a small increase in labor, capital, output, and consumption, and a small decline in the non-employment rate and wealth Gini coefficient. See Daphne Chen, Shi Shao Qi, and Don E. Schlagenhauf, “Corporate Income Tax, Legal Form of Organization, and Employment” (working paper, Federal Reserve Bank of St. Louis Working Paper Series, 2017).

7. In equilibrium, this is equivalent to a financial intermediary issuing debt to households, since all outstanding debt must be in zero net supply.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.