Overview

Harris County is the most populous county in Texas and the third-largest local government in the United States. Its budget decisions affect millions of residents, influence regional economic outcomes, and impact the provision of essential public services, including transportation, flood control, public health, law enforcement, and the justice system.

In October 2025, Harris County adopted its budget for the 2026 fiscal year (FY 2026 Adopted Budget).[1] In June 2024, it published the report, “Harris County Five-Year Financial Plan and Opportunities” (Five-Year Financial Plan), which examines various financial scenarios through 2029.[2] These documents, together with the “Annual Comprehensive Financial Report for the Fiscal Year Ended September 30, 2025” (FY 2025 ACFR), suggest two conclusions:

- While the county’s overall finances are stable, it is facing a growing structural deficit in its general fund.

- There are meaningful improvements that could be made to the budgeting process that would both enhance the county’s management of its resources and provide the public with greater access and clarity regarding its revenues and expenditures.[3]

County’s Fiscal Prospects

Harris County is operationally stable at a consolidated level. According to the most recent audited financial statements, its net assets marginally increased over the past few years, and the general fund balance has largely remained unchanged.[4] However, the county faces growing challenges to the long-term budgetary sustainability of its general fund. This is how the Five-Year Financial Plan summarized its financial prospects: “Expense growth has accelerated while Harris County has revenue growth restrictions limited by 2019 Statutory changes. With no ability to absorb high inflation, maintaining resiliency will require maximizing available revenue sources while simultaneously controlling costs.”[5]

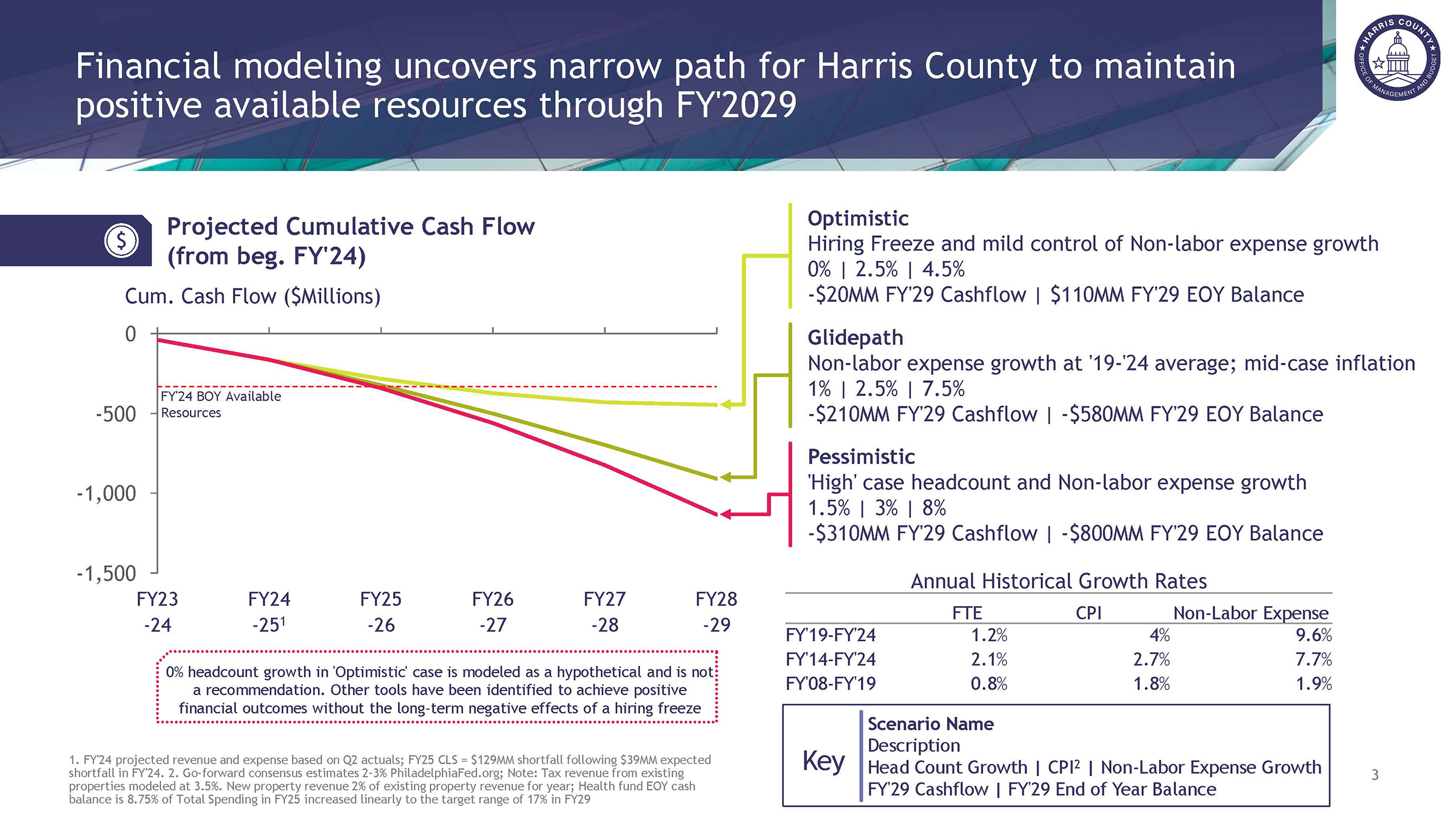

The Five-Year Financial Plan indicates the county’s general fund balance will steadily decline and could reach a historic deficit by FY 2029 unless revenues are enhanced or expenditures constrained. However, despite this warning, the two most recent budgets — FY 2025 and FY 2026 — significantly increased general fund expenditures. In its recent preliminary budget forecast for FY 2027, the county budget office projects a $129 million general fund deficit without expenditure reductions or increases in property taxes above the voter-approved rate. Without adjustments to the current expenditure trajectory, general fund reserves will erode more rapidly than projected in the Five-Year Financial Plan.

Improving the Budgetary Process

Harris County’s finances are highly complex. This complexity is primarily the result of extensive fund accounting required by statute, and its subsidiary governmental entities — the Harris County Flood Control District (HCFCD), Harris Health, and the Harris County Toll Road Authority (HCTRA). This structure presents significant challenges for the budgeting process. However, the county could adopt improvements to the budget process to present its finances more comprehensively and transparently. In particular, the budget processes for funds not included in the general fund provide little detail on how those funds are expended.[6]

Historical Context

Texas counties operate under limited statutory authority and possess only those powers expressly granted by the legislature. Unlike cities, counties lack broad home-rule or ordinance-making authority, reflecting their historical role as administrative units serving primarily rural populations. Consistent with that limited role, county revenue options are also narrowly constrained, relying heavily on property taxes and fees authorized by state law.

In large urban counties, especially those where substantial populations live in unincorporated areas that require urban-level infrastructure and services, this governance structure creates tension between expanding service expectations and limited regulatory and fiscal tools to meet them. This tension is particularly acute in Harris County because about half of its population lives in unincorporated areas. Indeed, if the unincorporated portion of Harris County were its own county, it would be the ninth largest in the U.S.

This limited role for county government has also spawned a plethora of special-purpose governmental entities, such as municipal utility, special development, and emergency service districts. According to the Harris Central Appraisal District, there are 758 governmental entities within Harris County.[7] This fragmented network of governmental entities may contribute to inefficiencies and situations in which entities work at cross-purposes. Reform of local government structure, especially in large urban counties, should be the subject of additional research and legislative review.

Harris County has experienced decades of rapid population growth. This growth has steadily expanded the tax base. However, that growth has also increased the demand for services and infrastructure needs.

In past years, leadership has been able to conservatively manage this growth and maintain a healthy fiscal position. However, in recent years, the county’s ability to maintain its fund balances has increasingly relied on intergovernmental revenue, primarily from the federal government, expenditure shifting, and property tax increases. For reasons discussed below, these sources will likely be significantly constrained in the future, resulting in increased fiscal pressure as outlined by the Five-Year Financial Plan.

Projected General Fund Structural Deficit

The county’s financial accounting — as required by Texas statutes, generally accepted accounting principles (GAAP), debt covenants, multiyear capital projects, and quasi-government units for healthcare, toll roads, and flood control — is broken down into hundreds of individual funds, with complex interactions among them. However, the general fund is the largest and most consequential.[8] The general fund provides resources for basic services, such as law enforcement, administration of justice, parks, housing, infrastructure maintenance, and a variety of social and health programs.

The Five-Year Financial Plan projects that general fund revenues will increase by 4.55–5% annually.[9] However, over the last decade, general fund expenditures have grown by an average of 6% per year, and over the last five years by 7% per year. The preliminary FY 2027 budget indicates that to maintain the “Current Level of Service and Spending” would require a 10.3% increase ($2.769 billion–$3.056 billion).[10] If this pattern continues, the county faces the potential of a growing structural imbalance in its general fund.

The Five-Year Financial Plan describes three potential scenarios.

- Glidepath extrapolates recent historical trends and projects that the general fund annual deficit will reach $210 million by FY 2029 and result in a negative ending fund balance of $580 million.

- Optimistic assumes aggressive cost-control measures and projects that the county would still run deficits and come close to exhausting the general fund by FY 2029 with a $110 million remaining balance.

- Pessimistic describes a scenario in which costs continue to increase, the general fund’s annual deficit exceeds $300 million in FY 2029, and the fund balance falls to a negative $800 million.

Under any of these scenarios, the county would not be able to maintain its current level of services or the minimum Public Improvement Contingency Fund balance established by Commissioners Court in 2024 (Figure 1).[11]

Figure 1 — Harris County Projected Cumulative Cash Flow, FY 2023–FY 2029

As noted above, despite the warnings set out in the Five-Year Financial Plan, the last two approved budgets increased general fund expenditures by far more than the projections assumed in the Five-Year Financial Plan.

General Fund Revenue Analysis

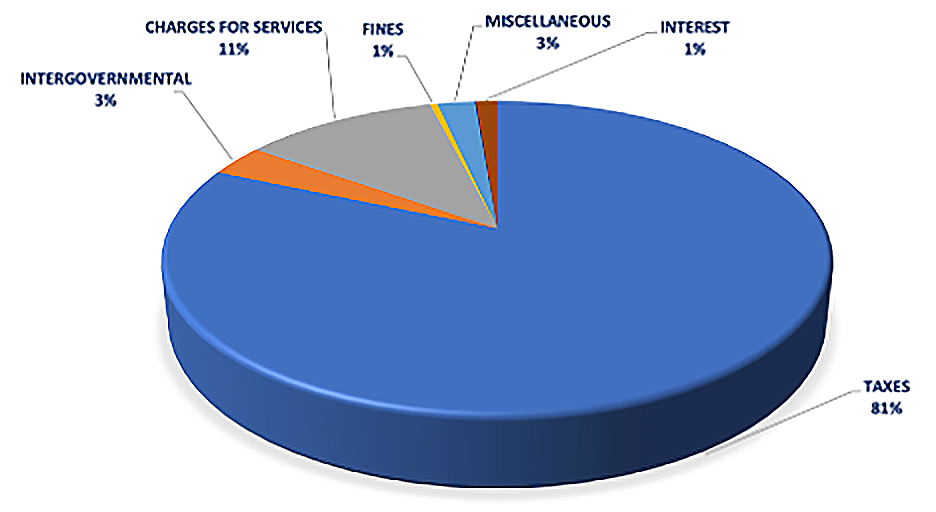

The general fund relies primarily on property taxes. This year, property taxes will represent over 80% of general fund revenue. Other significant sources include fees, charges, and fines (12%) and intergovernmental revenues (3%) (Figure 2). The county’s financial performance is, therefore, highly dependent on property tax receipts, which in turn depend on demographic and market factors largely beyond its control.

Figure 2 — Harris County General Fund FY 2026 Estimated Revenues

Property Tax Analysis

The county’s ability to increase property tax rates is constrained by both political pressure and state limitations. For many years, Texas counties were subject to a rollback election provision that allowed voters to challenge property tax increases exceeding 8% in a year. In 2019, the Texas Legislature passed SB 2, which significantly tightened this restriction going forward.[12] It lowered the threshold to 3.5% and required counties to affirmatively obtain voter approval for any increase above that level. However, there are exceptions to this constraint, one of the most consequential being the declaration of a state of emergency.

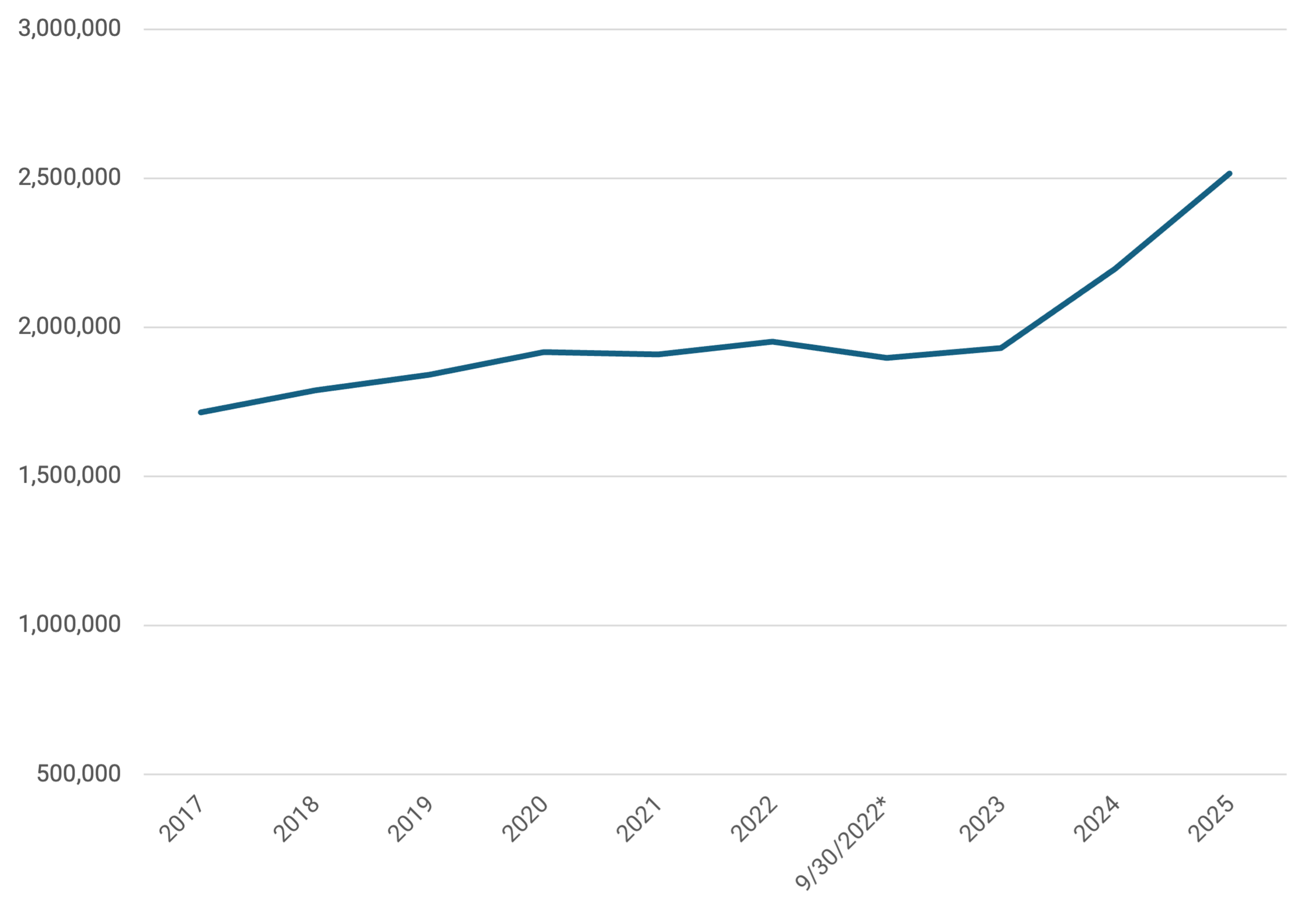

For the first half of the last decade, Harris County only made small changes to its property tax rate. Nonetheless, because appraised values continued to climb, property tax collections rose by 4.3% annually. Due to state limitations and historic increases in property valuations, particularly in FY 2022 and FY 2023, the county was forced to reduce its tax rate each year from FY 2020 to FY 2023. Those rate reductions were mostly offset by valuation increases, resulting in relatively flat property tax revenue for those years.

However, there were double-digit increases in property tax revenues in FY 2024 and FY 2025. The increases resulted from higher valuations and certain technical adjustments permitted by state law. Also, in FY 2025, the Commissioners Court used the emergency declarations invoked for the derecho storm and Hurricane Beryl to increase the tax rate by slightly more than 10% (from 0.35007 to 0.38529).[13] This rate hike, combined with the property valuation increase, generated a historic 30% increase in property tax levies from FY 2023 to FY 2025 (from $1.93 billion to $2.51 billion) (Figure 3). The county’s recently issued audit noted that the general fund net fund balance increase was “largely due to higher property tax revenue.”[14]

The county budget office maintains that the increases in FY 2024 and FY 2025 resulted from tax revenues remaining flat over the three previous years, even as general fund expenditures increased, and should be contextualized against those years.[15]

Figure 3 — Harris County Property Tax Levy, FY 2017–FY 2025

Note: * Harris County changed its FY in 2022 (it was Mar. 1 to Feb. 28, and it changed to Oct. 1 to Sept. 30).

As noted in the budget, the tax base has increased by an average of 6.7% for the last decade, but the growth slowed significantly in FY 2024 and FY 2025. Its projection is for a 3.3% increase this year and a 5.5% increase going forward (Table 1). However, based on recent trends and preliminary FY 2026 tax roll numbers, 5.5% may be overly optimistic.[16]

Table 1 — Projected Maintenance and Operations (M&O) Tax Revenue, FY 2025–FY 2030

General Fund Expenditure Analysis

For FY 2026, the county budgeted $2.77 billion in general fund expenditures, a 3.7% increase over the FY 2025 budget and 5.2% over FY 2025 actual expenditures. However, it shifted $78 million in medical expenditures for jail inmates from the general fund to Harris Health in its FY 2026 budget. Without that expenditure shifting, the FY 2026 budget would have represented a 6.7% increase over the FY 2025 budget and an 8.2% increase over FY 2025 actual expenditures. The increases in the FY 2026 budget came on top of those in the FY 2025 budget, which increased expenditures by 11.1% over the FY 2024 budget and by 9.4% over FY 2024 actual expenditures.

In the FY 2026 budget, the budget office originally estimated that, to maintain the county’s current level of service, it would need to spend about $2.8 billion. This included approximately $50 million for a compensation adjustment package.

However, due to rising salaries for law enforcement officers in the Houston region and challenges in recruiting and retaining officers, the county opted to add about $130 million to the budget to provide substantial raises to its officers. That increase would have raised the general fund budget to over $2.9 billion and created a substantial deficit for the year. To reduce the potential deficit, the budgets of numerous departments were cut. About half of the reduction, however, came from shifting the jail medical expenditures to Harris Health, as described above.

As discussed in the Five-Year Financial Plan, spending at the levels of the last two budgets is unsustainable, even under the most optimistic assumptions.

General Fund Expenditure Breakdown

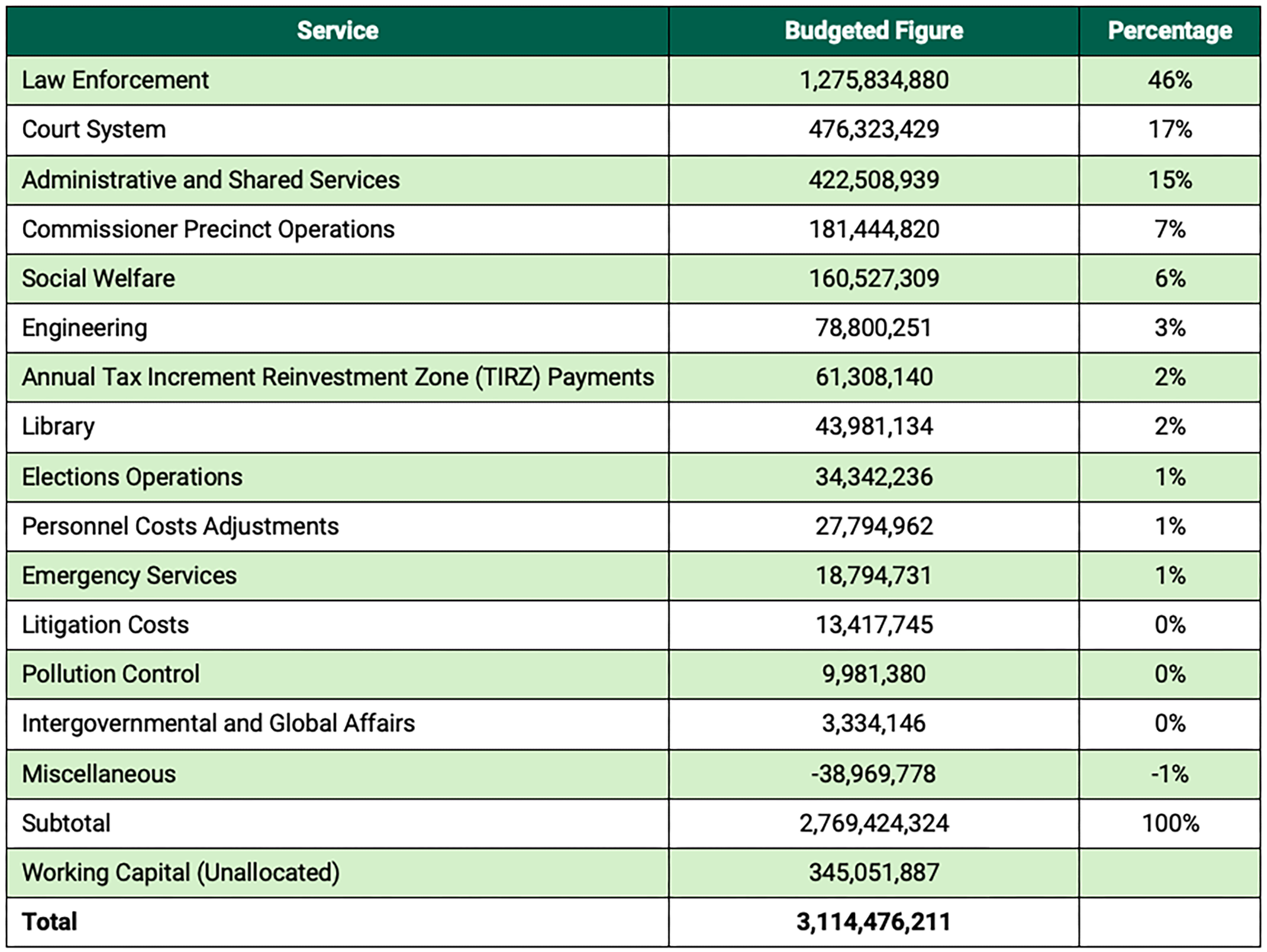

The county’s budget presentation includes a high-level breakdown of general fund expenditures.[18] Included in this breakdown is a budget item titled “General Administrative,” to which approximately $194 million is allocated in the current budget. This category is somewhat of a catch-all for various expenditures. Because this report’s review indicated that some of the line items were linked to specific departmental operations, these items were reallocated to the departments with which they were functionally related.

After these adjustments, Table 2 represents the major categories of the county’s general fund expenditure.

Table 2 — Harris County General Fund Expenditure, FY 2026

As indicated above, general fund expenditures are primarily directed toward public safety and the court system at 63%. The next largest category, Administrative and Shared Services, comprises true administrative expenditures, such as the administration, budget, and treasury offices. However, it also includes expenditures that would be more appropriately allocated to the respective departments. For example, approximately $115 million is budgeted for “Universal Service” and “Universal Services-IT.”[19] This report discusses improvements to the budgeting process below.

The Working Capital Line Item

In developing its budget, the county uses an important and unusual mechanism involving what it terms “working capital.”[20]

Each year, the budget is based on the county auditor’s “Final Estimate of Available Resources” (FEAR). This publication estimates all funding available for spending — including existing cash and investment balances by fund and expected annual revenue — and, by law, the Commissioners Court cannot budget expenditures that exceed this estimate.

Historically, the county has budgeted general fund departmental expenditures significantly below the FEAR. In FY 2026, for example, the estimate was $3.1 billion while specific departmental expenditures totaled $2.77 billion, leaving $345 million unallocated. The adopted budget describes this difference between the FEAR and the budgeted departmental expenditures as working capital.[21]

This working capital line item appears to serve as a contingency fund for budget variations during the year or to address unexpected expenditures. However, county budget office data since FY 2022 shows that overruns have been modest, peaking in FY 2023 at $66 million, just 3% of that year’s total budget. As a result, this allocation has largely been carried forward each year, with changes only for variations in available resources.

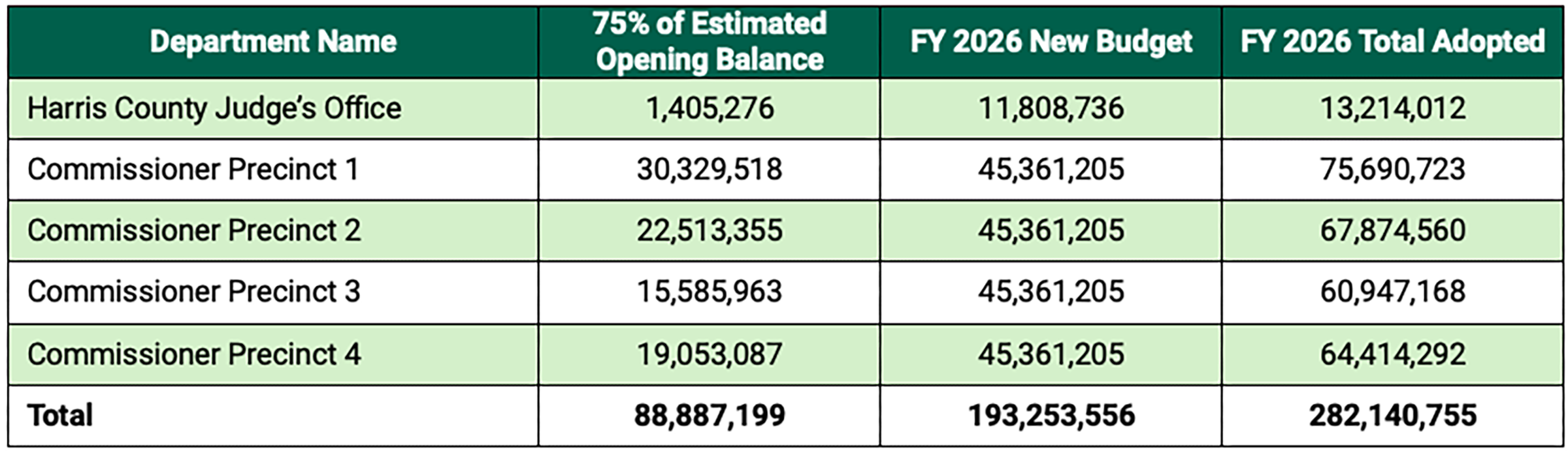

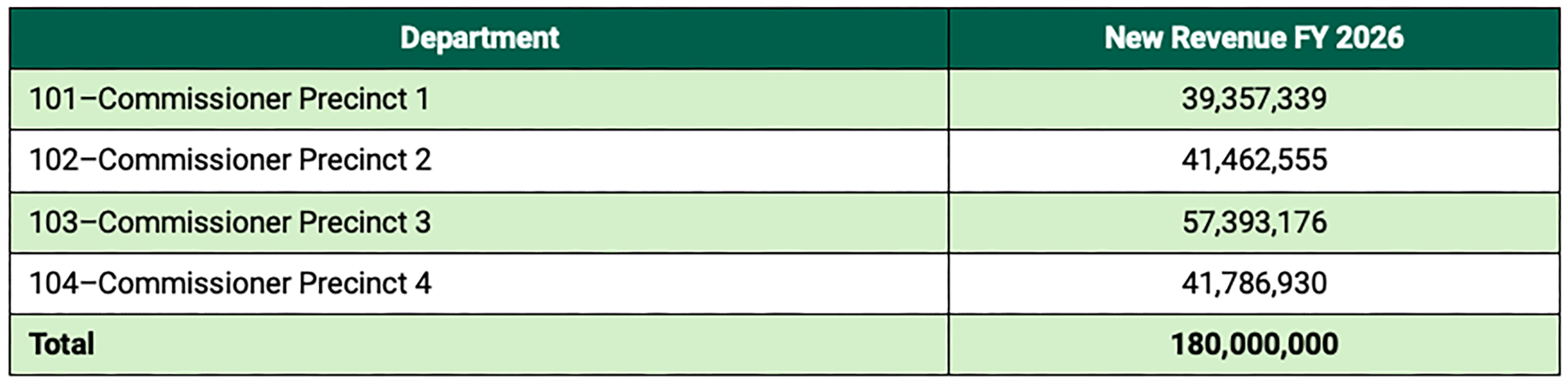

The budget also includes an allocation of this working capital to the county judge’s office and the individual commissioner precincts; in the FY 2026 budget, this totaled to $89 million. However, this amount is not included in the $2.77 billion general fund total.[22] Nonetheless, these allocations are included in the individual department budgets. For example, the line-item budget for Precinct 1 is $45.3 million. However, in the individual budget summary, the total is $75.7 million, with no detail on how the additional working capital allocation might be spent (Table 3).

Consequently, how these working capital allocations affect the county judge’s office and commissioner precincts is unclear.[23] While the budget office notes these funds are typically used to make facility capital improvements, the lack of itemization provides little transparency as to the funds’ actual use. Furthermore, if these allocations were fully spent, the FY 2026 expenditure increases over the prior year would be even more pronounced.

Table 3 — Commissioners Court Budget Overview, FY 2026

Opportunities for Expenditure Reduction

As outlined in the Five-Year Financial Plan and the FY 2026 Adopted Budget, the county’s leadership should identify additional revenue sources or reduce expenditures. Because of state-imposed limitations on property tax increases, there appear to be relatively few opportunities to increase revenue. Therefore, the bulk of the projected budgetary shortfall should be offset by expenditure control.

Controlling Administrative Expenditures

The breakdown of expenditure above illustrates that approximately 15% of the budget is allocated to administrative expenses. The annual audit indicates that 20% of the county’s employees are involved in “County Administration.”[24]

However, the total administrative expenditure is substantially higher than this cursory view would suggest. Within each department, there are considerable layers of additional administrative expenditure. For example, out of the Public Health Services Department’s 518 positions:

- The descriptors of director, manager, supervisor, and executive assistant apply to 184 positions; 25 were added in the current budget.

- Employees involved in administrative duties now comprise 40% of the department’s payroll.

- On average, each manager supervises about four employees.[25]

While similar ratios appear across other departments, evaluating whether they are justified is beyond the scope of this research. The county budget office believes these administrative headcounts may be overstated due to misclassification: For example, while the county judge’s entire budget is classified as administrative, roughly half funds emergency management services.[26] An external review of staffing levels could resolve any classification errors and identify potential administrative savings.

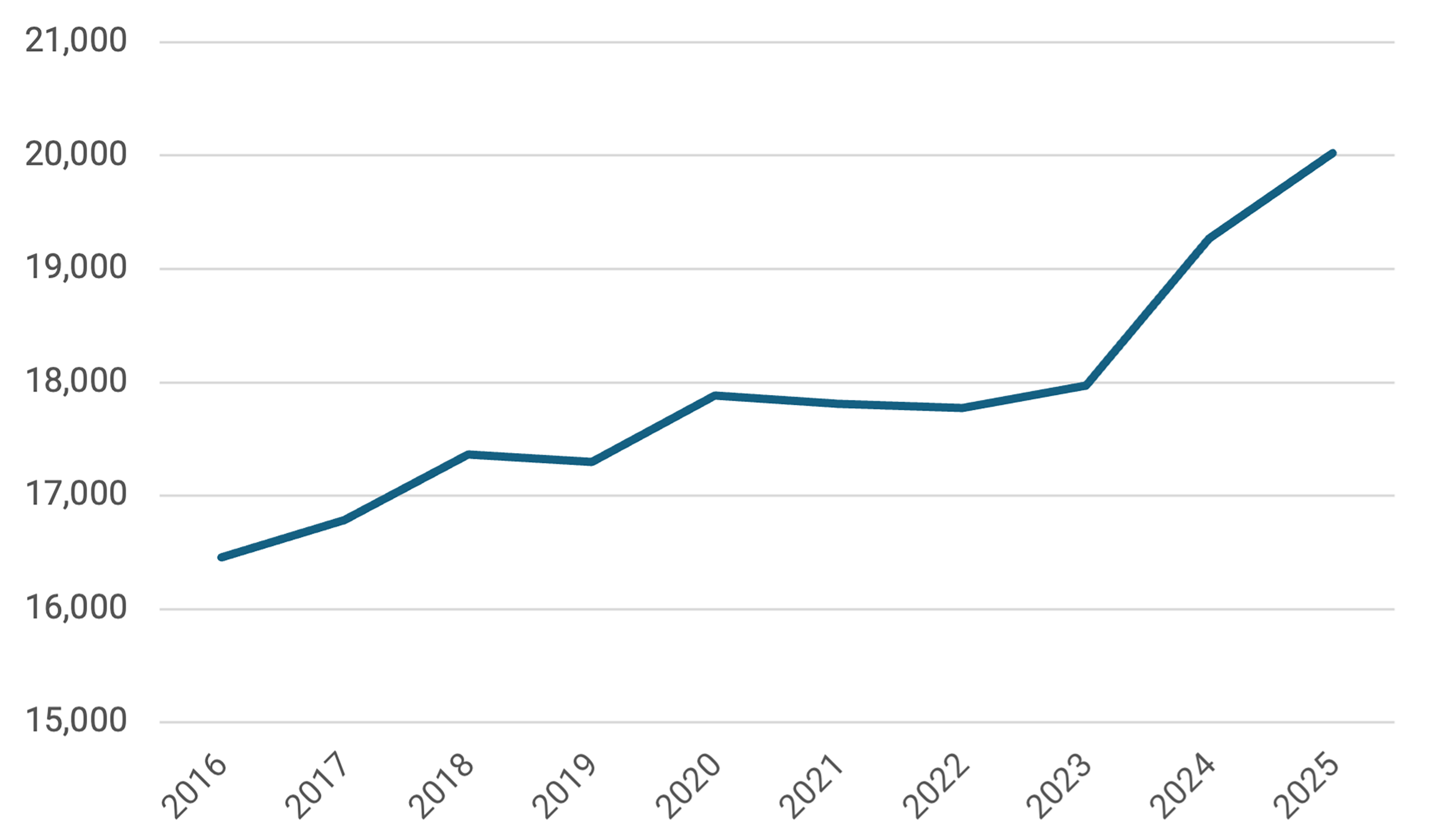

Controlling Headcount Growth

From FY 2016 to FY 2023, the employee headcount grew by an average of 1.2%. That was in line with the county’s population growth over that time. However, in FY 2024 and FY 2025, the county added over 2,000 new positions, increasing its headcount by more than 11% (Figure 4).[27] Expanding the employee headcount at this pace will inevitably compound the fiscal challenges outlined in the Five-Year Financial Plan.

Figure 4 — Harris County Full-Time Equivalent (FTE) Employees, FY 2016–FY 2025

Controlling Payroll Costs

As discussed previously, the county gave large raises to law enforcement employees. It also implemented a comprehensive compensation adjustment for most county employees based on a consultant’s review. These raises will increase the county’s payroll expenditures by approximately $200 million and add to the financial pressure on the general fund in future years. Controlling pay increases will be essential to avoid unsustainable future deficits.

Other Areas of Concern for Long-Term General Fund Stability

End of American Rescue Plan Funding

The American Rescue Plan Act (ARPA) was passed by Congress in 2021 in response to the COVID-19 pandemic, and Harris County received an allocation of $915 million from the federal government under ARPA. In addition to the federal funds allocated to the county, it earned $75 million in interest, bringing the total to about $990 million. Under the terms of ARPA, all funds must be spent by the end of 2026.

Prior to the current budget year, the county had spent about 75% of its ARPA funds. In the current budget, it committed $192 million to fund around 16 programs, which means that at the end of this fiscal year, about $50 million of ARPA funding will remain.[28] Many of the current allocations fund ongoing programs, such as creating 20 new chronic disease prevention positions. Consequently, the county faces a decision in the next budget cycle to either terminate these programs or absorb them into the general fund, further compounding future deficits.

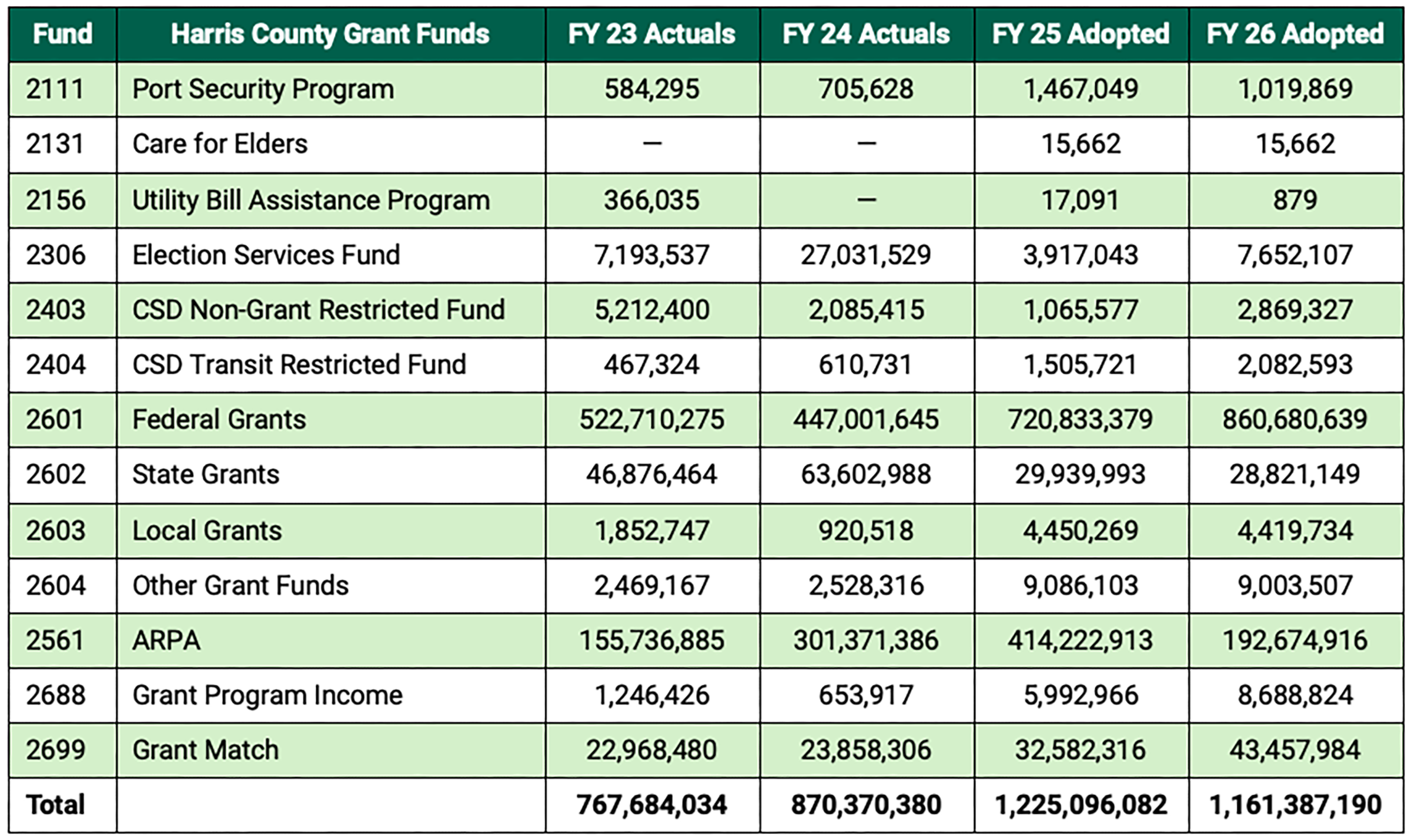

Reliance on Other Grants

Harris County budgeted $1.16 billion in grant income for the current fiscal year, down from $1.22 billion in the previous year. Out of these funds, $861 million comes from federal grants other than ARPA funds because those funds are already committed (74%) (Table 4).

Table 4 — Harris County Grant Funds, FY 2026

While most of these grants are spent outside of the general fund, they provide services to Harris County residents. Many represent long-term commitments by state and federal governments, but increasing fiscal pressure at both levels could jeopardize future funding. Any reductions would place the county into a challenging trade-off: either eliminating or reducing those services or attempting to pay for them from the already-stressed general fund.

Criminal Justice Expenses

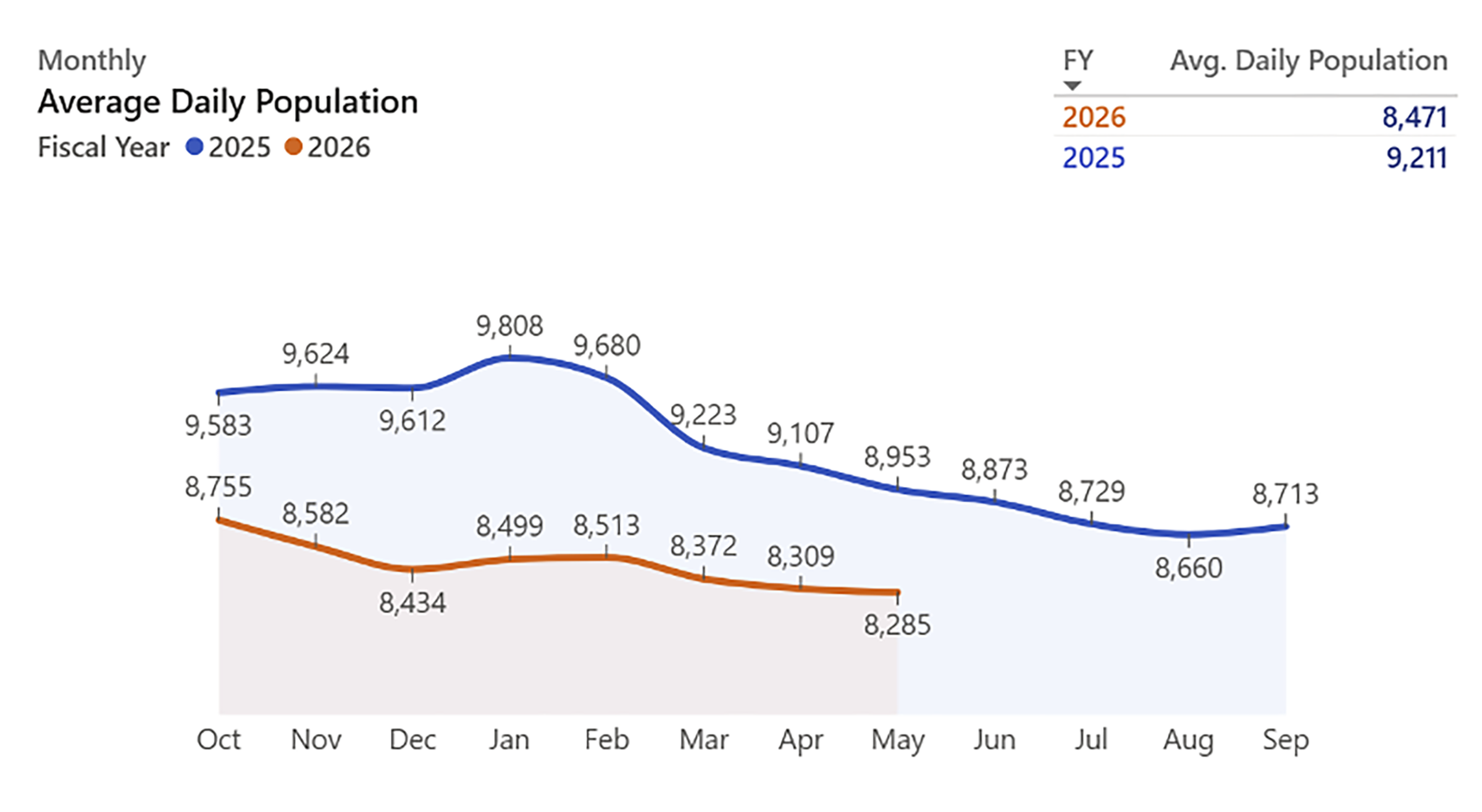

In recent years, the county has adopted a number of initiatives to reduce its jail population and, in turn, its jail-related expenses. However, the efforts were largely offset by the spike in serious crimes beginning around 2018 and exacerbated by lengthy trial backlogs in the county’s criminal courts due to facility issues related to Harvey flooding and the COVID-19 pandemic. These issues also increased legal fees for indigent defendants. Over the last year, as crime rates have subsided and more cases have been tried, there has been some improvement. According to figures, the average daily jail population this year is down by about 8% from last year (Figure 5).[29] If this trend continues, it could provide some relief to the general fund.

Figure 5 — Harris County Jail Population, FY 2025–FY 2026

Reliance on Toll Road Revenues

Harris County owns and operates an extensive toll road system, administered by the HCTRA. In the last decade, HCTRA has generated over $4 billion in surpluses. For many years, the county has withdrawn funds from HCTRA to pay for mobility maintenance and improvement projects. These withdrawals have relieved pressure on the county to borrow for these improvements and increase property taxes.

The amounts withdrawn ramped up sharply from FY 2021 through FY 2025, with the county withdrawing $1.9 billion during that period. According to the recent audit, it spent $250 million from these funds in FY 2025.[30] In addition to the withdrawals, HCTRA reimburses the county about $46 million per year for law enforcement and administrative costs.[31]

Transfers from HCTRA are distributed to the commissioners for mobility projects within their precincts. There has been some dispute over how the transfers are distributed among the precincts.[32] Table 5 shows the allocations adopted in the FY 2026 budget.

Table 5 — Budgeted Allocations of the HCTRA Withdrawals, FY 2026

Revenue from HCTRA was used to offset the impact of stalled property tax receipts from FY 2020 to FY 2023 and will be important in the future for relieving pressure on the general fund. While HCTRA’s financial condition remains strong, its most recent financial results have begun to show some signs of strain, and growth may be flattening. Accordingly, the county is possibly nearing the limits of its ability to withdraw funds or charge back expenditures on an ongoing basis.[33]

Demographic Headwinds

As previously noted, Harris County has experienced rapid population growth for the last 50 years. That growth was interrupted only by the 1980s oil crash. However, recent U.S. census data suggest that growth is likely slowing, which may pose additional fiscal challenges.[34]

Of particular concern is domestic out-migration from the county. Last year alone, the county lost 43,000 residents to other parts of the U.S., bringing the total over the last decade to over 300,000.[35] However, high volumes of international in-migration have offset this trend. Although a detailed demographic analysis falls outside the scope of this report, international immigrants may arrive with a greater need for services — particularly healthcare — alongside a smaller initial tax base contribution than those leaving.

Future Property Tax Base Valuations

Harris County is reliant on property tax revenue and therefore, to the valuation of its property tax base. The county is assuming a 5.5% increase in its property tax base through its forecast period. This is generally consistent with historic trends. The increase in FY 2026 was 5.27%. However, a number of crosscurrents may affect the property tax base.

Single-family residences make up over 40% of the county’s tax base.[36] Public opposition to property taxes has been growing, with many now calling for their end, at least for homes.[37] Public frustration with property taxes on homes has been the driving force behind the recent adoption of restrictions on local governments increasing their taxes. With housing affordability topping voters’ minds in recent surveys, the pressure to contain property tax increases is unlikely to wane in the near future.[38]

This opposition can manifest in numerous ways. There are already discussions at the state level about additional restrictions. Also, the Harris Central Appraisal District (HCAD) reports it is receiving a record number of protests and appeals. Some preliminary reports from HCAD suggest that there will be little to no increase in the single-family tax base this year.[39]

There are also indications of significant reductions in office building valuations due to high vacancy rates.[40] Potentially countering that trend, however, is a surge in manufacturing and warehouse facilities associated with recent announcements of technology and petrochemical plants.[41]

The county should closely monitor this issue, and develop a contingency plan in case the tax base falls short of meeting the projected 5.5% growth rate.

Potential Improvements to the Budgeting Process

Greater Transparency on Non-General Fund Budgeting

Despite a two volume FY 2026 Adopted Budget spanning over 1,400 pages, there is very little detail on funds not included in the general fund. For example, a volume 1 appendix titled “All Funds and Amounts” lists over 300 non-general funds totaling nearly $18 billion across just seven pages. Expanded disclosure and explanation should be provided regarding these substantial accounts.[42]

Greater General Fund Expenditure Detail

The county’s budget breaks down expenditures by department and, within each department, by program. However, the financial information is presented in summaries with little supporting detail. For example:

- The section on performance measures provides no explanation of how targets were established or what they cost to achieve.

- The headcount section lists position titles by each program area, without any information regarding salary ranges or costs for each category.

While these various schedules generate a lengthy budget document, the current presentation makes it very difficult to assess the reasonableness or effectiveness of the county’s general fund expenditures.

Improve Budget Allocations for Shared Services

Allocating the costs of shared services to the departments that directly benefit from them is well supported in the academic literature on cost accounting and public finance, as it promotes both efficiency and accountability. Cost allocation leads to more efficient resource use by aligning incentives, ensuring that departments internalize the costs of the services they consume.[43]

There are several categories of expenditures that appear to be shared services, for which the budget makes no attempt to allocate funds. In some cases, expenditures are clearly allocable to a department but are instead grouped under general budget line items. Developing a rigorous shared allocation would significantly improve the budget process and provide the Commissioners Court with improved data to make budgetary decisions.

Greater Clarity on Use of Toll Road Transfers

Currently, the budget provides no detail on how each precinct spends the toll road funds it receives, leaving taxpayers with little transparency on the use of those funds.

Texas Transportation Code §284.0031 limits the use of excess toll revenues. After the Texas Legislature raised questions about how the HCTRA transfers have been used, in December 2025 the Commissioners Court authorized a third-party audit to determine whether expenditures from the toll road funds comply with the statute. The first audit will cover FY 2026.

The Harris County Auditor’s Office has occasionally audited the use of the toll transfers for the same reason. The third-party auditor also appears to assess compliance as part of the county’s ACFRs.[44]

While a technical review of statutory compliance is unlikely to provide much substantive information on the actual projects being financed, adding a detailed description during the budgeting process of how these funds may be used each year would greatly increase transparency.

Working Capital Designation

As previously discussed, the county budget uses the term “working capital” as a balancing item between total available resources and departmental appropriations. As shown in the FY 2026 Adopted Budget, this amount is included as a funding source alongside current-year revenues. In substance, it represents accumulated prior-year resources, adjusted for recent operating surpluses or deficits. In other words, this amount represents prior-year budget authority that was not expended, rather than newly generated revenue, and therefore functions differently from recurring revenue sources used for expenditures. Most governmental entities would instead present such amount as a beginning fund balance or an available fund balance.

The term “working capital” appeared for the first time in the FY 2021 budget cycle. This timing coincides with the county’s shift away from its prior practice of allowing departments to roll over unspent funds from the previous year. As a result, balances that previously would have remained at the departmental level appear to have been centralized and reflected in this working capital category.

However, an exception has been carved out since FY 2021, allowing working capital allocations for the county judge’s office and the commissioner precincts to roll over annually. Its current iteration includes a column entitled “75% of Estimated Beginning Balance” (Table 3). There is no explanation in the budget for the 75% calculation, but it appears to be an amount carried forward from year to year. If so, it implies that there is around $100 million of carryover funds that could be tapped by the county judge and commissioners for their operations. This un-itemized column is added to the amount allocated in the departmental budgets to calculate the “FY 26 Total Adopted Budget.”

Since the adoption of this policy, $568 million has been budgeted for the county judge and commissioner precincts through beginning-balance allocations. However, from FY 2022 to FY 2025, it appears that the working capital authorizations have been used sparingly. During that time, their combined expenditures have only exceeded the specific departmental budgets by $6.5 million, and have frequently been lower, thus increasing the carry-forward for the following year. The largest use of the allocated beginning balance by any single office in one year was $11.7 million.

Nonetheless, these working capital allocations to the county judge and commissioner precincts increase spending authority beyond the normal year-to-year budget, which would typically be visible to taxpayers. Additionally, the failure to reconcile the working capital each year — as would happen with normal beginning- and ending-balance accounts — creates the possibility that over time, these practices could blur the distinction between recurring and one-time resources. This practice can mask declining fund balances and complicate efforts to reconcile adopted budgets with financial reports.

The result is a real increase in spending capacity, but one that is less transparent than changes reflected in the core adopted budget. For taxpayers, the key issue is not the label, but that these carry-forward allocations can materially increase spending authority even when the adopted budget appears stable.

For these reasons, the county and its taxpayers would be better served to adopt traditional beginning and ending fund balances for each department. It should be noted that transitioning to this traditional accounting methodology does not restrict the Commissioners Court’s discretion in setting policies for the use of unspent funds by specific departments.

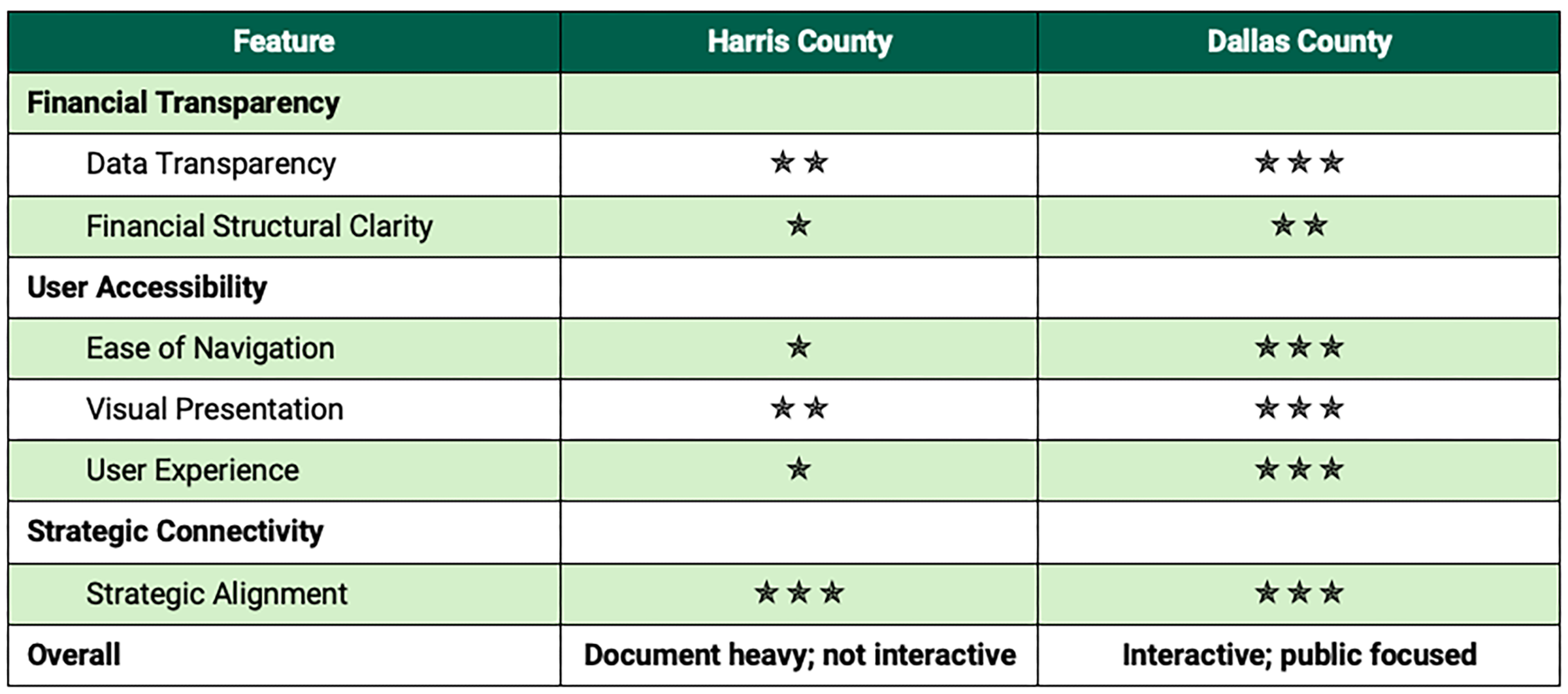

Adoption of the User-Friendly Budget Portal

Improving the budgeting process is fundamental to establishing a clear, transparent structure financial structure. To build on these structural changes, Harris County can also modernize its presentation to make the budgets more accessible to residents.

While Texas counties vary in their communication philosophies, the overarching goal should be financial clarity. Currently Harris County has a very text-heavy budget presentation. In contrast, Dallas County has adopted an interactive, digital portal that — based on a brief review — offers residents greater detail and ease of use.[45] While a detailed comparison of the various budget public-facing portals is beyond the scope of this research, it appears that adopting a similar digital approach could significantly enhance Harris County's public transparency.

Table 6 — Comparison of Harris and Dallas County Budget Portals

Note: More stars mean a higher rating in the corresponding category.

Conclusion

Harris County will enter the FY 2027 budget planning period in a relatively stable position. However, general fund stability may soon deteriorate without spending curbs or new revenue. Given the limited opportunities to improve revenue streams, implementing significant cost controls could be one of the few available options to prevent a growing, unmanageable structural deficit. Understanding this dynamic is essential for an informed discussion between policymakers and taxpayers about the county’s fiscal direction and the trade-offs that may be required to maintain services over time.

This challenge underscores the importance of transparency in the county’s finances. Clear distinctions between reserves and operations, improved reconciliation of budget documents, and treatment of reserve usage as a policy choice would strengthen public understanding, financial transparency, and institutional accountability.

Ultimately, Harris County’s experience offers a broader lesson for large local governments: Fiscal resilience is not only a function of how much capacity exists but also of how clearly that capacity is deployed, disclosed, and sustained over time.

Acknowledgment

This review of the Harris County budget is part of an initiative of the Center for Tax and Budget Policy at Rice University’s Baker Institute for Public Policy to provide financial data and information on state and local governmental entities to the public. The authors would like to recognize the extraordinary cooperation that was received from the Harris County Office of Management and Budget (OMB) and the Harris County Auditor’s Office, in preparing this report.

Certain numbers and figures are rounded for ease of reading.

Notes

[1] Fiscal year (FY) 2026 spans Oct. 1, 2025, through Sept. 30, 2026. “Budget Documents: Fiscal Year 2026,” Harris County Office of Management and Budget (OMB), https://budget.harriscountytx.gov/budget.aspx.

[2] OMB, “Harris County Five Year Financial Plan and Opportunities” (“Five-Year Financial Plan”), PowerPoint presentation, June 4, 2024, https://files.constantcontact.com/9b0ba6dd101/3230425d-5c71-4ed2-9fb4-3122dc838e95.pdf.

[3] Harris County Auditor, Annual Comprehensive Financial Report for the Fiscal Year Ended September 30, 2025 (FY 2025 ACFR), April 7, 2026, https://bit.ly/44JaieA.

[4] Harris County Auditor, FY 2025 ACFR, Tables 2—3, 239–41. For the purposes of this analysis, the General Fund is a combination of several subfunds, including General Operating, Public Contingency, Mobility, Infrastructure, General Debt, and several other small subfunds. The subfunds are separated due to restrictions on their use. The only subfund that is not restricted is General Operating. References to the General Fund mean the General Operating subfund only, unless noted otherwise.

[5] OMB, “Five-Year Financial Plan,” slide 2.

[6] A key factor affecting the interpretation of the county’s budget is that the budget is prepared on a cash basis, while financial results in the ACFRs are reported on a modified accrual basis, creating structural differences in how revenues, expenditures, and fund balances are recognized.

[7] “Jurisdictions,” Harris County Appraisal District, https://hcad.org/search/jurisdictions/.

[8] The county’s finances are further complicated by the fact that the Commissioners Court also controls two other significant entities: Harris County Flood Control District and Harris County Toll Road Authority. This analysis focuses on the county’s General Fund and other subsidiary budgets and incorporates aspects of these other entities only to the extent they affect county operations. According to the county auditor, the county’s total revenue for all funds was $8 billion (Harris County Auditor’s Office, Final Estimate of Available Resources, Fiscal Year 2026 [FY 2026 FEAR], September 18, 2025, https://bit.ly/4eIb7dH).

[9] The county auditor estimates revenues for the upcoming fiscal year in the FY 2026 FEAR. For FY 2026, the auditor has estimated the revenue increase at slightly over 3%, compared with the OMB’s estimate of slightly under 4%. For a discussion of the differences in the two estimates, see OMB, Fiscal Year 2026 Adopted Budget (FY 2026 Adopted Budget), vol. 1, 37, https://bit.ly/4gS50oq.

[10] “Current level of service and spending” is the baseline cost of maintaining existing programs, staffing, facilities, benefits, debt obligations, contracts, and service standards for the next budget period, adjusted for known cost changes such as inflation, salary commitments, population growth, caseload changes, utility costs, contractual increases, and legally required payments.

[11] In 2007, the Commissioners Court created the Public Improvement Contingency Fund, a subfund of the General Fund. It was renewed in August 2024, when the Commissioners Court adopted a policy to maintain a contingency fund in the event of an emergency, “equal to 12.5% of the Auditor’s estimated General Fund revenues for each fiscal year” (Harris County Commissioners Court Agenda, File#: 24-5008, August 15, 2024, bit.ly/3SexdM1).

[12] Texas Property Tax Reform and Transparency Act of 2019, S.B. 2, 86th Leg. (2019–20), https://capitol.texas.gov/tlodocs/86R/billtext/pdf/SB00002F.pdf.

[13] “Hurricane Beryl and Derecho,” Harris County Housing & Community Development, 2024, https://hcd.harriscountytx.gov/Disaster-Recovery/Hurricane-Beryl-Derecho; OMB, FY 2026 Adopted Budget, vol. 1, 14: OMB, FY 2025 Adopted Budget, vol. 1, 34, https://bit.ly/4ffV6M8.

[14] Harris County Auditor, FY 2025 ACFR, 25.

[15] This is the view expressed by Harris County and Harris County Central Appraisal District officials interviewed by the researchers.

[16] The county is assuming a 3.5% valuation increase on existing properties and a 2% increase from new improvements. As of the writing of this report, the Harris County tax base for the current year is up by 5.6%. However, a record number of appraisal protests are pending, suggesting the final increase may come in substantially lower.

[17] The county’s budget projections are lower than the property tax levies in Figure 3 because the county projections are for the maintenance and operation rate only, and the levy includes other components of the total tax rate.

[18] OMB, FY 2026 Adopted Budget, Excel spreadsheet, https://bit.ly/4eBbwgB.

[19] OMB, FY 2026 Adopted Budget, vol. 2, 483–516, https://bit.ly/4vdw70K.

[20] OMB, FY 2026 Adopted Budget, vol. 1, “Appendix.”

[21] The description of the difference between the FY 2026 FEAR estimate and the budgeted departmental expenditures as “working capital” is a misnomer and not consistent with the commonly used definition of that term. The difference would be more appropriately described as an unallocated reserve on contingency.

[22] OMB, FY 2026 Adopted Budget, vol. 1, 24.

[23] OMB, FY 2026 Adopted Budget, vol. 2, 111.

[24] Harris County Auditor, FY 2025 ACFR, Table 19, 238.

[25] OMB, FY 2026 Adopted Budget, vol. 2, 330–98.

[26] OMB, FY 2026 Adopted Budget, vol. 2, 100–108.

[27] Harris County Auditor, FY 2025 ACFR, Table 19, 238.

[28] The following line items are interspersed through the current budget:

- $6M to expand chronic disease prevention and create 20 positions to support the program.

- $5.8M to expand access to comprehensive reproductive healthcare options for low-income, uninsured Harris County residents.

- $23.7M to expand access to counseling services for youth and families and tools and training to support emotional health.

- $7.7M to support maternal and child health programs.

- $6.4M committed to the small business assistance program.

- $17.6M to expand apprenticeship opportunities for underemployed residents.

- $14.2M to provide high-quality job training, technical or sector-based training, licenses, degrees, and wraparound services.

- $57.5M to contract with childcare centers to serve 800 families.

- $17.7M to support funding for childcare providers to construct, remodel, and expand projects for early learning and care space.

- $16.5M to support quality initiatives across all types of childcare services.

- $14.9M to support early childhood programs.

- $8.4M to support summer programs for children to address educational disparities.

- $7.3M to provide incentives for training childcare workers.

- $4.3M to improve care for young children with disabilities.

- $15M to purchase more than 100 homes to provide affordable housing.

- $7.3M to acquire and pre-develop the Yellow Cab Project, a mix of single-family and multifamily units.

- $4.2M to acquire land to add to the Kingsland Park multifamily development, creating five new affordable units and preserving 141 existing ones.

[29] “Harris County Jail Population Dashboard,” Harris County Sheriff’s Office, based on daily snapshots, https://charts.hctx.net/jailpop.

[30] Harris County Auditor, FY 2025 ACFR, 271.

[31] OMB, FY 2026 Adopted Budget, vol. 1, 36.

[32] Kyle McClenagan, “Bill to Limit Harris County’s Authority over Surplus Toll Road Funds Dies as Legislative Session Ends,” Houston Public Media, June 2, 2025, https://www.houstonpublicmedia.org/articles/news/transportation/2025/06/02/522887/bill-to-limit-harris-countys-authority-over-surplus-toll-road-funds-dies-as-legislative-session-ends/.

[33] For a more complete discussion of the financial condition of Harris County Toll Road Authority (HCTRA), see Bill King, Joyce Beebe, and John W. Diamond, “Harris County Toll Roads Are Generating Large Surpluses,” Rice University’s Baker Institute for Public Policy, August 14, 2025, https://doi.org/10.25613/RAMW-WT48.

[34] Between 2023–24 and 2024–25, population growth changed from 2.04% to 0.97%, with most changes resulting from net migration instead of vital events, such as births and deaths (“County Population Totals and Components of Change: 2020-2025,” United States Census Bureau, March 2026, https://www.census.gov/data/tables/time-series/demo/popest/2020s-counties-total.html).

[35] This figure is a cumulative total calculated across two US Census Bureau data series tracking domestic migration. For the period 2020–25, Texas recorded a net domestic migration of -162,694, as documented in "Annual Estimates of the Resident Population, Estimated Components of Resident Population Change, and Rates of the Components of Resident Population Change for States and Counties: April 1, 2020 to July 1, 2025 (CO-EST2025-COMP-48)," US Census Bureau, Population Division, https://www.census.gov/data/tables/time-series/demo/popest/2020s-counties-total.html. For the period 2016–20, the net domestic migration totaled -164,327, derived from the sum of columns CD through CH in row 2670 of "Annual Resident Population Estimates, Estimated Components of Resident Population Change, and Rates of the Components of Resident Population Change for States and Counties: April 1, 2010 to July 1, 2020 (CO-EST2020-alldata)," US Census Bureau, Population Division, May 2021, https://www.census.gov/programs-surveys/popest/technical-documentation/research/evaluation-estimates/2020-evaluation-estimates/2010s-counties-total.html. Together, these periods account for a cumulative net domestic migration of -327,021.

[36] For 2025 Harris County Certified Roll, single family residential housing taxable value = $297,321,053,343 and total value on roll = $677,609,464,691 — this is about 44% (“HCAD Jurisdiction Recap Report,” Harris County Central Appraisal District, https://hcad.org/hcad-resources/hcad-reports/jurisdiction-recap-report).

[37] Natalie Weber and Julianna Washburn, “Greg Abbott Touts Campaign Plan to End School Property Taxes in Texas During Houston-Area Visit,” Houston Public Media, April 1, 2026, https://www.houstonpublicmedia.org/articles/news/politics/2026/04/01/547759/texas-school-property-tax-cut-plan-greg-abbott-galveston/.

[38] Bipartisan Policy Center, “U.S. Opinions on Housing Legislation: A BPC/Advocus Partners Poll,” May 8, 2026, https://bipartisanpolicy.org/article/u-s-opinions-on-housing-legislation-a-bpc-advocus-partners-poll/.

[39] This is the view expressed by Harris County and Harris County Central Appraisal District officials interviewed by the researchers.

[40] Ariel Guerrero, “Distressed Buildings Dragging Down Houston’s Office Market,” Avison Young, February 10, 2026, https://www.avisonyoung.us/w/distressed-buildings-dragging-down-houston-s-office-market.

[41] Melissa Enaje, “World’s Largest Data Center Market? One Houston-Area Suburb Prepares for Texas’ Tech Boom,” Houston Public Media, June 8, 2026, https://www.houstonpublicmedia.org/articles/news/in-depth/2026/06/08/553915/missouri-city-data-centers/; Millie Hoe, “Texas-Sized Investment: Eli Lilly Announces $6.5Bn Houston Manufacturing Facility,” BioProcess International, September 24, 2025, https://www.bioprocessintl.com/facilities-capacity/texas-sized-investment-eli-lilly-announces-6-5bn-houston-manufacturing-facility; Danny Levin, “Greater Houston Home to $15 Billion Worth of Projects Under Construction,” Industrial Info resources, January 8, 2026, https://www.industrialinfo.com/news/article/greater-houston-home-to-15-billion-worth-of-projects-under-construction--351513.

[42] OMB, FY 2026 Adopted Budget, vol. 1, 99–105.

[43] Anthony E. Boardman et al., Cost-Benefit Analysis: Concepts and Practice, 5th ed. (Cambridge University Press, 2018), 13–6 and 430–2.

[44] This is the view expressed by Harris County and Harris County Central Appraisal District officials interviewed by the researchers.

[45] Dallas County, Adopted Budget for Fiscal Year 2026, updated June 29, 2026, https://stories.opengov.com/dallascountytx/9beb778d-aa91-4d04-89c8-b539ba498c07/published/bsQCNJA5G?currentPageId=68c42dccab46cdb3a601f2fa. Dallas County started using this cloud-based system in 2021, “thereby providing transparency and efficiency to the budgeting process” (Dallas County FY2022 Budget, Fiscal Year 2021–2022, 7, https://www.dallascounty.org/Assets/uploads/docs/budget/fy2022/FY2022-BudgetBookDetail-OnlineVersion-Adopted-FINAL.pdf).

This publication was produced by Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by outside experts prior to release. Any errors or omissions are solely the responsibility of the author(s).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.