Author(s)

Overview

Indigenous peoples represent a small share of the global population, yet they are disproportionately affected by natural resource extraction and large-scale industrial projects. Their lands overlap with at least one-third of the world’s documented environmental conflicts. Where mining activities frequently affect Indigenous territories — as in resource-rich northern Chile — Indigenous engagement is a critical factor for project advancement.

This brief examines how copper and lithium development in northern Chile intersects with Indigenous communities, and how major mining operators — primarily from the United States and Canada — approach Indigenous engagement in the context of the global energy transition. It draws on the production footprint and project portfolios of companies with major operations in Arizona and Nevada (U.S.), British Columbia and Ontario (Canada), and Chile’s Atacama and Antofagasta regions.

Why Chile Matters for the Energy Transition

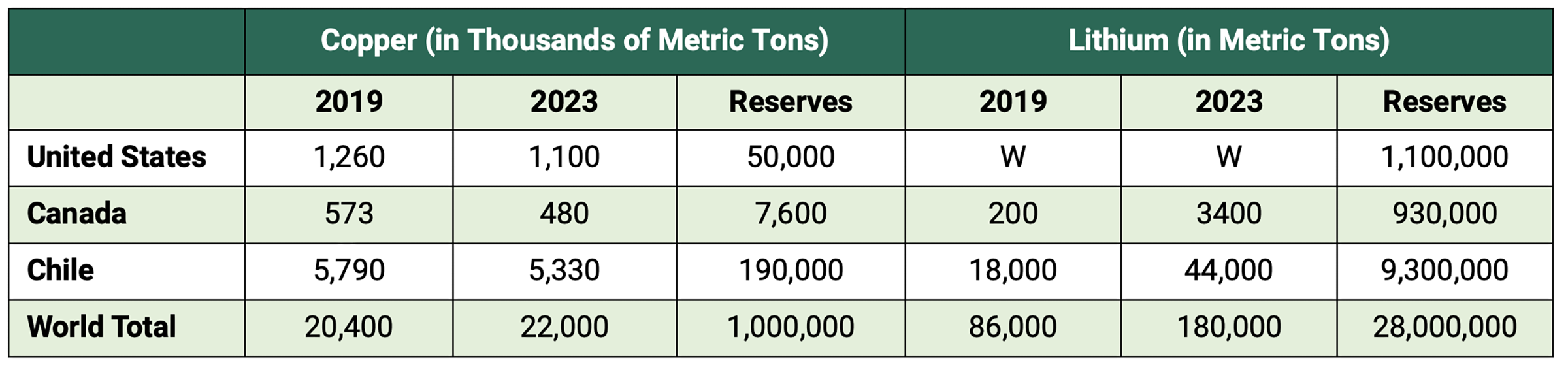

Chile is a global leader in critical minerals, ranking as the world’s top copper producer with roughly 24% of global output and as the second-largest producer of lithium, which is sourced primarily from high-quality brine deposits in the Atacama Salt Flat in northern Chile. Lithium and copper are essential for electrification, battery manufacturing, renewable energy expansion, and the rapidly growing clean-technology supply chain. As global demand accelerates, the economic stakes for Chile, and the environmental and cultural stakes for Indigenous communities living near these deposits, continue to rise. Table 1 summarizes copper and lithium production and reserves across Chile, the United States, and Canada.

Table 1 — Copper and Lithium Production and Reserves

Note: “W” — data withheld to avoid disclosing company-specific information.

Mining Access and Resource Governance

Chile

Chile’s mineral resources are owned by the state. Most minerals can be explored and exploited through concessions, with the major exception of lithium, which requires a special lithium operation contract (CEOL). Water rights, essential for mining operations, are granted permanently to private users by the state.

Key characteristics:

- Established system of mining concessions.

- Lithium governed under a separate regulatory regime.

- Water rights governed separately from mineral rights.

- High regulatory certainty but an evolving lithium framework.

United States

Minerals are generally privately owned unless they are located on federal or Indigenous lands. In Arizona and Nevada, the Bureau of Land Management (BLM) administers federal mineral rights, permitting, and environmental compliance. Mining on tribal lands requires leases made through federal agencies and agreements with the tribes themselves.

Canada

The Crown owns subsurface minerals in most provinces. First Nations’ land claims and treaties vary by region, shaping consultation requirements and benefit-sharing structures. Canada’s use of impact benefit agreements (IBAs) provides a valuable international model for structuring successful community partnerships.

Chile’s Copper and Lithium Industry Landscape

Chile’s copper sector is driven by a mix of state-owned and private operators, with major production by the National Copper Corporation (CODELCO) and the National Mining Company (ENAMI, Chile’s state-owned mining company), alongside global companies such as BHP, Freeport-McMoRan, Anglo American, and Antofagasta Minerals. These firms, together with numerous mid-size and independent operators, drive much of Chile’s mining economy. Over the past decade, mining has contributed approximately 10.5% of the national GDP and more than half of Chile’s total export revenues. Contributions by both state operated and private mining companies to the government’s budget include dividends, taxes, royalties and fees. These have fluctuated over the years, but on average they represent about 6% according to the COCHILCO (Chilean Copper Commission) statistical report.

Lithium production is dominated by SQM and Albemarle. In 2023, the government introduced its National Lithium Strategy, signaling a shift toward a public-private partnership model. Although the regulatory framework is still evolving, new project announcements continue, including:

- Rio Tinto has entered separate partnerships with CODELCO for the Maricunga project and with ENAMI for the Salares Altoandinos development.

- Wealth Minerals has formed a joint venture with the Quechua Indigenous Community of Ollagüe, giving local stakeholders an ownership position in the Kuska project.

These efforts reflect a broader movement toward deeper collaboration among the state, private operators, and Indigenous communities in shaping the future of lithium development.

Regulatory and Institutional Framework in Chile

Chile’s mining sector is governed by an extensive and interlinked regulatory framework, supported by a wide range of economic, environmental, and technical institutions. This regulatory architecture shapes every stage of project development, from land access, permitting, and water use to environmental compliance and Indigenous consultation. These key institutions are structured around the following categories: economic and fiscal authorities, mining oversight, environmental regulation, and innovation and development.

Economic and Fiscal Authorities

- Ministry of Finance — Manages national budget and the mineral taxes, royalties and state company revenues.

- Central Bank of Chile — Oversees exchange rate policy and foreign currency management.

Mining Oversight

- Ministry of Mining — Provides policy direction and sector development.

- National Geology and Mining Service (SERNAGEOMIN) — Deals with geological surveys, mine safety, and technical regulation.

- CODELCO and ENAMI — Serve as state-owned operators and project partners.

- COCHILCO — Conducts statistical analysis, market intelligence, and strategic advice.

Environmental Regulation

- Environmental Evaluation Agency (SEA) — Conducts environmental impact assessments.

- Superintendency of the Environment (SMA) — Enforces compliance and issues fines.

- Environmental Courts (Northern, Central, Southern) — Adjudicate environmental disputes.

- Ministry of the Environment (MMA) — Steers policy and national environmental strategy.

- Biodiversity and Protected Areas Service (SBAP) — This newly created body oversees ecosystems.

- General Directorate of Water (DGA) — Allocates and regulates water rights.

Innovation and Development

- Chilean Economic Development Agency (CORFO) — Manages economic development, innovation, and financing.

- Institute of Clean Technologies (ITL) — Functions as a research and development (R & D) hub for green hydrogen, solar, lithium materials, and low-emission mining processes.

- Public Institute for Lithium and Salt Flat Research (INLiSa) — Guides sustainable lithium development.

Indigenous Governance and Legal Context

Northern Chile’s Indigenous communities — primarily Atacameño (or Lickan Antay, their self-designation) and Quechua groups — are supported by a legal framework that recognizes historical land rights and mandates consultation.

Key components include:

- Indigenous Law no. 19.253 (1993) — Designates Indigenous lands and water rights.

- National Corporation for Indigenous Development (CONADI) — Promotes development of Chile’s Indigenous people.

- Indigenous Development Areas (IDAs) — Identify areas with large Indigenous populations for targeted development programs to improve living conditions and cultural protection.

- Indigenous and Tribal Peoples Convention (ILO Convention no. 169) — Mandates consultation with and participation of Indigenous communities (ratified by Chile).

- Environmental Tribunal for the Northern Region — Adjudicates Indigenous-related disputes.

- Ministry of Social Development — Oversees Indigenous affairs, development programs, and Indigenous representation in policy.

These frameworks are increasingly influential as Indigenous communities assert greater control over land stewardship, water resources, and cultural heritage.

Challenges at the Intersection of Mining and Indigenous Lands

Based on the social responsibility reports and annual reports of the companies involved, several persistent issues shape the relationship between mining and Indigenous communities:

- Water scarcity in the Atacama Desert, exacerbated by brine extraction and climate variability.

- Cultural heritage protection, including sacred sites and ancestral landscapes.

- Regulatory uncertainty around the evolving lithium strategy.

- Environmental degradation and concerns over long-term impacts on salt flats.

- Distribution of economic benefits, particularly for remote communities.

- Ongoing legal disputes and appeals through environmental tribunals.

These challenges make robust engagement and transparent governance essential for long-term project viability.

Indigenous Communities and Corporate Strategy

Although most of Chile’s Indigenous population lives in the south, the original communities of the north play a central role in shaping mining development because many copper and lithium operations sit near their ancestral lands. These communities interact with companies both through formal associations and direct engagement when projects are located in the vicinity.

As mentioned, a number of major international companies operate in northern Chile, including Albemarle (lithium) and BHP, Freeport-McMoRan, Anglo American, and Antofagasta Minerals (copper). State-owned companies such as CODELCO and ENAMI also play significant roles in both copper and emerging lithium ventures. Newer entrants, including Wealth Minerals and Rio Tinto, are expanding their presence in the region.

To secure long-term support and maintain their social license to operate, mining companies have adopted a range of approaches to Indigenous engagement.

- Albemarle has established a benefit-sharing agreement with the Council of Atacameño Peoples for operations in the Salar de Atacama.

- BHP is developing an Indigenous Peoples Plan focused on community-defined social and economic goals.

- Freeport-McMoRan emphasizes education, skill-building, and local leadership development.

- Wealth Minerals has taken a more collaborative step by giving the Quechua Community of Ollagüe a 5% ownership stake in its Kuska lithium project.

These models illustrate a broader shift across the sector. As mineral demand rises and mining expands deeper into Indigenous territories, companies are increasingly relying on strong environmental, social, and governance (ESG) standards, transparent communication, and long-term agreements to build trust. Many operators now seek free, prior, and informed consent in line with the United Nations Declaration on the Rights of Indigenous Peoples. There is also a growing trend toward multi-decade partnerships rather than short-term consultations tied to individual projects.

Companies are further strengthening relationships through local procurement, Indigenous workforce training, scholarships, and community investment. Water stewardship, cultural heritage protection, and environmental monitoring have become standard components of these agreements, particularly in sensitive areas like the Salar de Atacama. Independent certifications and audits, such as the Copper Mark and the Initiative for Responsible Mining Assurance (IRMA), add an additional layer of accountability, while advisory boards and grievance mechanisms give communities formal channels for ongoing dialogue.

Together, these efforts reflect an evolving recognition that Indigenous inclusion is not peripheral but essential to the long-term success and legitimacy of mining operations in northern Chile.

Conclusions and Recommendations

A successful and sustainable energy transition hinges on the availability of critical minerals such as copper and lithium, the focus of this brief. To secure long-term success, the following actions should be considered:

- Partnership Expansion — Expanding strategic partnerships between Indigenous communities, universities, and technical institutes.

- Workforce Pathways — Developing workforce pathways enabling Indigenous workers to join high-skilled mining and clean-tech jobs.

- Sustainable Innovation — Supporting R & D and innovation to reduce environmental impacts, particularly water use in lithium brine extraction.

- STEM Investment — Investing in STEM education and training for Indigenous youth.

- Local Enterprise — Promoting Indigenous-owned service providers and infrastructure, enhancing local economic multipliers.

- Regulatory Collaboration — Deepening advocacy and collaboration with local and national governments to strengthen regulatory predictability and community benefits.

By integrating Indigenous priorities into the national mineral strategy, Chile and its international partners can enhance community trust, secure project continuity, and ensure that the benefits of critical mineral development are broadly and equitably shared.

Acknowledgment

With appreciation to Tilsa Oré Mónago, a Baker Institute fellow in energy and market design, for her research support.

This publication was produced on behalf of Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by external experts prior to its release. Any errors are the responsibility of the author(s) alone.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.