Last week, House Speaker Nancy Pelosi proposed retroactively repealing the $10,000 cap on state and local tax (SALT) deductions as part of the next financial relief bill. Although many Americans are facing difficult financial situations, a repeal of the SALT deduction would almost exclusively benefit the highest income households. As the federal government scrambles to deal with the economic fallout of the Covid-19 pandemic, relief efforts should be focused on minimizing the severity of the impending recession and helping those most in need. In contrast, a retroactive repeal of the SALT deduction cap is regressive and does little to mitigate the economic downturn.

The Tax Cut and Jobs Act of 2017 capped the SALT deduction at $10,000 — a move seen by many Democrats as an effort to disproportionately harm high-tax states. Proponents of the SALT deduction argue that state and local governments provide important public goods, such as education and health care, and that these services should be encouraged through the federal tax code. They also argue that SALT deductibility can offset differences in the cost of living across regions. Opponents of the SALT deduction argue that it encourages state and local governments to levy higher taxes and increase spending. Even if the federal government wanted to encourage certain expenditures, opponents argue that such programs could be funded directly through federal grants rather than indirectly through tax deductions for high earners.

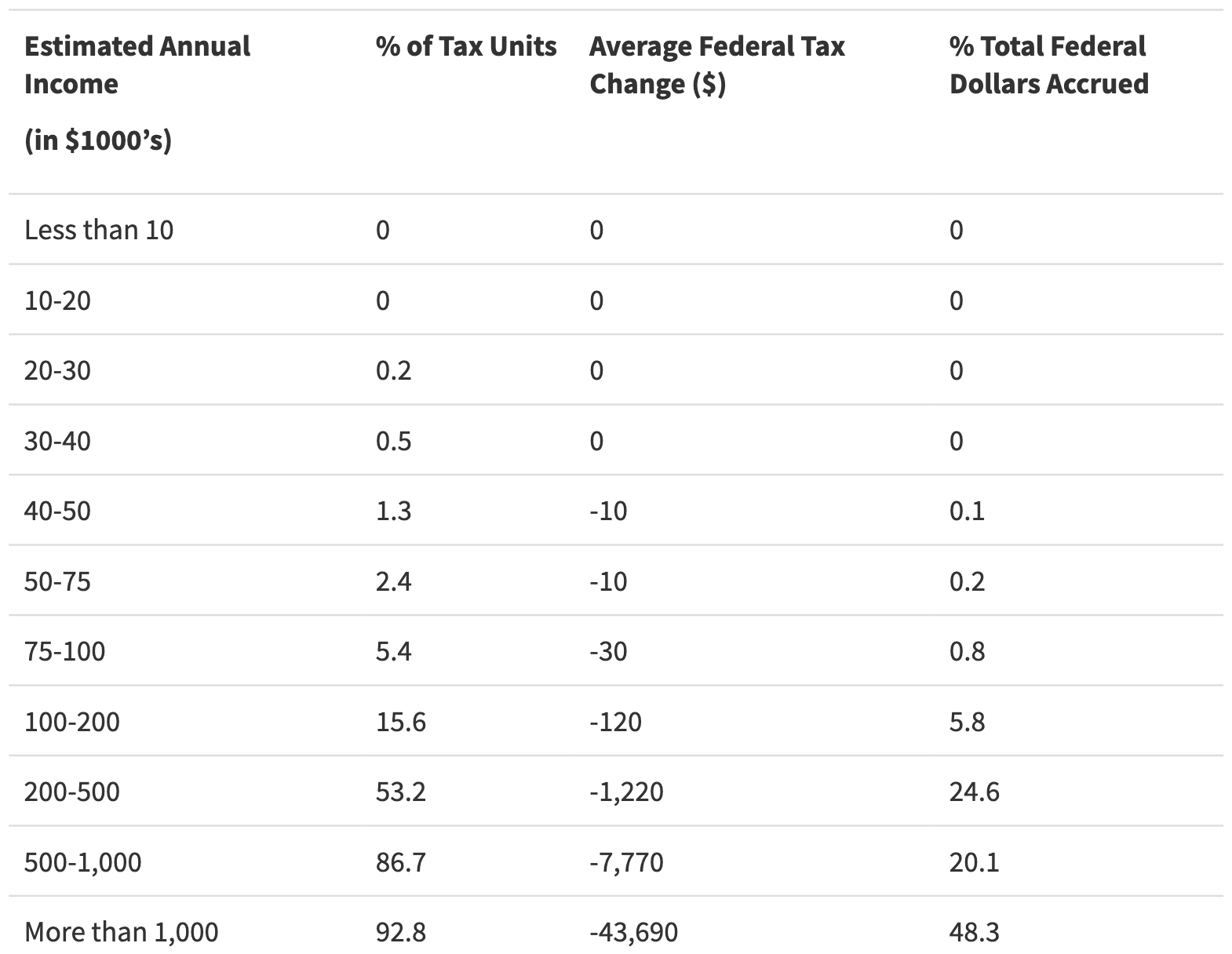

In 2018, the Tax Policy Center evaluated the distributional impact of a full repeal of the SALT deduction, which is summarized in the table below. The “Average Federal Tax Change” column shows the estimated benefits, broken down by income groups, and the column titled “% of Tax Units” gives the share of taxpayers affected by the proposal. According to these estimates, taxpayers making below $40,000 would not benefit under this proposal. Taxpayers making between $40,000 and $100,000 would receive an average benefit of around $10-$30, and less than 6% of these households would any benefit. At the opposite end of the income distribution, taxpayers making over $1 million would receive an average payment of $43,690, and more than 92% of high earners would receive a benefit.

The Joint Committee on Taxation recently estimated that repealing the cap on the SALT deduction would cost the federal government $77 billion. The far right column in the table shows how the benefits would be distributed by income group. Nearly half of all benefits would accrue to taxpayers earning more than $1 million, while only 1.1% of the benefits would accrue to those making less than $100,000.

To be fair, Pelosi’s spokesman Henry Connelly claimed that the tax cut would be modified and limited to benefit middle-class earners. But where would policymakers draw the line? Average benefits of up to $30 for households earning below $100,000 seem ineffective relative to other proposals. For the taxpayers earning between $100,000 and $200,000, the average payment would be $120, but even then, only 15.6% of those households would receive any benefit. Anyone making over $200,000 could hardly be characterized as “middle class,” since the Congressional Budget Office reports that such households are near the top 10% of U.S. household incomes.

Even before the current crisis, soaring government debt and deficits made efforts to repeal the SALT deduction cap difficult to justify. These efforts have become even less defensible given the growing concerns over a deep economic recession and mounting debts following the previous fiscal policy responses. Rather than providing benefits to the highest earners, policymakers should provide funding based on who needs it the most and where it would make the biggest difference: the unemployed and struggling businesses. With a variety of effective fiscal policy solutions available, an expansion of the SALT deduction seems wasteful and unnecessary.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.