Author(s)

This article is also featured in Energy Insights, which reflects a sample of ongoing research across the Center for Energy Studies’ diverse programmatic areas, all addressing the ever-evolving energy challenges across Texas, the U.S., and the globe. Read more from the inaugural edition.

The Premise

Energy transitions are complex. Integrating new technologies to achieve scalable solutions requires coordination along existing supply chains — in some cases, the development of new supply chains — and involves economics, politics, and regulation. Market design that promotes transparency and price formation is critical to attract investment that is sufficient to achieve stated aspirations. Moreover, scarcity is present in many dimensions for all forms of energy — resources, raw materials, land, water, human capital, logistics, etc. — yet it is rarely recognized in its entirety. For instance, wind and solar are renewable sources of energy, but harvesting them for delivery of energy services requires land and various types of materials, such as plastics, resins, lubricants, minerals and metals, etc., which are all depletable.

As energy markets transition, understanding the roles of legacy, scale, and technology is critical to what the future will bring. First, legacy is defined by existing infrastructures and energy delivery systems, and it is the foundation on which change will be built. Moreover, legacy is different everywhere, having been influenced by regional comparative advantages. Second, scale matters because energy systems are large and must accommodate energy affordability and reliability, while also supporting continued economic growth. Finally, technology constantly evolves, and ultimately signals how different energy sources will compete.

The influences of legacy, scale, and technology will render efforts to decarbonize energy systems to look different everywhere, hinging on resource endowments — nature, minerals, energy, human capital, etc. — that define comparative advantage. In fact, the current global energy system is already characterized by very different regional energy portfolios for this very reason. Hence, lowering the carbon footprint of energy systems will require multiple solutions given the scale of existing energy systems. Economics matter, and the principle of comparative advantage is key to understanding what will happen and where it will happen in a cost-effective manner.

Market structures also matter. If there is limited market participation for activities involving new technologies, deals to support investments along the supporting supply chains must be bilateral. Bilateral market arrangements require identification of a specific counterparty with sufficient risk tolerance, which can limit the scale of the activity. If, however, there are many market participants — i.e., market depth and liquidity — investments along the supply chain face lower risk because direct counterparty interaction is not needed. This leads to greater levels of investment.[1]

As energy transitions unfold, governments must remain mindful of an old, but important, concept: energy security. History has taught that energy disruptions are highly correlated with wholly undesirable macroeconomic dislocation, and recent events — i.e., Russia’s invasion of Ukraine — have provided a stark reminder of the importance of energy security. As such, it will remain a central consideration to policymaking, with different regions taking different approaches, typically prioritizing domestic energy sources whose supply chains are less exposed to foreign influence.[2]

All of this considered in the context of energy transitions, it is important to understand the “what” and “why” of the most impactful transitions affecting energy markets in the last 25 years: the shale revolution in the U.S. and demand growth in Asia. Each drove profound changes in the global energy system, impacting supply-demand balance, global trade, and geopolitics. Breaking it down, the shale revolution is a product of innovation in the upstream that was able to leverage existing infrastructures, market structures, and human capital to rapidly alter the U.S. upstream. The tremendous demand growth seen in Asia since the turn of the century is a product of rapid economic growth that fueled new demands for energy. Hence, the two biggest drivers of change in energy markets over the last 25 years have been: 1) innovation and 2) economic growth. In fact, these two factors have always been the largest instigators of long-term structural change in energy systems, and they are likely to remain so for the foreseeable future. Understanding how they will manifest going forward is vital to understanding energy transitions.

Energy Transitions and an Optimal Energy Crisis?

An article in “The Energy Journal” published in 2016 showed that a shift from fossil fuels to renewable energy could be accompanied by a protracted period of higher energy prices and slower economic growth, i.e., an energy crisis.[3] The crisis is optimal, in a neoclassical growth setting with endogenous technological progress, because capital is shifted away from the incumbent energy resource (fossil fuels) to the new entrant (renewables), which forces the cost of energy to rise to cover the capital costs of remaking the energy system. Among other findings, a fundamental lesson in that research is not that a protracted energy crisis is looming. Rather, it is that capital chases returns, so returns must be sufficient to drive investment. This is critical for technology adoption, the role of subsidies, and fixed costs of deploying new energy technologies.

The Promise of New Technologies

Over the last several years, in the U.S. and elsewhere, policies — such as direct subsidies and portfolio standards — and cost-reducing innovations have propelled wind and solar energy growth. Recently, policies directed at fostering energy transitions, such as the Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA), have expanded the scope of subsidies for multiple new technologies.

Shifts in investor and consumer sentiment are also motivating firms to take steps to reduce their net CO2 footprints. Many firms have issued net-zero CO2 emission decrees and have begun to publish annual sustainability reports. In doing so, they are bringing a relatively new degree of transparency to their operations as they respond to investor pressures to reduce their environmental footprint and demonstrate performance.

So, the stars seem aligned to propel new technologies and drive rapid transitions. But what does that mean?

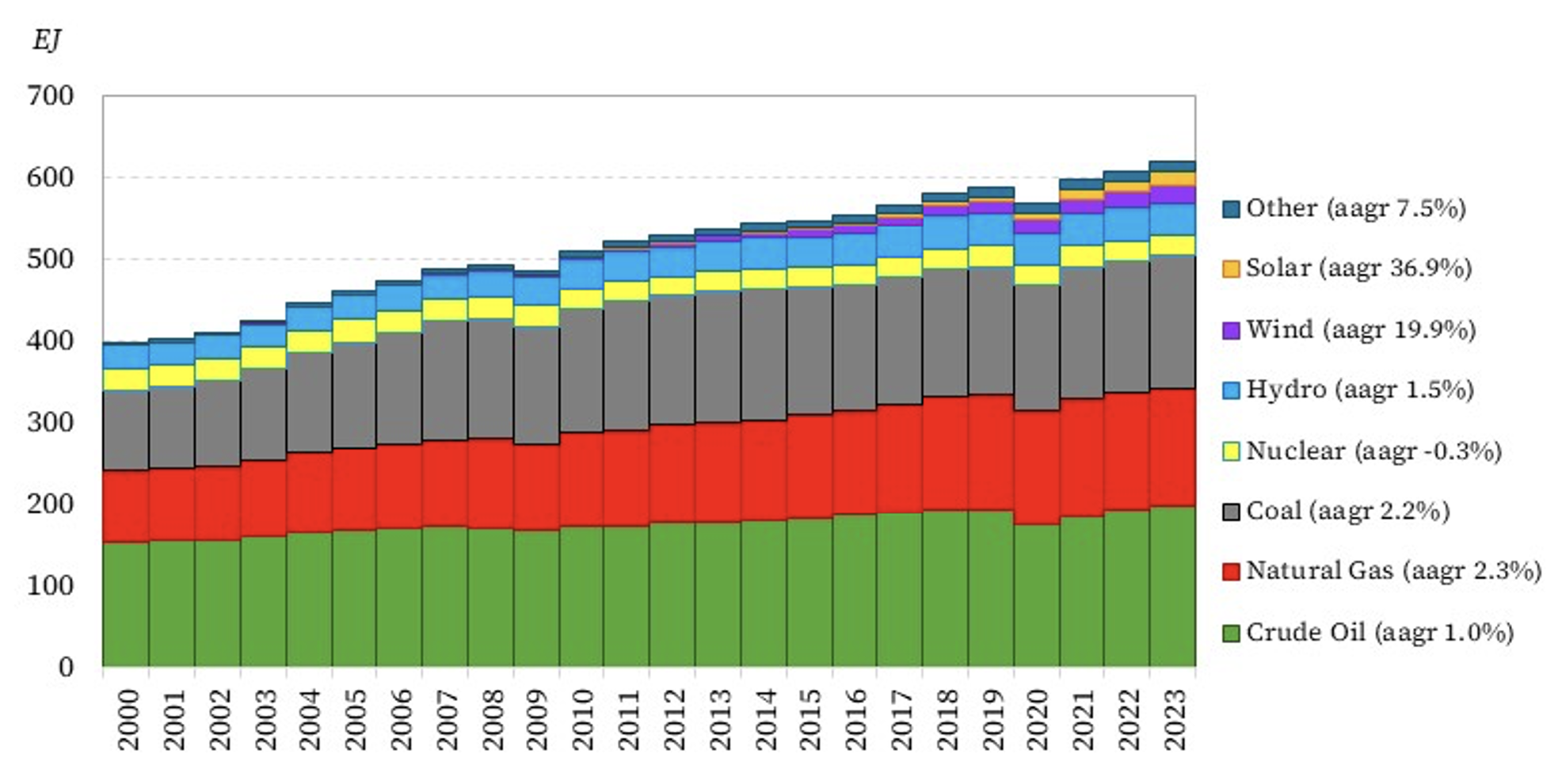

The scale of energy systems and the legacy of infrastructures that characterize them means that the astonishing growth of wind and solar energy have had very little impact on fossil energy resources. In fact, oil demand increased by an annual average of 1.1 million barrels per day from 2000 to 2023, with natural gas demand growing at an annual average clip of 6.5 billion cubic feet per day and coal use increasing by 182.8 million metric tons per year over the same period. As can be seen in Figure 1, focusing on average annual growth rates (AAGR) of new energy sources does not recognize the scale of other energy sources, or the growth rates needed to replace them.

Figure 1 — Global Primary Energy Use by Source, 2000–23

Note: The average annual growth rate (AAGR) for the period pictured is included in the legend.

Suffice it to say, fossil fuels will very likely be an important part of the energy mix for some time. Accordingly, the portfolio of options to successfully decarbonize economic activity must expand. Fortunately, the list of technologies that show promise is growing, as indicated in Table 1. But we are still left to wonder: Which technologies will succeed?

Table 1 — Technologies To Reduce Emissions

Coordination and Supply Chains

Not all technologies prove successful. History teaches us this repeatedly. Nevertheless, policy can play a constructive role, if it recognizes the critical role of supply chains and ways technology integrates into them.

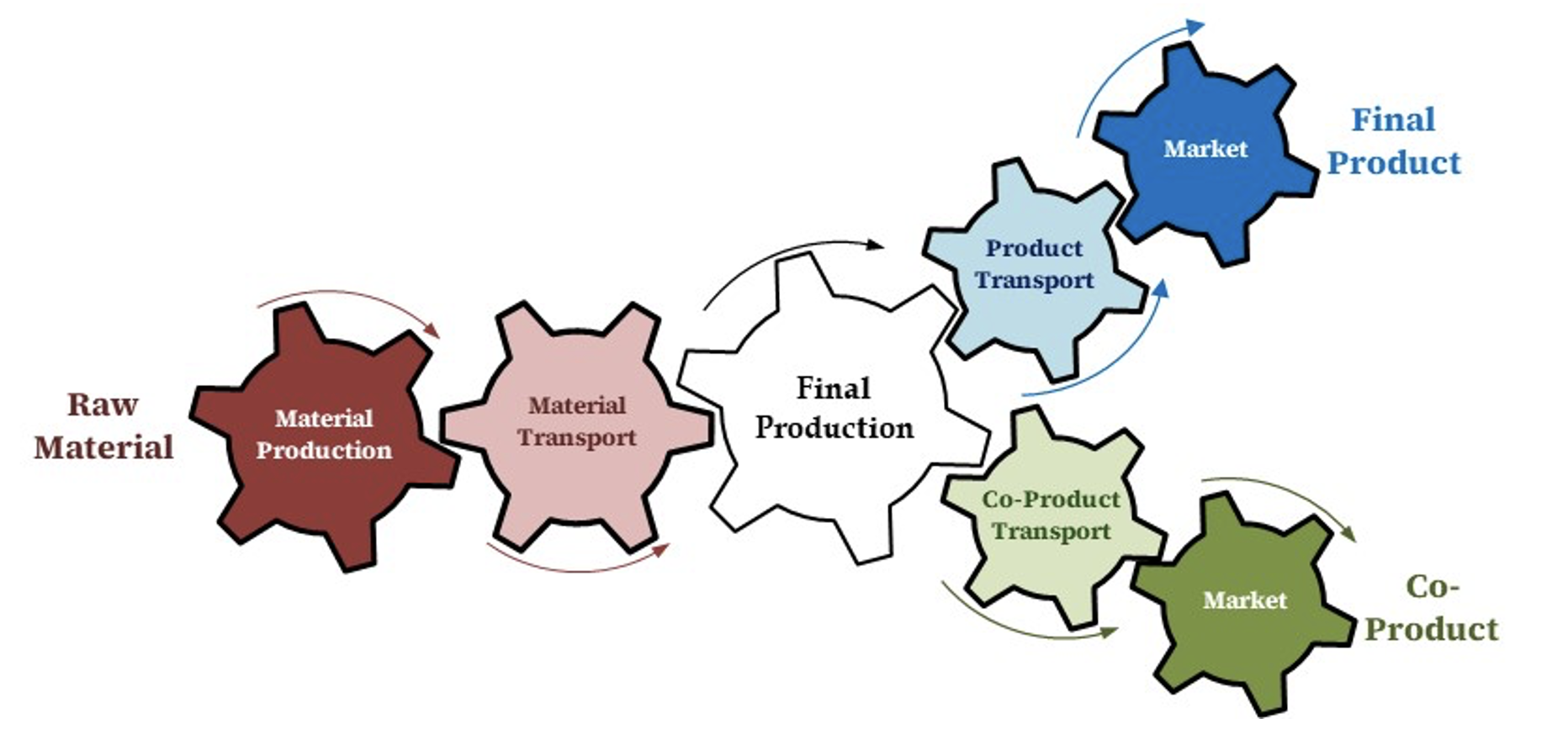

Every production process involves a supply chain connecting raw material inputs to a production process to deliver a final product, and potentially a coproduct, to end-users (Figure 2). If any part of the complex set of interactions along a supply chain breaks down, coordination failure ensues, and the commercial viability of investments at any point in the supply chain is compromised.[4]

Figure 2 — Supply Chains and Coordination

Importantly, value must be generated at every point in the supply chain for it to develop from the onset and then remain functional. As the capital intensity of each step in the supply chain increases, the value created at that step must increase commensurately to cover cost. For energy, technology is embodied in large, long-lived infrastructure that requires significant upfront capital investment. Once a petrochemical facility or power plant is built, for example, it takes years to recoup the massive capital outlay, and technology is embodied in the infrastructure. As such, the fixed cost burdens of new technologies must not only recoup their own fixed costs, but the overall system must also cover stranded costs for equipment that may be retired prematurely, or risk insolvency.

The Parable of Widgets: A Tale of Promise Unfulfilled and the Cost of Adoption

To understand how this impacts technology adoption, consider the following. Imagine we work in a university lab that is focused on production technologies for a product called, “widgets.” In this world, widgets are a manufactured good that is in high demand. One day, we have a breakthrough with a technology we have been developing that will cut the cost of producing widgets in half. We quickly work with university administration to secure patents and intellectual property protections, and the university issues a press release about our disruptive, game-changing technology that stokes a massive media response. All is good in our lab.

Next, we have a conversation with the world’s largest widget manufacturer about our technology. They are intrigued, and we are convinced they will license the rights to our technology so they can deploy it, guaranteeing years of royalty revenues for our lab and the university. They ask for six months to perform their own internal assessment, signing all the necessary intellectual property protections. All is good in our lab.

After six months, the company comes back to us, declining the option to continue discussions. We cannot understand what went wrong. Then, six months later, compounding our frustration, we learn the company has adopted a technology from a competing lab at another university that only cuts production costs by 10%. This, of course, throws us into a frenzy. Our mindset devolves into conspiracy theories, and we even agree to write a book about it. All is not good in our lab.

What happened?

The company, when performing its internal assessment, evaluated the technology’s impact on their production cost, which confirmed what we had found in our lab. But they also evaluated the adoption cost and found it to be exceedingly high. They determined that they would need to replace multiple parts of their supply chains, which are all capital intensive. This presented a fixed cost barrier to adoption for the technology that the cut in production costs could not overcome.

In contrast, the technology from the competing lab could simply bolt into existing — or legacy — infrastructure, making its fixed cost of adoption very low. So, even though the production costs did not fall as much, its adoption was commercially viable.

Such complexities abound in any capital-intensive industry, like energy. It has a lot to do with why disruptive technologies are exceedingly rare in such industries. Even wind and solar technologies are not disruptive, as they can effectively bolt into existing electricity grids to provide energy without requiring a massive overhaul of the entire system. If a new technology requires development of an entirely new supply chain, then it may face overly burdensome fixed costs of adoption, which can push the technology into the valley of death. Technologies that can leverage legacy infrastructures generally face fewer hurdles to adoption and can more easily diffuse into the market.

The Uncertain Impact of Policy

The current wave of policy interventions to propel new technologies and accelerate energy transitions is not a new phenomenon. Consider, for example, the energy crises of the 1970s and 1980s. High energy prices coupled with stagnating to declining domestic oil and gas production triggered concerns about energy security and economic growth. This led to policies that favored domestic energy sources, such as coal, nuclear, wind, and solar, along with bans or restrictions on certain oil and gas related activities in effort to ensure adequate domestic supplies. Even large segments of industry threw support behind robust intervention. At the request of the Secretary of Energy, the National Petroleum Council (NPC) examined these concerns and made policy recommendations in a report from 1987 that expressed several familiar sentiments:

“The decline in … industry capability … when combined with growing demand, will result in even greater dependence on imports. The nation must address the increased vulnerability that will inevitably result from a continuation of these trends.

…

[There were numerous] proposals that call for immediate intervention by the U.S. government. These include, singly or in combination: establishing floor prices or import fees; levying consumption taxes; and providing domestic production and/or exploration incentives.”[5]

Little has changed in the last four decades.

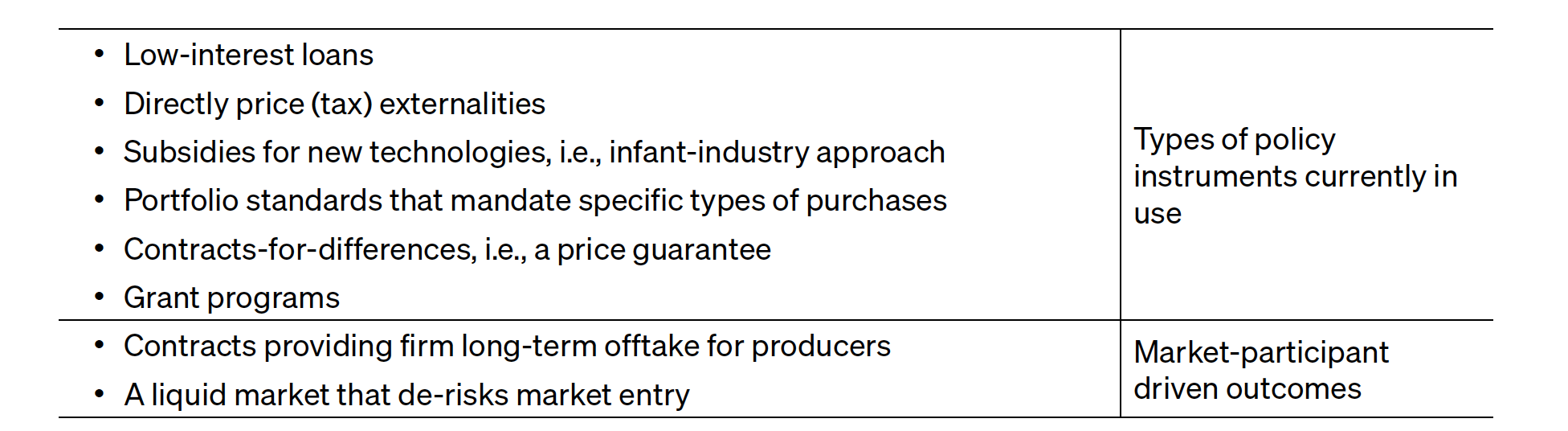

Currently, the U.S. government is putting support behind several different market interventions, each aimed at tilting investment into new energy technologies. Of course, attracting investment into each part of a supply chain is dependent on the returns earned. Only positive returns to invested capital will drive scale for any technology, and if a comparative advantage can be captured, there are policy levers, as well as market participant actions, that can facilitate technology uptake (Table 2).

Table 2 — Types of Interventions

There are, of course, costs and benefits with any intervention. The primary impacts, as well as any unintended consequences, will ultimately define which interventions are successful. Notably, history in the largest energy commodity markets, such as crude oil and natural gas, teaches us that the emergence of market liquidity tends to result in the most scalable changes because it de-risks market entry and provides flexibility.

The IIJA, Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act, and IRA are examples of legislation that aim to accelerate deployment of new energy technology.[6]

- The IIJA, a.k.a. Bipartisan Infrastructure Law, passed the House on July 1, 2021 (vote: 221–201). After amendment, it passed the Senate with broad bipartisan support on Aug. 10, 2021 (vote: 69–30), and became law on Nov. 15, 2021.

- The CHIPS Act passed the House on July 28, 2021 (vote: 215–207). After amendment, it passed the Senate with broad bipartisan support on July 27, 2022 (vote: 64–33), and became law on Aug. 9, 2022.

- The IRA, originally introduced as the Build Back Better Act, was passed on purely partisan lines in the House of Representatives on Nov. 19, 2021 (vote: 220–213). After several amendments, it passed the Senate on Aug. 7, 2022 (vote: 51–50) with the tiebreaking vote cast by Vice President Kamala Harris and became law on Aug. 16, 2022.

Each of these is legislation, so they have staying power, even if they passed along slim party-line margins. Undoing legislation, even when contentious, is difficult.[7] There are pathways for legal challenge, and agency rulemaking based on interpretation of legislation is in the crosshairs following the recent Supreme Court ruling on the Chevron doctrine, although the full ramifications of that ruling remain to be seen.[8] However, the benefits of these legislative acts are likely to accrue most heavily to businesses in Republican-held Congressional districts.[9] Thus, repealing it will be difficult, especially once the benefits begin to impact constituencies in those districts. As to whether these seminal pieces of legislation are truly game-changing, the devil is in the details. Impacts will vary regionally as different regions of the country have distinct comparative advantages and legacy infrastructures that better suit them to capture different benefits of the legislation. But, even then, there is an Achilles’ heel — infrastructure.[10]

How markets are promulgated will also matter. Take hydrogen, for example. With limited market participation, deals to support investments along the value chain must be bilateral, which can limit entry. Transparency and liquidity are important elements of a market that achieves significant scale.[11] Investing in infrastructure is a real option that is only exercised when profitable. In the absence of market depth, a liquidity premium exists that renders option value lower, thus reducing investment. Of course, the path to a transparent, liquid hydrogen market will not be instantaneous. Rather, it will likely evolve as a set of regional utility-style markets that favor incumbency rather than new entry. However, to the extent this leads to regional price dislocations, interstate trade will be encouraged. At that point, the entire regulatory architecture of a national hydrogen market could evolve significantly.

What To Expect

Regardless of which political party is in power, expect more policy debate about energy transitions. Much of this is rooted in the fact that there are costs and benefits that are not distributed evenly. Make no mistake, addressing environmental externalities is a good thing. But so are economic growth, improved standards of living, and social welfare gains. Perceptions about how these are all impacted are at the heart of debates.

In the end, the impacts of policy on economic growth and consumer costs will drive political acceptance. Economic growth has historically been characterized by reducing capital intensity (capital per $ GDP) and dematerialization (reducing the materials per $ GDP).[12] The push to electrify everything with renewables and batteries is pushing the energy system toward higher capital intensity and lower energy density, which is at odds with over a century of modern economic growth. This is made even more problematic by the rising anti-globalization mantra. Subsidizing higher capital intensity endeavors and erecting barriers to potential trading partners have a crowding-out impact. This is not good for economic growth, and it is inflationary. People must still see improvements in standards of living if they are to be supportive of any policy direction. Make no mistake, politicians understand this.

< Previous article | Next article >

Notes

[1] One can think of this through the lens of real options. Investing in infrastructure is a real option. One only exercises the option when profitable. In the absence of market liquidity, a liquidity premium exists that renders the option value lower, thus reducing investment. Liquidity increases scale.

[2] See, for example, Kenneth B. Medlock III, “China’s Coal Habit Will be Hard to Kick,” Barron’s, October 6, 2021, https://www.barrons.com/articles/chinas-coal-habit-will-be-hard-to-kick-51633462019; and Medlock, Amy Myers Jaffe, and Meghan O'Sullivan, “The Global Gas Market, LNG Exports and the Shifting US Geopolitical Presence,” in “US Energy Independence: Present and Emerging Issues,” ed. Jaffe, special issue, Energy Strategy Reviews 5 (December 2014): 14–25, https://doi.org/10.1016/j.esr.2014.10.006.

[3] See, Peter R. Hartley et al., “Energy Sector Innovation and Growth: An Optimal Energy Crisis,” The Energy Journal 37, no. 1 (January 2016): 233–58, http://www.jstor.org/stable/24696708.

[4] Avoiding this risk provides a commercial justification for holding inventories.

[5] National Petroleum Council, Factors Affecting U.S. Oil & Gas Outlook: A Report of the National Petroleum Council, February 1987, npc.org/reports/reports_pdf/1987-Factors_Affecting_US_Oil_n_Gas_Outlook.pdf.

[6] Infrastructure Investment and Jobs Act (IIJA), Pub. L. No. 117-58, 135 Stat. 429 (2021); Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act, Pub. L. No. 117-167, 136 Stat. 1366 (2022); and Inflation Reduction Act (IRA), Pub. L. No. 117-169, 136 Stat. 1818 (2022).

[7] We have seen this in recent history with the Affordable Care Act (ACA), which passed the House of Representatives along party lines and triggered significant debate in subsequent campaigns. However, the ACA has yet to be overturned.

[8] The recent Supreme Court ruling has overruled the Chevron doctrine that held since Chevron U. S. A. Inc. v. Natural Resources Defense Council, Inc., which gave agency interpretation of the statutes they administer priority (Loper Bright Enterprises v. Raimondo, 603 U.S. 22-451 [2024], https://www.supremecourt.gov/opinions/23pdf/22-451_7m58.pdf).

[9] For more on this topic, see “Map: Energy, Environment, and Policy in the US” (Houston: Rice University’s Baker Institute for Public Policy), https://www.bakerinstitute.org/energy-environment-and-policy-us.

[10] Medlock, “Recent Legislation Can Dramatically Impact the US Energy System — If Infrastructure Isn’t an Achilles' Heel” (Houston: Rice University’s Baker Institute for Public Policy, August 7, 2023), https://doi.org/10.25613/7ZT2-WK51.

[11] Medlock and Shih Yu (Elsie) Hung, “Developing a Robust Hydrogen Market in Texas” (Houston: Rice University’s Baker Institute for Public Policy, February 16, 2023), https://doi.org/10.25613/YKKH-8K02.

[12] Medlock and Ron Soligo, “Economic Development and End-Use Energy Demand,” The Energy Journal 22, no. 2 (April 2021): 77–105, https://doi.org/10.5547/ISSN0195-6574-EJ-Vol22-No2-4.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.