Author(s)

In the United States, state and municipal governments rely heavily on consumption tax revenues to finance their expenditures. According to the U.S. Census Bureau, consumption taxation generated $544 billion of revenue in 2015, amounting to 3% of gross domestic product and financing roughly one-third of all sub-federal level expenditures. Roughly two-thirds of consumption tax revenue was generated by sales taxes, while the remaining one-third was generated by excise and other consumption taxes. As of 2017, 45 states and the District of Columbia, as well as municipal governments in 38 states, collect sales taxes,1 while every state and several municipal governments, as well as the U.S. federal government, levy some kind of excise tax.2

Given this extensive dependence on consumption taxation to finance government expenditures, policymakers should carefully consider who bears the burden of the tax.

On the surface, a consumption tax seems simple: a tax that is proportional to the things that we consume. In reality, consumption tax bases are highly partitioned into groups of expenditure items that receive special treatment, either through differential tax rates or through tax exemptions. Housing, for example, is not taxed at the sales tax rate, but rather at the property tax rate. Most health care expenditures, by contrast, are exempt from taxation altogether.

Many argue that sales and excise taxes are regressive based on the strict relationship between annual income and taxes paid. As a household’s income rises, the portion of income allocated to consumption declines, and the portion allocated to savings rises—concepts for which John Maynard Keynes coined the terms “marginal propensity to consume” and “marginal propensity to save.” This decline in consumption as a percentage of income is often used to substantiate claims of consumption tax regressivity. Such a claim obfuscates the fact that savings is just another term for future consumption, which eventually faces similar tax exposure.

Because annual income fluctuates significantly over a lifetime, economist James Poterba argued that annual consumption taxes paid as a fraction of annual income is not a good measure of tax progressivity. Individuals use savings to shift consumption throughout their lives, suggesting that lifetime consumption taxes paid as a fraction of lifetime income is a better measure of consumption tax progressivity. As a proxy for lifetime consumption tax progressivity, Poterba proposed studying consumption expenditure composition as it relates to income. If consumption composition shifts away from taxable items as income increases, then the consumption tax burden falls disproportionately onto households with lower lifetime income, confirming claims of consumption tax regressivity. However, if taxable consumption increases with income, we have no reason to conclude that the tax burden falls more heavily onto households with lower lifetime income.

A particularly interesting feature of sales and excise taxes is that individuals can avoid them by not consuming the taxed items. For example, one could take public transportation to avoid paying sales tax on a vehicle and excise tax on fuel. Because of this differential tax treatment across consumption goods, each household expenditure can be categorized according to whether or not it is included in the sales or excise tax bases. Following Poterba’s method, measuring the relationship between sales- and excise-taxable expenditures and income provides a better indication of how the respective tax burden corresponds to lifetime income.

To test whether high-income earners substitute away from taxable goods, a typical tax base can be reconstructed using the Consumer Expenditure Survey (CEX). This data set contains detailed information regarding household expenditures and income levels. The first step in analyzing the data involves identifying which consumption items are typically included in sales or excise tax bases. The next step involves determining how taxable consumption in each tax base changes with household income. A negative relationship would indicate that the tax burden falls more heavily on low-income households, while a positive relationship would imply the opposite.

Description of Data

This study analyzes data from the 2015 CEX, which documents an estimated 60-70% of all household expenditures at varying granularity of consumption categories.3 Although the expenditure items in the survey do not comprise an exhaustive budget, the CEX still provides the best data available for studying taxable expenditure patterns as they relate to income.

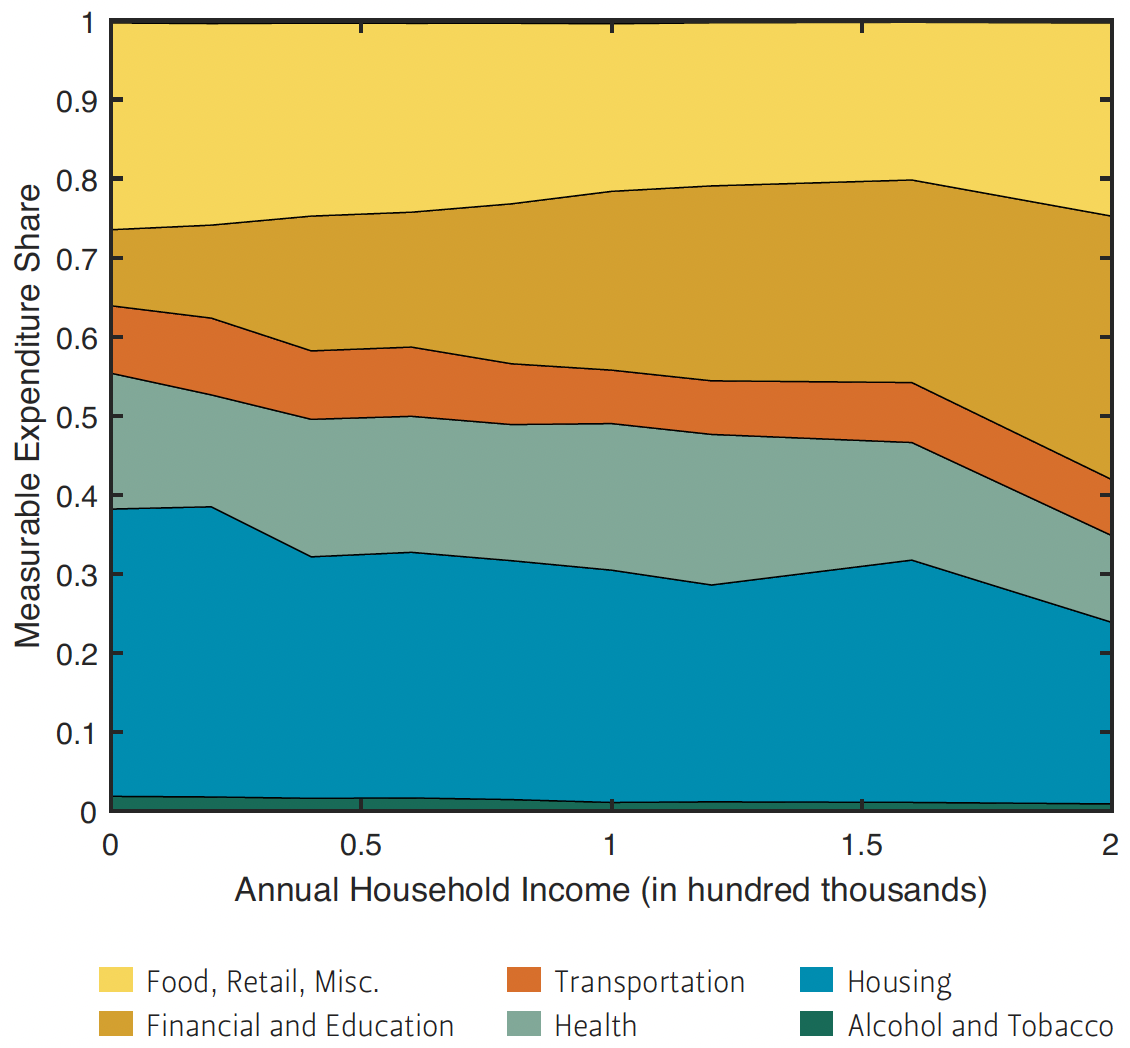

Figure 1 — Expenditure Composition and Income

Figure 1 shows how broad expenditure categories change with annual household income levels. The largest expenditure share is housing, which makes up roughly one-third of all measured expenditures and declines as income rises. The next largest share is food, retail, and miscellaneous expenditures, which comprise nearly a quarter of measured expenditures at every income level. Education and financial expenditures, which include insurance payments and contributions to pensions, tend to rise with income. Transportation outlays, including vehicle payments and fuel, comprise around 10% of measured expenditures and decline with income. Average health expenditures by households are less than 10% of measured consumer expenditures, and the expenditure share declines slightly with income. Finally, alcohol and tobacco maintain a small but flat share of expenditures.

Description of Taxable Items

Sales Tax Base

While each state levies its sales tax on a unique set of consumption goods, several states have many of the same items in their tax bases. Of the large expenditure categories, education, financial services, and health are generally excluded from sales taxation. Within the housing expenditures category, property payments, such as rent or mortgage, are generally excluded from the sales tax base, but home furnishings and appliances are usually not excluded. This leaves transportation, food, retail, and miscellaneous expenditures to comprise the remaining sales tax base. Groceries are usually exempt from sales taxation, while restaurant dining is often not exempt. Public transportation is generally excluded from sales taxation, but vehicle payments are included in the sales tax base. Retail and miscellaneous items, such as personal care products, are generally taxed as sales, but most services are not taxed. For the purpose of constructing a realistic sales tax base, entertainment services, such as sporting event tickets, are included in the sales tax base, but other services are excluded.

Excise Tax Base

Consumption items are categorized as excise-taxable based on whether they are generally treated by the tax system uniquely. Motor vehicle fuel, alcohol, tobacco, lodging (e.g., hotel stays), and home utilities, such as electricity and water, each satisfy the definition of an excise tax and collectively comprise the excise tax base.

Measuring Progressivity

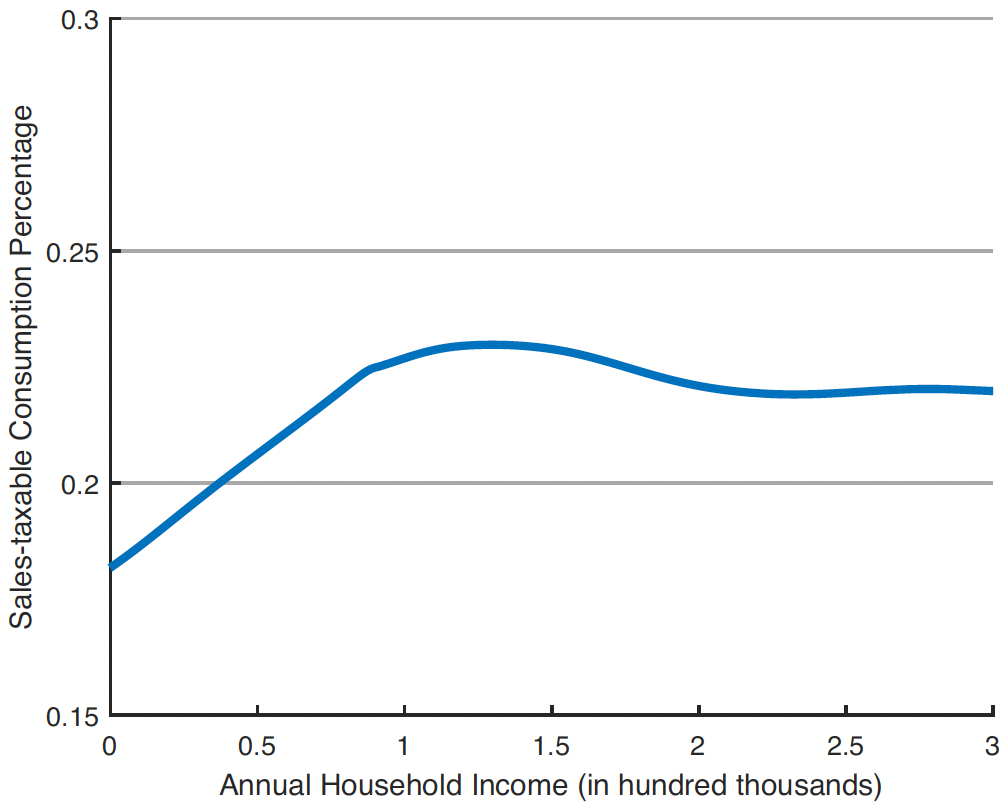

Figure 2 — Sales-taxable Consumption Share and Income

After carefully evaluating the CEX data set and constructing a typical tax base, the next step is to estimate the percentage of taxable expenditures across income levels.4 Figure 2 shows that the share of expenditures included in the sales tax base increases steadily by roughly five percentage points—from 18% to 23%—for households earning up to $100,000 per year. However, the base declines around one percentage point beyond $130,000 and stabilizes at around 22% of consumption for households earning above $200,000.

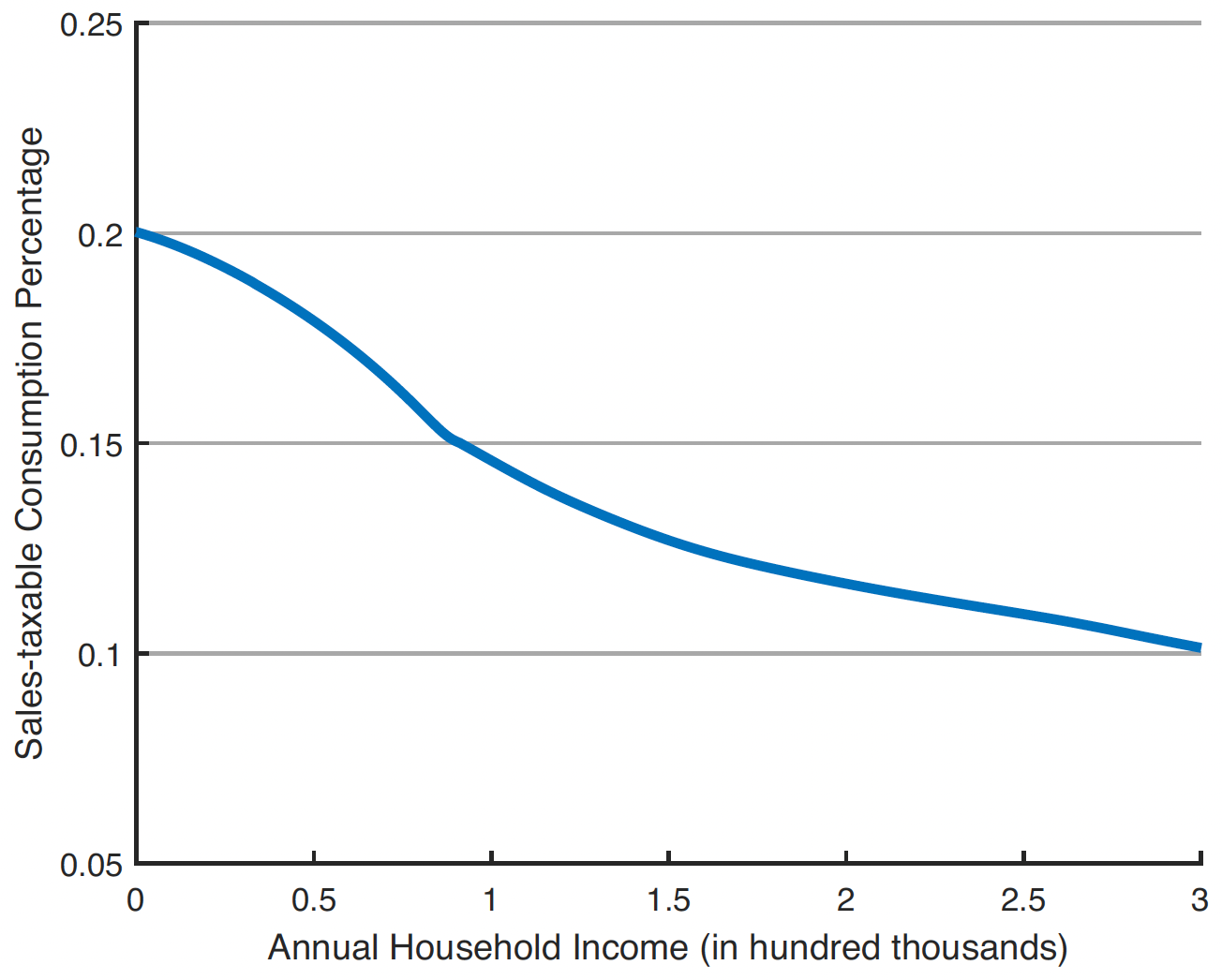

Figure 3 — Excise-taxable Consumption Share and Income

This graph suggests that sales taxation may actually be progressive for most households. Data from the 2015 Current Population Survey shows that 73.6% of U.S. households had an annual income less than $100,000, and 87.7% of households had an income below $150,000. Further breakdown of this relationship across different age groups results in a similar pattern, suggesting that lifetime consumption patterns do not show evidence of differential age-dependent tax incidence after accounting for income. This suggests that a shift in taxation toward sales taxation may actually increase a state or municipal tax structure’s progressivity.

Figure 3 shows that the excise tax burden falls more heavily on lower-income households. As household income increases up to $100,000, the fraction of excise-taxable expenditures falls about six percentage points and declines another four percentage points as household income rises to $300,000. As opposed to sales taxation, a shift toward excise taxation reduces the progressivity of a state or municipal tax structure.

Conclusion

Although sales taxation often faces opposition based on the assumption of a strict relationship between income and taxes paid, this analysis shows that sales-taxable consumption actually rises with income. This implies that the burden of an increase in the sales tax rate may actually fall more heavily on households with higher lifetime incomes. By contrast, excise-taxable consumption falls as income rises, suggesting that increases in excise taxes unambiguously affect lower-income households more than higher-income households.

While this study can serve as a quick reference for policymakers considering the effects of changing the sales or excise tax rate, a tax jurisdiction’s actual tax progressivity depends on the unique composition of its tax base. Choosing to restructure the sales or excise tax base through exemptions and inclusions almost certainly changes the tax structure’s progressivity. To that extent, policymakers wishing to study the progressivity of taxing particular consumption bundles can reconstruct elements of their specific tax base using the CEX to measure the relationship between taxable consumption share and income.

Endnotes

1. See Tax Foundation at https://taxfoundation.org/state-and-local-sales-tax-rates-in-2017/.

2. Ibid.

3. See Bureau of Labor Statistics at https://www.bls.gov/opub/hom/cex/data.htm.

4. In Figures 2 and 3, a non-parametric locally weighted regression is used to estimate the percentage of taxable consumption as it relates to income.

References

Keynes, John M. 1936. The General Theory of Employment, Interest and Money. New York: Harcourt Brace Jovanovich.

Poterba, James M. 1989. “Lifetime incidence and the distributional burden of excise taxes.” Working paper no. 2833, National Bureau of Economic Research.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.