Background

The Harris County Toll Road Authority (HCTRA) was established in 1983 by the Texas Legislature. It began operations with the opening of Hardy Toll Road in 1988. Since then, the system has expanded to encompass 128 miles of toll roads and is now the second-largest toll road system in Texas (Figure 1). Harris County is home to the city of Houston and the state’s most populous county.

Figure 1 — HCTRA System Map

HCTRA is organized as a direct control toll road authority under Chapter 284 of the Texas Transportation Code. In contrast to regional toll road authorities, such as the North Texas Toll Road Authority, HCTRA is not a separate legal entity. Rather, it is legally a subdivision of Harris County and governed by the Harris County Commissioners Court.

The financial condition and operating results of HCTRA are included in Harris County's consolidated financial statements; however, the county also issues stand-alone financial statements for HCTRA. The most recent set of financial statements is for the year ending Sept. 30, 2024 — typically, the Annual Comprehensive Financial Reports (ACFR) and financial statements for governmental entities are issued approximately six months after their fiscal year end.

Impact of Fiscal Year Change

In 2022, Harris County changed its fiscal year-end from the end of February to the end of September. As a result, two sets of financial statements were issued in 2022. One was for the full year, March 1, 2021, through Feb. 28, 2022, and the other was for the seven months covering March 1, 2022, through Sept. 30, 2022. The seven-month report is referred to as the “stub year.” This change skews unadjusted annual comparisons. Therefore, in some cases, the values are annualized to allow better comparison, and in others, the monthly averages are used to compare results across different years, depending on the context.

Overview

With the growth in Harris County’s population over the last three decades and the expansion of the HCTRA system, traffic counts have approximately doubled in the last 20 years. This has driven strong growth in toll revenue which in turn has generated large surpluses, totaling over $4.5 billion since 2011. HCTRA has a strong balance sheet, with net position of $2.1 billion at the end of FY 2024 and has a total-liability-to-net position ratio of 1.72.

Consequently, HCTRA holds the highest bond rating among all toll road operators in Texas. Nonetheless, HCTRA is substantially indebted. At the end of FY 2024, its long-term liabilities were just under $3.3 billion, and it plans to issue substantial new borrowing in the future. Notwithstanding HCTRA’s strong financial position and operating results, it faces some potential headwinds, including slowing growth and compression of its operating margins.

Highlighted Issues

COVID-19 Downturn in FY 2021

Due to the lockdowns associated with COVID-19, HCTRA saw a dramatic decline in toll road usage and revenue in FY 2021 (March 2020–February 2021). Therefore, the results of that year cannot be compared to other years. When data from FY 2021 are included in historical data and charts, it is labelled as “2021COVID” to note the impacts of the pandemic.

Compression of Operating Margins

Since 2015, toll revenue has increased by 27% (from $689 million to $874 million). Generally, the costs of operating toll roads are relatively fixed. The marginal cost for each additional vehicle using the system should be near zero, at least in the short to medium term, resulting in high operating leverage.

However, HCTRA’s operating expenses have grown faster than toll revenue, compressing its net operating margins. As a result, despite increasing toll revenues, HCTRA’s average monthly operating income remains roughly the same as it was a decade ago. HCTRA’s management considers this compression to be a temporary phenomenon caused by certain extraordinary events that should normalize in the future.

Although HCTRA’s operating margin has been narrowed in recent years, it still compares favorably to the North Texas Tollway System (NTTS), a key peer. In 2023 and 2024, NTTS reported an operating margin of approximately 32% compared to HCTRA’s margin of just under 50%.

Withdrawals by Harris County

The enabling statute for county toll road systems allows the sponsoring counties to withdraw excess revenues generated by the toll roads. The Transportation Code specifies in §284.0031(a)(1) that the excess revenues may be used “to pay or finance the costs of a project for the study, design, construction, maintenance, repair, or operation of roads, streets, highways, or other related facilities that are not part of a project under this chapter.” The term “other related facilities” is not further defined so gives the county significant discretion in how the funds should be spent. The statute also specifies that the state has no authority to supervise or regulate how the county uses its excess proceeds.

The withdrawals by Harris County have significantly increased in recent years. Before FY 2021, transfers to the county averaged slightly under $130 million annually. However, in FY 2021 through FY 2024, the county withdrew slightly under $1.5 billion, including $545 million in FY 2021 alone.

The county accounts for these withdrawals through a designated fund, the Harris County Mobility Fund. As part of the budgeting process, the funds are allocated to various county departments, with the largest share being divided among the four commissioner precincts.

Limited Oversight

Once the funds are allocated to a precinct, the Commissioners’ Court as a body does not exercise any oversight regarding how the funds are spent. The only oversight on how individual commissioners spend their allocated funds is a review by the county auditor and the county’s outside auditor. They examine the expenditures each year to ensure the county is in compliance with all laws, specifically the restriction in the Texas Transportation Code regarding how excess funds can be spent. In a report issued in December 2022, the County Auditor found that expenditures from the excess funds “generally complied with the Texas Transportation Code,” but identified several deficiencies in the documentation of those expenses.

Due to the vague statutory language regarding the use of excess funds, auditors have limited options for documenting how these funds are spent. It would be beyond their scope, for example, to specify what projects are funded by the excess proceeds. Also, since the commissioners are hesitant to oversee each other’s spending of these funds, the public has little information on how the excess proceeds are used, beyond what each commissioner chooses to disclose.

In addition to cash withdrawals, the county has, at least once, accomplished the same financial result by transferring expenses to HCTRA. In March 2020 (FY 2021), the county transferred responsibility for the operation and maintenance of the Lynchburg Ferry and the Washburn tunnel to HCTRA. The expenses assumed by HCTRA for these two facilities were just under $8 million in FY 2024.

Transition to an Electronic Toll Collection System

For some time, HCTRA has been migrating toward an electronic toll collection system of collecting tolls. In 2021, it completed that transition, closing the last staffed toll booths. The advent of electronic toll collection systems has enormously improved the efficiency of toll road operations, and it has largely eliminated the congestion that was once common at traditional toll booths.

However, electronic toll collections have created operational challenges for HCTRA because they also greatly increase the possibility that drivers can use toll roads without paying. Harris County Commissioners’ Court recognized this in its background to its January 2023 Toll Setting Policy Statement: “Since the full elimination of cash collection, HCTRA has experienced significant revenue leakage and higher costs of processing.”

The collection of tolls after the transition to a fully electronic system is an issue for all toll road operators, and HCTRA has been no exception. According to Note 3 to the 2024 HCTRA’s Basic Financial Statement (BFS) (page 28) HCTRA’s accounts receivable at year-end were approximately $155 million, after accounting for close to $ 749 million that had been written off as uncollectible. According to the County Auditor’s office, the note reflects the total write-off since the inception of HCTRA. However, 45% of the write-offs have occurred since the transition to electronic tolling.

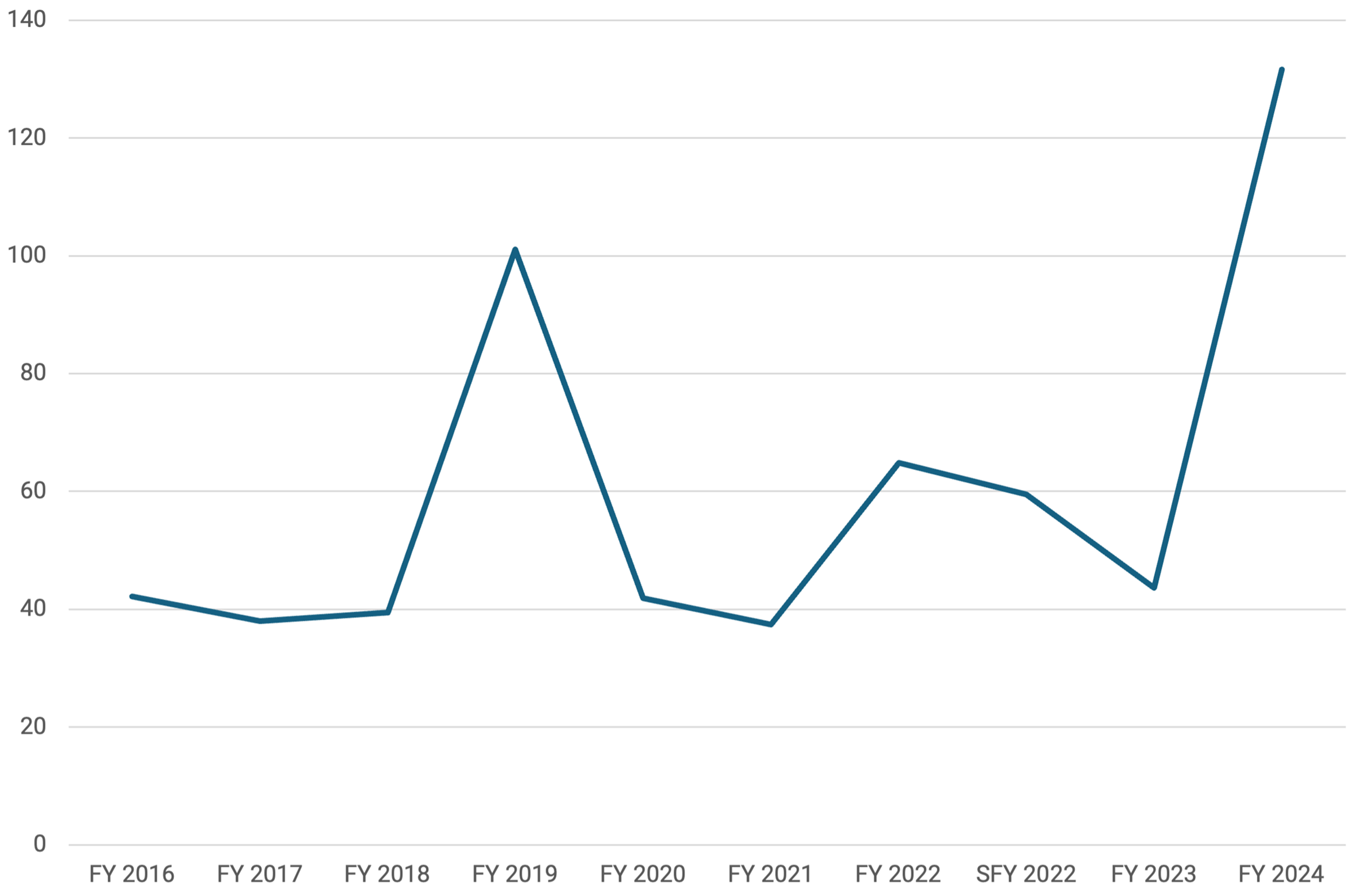

Annual write-offs of tolls averaged $52 million annually between FY 2016 and FY 2020, before a fully electronic system was implemented. Since then, the average has increased to $62 million, reaching an all-time high of $132 million last year (Figure 2). Since the Texas Constitution (Article 3, Section 55) prohibits a governmental entity from forgiving a debt, no account receivable is ever permanently deleted from the system.

Figure 2 — Accounts Receivable Write-Offs, FY 2016–24 ($ Millions)

Note: The stub fiscal year (SFY) 2022 value is annualized.

Payment Methods

EZ TAG

Most vehicles that use HCTRA’s toll roads are equipped with an electronic tag (EZ TAG) to identify the vehicle. Customers either have a credit card on file or maintain deposited funds in their accounts. If a card is on file, HCTRA may use the card to periodically add funds to the customers’ account. Funds are then withdrawn as toll charges are incurred. The system works very well, with only occasional collection issues, such as an expired credit card. In FY 2024, HCTRA used this system to collect tolls on 492 million transactions — which represented 75% of all vehicles that passed through a tolling location.

Preregistered License Plates

HCTRA also allows users to preregister a license plate. This system operates like the EZ-TAG system, but without the electric transponder located in the EZ TAG. The procedure is primarily used for commercial accounts, such as rental car companies and companies using vehicles on a temporary basis, allowing the customer to adjust its inventory of vehicles for which it is responsible.

Uncollected Toll Procedure and Revenue Loss

Last year, vehicles passed a tolling location without an EZ TAG on 156 million occasions. This was nearly double the number of non-EZ TAG transactions in 2020, the last year before the toll booths were closed. These transactions create a significant operational and financial challenge for HCTRA.

To begin, HCTRA must identify the vehicle and its owner from cameras located at the tolling locations. Last year, HCTRA was able to do so about 92% of the time (143 million) — this included preregistered license plates. The remaining — approximately 13 million — violations could not be identified due to poor image quality or the inability to obtain a match from state vehicle registration systems. Of course, the potential revenue from these 13 million vehicles, which was probably around $18 million last year, is completely lost. HCTRA does not record these transactions as revenue, and therefore, this lost revenue is in addition to the allowances for uncollectible accounts described above.

Once HCTRA identifies the owner, it recognizes the toll due as revenue and debits accounts receivable. HCTRA refers to these as “video transactions.” If the toll is not paid within 30 days, HCTRA sends the owner an invoice. According to HCTRA, in 2024, 69 million of the 143 million video-identified transactions were paid within 30 days without HCTRA needing to send an invoice. That users would voluntarily pay a toll even before being notified of the amount seems highly unlikely and suggests that there may be a data or analysis anomaly resulting in this conclusion. This is an issue that deserves some additional review.

In 2024 HCTRA mailed 7.4 million invoices — covering 54 million transactions — by grouping transactions for the same vehicle to minimize mailing costs. As of June 2025, 2.96 million, or about 40%, of the invoices have been paid. The remaining 60%, about 4.48 million invoices, were sent to the County Attorney’s office for collection. No data on the collection rates on these invoices was available. However, considering the magnitude of the allowances for bad debt, the rate must be quite low.

Taking all this data, it appears that HCTRA is losing approximately $100 million annually in revenue due to drivers using its system without paying tolls. To put that into perspective, it exceeds HCTRA’s total annual personnel expenses.

Slowing Growth?

While HCTRA has experienced strong revenue growth since its inception, there are indications that this growth may have peaked. Last year, toll revenue, after rebounding post-pandemic, decreased slightly from the previous year (down 2.5%). Since the pandemic, monthly toll revenues have shown little upward momentum, stabilizing at approximately $72 million to $76 million per month.

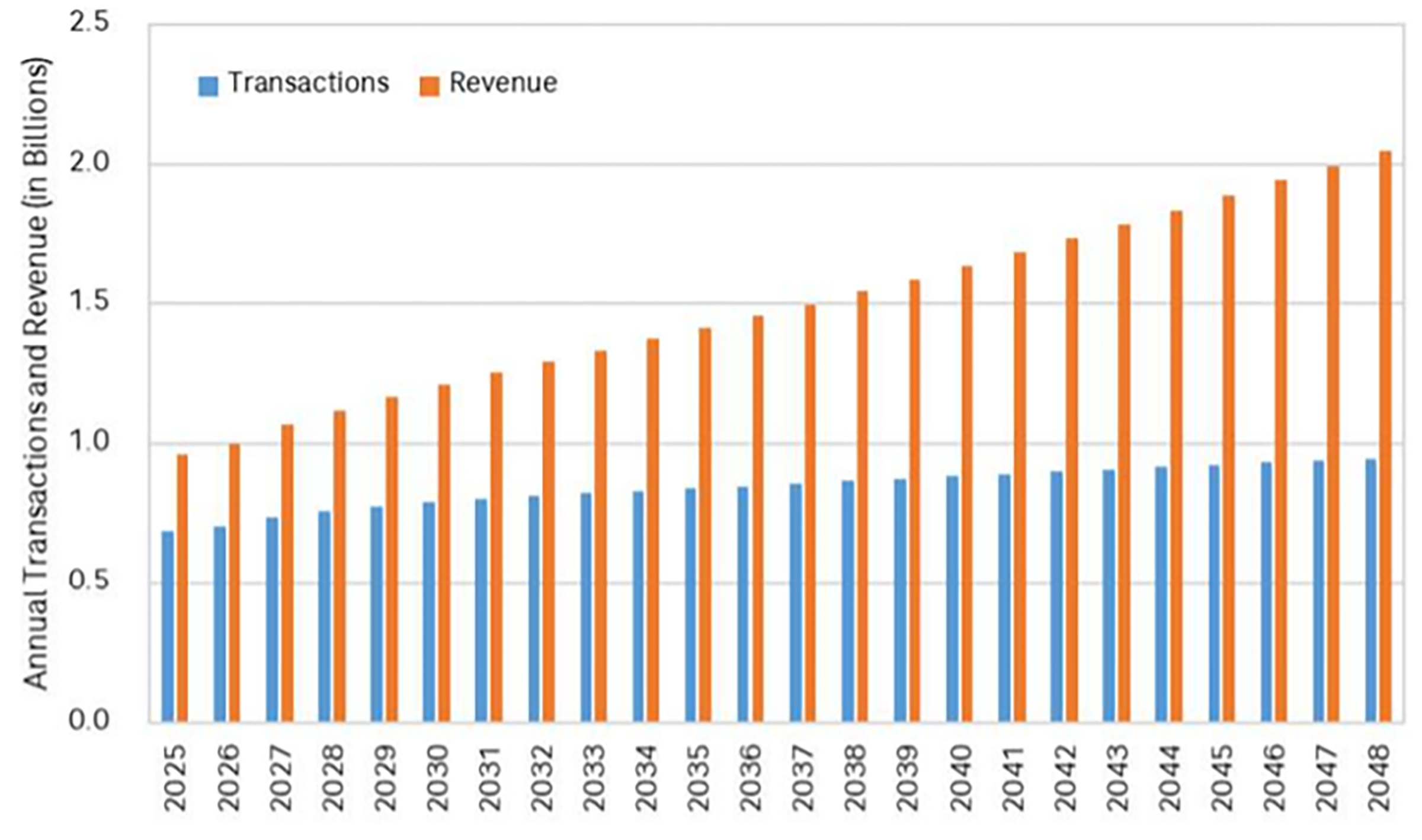

In December 2024, consulting firm CDM Smith completed a forecast of HCTRA’s future traffic volumes and revenue through 2053. It predicts that the number of transactions per year should grow from the current 675,000,000 to approximately 977,000,000 (+1.4% per annum), and revenues should grow to nearly $2.3 billion (+3.3% per annum) over that period. This is a relatively modest projection, assuming roughly 1.4% growth in system use and that toll rates will increase in line with inflation, around 2.0% (Figure 3).

Figure 3 — HCTRA Systemwide Annual Transactions and Revenue ($ Billions)

This projection for future growth in use of the system relies heavily on demographic projections for the region, including those from the Houston-Galveston Area Council (HGAC), the Texas Demographic Center (TDC), and a projection prepared specifically for the forecast by Community Development Strategies (CDS). At the time of the CDS projection, the most recent projections from HGAC and TDC were from 2018 and 2022, respectively. Both agencies have since issued new, more conservative projections. However, CDS projection is still lower than the updated HGAC and TDC projections. CDS projects that the regional population should reach 9.6 million by 2045. The annual growth rate gradually declines over the forecast period from 1.6% to 1.0%.

However, this projection of the region’s growth may now be overly optimistic. The CDS forecast was published in February 2024, before the release of the Census Bureau’s 2023 and 2024 ACS data, which confirmed that Harris County has continued to experience negative domestic migration and that population growth is increasingly dependent on international immigration. Moreover, the CDS report assumed that international migration would remain a “major factor” in regional growth, characterizing the pandemic slowdown as temporary. That assumption has since been overtaken by subsequent events.

Following the 2024 national elections, the federal government implemented significant restrictions on both legal and illegal immigration. These include mass deportation initiatives, stricter visa rules, and reduced refugee admissions, all of which are already resulting in a measurable decline in immigration flows. While the long-term effect remains uncertain, the near-term outlook strongly suggests that immigration will decline, casting doubt on the baseline population growth assumptions underpinning the CDS forecast. The current projections from HGAC and TDC also assume a stable level of international immigration. However, both have acknowledged the effect that a dramatic policy change would have on their projections.

Additionally, opportunities to expand the system’s footprint are limited. The current system already covers most of Harris County’s geographic area. HCTRA is currently committed to five improvements that are either in planning or already underway. The most significant of these are the replacement of the Ship Channel Bridge at Beltway 8 and the extension of the Hardy Tollway from Loop 610 into downtown. These enhancements will undoubtedly boost the system’s usage; however, revenue growth from them is likely to be modest.

The commissioners have the option to raise tolls to increase revenue. However, they lowered tolls for passenger cars in 2023 and conducted a highly publicized campaign to announce that reduction. In a recent Commissioners’ Court meeting, the county judge mentioned (at 3:00:03) a commonly-held belief that residents had been promised that the roads would be free after the debt was paid.

In fact, no such promise was made, and, of course, HCTRA is nowhere near retiring all its debt. But the judge’s comment and the court’s move to lower tolls for passenger cars highlight a political sensitivity to toll rates, which will likely limit future rate increases.

Another key issue is whether future toll increases might reduce demand. Elasticity of demand measures how sensitive usage is to price changes. Using somewhat dated data (2014), one study found average elasticity to be just -.038, suggesting demand is generally price-insensitive. However, it also found that elasticity varies widely depending on local conditions, such as the availability of alternative routes.

The 2024 forecast does not specifically address price elasticity, but it offers an indication: compared to a base case with 2% annual toll increases, a no-increase scenario projects 4.2% higher usage. That implies the elasticity for the system would be -2.1 — in other words, quite high. This area warrants further research, particularly before the Commissioners’ Court makes any significant changes to the toll rate structure.

The assumption used in the 2024 forecast that the toll will not be increased above inflation suggests a limited upside from future toll increases. That leaves the fate of HCTRA’s future revenues largely at the mercy of future demand for the system, which in turn depends on the region’s population growth trajectory.

Review of Basic Financial Statements

Statement of Net Position

Assets — As of FY 2024 end, HCTRA had assets of $5.7 billion. Its current assets were $2.08 billion, with $1.2 billion in cash and $697 million in investments. It also held $193 million in restricted cash and investments. The restriction on these cash and investments is mostly related to bond covenants.

Value — The value of the existing system was $1.68 billion net of depreciation, and HCTRA had $1.63 billion in ongoing construction and land. It also had $173 million of license rights, derived from a series of complex agreements with the Texas Department of Transportation regarding the construction and operation of various segments of toll roads within the county.

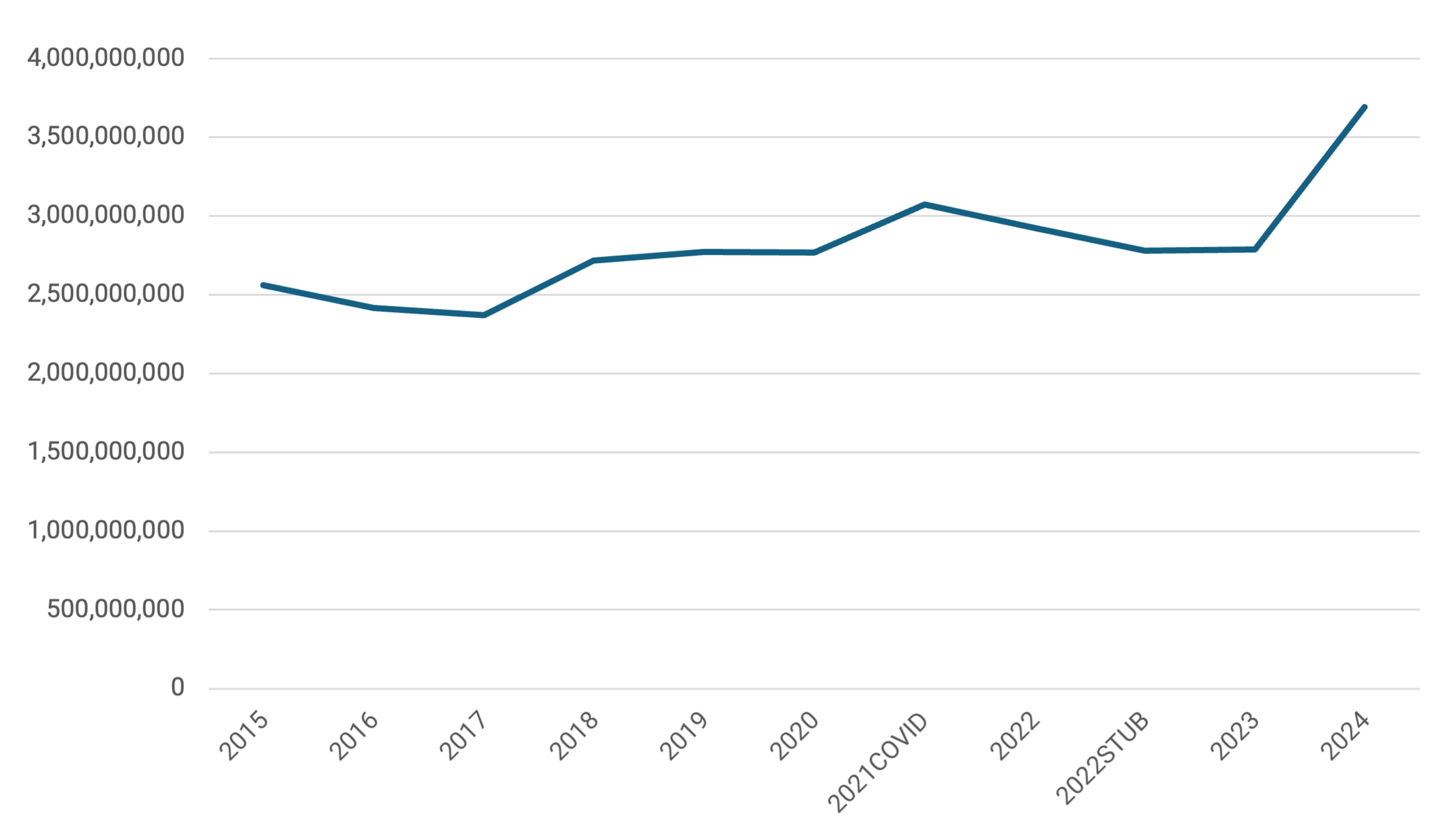

Liabilities — The total liabilities at year-end reached an all-time high of $3.7 billion, representing a 32% increase from the previous year ($2.8 billion to $ 3.7 billion) and a level that is 36% above its 10-year average. Figure 4 shows HCTRA’s total liabilities over the last decade.

The increase was primarily due to HCTRA’s issuance of $950 million in additional bonds last year. As of the end of the year, most of the bond proceeds had not been used and are reflected in a substantial increase in cash and investments ($1.055 billion to $1.92 billion). Presumably, that should decline as the cash is deployed on capital projects.

The remaining liabilities were routine. The largest is its OPEB (other post-employment benefits) liability at $164 million. The OPEB is the actuarily estimated liability for future medical expenses of retirees. HCTRA also provides its employees with a retirement plan, part of the statewide system for county employees. At the end of the year, HCTRA had a modest unfunded pension liability of $16 million.

Figure 4 — HCTRA Total Liabilities, FY 2015–24

Note: SFY 2022 value is annualized.

Capital Improvements — HCTRA’s current capital improvement plan calls for investments exceeding $5 billion over the next five years, which would require substantial additional borrowing. A May 2024 Moody’s credit opinion on HCTRA projected that $3.1 billion would need to be added to its debt to finance the improvements.

As previously discussed, the new improvements, which this debt is intended to fund, are unlikely to generate substantially higher revenues. Therefore, the interest associated with this additional debt is likely put further pressure on HCTRA’s profitability.

Statement of Revenue, Expenses, and Changes in Net Position

Toll Revenues — As previously mentioned, toll revenues decreased slightly last year ($896 million to $874 million, -2.5%). The notes to the BFS attribute the decrease to an increase in the allowance for toll violations deemed uncollectible. It is noteworthy that the monthly average for toll revenue for the previous year, FY 2023, was also about a 2% decline from the year before. According to the County Auditors’ monthly reports, the average monthly revenue for this year is about the same as last year.

Investment Income — Investment income is the only other significant source of revenue. It increased dramatically from last year ($37 million to $86 million, up 132%). Also, the amount is uncharacteristic compared to previous years. The BFS attribute the increase to “an increase in interest earned from investments.” This was likely the result of an interest rate arbitrage on the unused bond proceeds previously discussed.

Notably, while section 148 of the Internal Revenue Code generally prohibits governmental entities from investing the proceeds of tax-free bonds in interest-bearing instruments and earning an arbitrage, there are exceptions, especially while the entity is in the process of using the funds. Investment income should return to a level more in line with the historical average as the bond proceeds are deployed.

Operating Expenses — Operating expenses for the year hit an all-time high of $465 million. While the increase for last year was relatively modest (approximately 2%), operating expenses have averaged rising 10% annually since the recovery from COVID-19. Operating expenses, net of depreciation, have doubled in the last 10 years.

As previously mentioned, HCTRA’s expenses have increased due to the county transferring non-toll expenses to it — a ferry and tunnel operation. It is unclear if other such expense shifting has taken place.

Services and Fees — The largest operating expense is labelled “services and fees,” although the BFS do not provide any detail about this category. Over the past decade, these expenses have fluctuated widely. Immediately after COVID-19, services and fees expenses increased sharply by 10% annually, until leveling off this year.

According to HCTRA management, the increase in the services and fees is largely due to the implementation of the fully electronic collection system and the resulting increased volume of invoiced transactions. However, management expects to reduce these costs by renegotiating contracts and deploying new technology.

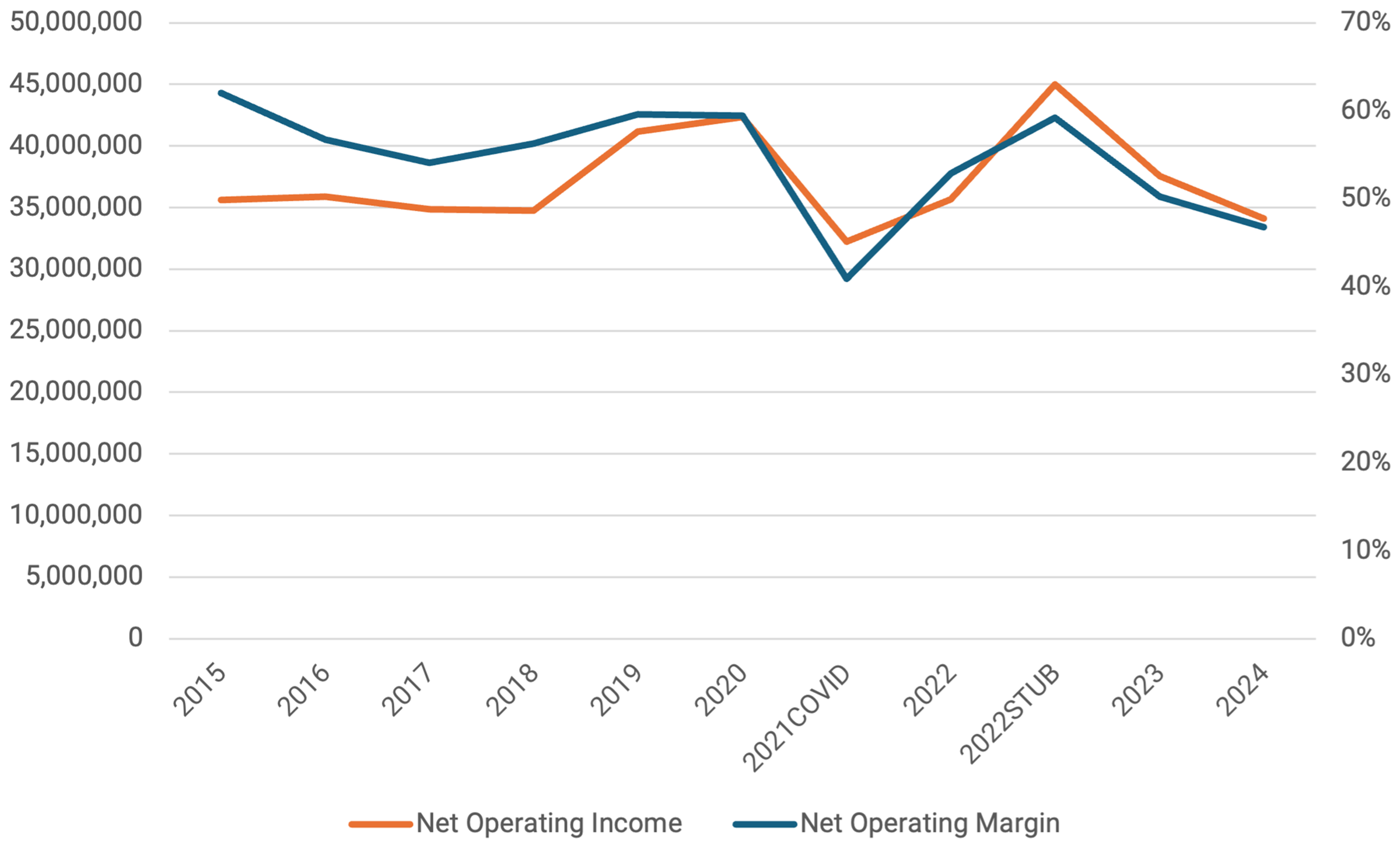

Salaries — The other large operating expense is salaries. Except for a brief respite after COVID-19, HCTRA’s salary expense has steadily moved higher throughout the last decade. The previous two years have seen the most dramatic increases when salaries shot up 16% and 19% in FY 2023 and FY 2024, respectively. Figure 5 provides a summary of operating net income and net margin from FY 2015–24.

It is noteworthy that the elimination of toll booth personnel did not have any detectable impact on the level of personnel expense. HCTRA management reported that this was because most of the former toll booth collectors were reassigned to review the larger volume of images that the transition to complete electronic tolling produced.

Figure 5 — Operating Net Income and Margin, FY 2015–24 Monthly Average

Conclusion

Harris County’s toll road system is a great legacy asset that has generated $5.7 billion of excess cash flow from operations over the last decade and vastly improved mobility in the region. Of that cash flow, $4.8 billion has been used to expand and renovate the system ($2.6 billion) and to pay debt service ($2.2 billion). Harris County’s withdrawals significantly reduced HCTRA’s ability to self-fund capital improvements, thereby increasing the necessity of debt issuance to maintain its investment program, driving its debt level to the highest level in HCTRA’s history. If HCTRA implements its current capital improvement budget, its debt level will increase significantly.

At the same time, HCTRA’s operating margins are facing increasing pressure due to rising expenses and stagnant toll revenues. Margins and cash flow are likely to come under greater pressure from the increased interest expenses and debt service if HCTRA goes further into debt to finance its current capital investment plans. Unless HCTRA can control its expense growth, improve collections from nonpaying users, and limit its capital improvement program to projects that enhance operating margins, it will be unable to generate the level of cash flow the county has come to expect.

Acknowledgment

This review of the Harris County Toll Roads Authority’s fiscal year 2023–24 Basic Financial Statements (BFS) is part of an initiative by the Center for Tax and Budget Policy at Rice University’s Baker Institute for Public Policy to provide financial data and insights on state and local governmental entities. The authors would like to recognize the extraordinary cooperation from the Harris County Auditor’s Office and the leadership of the HCTRA in preparing this brief.

This publication was produced on behalf of Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by external experts prior to its release. Any errors are the responsibility of the author(s) alone.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.