“... because these tax exemptions are granted outside of the normal public process and do not appear as a line-item spending in government budgets, the true cost is often obscured from both the public and policymakers ...”

Executive Summary

In the last decade, the use of legislation granting property tax exemptions for affordable housing has greatly expanded. Both newly constructed and existing multifamily properties have been granted tax-exempt status pursuant to transactions commonly referred to as public facility corporations (PFC) and housing finance corporations (HFC).

Uncovering The True Cost

The property tax exemptions granted to these PFC and HFC projects function as tax expenditures by exempting property tax levies in lieu of a direct appropriation that subsidizes housing costs. But because these tax exemptions are granted outside of the normal public process and do not appear as a line-item spending in government budgets, the true cost is often obscured from both the public and policymakers — making it difficult to judge if the community is getting a fair return on its multibillion-dollar investment.

Lost Tax Revenue Affects Local Services

The resulting revenue loss puts pressure on local taxing entities that have no control over when or how these exemptions are granted. These entities — including counties, school districts, municipalities, and special districts — must either offset the resulting shortfall in tax revenues through spending reductions, increased tax rates on non-exempt property, or an increase in an alternate revenue source.[1] Throughout this paper, references to lost property tax revenues recognize that the waived property tax revenue is acknowledged as a cost of encouraging affordable housing projects and that some local entities may have offset the lost tax revenue by increasing tax rates for other taxpayers.

Millions in Tax Revenue Lost Each Year

In the past, the efficacy of these programs has been the subject of both academic research and media attention.[2] However, there has been no comprehensive attempt to quantify the actual cost of these projects in terms of the property tax revenue waived until this report, which calculates the cost of lost revenue for taxing entities in Harris County, Texas. Authors’ analysis showed four significant financial impacts of these PFC/HFC transactions:

- Property value removal: More than $5 billion in appraised property value has been removed from Harris County tax rolls as of 2025.

- Cumulative revenue loss: Affected local taxing entities lost $124 million in 2025 tax revenues and a total of $355 million between 2020 and 2025.

- Accelerating revenue loss: Annual fiscal impacts have grown 15-fold since 2020, rising from $7.7 million to $124.5 million in 2025.

- Billions in future costs: These programs are expected to exceed $2 billion in costs over the next decade.

The Need for Accurate Cost Analysis

To address the growing housing affordability challenge in the U.S., governments at all levels have implemented various programs to subsidize housing. Exempting housing projects from local property taxes in exchange for a relatively small number of lower-rent units has become a widely used policy alternative. However, there has been little systematic research on the impacts of these policies on local government entities, specifically regarding foregone property tax revenues.

Since it is impossible to evaluate the effectiveness without knowing the cost in terms of lost property tax revenues, the Center for Tax and Budget Policy (CTAB) conducted a review of property tax revenue waived in connection with multifamily projects granted tax-exempt status in exchange for affordability concessions in Harris County, Texas.

Methodology

This research is restricted to transactions that were granted exemptions pursuant to the Private Facilities and Housing Finance Corporation statutes.[3] There are also housing projects and other properties that are owned and managed directly by housing authorities. This report did not attempt to quantify the property tax expenditure cost of those types of property.

One of the difficulties in conducting this research was identifying the universe of PFC and HFC projects, as no consolidated database exists, and there is no uniform coding system employed across appraisal districts. The authors were fortunate to have the substantial cooperation of the Houston Housing Authority and the Harris Central Appraisal District (HCAD) in identifying the properties that have been granted exemptions.[4]

After identifying the properties, data were collected on the target properties’ key characteristics and exempt values for the years 2020–25. The next step was to find the list of taxing entities that would have assessed property taxes in the absence of an exemption granted to each property. Each entity’s annual tax rates were then identified. Using this information, the lost property tax revenue for each entity per year was calculated by multiplying the exemption amount by that entity’s tax rate for the year.

The transactions examined rarely closed at year-end. Thus, for most transactions, the tax liability reported by HCAD for the year in which the exemption was granted is prorated. In a small number of cases, the property and exemption values differed across taxing entities. These are accounted for in the analysis.

In addition, there are four projects located outside Harris County but organized by the Houston Housing Authority. For these interjurisdictional transactions, the estimated total property tax loss in those counties is not allocated to the taxing entities. The total cost, inclusive of these projects, is detailed in the tables of this report.

In addition to quantifying the property tax revenue lost in 2020–25, this study also estimates the long-term costs of these programs for Harris County taxing entities. The principal challenge is that it is very difficult to project the likely life of the tax-exempt status. This analysis ultimately settled on estimating the cost over the next decade. The methodology for making that estimate is discussed below.

In some PFC and HFC transactions, the exempted property makes payments in lieu of property taxes (PILOT). Such payments, in theory, could offset the property tax revenue lost by taxing entities. Anecdotal information indicated that some transactions in Harris County may have included PILOT payments. Similarly, representatives of the Houston Housing Authority indicated that, for most of these projects, the authority retains a financial benefit that accrues upon termination of the tax-exempt status. These termination benefits vary greatly from transaction to transaction. However, the authors were unable to find any evidence that PILOT payments or termination agreements benefited the taxing entities that provided the subsidies, i.e., the lost property tax collections. Therefore, this analysis does not account for the effects of either PILOT or termination payments.

Because of various factors, the amount calculated in this report as foregone revenue may not actually result in reduced revenue to the particular taxing entity in question. For example, there are limitations on the amount of property taxes taxing entities can collect due to state and city tax limits and the recapture system in education finance. Exceeding these limitations triggers certain adjustments, such as lowering the entity's tax rate to hit a revenue limit or shifting revenue to other school districts. However, in all cases considered in this research, even though the entity's revenue might not be reduced, a related economic impact equal to the value of the tax exemption is shifted onto other taxpayers.

For example, if the properties had remained on the tax roll, the state limit on property tax revenue growth would require taxing entities to lower their tax rates. This rate decrease would have reduced tax payments for all taxpayers. Alternatively, allowing the exemption would shrink the tax base and the required reduction in the tax rate for other taxpayers in that taxing entity. Therefore, the foregone tax revenue calculation represents the total cost of these affordable housing transactions, taking into account the shift in the incidence of property tax levies, even when total tax levies remain constant.

Historical Background

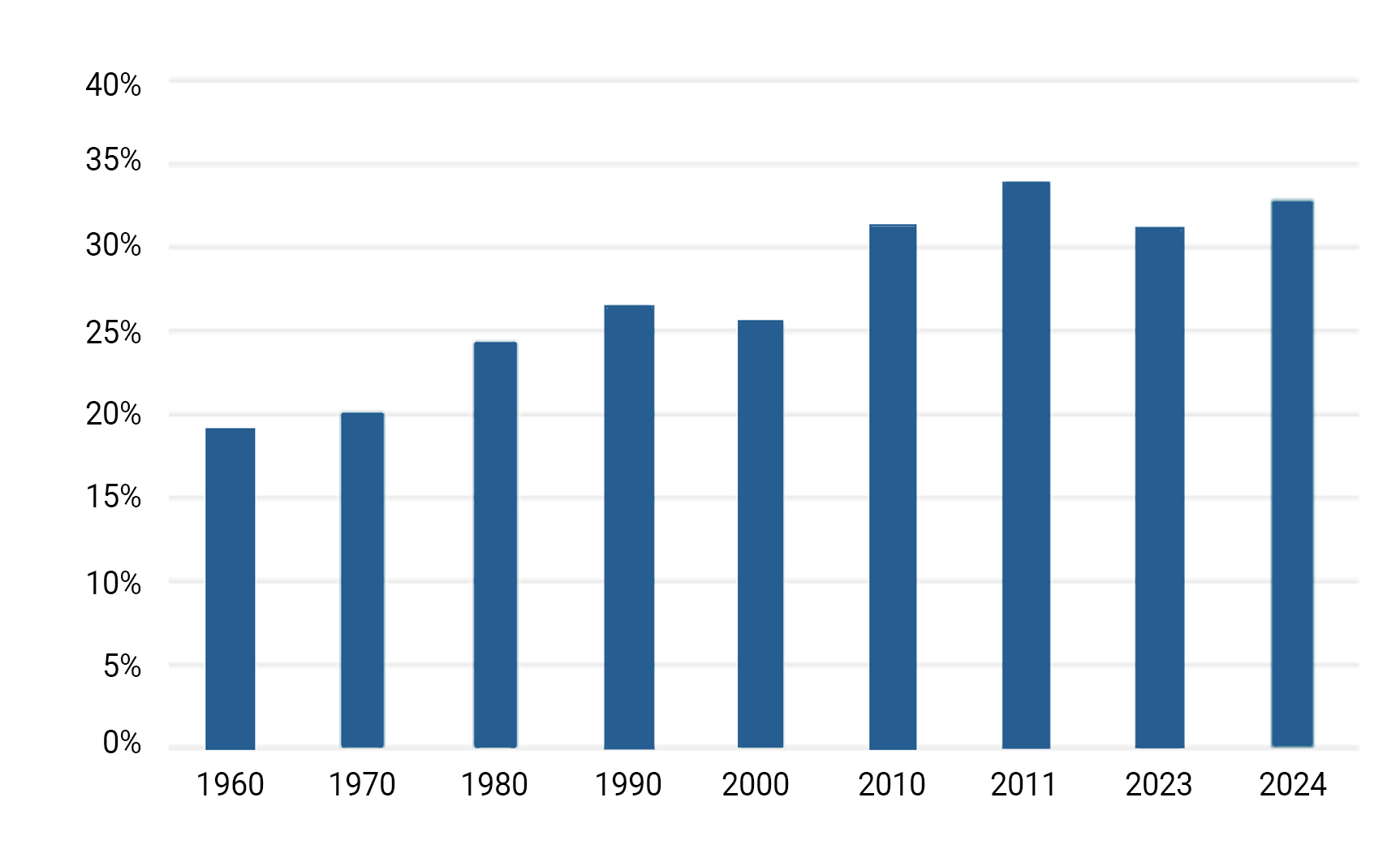

In recent decades, rental housing costs in the United States have risen faster than median household income, resulting in sustained increases in rent burdens for households most likely to live in multifamily housing. Inflation-adjusted rent indices show steady real growth since the 1970s, with particularly sharp accelerations after 2000 and again after 2020. By contrast, median household income has grown more slowly and unevenly, with extended periods of stagnation. As a result, a rising share of renter households now spends more than 30% of their income on housing, a commonly used threshold for cost burden. Demographic and household-structure changes also contribute to higher measured rent burdens by reducing income pooling and altering the composition of renter households.

Figure 1 — Median Rent-to-Income Ratio

To address the rising rental burden, many states enacted laws allowing local governments to exempt multifamily housing projects from property taxes in exchange for various rent concessions.

Texas joined this broader national movement by adopting and subsequently expanding statutory frameworks that enabled local governments to promote affordable rental housing through ownership-based tax exemptions. The Texas Legislature authorized the creation of housing finance corporations in the late 1970s, a move codified in Chapter 394 of the Texas Local Government Code, which explicitly empowers these entities to own residential property, issue tax-exempt bonds, and provide rental housing for low- and moderate-income households. Public facility corporations were authorized slightly later, in the early 1980s, under Chapter 303 of the Local Government Code. Although originally intended as general-purpose entities for public infrastructure, subsequent legislative amendments and administrative interpretation expanded the definition of public facilities to include multifamily rental housing projects.[5]

Together, these statutes positioned Texas local governments to attempt to address rental affordability pressures not through direct appropriations, but through public ownership structures that confer full ad valorem (i.e., according to value) tax exemptions in exchange for long-term rent restrictions. This was a particularly attractive alternative in Texas because of its relatively high property tax rates.[6]

Use of Affordable Housing Programs in Harris County

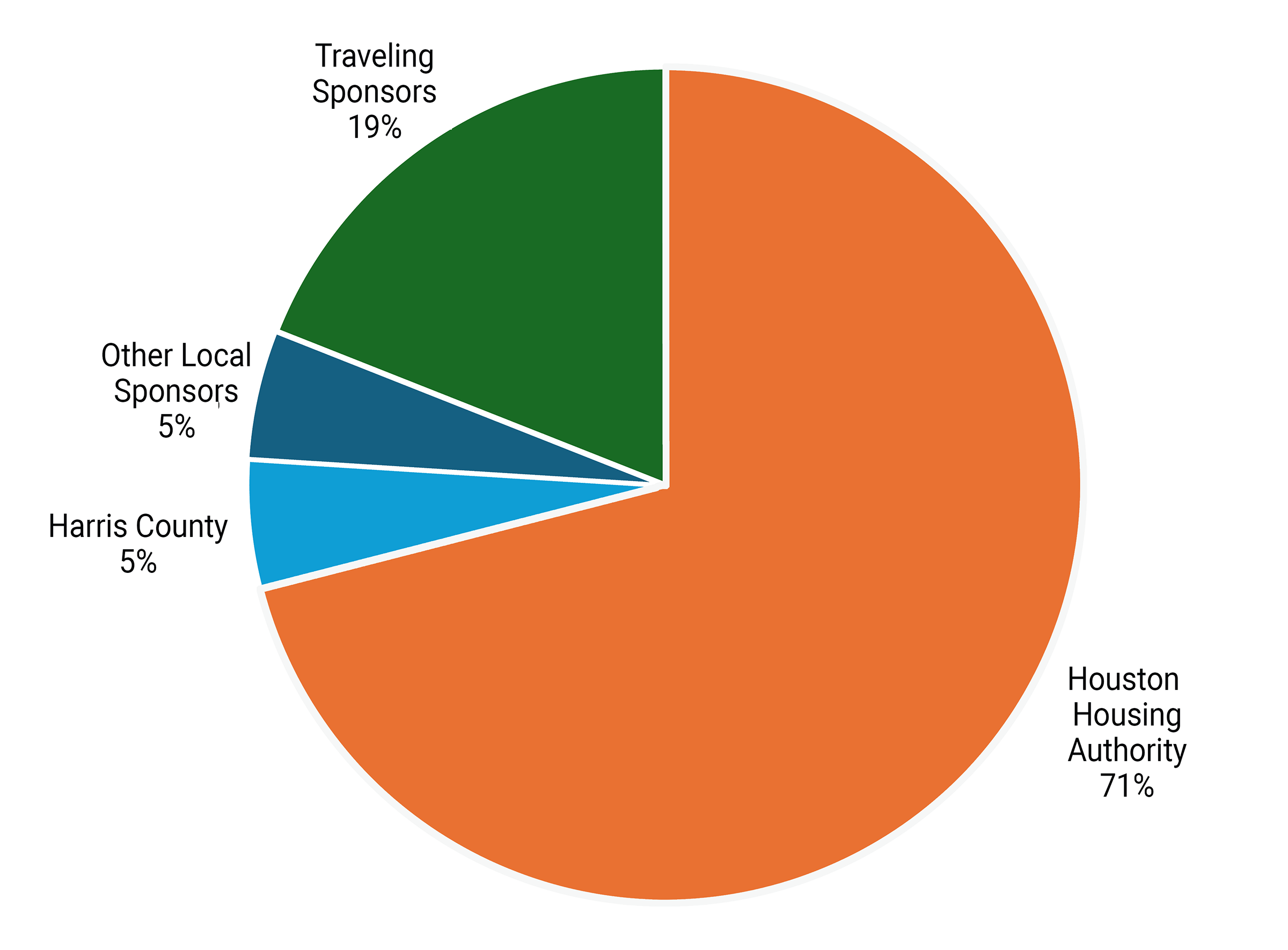

As of this report, 173 multifamily projects had been granted a complete property tax exemption in exchange for affordable rent concessions.[7] Among them, 123 (71%) were sponsored by the Houston Housing Authority.[8]

Figure 2 — Sponsors of PFC/HFC Projects in Harris County

After the Houston Housing Authority, the most active sponsors of these projects are a variety of housing authorities outside the Houston region. These are commonly referred to as traveling sponsors. For example, the Pleasanton Housing Authority sponsored 12 projects that removed over $176 million of property value from the Harris County tax rolls. Pleasanton, Texas, is a municipality of approximately 10,000 residents located about 50 miles south of San Antonio. The use of traveling sponsors was significantly restricted in reform legislation passed in 2023 due to PFCs granting property tax exemptions for apartment complexes located hundreds of miles outside their own jurisdictions. This made it possible for smaller towns to collect administrative fees while stripping larger cities nearby of tax revenues without their consent and without providing affordable housing in return.[9]

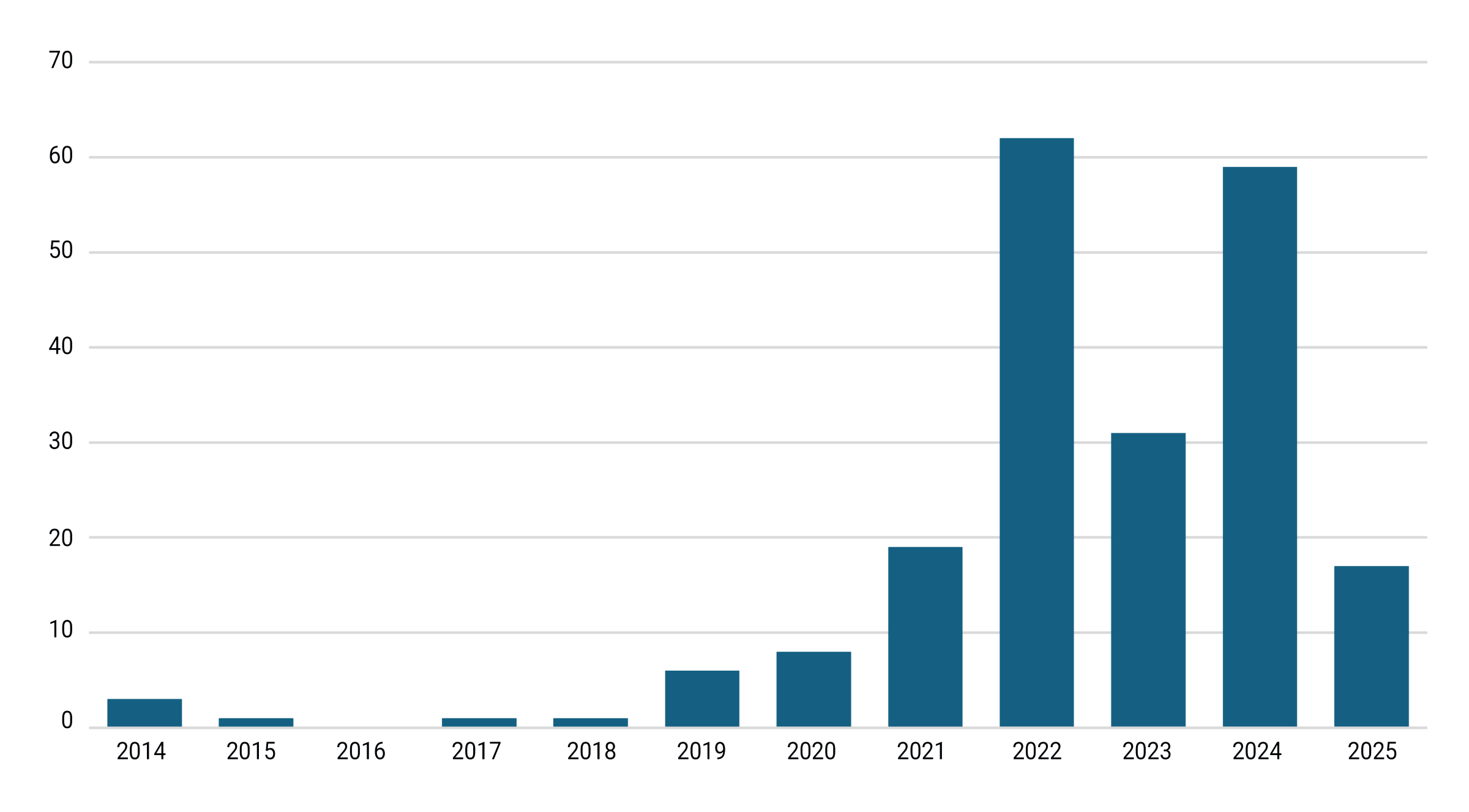

There is no evidence of property tax exemptions being used to promote affordable housing in Harris County before 2014, and the programs were used very sparingly through 2018. However, in 2019, the pace of transactions began to rapidly accelerate. By 2022, more than one transaction per week was being approved. About midway through 2025, the newly elected mayor of Houston made substantial changes to the board and management of the Houston Housing Authority, resulting in a significant curtailment of these projects.

Figure 3 — Affordable Housing Transactions in Harris County, 2014–25

A Rapid Rise in Costs

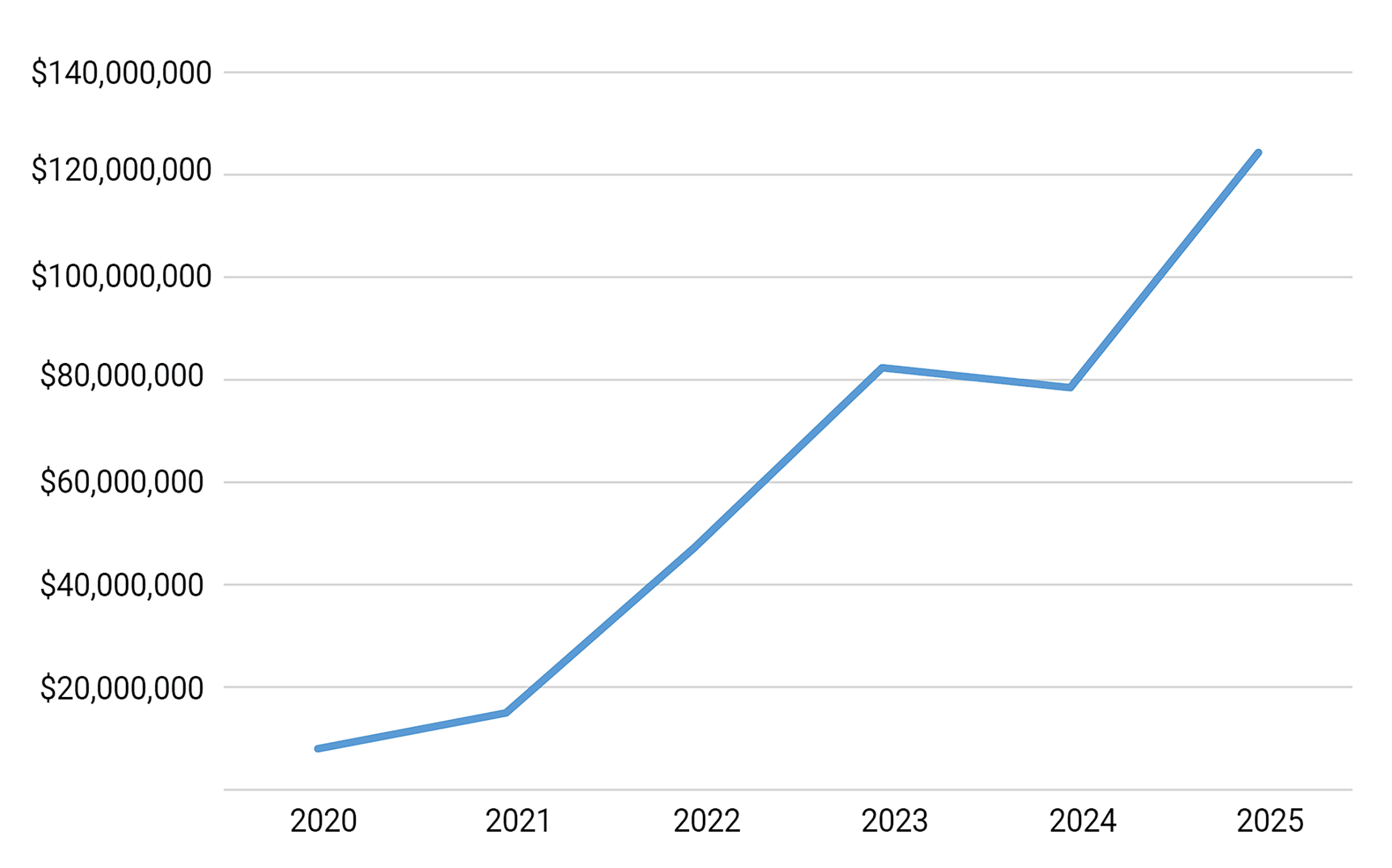

As a result of this surge in tax-exempt transactions, the cost to local entities began to rise rapidly after 2019. From 2020 to 2025, the cost of these projects to all taxing entities rose from $7.7 million to $124.5 million. The total cost for 2020–25 was $355 million. The tax entity most affected was Harris County: The cost to Harris County and its related entities was $34 million for 2025 and $91 million since 2020. School districts were also particularly hard hit. The cost in 2025 for all Harris County school districts was $51 million, and the total since 2020 was $153 million (see Table 1).

Figure 4 — Cost of Property Tax Exemptions on Affordable Housing Projects, 2020–25

If the current curtailment of these transactions continues, the rate of increase in lost tax revenue should ease somewhat. Nonetheless, at the end of 2025, 69 applications for tax-exempt status were pending with HCAD. This analysis estimates that if all those applications are approved, it will result in an additional $55 million in lost property tax revenue in 2026.

The expiration dates of the tax-exempt status for PFC and HFC projects appear to vary significantly depending on the negotiated terms and market conditions. Determining these terms would require attorneys to review agreements transaction by transaction, a task beyond the scope of this research. However, staff at the Houston Housing Authority speculated that, regardless of the negotiated terms, there was a distinct possibility that projects with exemptions would be sold to new owners and that the exemptions would be terminated. Because these transactions are still relatively new, it is impossible to say how likely it is if, or when, market conditions might result in terminations of tax-exempt status.

Exemptions That Last a Lifetime

During hearings in the 2023 Texas Legislature on reforming the PFC statute, witnesses testified that some exemptions were scheduled to last 75–99 years. Several witnesses described these exemptions as generational.[10]

To give some sense of the scale of the programs’ costs over the longer term, this analysis has estimated the potential cost for the next 10 years. For this calculation, the following assumptions applied:

- All of the projects pending approval at the end of 2025 will be approved in 2026.

- The tax-exempt status for all projects will continue for the next 10 years.

- The appraised value of these projects will increase by 3.5% annually.

- The average tax rate for all pending HFC entities will be 2.2%.

- The applicable tax rate for approved HFC projects over the next 10 years will be the same as in 2025.

Based on these assumptions, analysis estimates the cost of the approved and pending-approval projects for 2026 through 2035 to be nearly $2.2 billion. Consequently, if additional projects continue to be approved, the cost will be higher (see Table 2).

Conclusion

A Loss of Revenue Without Consent

Tax expenditures of any type, especially those achieved through property tax exemptions embedded in PFC and HFC transactions, tend to obscure the true fiscal cost of the programs they support. In the case of the PFC and HFC transactions, the cost of affordable housing programs is borne by the local taxing entities or by their taxpayers without any public budgeting process taking place. Indeed, the governing bodies of the affected taxing entities have little or no control over how much of their tax revenue will be lost to affordable housing project tax exemptions.

A Cost That Is Difficult To Track

Unlike direct appropriations, which appear explicitly in annual budgets and are subject to regular legislative scrutiny, the lost property tax revenues are dispersed across multiple taxing jurisdictions and rarely aggregated or reported as a single programmatic cost. As a result, the cumulative value of these exemptions is difficult for policymakers and the public to observe, compare, or evaluate against alternative housing subsidies.

Reduced Visibility Reduces Accountability

This reduced visibility can weaken accountability, complicate cost-benefit analysis, and make it harder to assess whether the public benefits of PFC and HFC projects are proportionate to the long-term revenue losses borne by cities, counties, school districts, and special districts. Hopefully, this research will provide policymakers with a baseline for future regulation of these transactions.

This research, which the researchers plan to update annually for Harris County, will provide an ongoing estimate of the cost of subsidizing these projects to serve as a baseline for comparing and evaluating the cost and effectiveness of these projects going forward.

Tables

Note: Additional information on the data tables and sources compiled by the authors is available upon request.

Table 1 — Lost Property Taxes by Taxing Entity, 2020–25

Table 2 — Estimates of 10-Year Lost Revenue by Taxing Entity

Table 3 — Estimates of 10-Year Cost for Pending Affordable Housing Projects

Notes

[1] It is important to note that the taxing entities bearing the fiscal impact of these property tax exemptions typically exercise little to no control over the associated tax expenditure. In most cases, affected jurisdictions are not parties to the transaction, do not approve the exemption, and are not formally notified when the property is removed from the tax roll. As a result, taxing entities may only become aware of the revenue loss after the exemption has been applied and reflected in the certified appraisal rolls, at which point the foregone revenue is effectively irreversible for that tax year.

[2] Heather K. Way, Public Facility Corporations and the Section 303.042(f) Tax Break for Apartment Developments: A Boon for Affordable Housing or Windfall for Apartment Developers? (Entrepreneurship and Community Development Clinic, University of Texas School of Law, 2020), accessed February 15, 2026, https://law.utexas.edu/wp-content/uploads/sites/11/2020/09/2020-ECDC-PFC-Report.pdf; R.A. Schuetz et al., “Who’s Cashing In Big on Houston’s Affordable Housing System? Not the Renters,” Houston Chronicle, March 27, 2025, https://www.houstonchronicle.com/projects/2025/affordable-housing-winners-losers/.

[3] Public Facility Corporation Act, Tex. Loc. Gov’t Code Ann. §§ 303.001–.903 (West 2024); Texas Housing Finance Corporations Act, Tex. Loc. Gov’t Code Ann. §§ 394.001–.907 (West 2024).

[4] In January 2026, the Houston Housing Authority changed its name to the Housing Alliance HTX.

[5] Public Facility Corporation Act, Tex. Loc. Gov’t Code Ann. §§ 303.001–.071; Texas Housing Finance Corporations Act, Tex. Loc. Gov’t Code Ann. §§ 394.001–.902. Housing finance corporations were authorized by the Texas Legislature in 1979. Public facility corporations were authorized in 1981 and subsequently applied to residential rental housing through legislative amendments and interpretive guidance.

[6] Tax Foundation, “Property Taxes by State and County, 2025,” accessed February 15, 2026, https://taxfoundation.org/data/all/state/property-taxes-by-state-county/.

[7] The projects in this analysis span 211 property tax accounts in Harris County, as some projects had multiple accounts. Four of the 173 projects are located outside of Harris County but were sponsored by the Houston Housing Authority.

[8] The Houston Housing Authority is a public housing authority created under Texas law that operates as a separate political subdivision of the state of Texas. While the authority is independent of the City of Houston for operational and financial purposes, the City plays a limited oversight role, primarily through the mayor’s appointment of the Authority’s board members, subject to confirmation by the City Council (Tex. Loc. Gov’t Code §§ 392.031–.033; Houston Housing Authority, FY 2026 Annual PHA Plan & MTW Supplement, accessed February 15, 2026, https://cdn.prod.website-files.com/693a083bb9dac41de47a7499/698401201e8899940de09611_Part-III_HHA-FY-2026-MTW-Supplement-Attachments_rev-10142025.pdf). For the purposes of this analysis, HFC projects sponsored by the Houston Housing Finance Corporation were included. Houston Housing Finance Corporation is a separate legal entity from the Houston Housing Authority, but under the same political leadership of the City of Houston. Similarly, Harris County has sponsored PFC/HFC projects through several different housing-related entities, which have been included in the Harris County sponsor count.

[9] “Texas House Votes to Abolish Traveling HFCs,” posted April 28, 2025, by CBS Texas, YouTube, https://www.youtube.com/watch?v=U6MHwfA58E0.

[10] Public Hearing on H.B. 2071, 88th Leg., Reg. Sess., Texas House of Representatives, Committee on Ways and Means, February 28, 2023, https://capitol.texas.gov/billlookup/Actions.aspx?LegSess=88R&Bill=HB2071; Schuetz, “New Law Reforms Big Tax Cuts For Not-So-Affordable Housing,” Houston Chronicle, updated July 8, 2023; Jen Rice, “Abbott Signs Law Aimed at Reforming Controversial Affordable Housing Tax Break,” Houston Chronicle, June 20, 2023, https://www.houstonchronicle.com/news/houston-texas/housing/article/pfc-reform-law-signed-affordable-housing-tax-break-18141906.php; and Way.

This publication was produced by Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by outside experts prior to release. Any errors or omissions are solely the responsibility of the author(s).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.