Since at least the end of World War II, the United States and Mexico have followed divergent energy policy models. The United States has traditionally allowed private property to be utilized for the exploration and extraction of subsoil resources and has used tax and market incentives—albeit limited and sometimes directed by energy security criteria—to develop a domestic and diversified energy supply. The U.S. federal government has even developed a strategy of energy diplomacy to ensure the reliable supply of its crude oil imports, with both Mexico and Canada serving as strategic partners. By contrast, Mexico has followed a sovereign model in the ownership of subsoil resources, especially since the 1960s. It has done so under two state monopolies: Petróleos Mexicanos (Pemex), for the development of all hydrocarbon value chains, and the Comisión Federal de Electricidad (CFE), for the development of the electricity industry.

Although the energy models followed by the U.S. and Mexico are substantively different, the development of their respective industries has been compatible with each nation’s foreign policy interests. In the decades since World War II, both nations have been able to mutually benefit from the other’s energy policies, creating a balanced bilateral relationship.

The rapid development of U.S. shale oil and gas production in the last two decades, however, upended the status quo. The strategic relationship between the two countries was reversed—the United States became a net exporter of energy and a strategic supplier of natural gas and oil products to Mexico. The United States is also in the middle of a major energy transition effort. Faced with this new reality, Mexico carried out a far-reaching energy reform in 2013 that abolished the state monopoly regime and opened all the industry’s value chains to private investment, both national and foreign. Although the government did not relinquish national sovereignty over subsoil resources, this market-oriented reform was meant to align the Mexican energy industry with the U.S. energy model for the 21st century.

However, since Mexican President Andrés Manuel López Obrador took office in December 2018, the energy interests of the two nations have diverged again. López Obrador has sought to severely limit market forces in the energy industry and reconstitute a state-led model. His administration is not keen on moving Mexico toward an energy transition model either. This presents unique obstacles for the future of Mexico’s energy industry and major challenges to U.S. strategic goals. Several important questions arise: How do we understand the key differences between these two divergent models? Are they sustainable? How might they evolve in the face of the latest shock to global energy markets—Russia’s invasion of Ukraine?

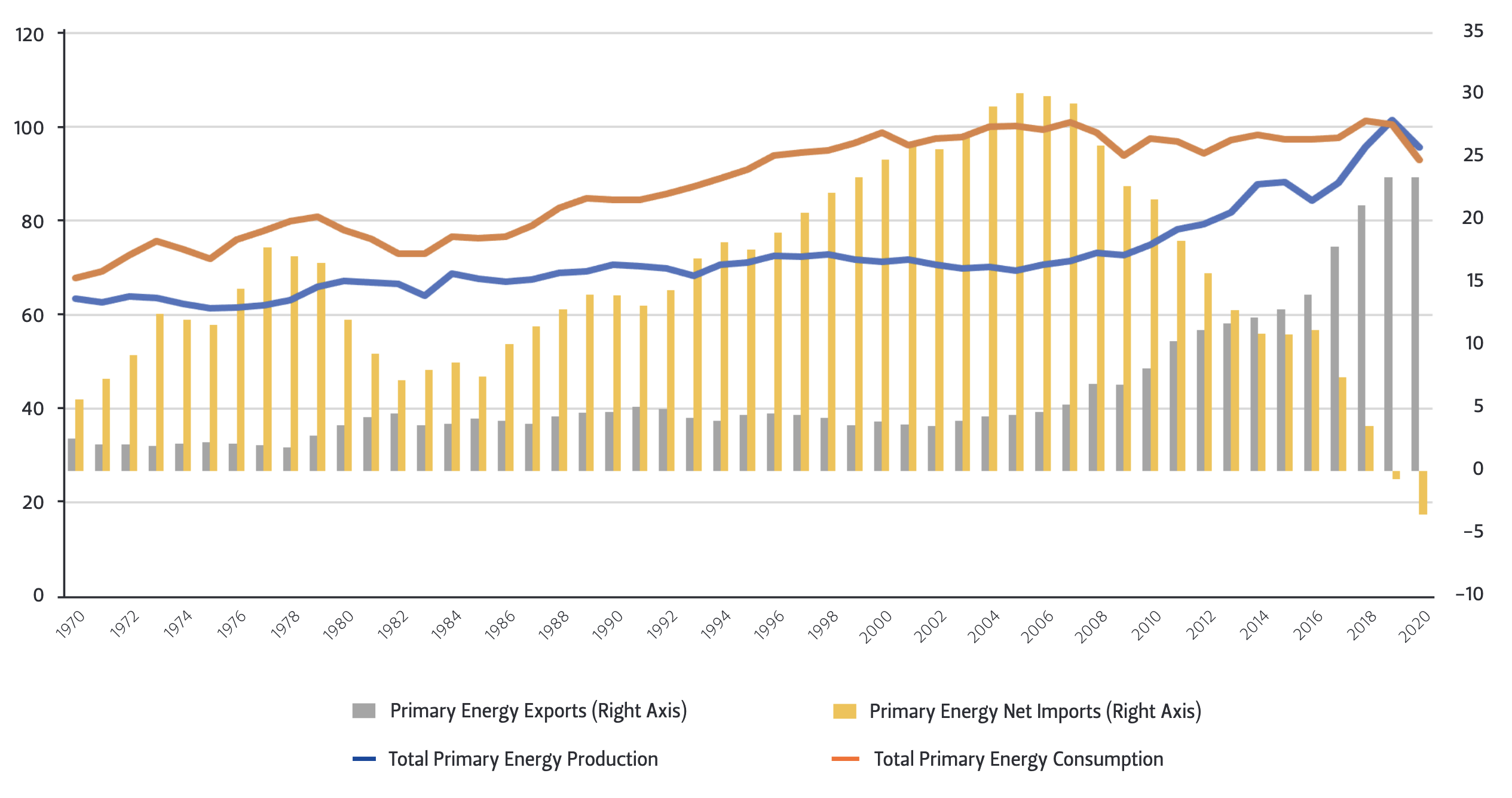

Figure 1 — U.S. Energy Balance and Foreign Trade (Billions of British Thermal Units)

The Biden Administration’s Drive to Decarbonize the U.S. Economy

Joe Biden became president at a time when the United States was becoming a net exporter of energy. As Figure 1 shows, from the early 1970s until the end of the last decade, the United States has been a net importer of energy, especially crude oil. In fact, during the 1990s and 2000s, that dependence on crude oil imports became critical. During those years, Canada and Mexico served as strategic suppliers to the United States, but that relationship changed with the development of shale oil and gas production from Texas and the Appalachian basin. By the end of the 2020, when Democrats returned to the White House and obtained a majority in both houses of Congress, the United States was already becoming a net exporter of natural gas and oil products.

During his presidential campaign, Biden pledged to push aggressively for renewable energy and the accelerated decarbonization of the U.S. economy. The goal was to make electricity generation carbon neutral by 2035 and the rest of the economy carbon neutral by 2050. His plan also sought to accelerate the transition of the automotive industry toward electric vehicles. This would bring the nation closer to achieving the global decarbonization goals promoted by the Paris Agreement, which was signed by President Barack Obama in 2015. Although the agreement was renounced by the Trump administration, Biden has now recommitted to it.

The current administration’s objectives are not limited to the energy industry. Decarbonization has become an essential goal requiring shifts in industry, infrastructure, and scientific research policy that will generate economic growth and new jobs while strengthening U.S. leadership in global energy matters. At the industrial level, the two axes of economic reactivation rest on the promotion of an emissions-free electricity industry and an automotive fleet free of liquid fuels. It is crucial for the U.S. power industry to develop more clean energy sources (renewable and nuclear) if the United States is to consolidate its leadership position in the global digital revolution and the new era of connectivity— which depend on electricity and a complex distribution and interconnection infrastructure network.

The U.S. “renewables revolution” under Biden is ambitious. Regarding the automotive industry, Biden’s plan promotes the development of electric transport, both private and public, with technology developed in the country. According to the Biden administration, this will create 1 million new jobs, in addition to new supply chains and infrastructure linked to the automotive sector. The rapid takeoff of the electric car company TESLA, as well as General Motors’ commitment to assemble only plug-in cars by 2035, show that the era of mobility based on internal combustion engines has entered its twilight.1

The Democrats’ vision has also included a go-getting development strategy that includes the following: the development of efficient and high-capacity lithium batteries and other materials; a push for the construction of solar panels; the development of green hydrogen (i.e., not from natural gas); industrial decarbonization in the manufacturing of chemical and construction materials (steel, concrete, etc.); the promotion of carbon capture and storage/ processing technology; the development of new materials to ensure emissions-free buildings; and a thrust to make the agricultural industry sustainable and free of emissions—including methane.2

With Biden, the return of the entrepreneurial state—this time with an energy reconversion package—is once again the axis of economic and social policy in the U.S., as it was during the Roosevelt era and in the two decades after the end of World War II. The return of the entrepreneurial state is also part of the mandate to defend the country’s democratic institutions, which the Trump administration put under stress, and to close the social and racial gaps that have widened in recent years—all with the intention of recovering the United States’ position as an international leader while maintaining traditional alliances and championing the fight against climate change.

After a year and a half in power, Biden’s most important achievement has been obtaining support from Congress for over $1.7 billion in infrastructure development. Although the bulk of investments will be directed to modernize the nation’s highways, roads, drinking water systems, and electronic connection, a significant amount will go toward the development of electricity transmission infrastructure.3 Still, at the end of 2021, Congress did not approve the most ambitious proposal, which pushed for substantial investments in renewable energy and energy transition technologies. The bill, known as the "Build Back Better Act”, called for more than $2.3 billion in investment. It passed in the House but was blocked in the Senate by Joe Manchin, a Democrat who caused the party to fracture over Biden’s decarbonization goals. After this setback, Biden has tried to rework the proposal, but Russia’s invasion of Ukraine has taken much of the attention away from the project, and Biden has had to refocus his efforts on passing financial support for Ukraine.

The Return to “Energy Sovereignty” Under the López Obrador Administration

Under López Obrador, Mexico has chosen a new path. From the beginning of his tenure, López Obrador considered the 2013 energy reform a privatization project, the purpose of which, according to him, was to weaken Pemex and the CFE. He has also argued that the reform did not fulfill its purpose—to attract significant private investment in order to increase oil and gas production. These stated reasons were his excuse to suspend all public tenders for oil, gas, and electricity.

Although the constitutional changes made by the 2013 reform have not technically been reversed, in practice, many of the laws and regulations have simply not been implemented. The regulatory and operational bodies, which in principle have administrative independence, have also been subordinated to the preferences of the executive branch—including the Energy Regulatory Commission (CRE), the National Natural Gas Control Center (CENAGAS), and the National Energy Control Center (CENACE), an entity in charge of guaranteeing state stewardship over transportation and distribution and, therefore, the reliability of power supply. The current administration’s energy policy aims to return to energy self-sufficiency—through the rhetoric of “recovering sovereignty”—under the command of Pemex and the CFE.

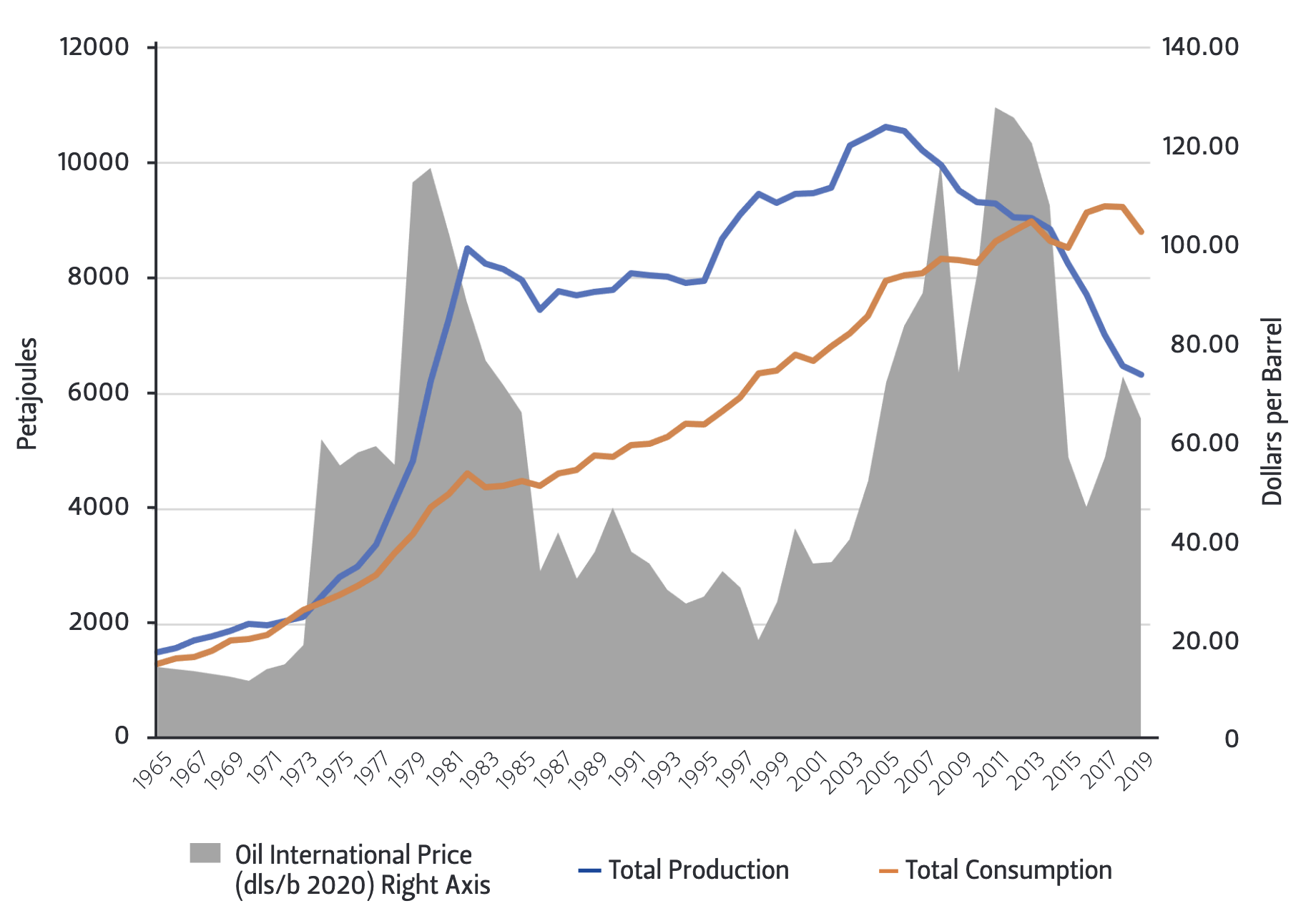

While there appears to be a similarity between López Obrador’s strategy and the one Biden is trying to follow—some form of energy independence—there is an essential difference between the two. Biden’s ambitious technological–industrial and energy plans do not seek to privilege certain companies over others, but rather to develop the research and infrastructure needed to promote the creation of new energy transition technologies. The focal point of Biden’s public interventionist approach is to penalize—for climate, public health, and energy resilience reasons— the consumption of coal (and even hydrocarbons) and to give the green light to investment in renewables. However, in Mexico, the executive branch seeks to ensure, without checks and balances, energy self-sufficiency at all costs while managing the energy transition under the supremacy of public companies. Private capital can join these strategies, but only without undermining the interests of the government and its public companies. If private investments are detrimental to them, then the interests of the former prevail. Moreover, there is no apparent strategy to incentivize renewables. Consequently, even though the López Obrador administration has made energy self-sufficiency its central objective, this goal is still far from being met, since thus far, Pemex has only barely managed to contain the fall in oil and gas production and has not managed to increase it at all. This stagnation spurred a deficit in the balance of oil products and raised gas imports, which currently represent more than 70% of national consumption. Mexico has ceased to be a purely exporting country and has become a net importing one, unlike what happened in the United States. Figure 2 shows this trend clearly and frames, in its historical dimension, the goal of the 2013 reform, which sought to reverse it.4

Figure 2 —Mexico’s Gross Production and Consumption of Energy, 1965–2019

Note The right axis shows international crude oil prices (2020 dollars per barrel).

The most controversial act under the current administration in Mexico was the executive branch’s attempt to promote a constitutional reform that would have reversed the gains made with the 2013 reform, at least in the power sector.5 The initiative, which ultimately failed, was riddled with invectives toward private companies that have participated in the power market for almost 30 years and mandated the renationalization of power generation, placing private generators in constitutional limbo and giving a majority market share (54%) to the CFE. It also suppressed or reduced the powers of regulators such as the CRE and CENACE.

This has not stopped the Mexican government from using its discretionary powers, such as those of co-opted regulatory agencies, to push for a greater market share in favor of the CFE. Its actions have included initiatives that modify the regulation of the power dispatch, changing the way it had been operating since 2016 when the Wholesale Electricity Market was launched, and enforcing criteria that favored the cheapest and most efficient generators over the more expensive ones. In effect, the dispatch was cancelled, giving preference to CFE power generation plants, without regard for costs or environmental impact. Private generators could make up for the power the CFE could not provide—with independent gas-fired producers having primacy—but, even these producers were still forced to sell only to the CFE. Self-supply companies, which generated renewable energy and were a target of attack from the start, were placed last in the list of priorities.

Even more controversial was the fact that the initiative terminated all the contracts in force with the CFE and CENACE and suppressed the clean energy certificates (CELs), a mechanism by which the CRE encouraged the participation of renewable energy companies in electricity generation in order to comply with Paris Agreement commitments. The initiative, therefore, not only stopped the entry of clean energy onto the grid, but also put private participants in legal limbo, canceled their contracts, and gave no indication as to how the damage done to their investments would be compensated. Subsequently, the president warned these companies that they would not be compensated for the cancellation of their contracts, indirectly responding to international companies’ threats to open litigation proceedings if the reform was approved as designed. These companies claimed to be protected by a range of international agreements signed by Mexico, including the United States–Mexico–Canada Agreement and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership. These legal tensions strained the government’s relationship with foreign companies. Mexico’s government, however, has insisted that the operation of the electricity sector has ultimately sought to favor these private companies.

Such an extreme position precipitated the creation of a broad opposition bloc to the constitutional reform, which brought together national and international stakeholders, opposition political parties, non-governmental organizations, and public opinion in favor of decarbonization. Before the constitutional reform was put to a vote, U.S. and Mexican companies, as well as the U.S. government, expressed concern about the political and economic costs of approving López Obrador’s proposal. U.S. Secretary of Energy Jennifer Granholm visited Mexico in January 2022 to raise concerns about the reform’s implications, warning of costly legal disputes if U.S. investments were affected. John Kerry, Biden’s special representative for climate change, visited Mexico three times to speak to its implications for climate change and Mexico’s commitments to reduce greenhouse gas emissions. Letters from Democrats in Congress and a statement from U.S. Trade Representative Katherine Tai highlighted the negative consequences for the Mexican economy and decarbonization if the constitutional reforms were approved.

If politics is above all a game of signs to be interpreted, López Obrador and Biden’s differences on energy matters, as well as on other issues such as Ukraine (Mexico’s rejection of Russia’s intervention but abstention to sanction it), should be considered messages. López Obrador’s refusal to personally attend the Summit of the Americas in Los Angeles from June 6 to June 10, 2022, is yet another sign that he is seeking to increase his political capital by showing his followers and detractors that he maintains a margin of autonomy—even if illusory—with respect to the United States. He also appears to be suggesting that the policy differences he upholds represent the price to pay to safeguard the “sovereignty” of his country vis-à-vis foreign intervention. Mexico maintained a similar position during the Cold War years, above all by refusing to support the embargo against Castro’s Cuba. On that occasion, the government’s objective, in addition to coping with internal support for the Cuban revolution, was to ensure that the Castro government did not attempt to export its revolution to Mexico. Today, López Obrador’s dissent against the United States does not seek to defuse any external pressure or threat, but only to maintain and increase the support of his constituency (as much as possible) to ensure that a candidate from his political party will succeed him once his term is over in 2024.

As anticipated, his party—the National Regeneration Movement, also known by its acronym Morena—did not reach a qualified majority to approve the bill reforming the power sector, yet this was ultimately the goal. López Obrador was not interested in negotiating with the opposition on the reform and never made any effort to reach out to them. In fact, since he knew it was not going to pass, it appears he pushed for it to further polarize the political elite, investors, companies, and stakeholders. He also knew he did not need it to pass, since Mexico’s Supreme Court declared a previous restrictive power law (known as LIE), which was contested by the Federal Commission of Economic Competition (COFECE), constitutional by default. That is, the Supreme Court did not explicitly say that LIE was constitutional, but instead dismissed the lawsuit by COFECE, alleviating some of the country’s polarization and making it possible for López Obrador to not lose face with the much-announced rejection of his proposed constitutional change. In the lawsuit dismissal, four elements of the original constitutional change were preserved anyway: (1) preference of the CFE in the electricity dispatch; (2) review—but not automatic suppression—of contracts, especially self-supply contracts; (3) expansion of the coverage of the CELs, but not their elimination, to cover the CFE’s hydroelectric generation; and (4) the suppression of concessions by the state to exploit lithium. Everything else was noise that the government and Morena took advantage of to raise their popularity and political capital.

In the end, the court’s dismissal and the failure of the constitutional change kept disagreements between the U.S. and Mexico from escalating. Although the U.S. ambassador to Mexico, Ken Salazar, noted that the court’s opinion could still subject Mexico to costly litigation by American companies affected by revision of the contracts, it did not prevent him days later, once the constitutional reform initiative did not achieve the votes in Congress, from participating in a meeting in Veracruz with López Obrador. At this meeting, Salazar reiterated the common interests of the United States and Mexico to invest in and successfully carry out the project in the transisthmian corridor, one of the flagships of the López Obrador administration aimed at modernizing the ports of Salina Cruz (Oaxaca) and Coatzacoalcos (Veracruz) and rebuilding the railroad between both points. For his part, López Obrador invited the affected private companies not to initiate litigation, but instead to negotiate an agreement with the country’s energy authorities.

The New Energy Shock and Its Possible Scenarios

The invasion of Ukraine by Russia on February 24, 2022, shocked energy markets and global politics. Regardless of how the conflict ends and the geopolitical imbalances entailed, the international oil, gas, and coal markets have been profoundly affected, resulting in what could be called a new energy shock. The sanctions imposed on Russia so far could remain indefinitely. Russia is the world’s main energy exporter and in 2020 exported 7.5 million barrels of oil per day, 8.4 trillion cubic feet of gas, and 5.66 exajoules of coal, with most of it going to European countries. In addition, 83% of Russia’s gas exports are by pipeline (of which 85% goes to Europe), and the rest by ship, in the form of liquefied natural gas, so a diversification of shipments is not feasible in the short or medium terms. Given that Moscow is also highly dependent on its fossil export earnings (approximately 30% of fiscal income), both Russian President Vladimir Putin and Western leaders have been cautious about enhancing or neutralizing Putin’s “energy weapon.”

Similar to previous crises, price volatility is not due to a substantial drop in oil or gas supply, but rather to the uncertainty caused by the invasion and the potential effects of Western sanctions on Russia’s hydrocarbon industry, which could include a moratorium on payments and a severe drop in its energy production. In addition, experts from the Organization for Economic Cooperation and Development and the International Monetary Fund have estimated that the crisis could enhance inflationary and recessive pressures resulting from the COVID-19 pandemic, eventually unleashing a global food crisis.6 From a geopolitical point of view, the eventual expansion of NATO—which could include Finland and Sweden—and the strengthening of the Beijing-Moscow axis could accelerate a fragmentation of global markets, including the technology market, exacerbating nationalism of all types. The new energy shock could also either speed up the decarbonization of Western economies or put the development of fossil energy sources back at the center of Western energy policy while energy transition strategies are delayed. How will this shock reverberate in the energy policies of the United States and Mexico?

If the crisis solidifies the Western alliance around NATO and makes it possible to decouple Western economies from Russia’s energy supplies, Washington and Brussels could promote a more accelerated decarbonization that would encourage the rest of the world to comply with what was agreed upon in the Paris Agreement. In 2026, the Western bloc would start imposing trade taxes on the products of countries that did not comply with their national commitments or that resisted upgrading them. This would be possible if Democrats remain in power after 2024, both in the White House and in Congress, giving continuity and strength to the green economy project outlined by Biden.

This would upend López Obrador’s energy strategy. Although the energy shock favors the kind of “recarbonization” promoted by López Obrador (i.e., a transition back to fossil-intensive energy systems), a number of factors could move Mexican energy policy toward something more consistent with that of the Western bloc, including constraints within both Pemex and the CFE to reactivate the energy industry, the need to revive an economy severely affected by the coronavirus pandemic and the current energy crisis, and the eventual imposition of taxes from the United States and Europe for the nation’s carbon footprint in trade. Such a scenario would be possible if a new political coalition comes to power in the 2024 elections in Mexico, and if Democrats remain in power in the U.S. Congress.

On the other hand, if the energy shock were prolonged, provoking a recession and price hikes for energy and food worldwide, investments in fossil fuels would once again become attractive, favoring recarbonization in both the United States and Mexico. The accelerated growth in the production of crude oil, gas, and even coal would also allow the White House to maintain its energy diplomacy to keep Russia’s supply from recovering, even downsizing it if the commercial and financial sanctions remain in place. If Democrats remain in the White House after 2024, they could still stand to lose a majority in the Senate if they hold onto a slim majority in the House. This situation would allow them to save part of their green agenda, although there would be many compromises with pro-fossil lobbies.

A shock that favors recarbonization would give more legitimacy to the statist agenda followed by López Obrador. Under this scenario, in the 2024 elections, Morena would continue in power, with a sovereigntist and self-sufficient discourse similar to the current one. However, given Pemex’s inability to increase its supply of crude oil and gas, whether for financial or technological reasons or both, the new administration could pragmatically return to the bidding rounds to increase the internal supply of hydrocarbons. The entry of private capital would be encouraged, and since prices of imported gas will keep growing, the development of unconventional gas basins located in the Burgos and Sabinas fields would be accepted. The goal of the new administration would be to optimize the revenues generated by an increase in crude oil exports and to reduce the gas imports coming from Texas. The CFE would maintain control of the power sector, choosing directly at its own discretion the private partners from whom it would buy electricity, and successfully dividing green energy generators against gas-fired utilities, delaying the market entry of renewables.

Undoubtedly, the energy policies of the two countries are at a crossroads, the future evolution of which will depend on how global energy markets adjust to the Ukrainian crisis. If hydrocarbon prices remain high in the medium term, as they have been up to now, and the European Union's energy embargo on Russia becomes feasible, Western countries will be able to accelerate their green projects and lead global decarbonization efforts in alignment with the goals of the Paris Agreement.

On the contrary, if Western countries succeed in weakening Putin's energy weapon, which would mean a drop in oil and natural gas prices, the appeal of recarbonization would, paradoxically, become more attractive. However, the outcome will depend on the geopolitical impact of the Ukrainian crisis. If Putin is strengthened after the crisis, the recarbonization of economies will likely continue as a national security measure, especially through public companies, as is the case in Mexico. On the contrary, if Putin’s intentions fail and Russia emerges from the conflict with significantly less geopolitical power, national pressures to ensure energy security are less compelling, making it feasible to negotiate, at the multilateral level, common policies for diversifying the energy mix of most countries following the commitments of the Paris Agreement.

Endnotes

1. Neal E. Boudette and Coral Davenport, “G.M. Will Sell Only Zero-Emission Vehicles by 2035,” New York Times, January 28, 2021, https://www.nytimes.com/2021/01/28/business/gm-zero-emission-vehicles.html.

2. “The Biden plan to build a modern, sustainable infrastructure and an equitable clean energy future,” Joe Biden’s Official Campaign Website, 2020, accessed January 15, 2021, https://joebiden.com/clean-energy/.

3. William Mallett, “Surface Transportation and Climate Change: Provisions in the Infrastructure Investment and Jobs Act (P.L. 117-58),” Congressional Research Service, March 4, 2022, https://crsreports.congress.gov/product/pdf/IF/IF11921.

4. British Petroleum “Statistical Workbook of World Energy,” 2021, 70th edition, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf; Secretaría Nacional de Energía, Sistema de Información Energética, http://sie.energia.gob.mx/.

5. For a detailed account of the trajectory of the power sector reforms, see Miriam Grunstein, When Opposite Poles do not Attract: López Obrador’s Path Toward Electricity Reform in Mexico, Rice University’s Baker Institute for Public Policy, June 8, 2022, https://doi.org/10.25613/20HK-BW11.

6. International Monetary Fund, “World Economic Outlook April 2022: War Sets Back the Global Recovery,” April 2022, https://www.imf.org/en/Publications/WEO/Issues/2022/04/19/world-economic-outlook-april-2022; OECD (Organisation for Economic Co-operation and Development), “Economic and Social Impacts and Policy Implications of the War in Ukraine,” OECD Economic Outlook, Interim Report, March 2022, https://www.oecd.org/economy/Interim-economic-outlook-report-march-2022.pdf.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.