Author(s)

This testimony was delivered before the U.S. Senate Committee on Finance on February 24, 2015.

I. Introduction

Chairman Hatch, Ranking Member Wyden, and Members of the Committee, thank you for inviting me to present my views on the importance of tax reform in promoting growth and efficiency. My testimony will focus on the case for tax reform, general principles that I believe should guide the evaluation of tax reform, and a discussion of the potential economic effects of various tax reform proposals put forth in the last decade. Given the fiscal crisis facing the United States, it is my view that tax reform must minimize the distortionary effects of taxation wherever feasible, seek to maximize long-run economic growth, and make simplicity a priority to achieve reductions in compliance and enforcement costs.

II. The Case for Tax Reform

Individual income tax revenues as a share of GDP are projected to increase significantly even before any policy changes are adopted to address the unsustainable nature of the U.S. budget. The Congressional Budget Office (2014, hereafter CBO) predicts individual income taxes will increase from 8.1 percent of GDP in 2014 to 9.5 percent of GDP in 2025. Under the CBO baseline, individual income taxes are projected to continue to increase to above 10 percent by 2039. Total revenues are projected to increase from 17.6 percent of GDP to 19.4 percent of GDP (only 1.6 percent below the Fiscal Commission target of 21 percent). Unfortunately, these built-in tax increases are not near large enough to offset the projected increases in spending. CBO projects that federal debt held by the public will increase from 74 percent of GDP in 2014 to 106 percent of GDP in 2039 (even under favorable budget assumptions about current law and ignoring the negative effects of higher debt). The obvious conclusion is that the major problem facing the United States is the unsustainable nature of spending increases moving forward. Whether revenue as a share of GDP remains at the projected level or is increased as part of a grand bargain, it is imperative that the United States reform its tax system to reduce economic distortions and maximize economic growth. Otherwise, the combination of rising taxes as a share of GDP and a relatively distortionary tax system could significantly hamper economic growth. This is particularly important given that, in general, economic distortions increase exponentially with the rate of tax.

Indeed, the income tax system in the United States is ripe for reform. The last fundamental reform of the system was the much-celebrated Tax Reform Act of 1986 (TRA86), which followed the classic model of a base-broadening, rate-reducing (BBRR) reform that financed significant corporate and personal rate cuts with the elimination of a wide variety of tax preferences. In the interim, however, many countries around the globe have reformed their tax structures. This is especially true for corporate income taxes abroad, where many nations — at least partly in response to the inexorable forces of globalization and international tax competition (Zodrow, 2010) — have dramatically reduced statutory rates while enacting base-broadening measures that have kept corporate tax revenues roughly constant as a share of GDP (Bilicka and Devereux, 2012). As a result, the United States, which was a relatively low tax country after TRA86, now has the highest statutory corporate tax rate in the industrialized world, and has also lost its advantage in marginal effective corporate tax rates (which take into account other features of a tax system, including accelerated deductions for depreciation and other investment allowances).

Proponents of corporate income tax reform argue that such high tax rates (1) discourage investment and capital accumulation and thus reduce productivity and economic growth; (2) discourage foreign direct investment in the United States while encouraging U.S. multinational companies (MNCs) to invest abroad; and (3) encourage U.S. and foreign multinationals investing in the United States to engage in income shifting, using a variety of techniques to move revenues to low tax countries and deductions to the relatively high tax United States. In addition, the combination of a high statutory tax rate coupled with a wide variety of tax preferences distorts the allocation of investment across asset types and industries and reduces the productivity of the nation’s assets while exacerbating the many inefficiencies of the corporate income tax, including distortions of business decisions regarding the method of finance (debt vs. equity in the form of retained earnings or new share issues), organizational form (corporate vs. non-corporate), and the mix of retentions, dividends paid, and share repurchases (Nicodème, 2008).

A separate issue that has attracted a great deal of attention is the tax treatment of U.S. and foreign MNCs under current law. Following recent reforms in the United Kingdom and Japan, the United States is now the only major industrialized country that operates a worldwide tax system under which the foreign-source income earned by U.S. subsidiaries is subject to a residual U.S. tax when repatriated to the U.S. parent, subject to a credit for foreign taxes paid. By comparison, most other countries — e.g., 28 of the 34 Organisation for Economic Cooperation and Development (OECD) nations — operate a territorial system under which the active foreignsource income of their domestically headquartered MNCs is largely exempt from any residual domestic taxation. Proponents of a move toward a territorial tax system in the United States argue that it would improve the international competitiveness of U.S. multinationals and end the current tax disincentive for the repatriation of foreign-source income that arises as firms defer repatriation to avoid paying residual U.S. taxes.

There is also widespread discontent with the individual income tax system. The top marginal tax rate has increased to 39.6 percent from the 28 percent enacted under TRA86, while the number and value of individual tax preferences has grown substantially. Tax expenditures are defined as “revenue losses attributable to the provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability” by the Congressional Budget and Impoundment Act of 1974 (Joint Committee on Taxation, 2014). According to the U.S. Governmental Accountability Office tax expenditures are approaching the size of discretionary spending in 2013.1 The arguments for reform are the same as those made during the debates surrounding TRA86 (McLure and Zodrow, 1987; Diamond and Zodrow, 2011): high individual tax rates coupled with widespread tax preferences inefficiently distort decisions regarding labor supply, saving, consumption patterns, and methods of compensation; significantly complicate administration of and compliance with the tax system; encourage tax avoidance and evasion; and result in a tax system that is widely perceived to be fundamentally unfair.

These developments have not gone unnoticed in the United States. Numerous proposals for reform have emerged. These include the reports of the President’s Advisory Panel on Federal Tax Reform (2005), the National Commission on Fiscal Responsibility and Reform (2010), and the Debt Reduction Task Force of the Bipartisan Policy Center (2010). In addition, the co-chairs of President Obama’s 2010 fiscal commission, Erskine Bowles and Alan Simpson, issued A Path Forward to Securing America’s Future, which included $2.5 trillion in deficit reduction, a BBRR reform of both the corporate and individual income tax systems that would raise almost $600 billion for deficit reduction, and a switch to a territorial tax system for international income. The most comprehensive proposal for reforming the corporate and individual income tax systems was put forth as a legislative discussion draft on February 26, 2014 by Rep. Dave Camp (R-MI), Chairman of the House Ways and Means Committee.2 However, others have also put forth reform proposals. Senate Finance Committee member Benjamin Cardin (D-MD) introduced a proposal to impose a 10 percent progressive consumption tax that would reduce or eliminate individual income tax rates for most individuals (while maintaining the charitable deduction, state and local tax deductions, health and retirement benefits, and the mortgage interest deduction) and reduce the corporate income tax rate to 17 percent. House Ways and Means Committee member Devin Nunes (R-CA) is working on a proposal to reform business taxes so that the tax rate on corporate and non-corporate businesses would be 25 percent on net business income. The proposal would allow businesses to expense new investments, would limit interest expense deductions, and repeal other existing deductions and credits. This bill does not deal with individual tax issues. Chairman Ryan of the House Ways and Means Committee has stated that tax reform is a major component of the Republican plan to promote economic growth and listed key goals of tax reform, while Finance Chairman Hatch and Ranking Member Wyden established working groups to examine key issues and develop proposals. The President released a framework for business tax reform in 2012 that would reduce the corporate tax rate to 28 percent and broaden the base by taking away business tax preferences. However, on the individual side, the President’s proposals are at odds with most reforms and would be best described as a plan to increase tax rates on capital income (mainly on capital gains and dividend income) and tax expenditures (new $500 second earner tax credit and an increase in the child credit to $3000 per child under five). The phase-outs of the expanded credits would also increase marginal individual income tax rates on labor income for some individuals.

The dilemma facing policymakers is choosing the structure of a tax reform package to meet several different goals.

III. General Principles for Evaluating Reform Proposals

Numerous criteria might be utilized to evaluate tax reform proposals. In my view any viable reform proposal should satisfy at least the following five criteria.

A. Revenue Neutrality

Fundamental reform of the income tax structure is sufficiently difficult that the process of reform should not be encumbered by a requirement to raise additional revenues, which would ensure that many if not most taxpayers would end up being “losers” from reform and make the passage of reform virtually impossible from a political perspective. To the extent that additional revenues will be needed to address our nation’s deficit and debt problems, it is better to raise additional revenues by reforming the structure of the tax system in conjunction with spending reforms that reduce expenditures as part of a sweeping fiscal reform package. Thus, the process can be separated into a two-stage approach to reform — a revenue-neutral fundamental tax reform, followed by fiscal reform that reduces future budget deficits while reaching a compromise on distributional issues and the politically acceptable size of the government. However, it may be reasonable to reverse the order of the two-stage process. For example, President Obama’s fiscal commission adopted targets for revenue (21 percent) and spending (22 percent in the short run and 21 percent in the long run) as a share of GDP.

Decisions regarding the size and scope of government must be left to the political process: a host of instruments, including the use of budget rules to limit expansions of the size of government, are available to reduce current deficits. But perpetuating a highly inefficient and complex tax system in the hopes that it might limit the growth of government is an extremely costly and highly inappropriate way of achieving that goal.

Also, revenue neutrality must be defined broadly to include long-run neutrality. This ensures that the long-run implications of provisions that accelerate revenues (e.g., conversion of retirement savings from traditional IRAs and similar accounts to Roth IRAs) are fully taken into account. At the same time, the definition of revenue neutrality, especially in the long run, should be broad enough to take into account conservative estimates of the dynamic revenue effects of reform-induced increases (or decreases) in economic growth.

B. Equity: Distributional Neutrality and Horizontal Equity

Again, following the approach that was successful in the passage of TRA86, tax reform should be approximately distributionally neutral (using a reasonable revenue baseline). As in the case of revenue neutrality, fundamental tax reform is difficult enough from a political perspective without complicating matters further by attempting to redistribute the tax burden across income classes.

Also, another dimension of equity — the equal treatment of households with similar taxpaying capacity, or horizontal equity — should guide all proposals for fundamental tax reform, as it did in TRA86 and as recommended by virtually all public finance specialists. Note that the implications of adopting horizontal equity as a prime criterion for evaluating reform proposals are far-reaching. In particular, it implies that all forms of compensation, including currently untaxed fringe benefits, should be included in the tax base to the extent administratively feasible.

C. Simplicity

Tax simplicity is often emphasized in early discussions of fundamental tax reform, but is usually largely ignored as the process of tax reform unfolds. This time around simplification should be advanced as an essential criterion for any current reform of the tax system. While some tax complexity is unavoidable in measuring income accurately in today’s complex economy, nevertheless there are many areas in which the tax code could be simplified significantly without seriously compromising accurate income measurement — for example, in the taxation of capital income, ad hoc adjustments for inflation that assume the Federal Reserve Board is successful in achieving its goal of maintaining inflation at around a 2 percent rate, rather than an elaborate system of comprehensive inflation indexing. More generally, any reform should adopt the simplification measures recommended in the 2005 Tax Panel report, including simplifying and coordinating various individual income tax credits including the standard deduction, personal exemptions, and the earned income tax credit; collapsing the current wide array of saving and investment incentives into a very small number of simplified plans; simplifying business accounting rules, especially for small businesses and in the area of depreciation allowances; and eliminating the alternative minimum tax.

D. Economic Efficiency and Tax Neutrality

An essential element of any successful tax reform proposal is the elimination of tax-induced distortions of economic decision-making (other than in a few very narrowly defined activities with widespread economic effects, such as investment in research and development and the emission of pollutants). As stressed in the debate surrounding TRA86, the government should in general not be engaged in an implicit industrial policy by distorting investment decisions through differential tax treatment of various investment activities and business sectors, and similarly should avoid distorting individual consumption decisions. While from a theoretical perspective economic efficiency can require differential tax rates, in practice, when one tempers efficiency considerations with equity concerns and takes into account the economic difficulties in determining an optimally differentiated tax structure and the political and administrative problems of implementing it successfully, simple economic neutrality — uniform tax rates on similar activities in the context of broad-based low-rate taxes — is a reasonable approximation to an efficient tax structure. Accordingly, economic neutrality should be a key guiding principle in the formulation of any fundamental tax reform proposal. This, in turn, has several implications.

Most fundamentally, the general approach to reform should follow the traditional path used in TRA86 of eliminating as many tax preferences as is politically feasible and using the resulting revenues to drastically lower marginal tax rates. This implies that the elimination of many preferences that have long been considered sacrosanct, even those not touched in TRA86, should be considered seriously. Note that such reforms are desirable on efficiency, equity, and simplicity grounds, and also to limit government expenditures that occur through the tax system and are thus subject to less scrutiny than direct expenditures. Moreover, many tax preferences are poorly designed in any case. The home mortgage interest deduction, discussed further below, is an excellent example. Although its primary purpose is to encourage home ownership over renting, it is very poorly designed to achieve this goal, as it offers little or nothing to low- and middle-income individuals who do not itemize, have total deductions that are less than or roughly equal to the standard deduction, or are subject to relatively low marginal tax rates. Instead, the vast majority of the benefits of the home mortgage interest deduction accrue to high-income taxpayers, encouraging overconsumption of housing at the expense of less investment in the rest of the economy.

In addition, neutral tax treatment should also be applied to saving decisions, that is, current consumption should not be favored over future consumption. In principle, this implies the tax base should be consumption rather than income. If the replacement of the income tax with a full-fledged consumption-based tax is not feasible at the current time, current personal income tax provisions that encourage saving should be maintained (although they should be simplified, along the lines described previously), and serious consideration should be given to reducing the burden of the corporate income tax on investment income. This would help alleviate the distortionary costs associated with the double taxation of corporate income.

E. Favorable Environment for Foreign Investment

Finally, in today’s globalized economy, the income tax system in the U.S. should not put our multinational companies at a disadvantage relative to competing firms based in other countries; at the same time it should discourage tax evasion and tax avoidance, especially in the form of income shifting to low-tax countries. In particular, the tax system should not discourage foreign investment by U.S. multinationals or discourage investment in the U.S. by foreign multinationals. Although a full discussion of the intricacies of the tax treatment of foreign investment is far beyond the scope of this testimony, note that (1) in order to make investing in the U.S. attractive to foreign multinationals, the taxation of capital income in the U.S. should be concentrated at the individual level; (2) the “territorial” system advocated in the “Simplified Income Tax” proposed by the 2005 Tax Panel has the advantage of putting U.S. multinationals on an equal footing with most of their competitors, but exacerbates incentives for shifting income abroad and requires complex allocations of U.S. costs across domestic and foreign activities; (3) any approach that instead increased the inclusion of foreign income in the tax base of U.S. firms (e.g., the elimination of deferral) should be accompanied by corporate income tax rate reductions that would leave effective tax rates approximately constant; and (4) another advantage of low statutory rates under the corporate income tax is that they reduce incentives for income shifting to other countries with relatively low tax rates.

IV. Economic Effects of Various Tax Reform Proposals

An important argument in favor of macroeconomic analysis is that it would potentially inform policy makers explicitly about the long-run growth effects of alternative policies, and thus allow for the adoption of a more efficient tax system and increased long-run economic growth. This section discusses the macroeconomic effects of various tax policies and reform proposals in an effort to inform the debate on structuring tax reform.

A. Several Studies Comparing the Macroeconomic Effects of Various Taxes

The Organisation for Economic Co-operation and Development (OECD, 2008) compares different types of taxes in terms of their effects on economic growth. The OECD study concludes that corporate taxes are the most harmful to growth, followed by personal income taxes (including payroll taxes). High marginal personal income tax rates are also shown to discourage entrepreneurial activity. By comparison, consumption taxes have smaller negative effects on growth, while property taxes are estimated to be the least harmful. These results are broadly consistent with a large body of research that argues that consumption-based taxes are generally more efficient than income-based taxes, and that increases in corporate income and dividend taxes create large distortions relative to other taxes and should be minimized. In fact, the downward pressure on corporate tax rates around the world is evidence that many countries view high corporate tax rates as a impediment to growth, especially with an increasingly integrated global economy and an increase in the mobility of the capital stock.

Diamond and Viard (2008) draw similar conclusions. They analyzed the macroeconomic effects of a permanent tax rate reduction on different types of income, including wage, interest, dividend, and corporate income, as well as the effects of a permanent increase in tax credits and deductions. They used the DZ model to simulate each of these tax rate reductions assuming that the reduction was debt-financed for 10 years and then paid for by either a reduction in discretionary transfer payments or an across-the-board tax increase. The magnitude of the tax reduction is determined so that the decrease in revenue over the 10-year period following enactment is $500 billion with no behavioral responses. They found that the wage, dividend and corporate rate reductions led to an increase in GDP in the long run if discretionary transfer payments were reduced. The increase in GDP was largest for the reduction in dividend and corporate tax rates. Note that an increase in personal tax credits decreased GDP in this case. If the cuts were offset by an across-the-board tax increase, the effect on GDP was negative for all of the tax cuts except for the dividend tax cut, which had no effect on GDP. The largest decrease in GDP (0.8 percent) occurred for the increase in tax credits (i.e., spending through the tax system). The implication is clear: a broad-based, low-rate tax system will increase economic growth while a narrow-based, high-rate tax system will reduce economic growth. President Obama’s latest proposals move the United States toward a more narrow-based, high-tax rate system. These proposals are likely to reduce job growth and living standards in the United States and should be rejected.

The Joint Committee on Taxation (2005, hereafter JCT) examined the macroeconomic effects of three proposals that each provide $500 billion in tax reductions. The three proposals examined were a decrease in individual income tax rates, an increase in the personal exemption, and a decrease in the corporate income tax rate. They showed that an individual rate reduction would increase GDP by 0.3–0.4 percent in the long run if government spending were decreased to stabilize the debt to GDP ratio after 10 years. In the case of no fiscal offset, so that debt increases as a share of GDP, the individual rate reduction led to a decrease in GDP in the long run ranging from 0.2–0.5 percent. A corporate rate reduction led to an increase in GDP in the long run ranging from 0.5–0.9 percent if government spending were decreased to stabilize the debt to GDP ratio after 10 years, an increase in GDP ranging from 0.5–0.6 percent in the long run with a decrease in personal exemptions, and an increase in GDP in the long run ranging from 0.0–0.3 percent with no fiscal offset (the case in which debt increases as a share of GDP). Finally, they reported that an increase in personal exemptions led to an decrease in GDP in the long run ranging from 0.4–0.7 percent with no fiscal offset, and that an increase in personal exemptions increased GDP in the long run by 0.1–0.2 percent if it is offset with a decrease in government spending (substituting spending through the tax code for direct spending). The results indicate that corporate tax reductions have the largest growth effects, followed by individual income tax reductions, and then an increase in the personal exemption (which reduces growth unless government spending is reduced). The order of the growth effects of the tax reductions is consistent with the findings reported in OECD (2008) and Diamond and Viard (2008). This implies that to maximize U.S. economic growth policymakers should adopt a tax system characterized by low capital income tax rates, low individual income tax rates, and minimal tax expenditures. To achieve this outcome, the United States could follow the BBRR reform approach such as the Tax Reform Act of 1986 or a modification of the recently proposed Tax Reform Act of 2014. Alternatively, the United States could also adopt a more modern approach and move toward some form of a consumption-based tax system.

B. Dynamic Analysis of the Tax Reform Act of 2014

The Tax Reform Act of 2014 was a comprehensive proposal for reform of both the corporate and personal income tax systems. The corporate income tax (CIT) reform was structured as a traditional base-broadening, rate-reducing reform. The plan would have lowered the CIT rate to 25 percent, phased in over five years, and eliminated a variety of business tax preferences, including accelerated depreciation (so that tax depreciation would approximate economic depreciation), expensing of research and development costs and half of advertising costs, and the deduction for domestic production. The plan would have not allowed the last-in first-out (LIFO) inventory accounting rule and would have permanently created a 15 percent tax credit for research and development expenses.

The reform also changed the treatment of foreign source income, including moving to a 95 percent participation exemption (territorial) system. In this case, the effective tax rate is roughly 1.25 percent with a 25 percent CIT rate. It also allowed for current taxation of foreign source income from intangibles, defined as income in excess of 10 percent on basis in depreciable assets (excluding other subpart F income and commodities income) due to foreign sales at a minimum tax rate of 15 percent (25 percent for U.S. sales), subject to foreign tax credits. The 15 percent rate also applied to intangibles income (income in excess of 10 percent on basis in depreciable assets other than from commodities) on sales to foreign markets from the United States. The reform would have limited subpart F income to low-taxed income and created a minimum tax of 12.5 percent for foreign sales and active financial services income, in addition to the minimum tax rates noted above. There was also a one-time tax on the stock of unrepatriated profits, at an 8.75 percent rate on cash and equivalents and at a 3.5 percent rate on illiquid assets.

The plan would have also reformed the tax treatment of individual income by broadening the tax base and lowering the rates on individual income. It would have included a 10 and 25 percent rate bracket, with a 10 percent surtax on high-income households (above $450,000 for married couples). The standard deduction, child credit, and the 10 percent bracket would have been phased out for high-income households. The plan would have repealed itemized deductions for state and local (non-business) taxes, medical expenses, personal exemptions, and the alternative minimum tax. In addition, it would have limited the mortgage interest deduction. Capital gains and dividends would have been taxed as normal individual income after a 40 percent exclusion.

The Diamond-Zodrow computable general equilibrium model was used to simulate the effects of TRA 2014. The model is structured so that consumers choose consumption, labor supply, and saving to maximize welfare over their lifetimes. The model includes 55 adult generations (intended to capture an adult’s working life from age 23 to 78) alive at any point in time, and is thus typically described as an overlapping generations model. Firms choose labor demand and the time path of investment to maximize profits, subject to adjustment costs. The model includes five different production sectors, including a multinational corporation (MNC), a domestic corporation, a non-corporate (pass-through) firm, and owner- and rental-housing sectors. In addition, the corporate firms have a variable debt-to-equity ratio. The government uses corporate and personal income taxes to finance a fixed level of government services. The model must begin and end in a steady-state equilibrium with all key macroeconomic variables growing at an exogenous growth rate (which equals population plus productivity growth). The model is calibrated to roughly match the U.S. economy in a given base year.

The model includes domestic and foreign MNCs (parents and subsidiaries) with highly mobile firm-specific capital (FSK) that earns above-normal returns, and relatively immobile ordinary capital that earns normal returns. This approach follows Becker and Fuest (2011) who argue that differential capital mobility is an important part of modeling international capital flows. All of the multinational corporations — the US-MNC parent firm and its foreign subsidiary, and the foreign-based RW-MNC parent firm and its U.S. subsidiary — are assumed to have analogous production functions. The modeling approach we utilize generally follows the approach for firm-specific capital developed by de Mooij and Devereux (2009) and Bettendorf, Devereux, van der Horst, Loretz, and de Mooij (2009). The MNC is assumed to own a unique firm-specific production input (FSK) — such as patents or other proprietary technology, brand names, or good will — coupled with unique managerial skills and knowledge of production processes, which allow it to permanently earn above-normal returns. This firm-specific factor is treated as “quasi-fixed,” as it is assumed to be fixed in total supply in any given period, but this fixed amount can be reallocated across the United States and the rest of the world (ROW). The main role of this assumption is to determine the fraction of production using FSK that occurs in the United States relative to the rest of the world. The elasticity of the location of production that uses FSK (whether FSK is used in the U.S. or ROW) with respect to the tax rate differential is assumed to be 8.6, which is calculated from the assumption that the capital-share-weighted aggregate portfolio elasticity of all capital (both FSK and ordinary capital) is 3.0. The basic idea is that the location decision of where to use FSK is highly elastic with respect to the tax rate differentials, although we do phase in over time the reallocation of production involving FSK in response to changes in relative taxes. In addition, MNCs engage in income shifting that depends on the tax differential between the U.S. and ROW, including tax havens. MNCs must make a repatriation decision and are subject to a residual U.S. tax on repatriations. The model includes foreign trade, international capital mobility, and foreign ownership of domestic capital. Ordinary capital (capital that earns a normal rate of return) is disaggregated into structures, equipment, and inventories.

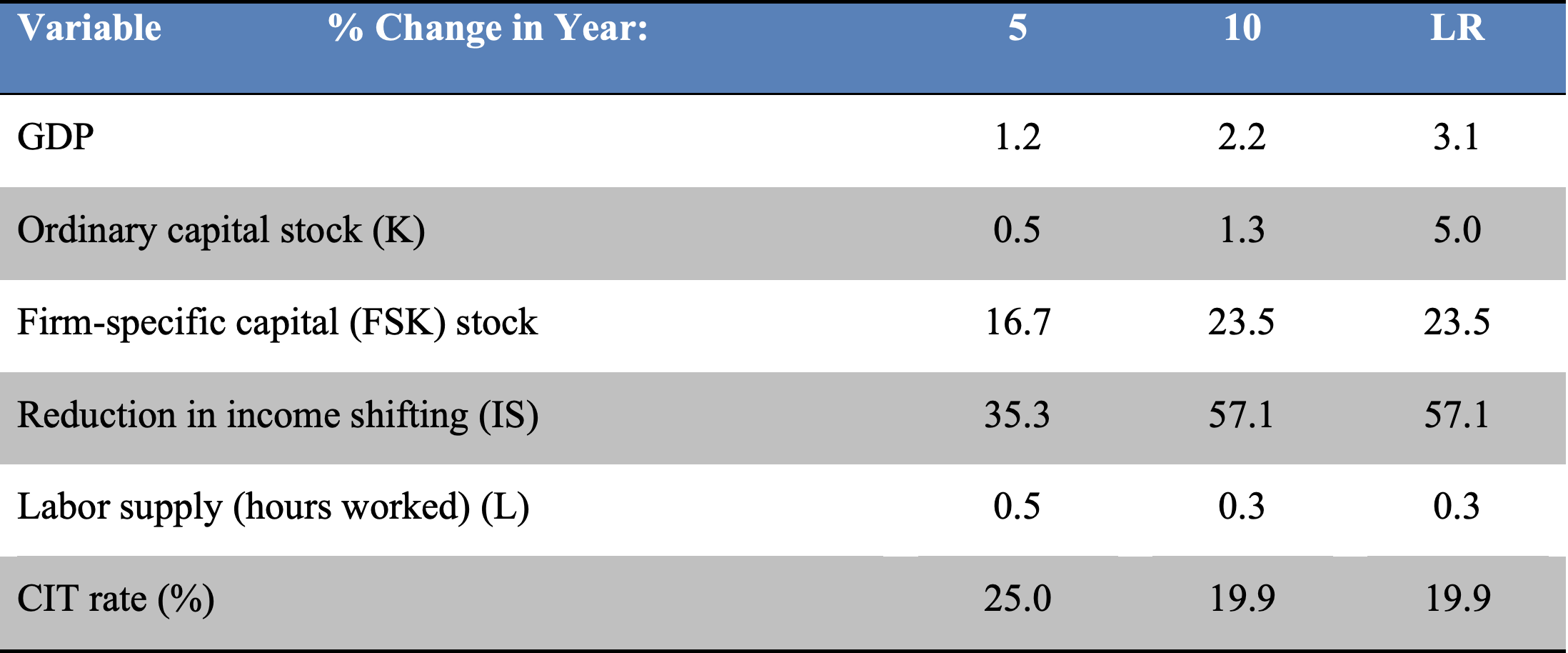

Table 1 shows the Diamond and Zodrow (2014) analysis of TRA 2014, which was prepared for the Business Round Table (BRT). The most important factor is the reduction in income shifting as the CIT rate declines. In addition, other important factors include the move to a territorial tax system, the more efficient allocation of the ordinary capital stock (K), and the reallocation of FSK (although this effect has a relatively small affect on the results).

Table 1 — Diamond-Zodrow Analysis of Camp for BRT

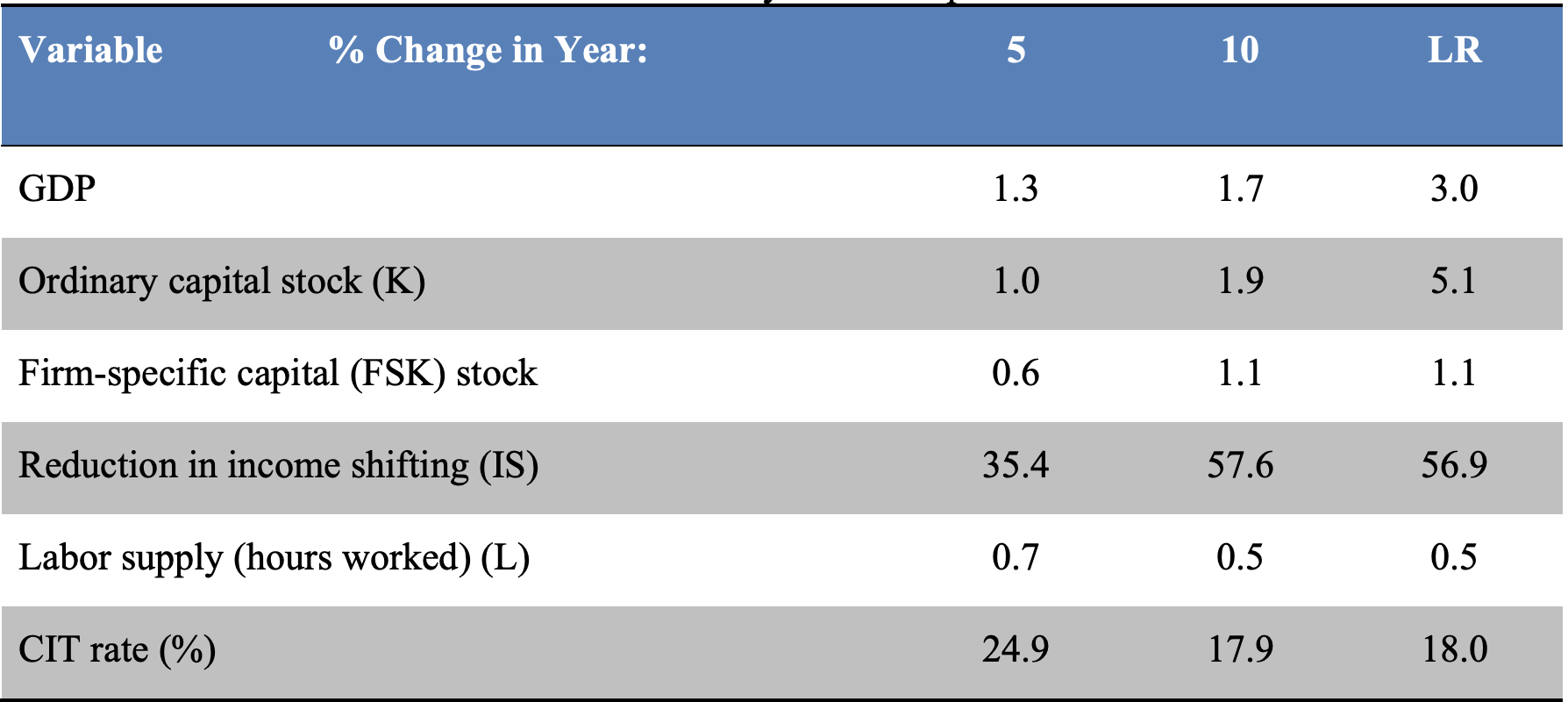

The DZ model includes differential capital mobility by having one capital good that is relatively immobile and another capital good that is assumed to be highly mobile. An important question is how this assumption affected the reported results. Table 2 shows the effects of adopting TRA 2014 under the assumption that all capital is relatively immobile (both capital goods have an elasticity of 0.5 with respect to the tax rate differential). In this case, GDP increases by 1.3 percent instead of 1.2 percent five years after reform, by 1.7 percent instead of 2.2 percent 10 years after reform, and by 3.0 percent instead of 3.1 percent in the long run. Without differential mobility, FSK increases by 0.6 percent five years after reform and 1.1 percent in the long run instead of 16.3 percent and 23.5 percent. The labor supply increase is slightly higher in this case. This demonstrates that the addition of FSK is not driving the results in the DZ analysis. Although the reallocation of FSK to the United States increases production of the good produced by the U.S. multinational, the GDP effects of this reallocation are offset by other factor reallocations, especially a return of ordinary capital to the rest of the world.

Table 2 — Diamond-Zodrow Analysis of Camp With Immobile FSK

By comparison, the Tax Foundation found much smaller results, with only a 0.2 percent increase in GDP in long run. The small size of its result is attributable primarily to a reduction in the capital stock of 0.2 percent as the cost of capital increases under TRA 2014. The Tax Foundation predicted that labor supply would increase by 0.5 percent. But, the Tax Foundation analysis discusses, then ignores, the benefits of reduced income shifting, the benefits of reallocation of firm-specific capital to the United States, and the benefits of moving to a territorial system. The DZ analysis included these factors in modeling the effects of the Camp proposal.

However, the DZ model can be used to find similar effects to those presented by the Tax Foundation. For example, using the DZ model and simulating the effects of a similar (the base broadeners are slightly different) CIT reform (but no individual income tax reform) while ignoring the three factors above produces significantly negative effects, with GDP down 1.7 percent in long run, and a CIT rate reduction to only 31.4 percent (reducing the rate to 25 percent would produce results more similar to the Tax Foundation results). In particular, this illustrates the significant impact on GDP of reversing income shifting and using the revenue gains from reform to further lower the corporate income tax rate.

There are several lessons that can be drawn from these simulations. First, a BBRR reform that repeals targeted investment incentives — such as eliminating accelerated depreciation or other incentives that affect investment at the margin — to finance rate reductions grants a windfall gain to existing capital by reducing the tax rate applied to such capital, with the windfall exacerbated by the existence of above-normal rates of return. The resulting increase in the cost of capital reduces investment and output, and makes it much less likely that a BBRR reform will result in positive macroeconomic effects in both the short and long run.

Second, the international considerations stressed above make it more likely that a BBRR reform will generate positive macroeconomic effects. A reduction in the statutory corporate income tax rate will result in a reallocation of highly mobile firm-specific capital that earns above-normal returns to the United States — although this effect is offset to a significant extent by other general equilibrium effects, including the return of ordinary capital to the rest of the world and a reduction in labor supply. More importantly, a reduction in the statutory corporate income tax rate reverses some income shifting from the U.S., which provides a “free” source of revenue — effectively a CIT rate cut without the costs of base broadening — that significantly increases the benefits of a BBRR reform. In addition, the changes in trade that accompany a reversal of income shifting also have important effects, increasing net exports and thus output. Note, however, that the amount of income shifting in the initial equilibrium, as well as the extent of the reversal of this income shifting with a reduction in the CIT rate in the United States, are open to debate, and that the macroeconomic benefits of a BBRR reform would be significantly reduced if the extent to which income shifting is reversed with U.S. CIT rate cuts were smaller than assumed in the simulations.

Third, although the simulations indicate that the net macroeconomic effects of the particular territorial tax reform analyzed are positive, the gains from such a reform are fairly modest. This is not surprising: since the current worldwide tax system — which taxes foreign source income only when repatriated and allows foreign tax credits (including cross-crediting of taxes from high-tax countries against income from low-tax countries) — imposes a very low residual U.S. tax rate on repatriations, switching to a territorial system is likely to have relatively limited macroeconomic effects. However, this also implies that repealing deferral could lead to significant losses in output to the extent it adversely affects the U.S. MNCs ability to compete with foreign MNCs.

Finally, as noted above, the net effect of all these factors implies that the macroeconomic effects of a BBRR reform depend very much on both the details of the specific reform proposal and the context in which it is imposed. These results indicate that a BBRR reform is more likely to result in positive macroeconomic effects if (1) the initial amount of income shifting is large and is reduced significantly when the statutory CIT rate in the United States declines; (2) accelerated depreciation is retained instead of being used as a base broadening provision; and (3) the BBRR reform includes a move to a territorial system of the type analyzed in the report, that is, one that includes anti-base erosion provisions that are sufficiently effective that the tax sensitivities of international capital and income shifting are the same as prior to the enactment of the reform.

C. The President's Advisory Panel on Federal Tax Reform

The President’s Advisory Panel on Federal Tax Reform (the Tax Panel) was charged with developing options for reforming the current federal income tax system that are simple, fair and pro-growth. This section discusses the economic growth effects of the three tax reform options discussed by the Tax Panel. The report showed that the largest increases in capital accumulation and economic growth were associated with the reforms that most resembled a move from an income to a consumption tax. This result is consistent with a wide body of previous research (Altig et al., 2001; Auerbach and Kotlikoff, 1987; Joint Committee on Taxation, 1997).

The Tax Panel’s Progressive Consumption Tax (PCT) is a modified version of David Bradford’s X-tax. The plan is a bifurcated subtraction-method VAT where labor compensation is deducted at the business level and taxed at the individual level at progressive rates of 15, 25, and 35 percent. All business investment is expensed and interest is not included nor deducted from the tax base.

The PCT proposed reforming the mortgage interest deduction to a 15 percent tax credit for mortgage interest payments that was capped and nonrefundable. The PCT was structured as a business cash flow tax and a tax on wages above the threshold of $115,000 for married couples at a statutory rate of 35 percent. The PCT provided subsidies to debt-financed owner-occupied housing (through the 15 percent mortgage interest credit). In general, the primary distinction between income- and consumption-based taxes is that under an income tax the normal return to capital is taxed, while under a consumption tax the normal return to capital is exempt from tax. In the case of the PCT, expensing of new business investment reduces the marginal effective tax rate on the normal rate of return to zero (since the value of the upfront deduction just equals the present value of tax paid on the normal return to the investment).

While the business cash flow tax effectively exempts the normal rate of return on new investments from taxation, it does impose a one-time tax on business capital existing at the time of reform to the extent that transition relief is not provided. The PCT would have included transition relief for old capital of approximately $400 billion during the first four years after the enactment reform. The present value of the transitional depreciation deductions is approximately one-quarter of the value of future depreciation deductions under current law, which implies that the vast majority of existing business capital faces a one-time tax.

Adopting a consumption tax should lead to more saving and investment, and thus higher levels of output and consumption in the long run. The Panel reported that in the long-run the capital stock increased by 15.2 percent, national income increased by 4.0 percent, and consumption increased by 3.4 percent (all results are from a closed economy version of the DZ model and relative to initial baseline values). These results are similar to other results found in the literature. For example, using an OLG model, Altig et al. (2001) estimated that an X-tax would lead to a 6.4 percent long-run increase in national income and a 21 percent increase in the capital stock.

The Growth and Investment Tax (GIT) is similar to the PCT but includes an additional tax on interest, dividends and capital gains at a rate of 15 percent at the individual level. This allows for lower tax rates on business cash-flow and wages compared to the PCT. The plan also expands the opportunities to save in tax-preferred accounts. Given this, the marginal effective tax rate is only 5.2 percentage points higher under the GIT compared to the PCT because of the expanded savings accounts and the relatively low statutory tax rate on individual capital income. This implies that the growth effects for the GIT should be almost as large as those under the PCT. In this case, moving to full expensing of business investment encourages new investment and thus an increase in the size of the economy in the long run, which is mitigated slightly by the increase in taxation of capital income at the individual level. For example, the capital stock increases by 11.1 percent in the long run (using the OLG model) — this is about 70 percent of the growth in the capital stock under the PCT. The size of the economy is projected to increase by 3.3 percent in the long run.

The Tax Panel also recommended the Simplified Income Tax (SIT). The plan reduces the double taxation of corporate income by providing full dividend exclusion and 75 percent exclusion of capital gains on corporate stock. Other capital gains are taxed at ordinary rates. This reform called for a reduction in the corporate income tax rate to 31.5 percent and a reduction in the top individual income tax rate to 33 percent. The rate reductions were financed by broadening the individual and business tax bases. As in the GIT, tax preferred saving opportunities were also expanded. The plan also proposed a simplified system for depreciation allowances that would slow down the cost recovery for capital. The net effect was a 2 percentage point reduction in the effective marginal tax rate on capital income. This implies that the SIT would have limited effects on the size of the long-run capital stock and economic growth. For example, the capital stock is only 1.4 percent higher in the OLG model simulations, and the long-run increase in the size of the economy is 1.2 percent.

In the end, the Tax Panel did not recommend switching to a consumption-based tax system (such as the PCT); instead the Tax Panel recommended the GIT and SIT, even though the growth effects of the consumption-based tax were larger. However, given the fiscal challenges facing the United States it may be time to adopt a reform that maximizes the accumulation of capital and economic growth in the long run, especially if it can implemented in a manner that maintains distributional neutrality as argued for above.

D. Other Ambitious Reform Proposals

As mentioned in the introduction there are a number of other reform proposals other than those discussed above. For example, Auerbach (2010) proposes reforming the current corporate income tax system by allowing an immediate deduction for all new investment as a replacement for the current depreciation system and moving to a system that only taxes transactions that occur in the United States (i.e., a destination-based cash-flow tax). In addition, the proposal would allow for the symmetric treatment of debt and equity by including the proceeds of new debt in the tax base and excluding the repayment of debt. Auerbach argues that such a reform would reduce the most distortionary and complex problems with the current corporate tax system, increase progressivity, and increase output potentially by as much as 5 percent. He also argues that maintaining the current corporate tax system and reducing the tax rate, as proposed under a BBRR approach, “would leave in place all the flaws of the existing system,” such as the tax bias favoring debt finance under the current income tax (which arises because interest on debt is deductible but dividends paid to shareholders are not).

Diamond and Zodrow (2011) propose that as part of the process of fundamental tax reform, serious consideration should be given to the implementation of an “allowance for corporate equity” or “ACE” that would result in roughly uniform treatment of debt and equity finance and lower the taxation of investment income at the business level to that associated with a consumption-based tax. This approach, which was recommended recently by the tax reform commission headed by Nobel Prize winning economist James Mirrlees in the United Kingdom and has been implemented successfully in a small number of countries, allows firms an extra deduction equal to the product of the book value of equity capital and a risk-free nominal interest rate. The economic effect of the ACE is to put debt and equity finance on an equal footing at the business level, as the ACE deduction for equity-financed investment is comparable to the deduction of interest expense for debt-financed investment. Moreover, the ACE approach can be applied to all businesses, perhaps with an exception for small firms, and thus would eliminate the current income tax bias against corporate entities.

There are certainly other proposals that are worthy of consideration as well.

V. Conclusion

Several recent reports on fixing our nation’s fiscal crisis have focused attention on the need for fundamental reform of the corporate and personal income tax systems. While several factors seem to make the enactment of such a reform somewhat more difficult than in 1986, a sweeping reform of the tax system is well overdue. In my view, given the fiscal crisis facing the United States, fundamental reform must minimize the distortionary effects of taxation wherever feasible, seek to maximize long-run economic growth, and make simplicity a more important goal to achieve reductions in compliance and enforcement costs. While there are many proposals that are worthy of consideration, we must ultimately choose one. Macroeconomic analysis of various proposals and provisions should offer guidance in that process.

References

Altig, David, Alan Auerbach, Laurence Kotlikoff, Kent Smetters and Jan Walliser. 2001. “Simulating Fundamental Tax Reform in the United States.” American Economic Review 91:574-595.

Auerbach, Alan J. and Laurence J. Kotlikoff. 1987. Dynamic Fiscal Policy (Cambridge University Press: Cambridge).

Auerbach, Alan (2010). “A Modern Corporate Tax,” The Hamilton Project, Brookings Institution Washington, DC. Available at http://www.hamiltonproject.org/papers/a_modern_corporate_tax/.

Bettendorf, Leon, Michael P. Devereux, Albert van der Horst, Simon Loretz, and Ruud de Mooij 2009. “Corporate Tax Harmonization in the EU.” CPB Discussion Paper 133. CPB Netherlands Bureau for Economic Policy Analysis, The Hague, Netherlands.

Bilicka, Katarzyna, and Michael Devereux, 2012. “CBT Corporate Tax Ranking, 2012.” Working paper. Centre for Business Taxation, Oxford University, Oxford, UK.

Bowles, Erskine and Alan Simpson, 2013. “A Bipartisan Path Forward to Securing America’s Future,”http://www.momentoftruthproject.org/sites/default/files/Full%20Plan%20of% 20Securing%20America's%20Future.pdf

Congressional Budget Office, 2014. The Long-Term Budget Outlook. Congressional Budget Office, Washington, DC.

Debt Reduction Task Force of the Bipartisan Policy Center, 2010. Restoring America’s Future: Reviving the Economy, Cutting Spending and Debt, and Creating a Simple, Pro-Growth Tax System. Bipartisan Policy Center, Washington, DC.

de Mooij, Ruud, and Michael P. Devereux, 2009. “Alternative Systems of Business Tax in Europe: An applied analysis of ACE and CBIT Reforms,” Taxation Studies 0028, Directorate General Taxation and Customs Union, European Commission.

Diamond, John W., and Alan D. Viard, 2008. “Welfare and Macroeconomic Effects of Deficit– Financed Tax Cuts: Lessons from CGE Models.” In Viard, Alan D. (ed.), Tax Policy Lessons from the 2000s, 145–193. The AEI Press, Washington, DC.

Diamond, John W., and George R. Zodrow, 2014. “Dynamic Macroeconomic Estimates of the Effects of Chairman Camp’s 2014 Tax Reform Discussion Draft,” available at http://businessroundtable.org/sites/default/files/reports/DiamondZodrow%20Analysis% 20for%20Business%20Roundtable_Final%20for%20Release.pdf.

Diamond, John W., and George R. Zodrow, 2011. “Fundamental Tax Reform: Then and Now,” Baker Institute for Public Policy Report, Rice University, published in the Congressional Record, JCX-28-11, pp. 27–38.

Joint Committee on Taxation, Washington, DC. Joint Committee on Taxation, Estimates of Federal Tax Expenditures for Fiscal Years 2014– 2018 (JCX–97–14), August 5, 2014.

Joint Committee on Taxation, Macroeconomic Analysis of Various Proposals to Provide $500 Billion in Tax Relief, (JCX–4–05), March 1, 2005.

Joint Committee on Taxation. 1997. Joint Committee on Taxation Tax Modeling Project and 1997 Tax Symposium Papers (JCS–21–97).

McLure, Charles E., Jr., and George R. Zodrow, 1987. “Treasury I and the Tax Reform Act of 1986: The Economics and Politics of Tax Reform.” Journal of Economic Perspectives 1 (1), 37–58.

National Commission on Fiscal Responsibility and Reform, 2010. The Moment of Truth: Report of the National Commission on Fiscal Responsibility and Reform. U.S. Government Printing Office, Washington, DC.

Nicodème, Gaëtan, 2008. “Corporate Income Tax and Economic Distortions,” CESifo Working Paper No. 2477. CESifo, Munich, Germany.

Organisation for Economic Co-operation and Development, 2008. “Taxes and Economic Growth,” Economics Department Working Paper No. 620. http://www.oecd.org/tax/taxpolicy/41000592.pdf.

The President’s Advisory Tax Panel on Federal Tax Reform. 2005. Simple, Fair, and ProGrowth: Proposals to Fix America’s Tax System (U.S. Government Printing Office: Washington, DC).

Zodrow, George R., 2010. “Capital Mobility and Tax Competition.” National Tax Journal 63 (4, Part 2), 865–902.

Zodrow, George R., and John W. Diamond, 2013. “Dynamic Overlapping Generations Computable General Equilibrium Models and the Analysis of Tax Policy.” In Dixon, Peter B., and Dale W. Jorgenson (eds.), Handbook of Computable General Equilibrium Modeling, Volume 1, 743–813. Elsevier Publishing, Amsterdam, Netherlands.

Endnotes

1. The GAO issue summary is located at http://www.gao.gov/key_issues/tax_expenditures/issue_summary#t=0.

2. The legislative text of the discussion draft is available at http://waysandmeans.house.gov/UploadedFiles/Statutory_Text_Tax_Reform_Act_of_2014_ Discussion_Draft__022614.pdf. Analysis of the draft legislation by the Joint Committee on Taxation is available at https://www.jct.gov/.