Author(s)

The Tax Cuts and Jobs Act of 2017 (TCJA, Pub. L. 115–97) placed a $10,000 limit on state and local tax (SALT) deductions. Previously, there was no cap on the amount taxpayers could claim for the deduction. Several states have since proposed or passed legislation to circumvent the limit. In response, the IRS first issued a warning against such state actions in May,1 which was followed by proposed regulations from the U.S. Department of Treasury in August to block these attempts.2 Four states (New York, Connecticut, Maryland, and New Jersey) filed a lawsuit against the federal government, claiming the cap unfairly targeted them and represented the federal government’s interference with state’s rights guaranteed in the Constitution.3 In November, the federal government sought to dismiss the lawsuit, arguing that the states do not have legal standing to file the lawsuit; instead, taxpayers in these states should bring the case to court if they choose to do so.4

Beyond the pointed statements between the federal and state government officials, these arguments bring up an important issue: What are the existing fiscal interactions between the federal and state governments, and how would the SALT deduction cap change these dynamics? This report first reviews the current fiscal connections between the governments, then summarizes the viewpoints in favor of and against a SALT deduction limit. It next discusses states’ recent actions to mitigate the effects of the cap, federal government reactions, and individual-level workaround actions.

Fiscal Connections Between the Federal and State Governments

Fiscal federalism, which describes the financial relations between different levels of government based on their respective responsibilities, is a unique and indispensable feature of a federal government system. In the U.S., the federal government provides substantial financial assistance to state and local (SAL) governments. This report focuses on two of the largest federal support mechanisms—federal grants and the SALT deduction.5 These instruments are administered through different procedures; the grants are channeled through the federal budget process, whereas the SALT deduction is provided through the tax code.

Federal Financial Assistance Through Grants

In FY 2018, which ran from October 1, 2017, to September 30, 2018, the federal government provided SAL governments with roughly $728 billion in federal grants, accounting for about one-third of state governments’ total funding.6 Federal grants to SAL governments have generally increased over time, with a surge from FY 2008 to FY 2010 due to increased federal aid to help states recover from the Great Recession.7

Once Congress decides that grants are the best funding mechanism to achieve certain policy objectives, it can choose from three types of grants: categorical grants, block grants, and general revenue sharing.8 These grants differ mainly in terms of how much federal control is involved.

Specifically, categorical grants are limited to narrowly defined activities, and thus have the highest federal restrictions. States have to follow the federal government’s guidance regarding what the funds may be spent on, which residents would be eligible to receive funds, and how to operate the programs. On the other hand, block grants allow more discretion over the use of the funds, which enables states to disburse them for a wider set of activities. General revenue-sharing agreements can be used for any purpose not expressly prohibited by federal or state law; hence, they have the least federal restraint.

In FY 2017, 1,319 federal grants were awarded to SAL governments, of which 1,299 grants (over 98%) were categorical grants and 20 were block grants; none of the grants were revenue-sharing arrangements. The dominance of categorical grants as a share of total overall federal grants has been consistent over time. A recent Congressional Research Service (CRS) study observes the following trends: First, Congress has the tendency to use federal grants to create jobs and promote economic growth, which implies that the federal grant amounts will continue to grow, though at a slower rate. Second, the federal government increasingly tends to use financial means to influence SAL government policies. Thus, the system of financial governance between the federal and SAL governments has become more centralized over time.9

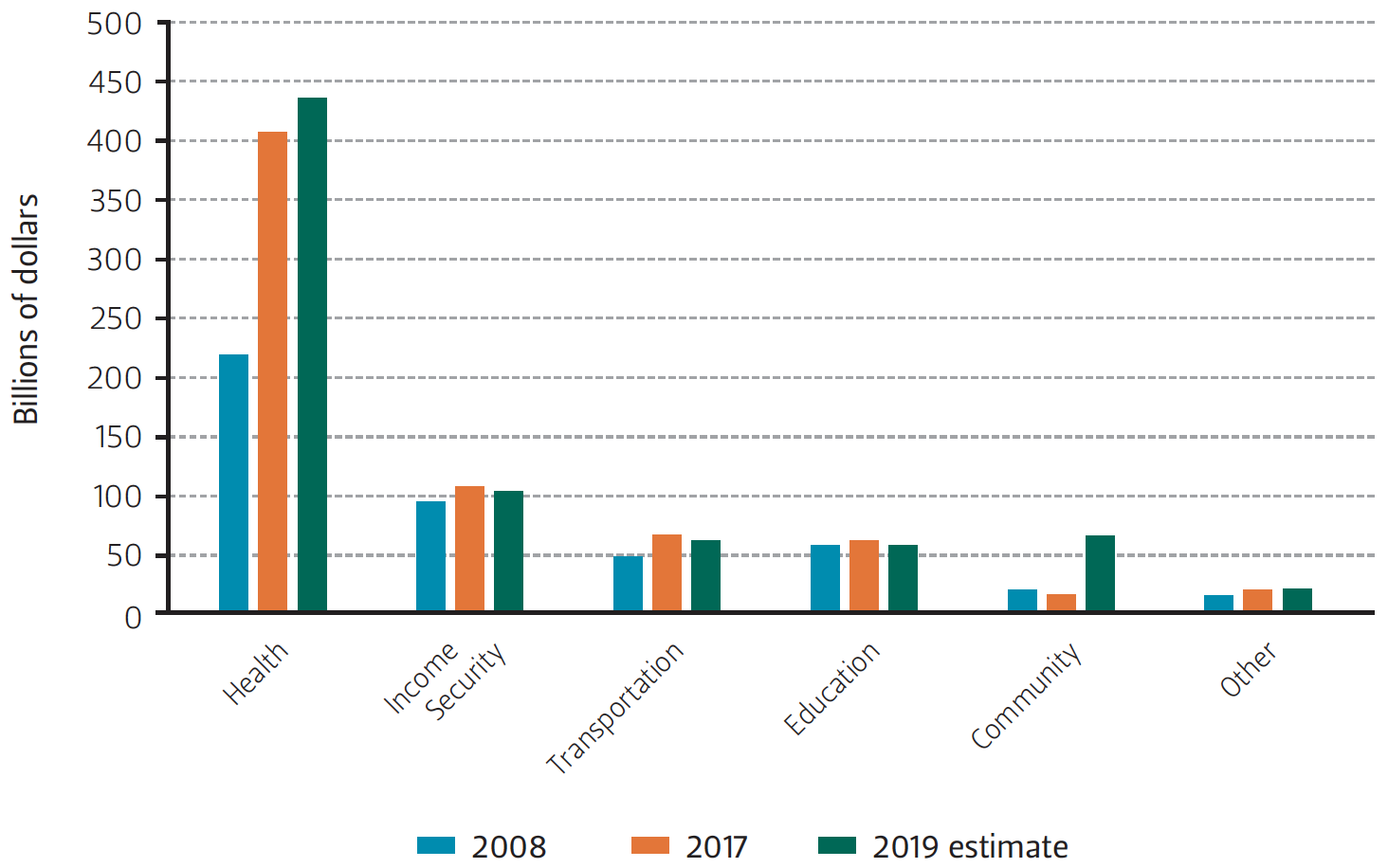

Figure 1 — Outlays for Federal Grants to SAL Governments by Functional Area

https://www.whitehouse.gov/omb/historical-tables/.

Note The full title of the “Education” functional area is “Education, training, employment, and social services,” and the full “Community” functional area is “Community and regional development.”

Although the total number of grants awarded is large, the funds are highly concentrated in several major functional areas. In FY 2018, the top three funding areas accounted for approximately 85% of the total outlay: health ($433 billion, or 60%), income security ($111 billion, or 15%), and transportation ($64 billion, or 9%). Within health, Medicaid expenditures alone were $400 billon, accounting for 55% of federal grants. Figure 1 shows spending by functional area in FY 2008 (the year before the effects of Great Recession-related federal aid kicked in), FY 2017 (the most current audited data available), and FY 2019 (current fiscal year projections).

In addition to the increasing federal control attached to grant awards, state budget officers are concerned about the growing volatility of federal funds, which could pressure cash flow stability at the state level.10 The volatility stems from the nature of the federal budget, because grants for SAL governments come from two types of federal spending: mandatory and discretionary.11 The mandatory program rules, which prescribe funding formulas, benefits, and eligibility requirements, are set in federal laws and remain in effect unless changed. This means Congress does not appropriate a certain amount to these programs each year; instead, when eligibility requirements are met, outlays are made without further congressional approval. In terms of dollar amount, entitlement programs such as Medicaid and the Children’s Health Insurance Program (CHIP) made up 82% of mandatory spending in FY 2016.12 Other mandatory programs include child nutrition programs and the adoption and foster care program, among other items.

In contrast, federal spending for discretionary programs is appropriated annually. The House and Senate appropriations committees review agency funding requests and propose levels of budget authority, which set the amounts to be appropriated for a program or the amount of funds that may legally be spent. In terms of the number and variety of grant programs, there are significantly more types of programs under discretionary grants than mandatory grants. Because funds are limited, the federal budget process requires that competing goals must be balanced, which not only reflects the priorities of Congress but also demonstrates the “power of the purse.”13

The largest discretionary programs include transportation (grants for highways, airports, and mass transit), education (support to improve outcomes for low-income students and students with special needs), housing subsidies for low-income families and seniors, and community development programs.14 Because discretionary grants are subject to annual review and approval, such funds are intrinsically unstable.

In recent years, increased outlays for Medicaid, a categorical grant program funded through mandatory spending, has been the primary driver of increased federal grant awards to SAL governments. To control this spending growth, the Trump administration floated the idea of changing Medicaid to a block grant program,15 which would give states flexibility in how they spend federal dollars and allow them to experiment with their own delivery mechanisms to improve the program’s efficiency. However, critics have said switching to a block grant might lock federal grants at a fixed level, and future increases in funds may not be as easy to obtain or may not keep up with the rapid growth of medical expenses.

Federal Financial Assistance Through Tax Subsidies

A second and less obvious channel through which the federal government provides financial assistance to SAL governments is the tax code. Prior to the TCJA, the Joint Committee on Taxation (JCT) estimated that the SALT deduction cost the federal government $70 billion in FY 2017 and $74 billion in FY 2018. Incorporating the TCJA’s SALT deduction limit, the JCT’s revised results indicate that the cost of the SALT deduction would increase to $101 billion in FY 2017, fall to $37 billion in FY 2018, and further drop to $21 billion in FY 2019.16 The increase in costs for FY 2017 is due to taxpayers claiming deductions prior to the TCJA’s effective date to avoid the $10,000 cap.17 The large reduction in tax expenditures as a result of the new SALT deduction limit, projected to be in the range of $40 to $50 billion per year, is at the center of the recent contentious debate.

IRS data for 2015 shows the nationwide average SALT deduction was $12,471 per return. Statewide averages show that in more than a third of the states (19) plus Washington, D.C., taxpayers claimed over $10,000 in SALT deductions, ranging from $10,221 on average in New Hampshire to $22,169 in New York State. Almost half of Maryland residents’ federal returns (46%) reported SALT deductions, whereas about a quarter (26%) of Ohio residents filed for the SALT deduction. This implies that not only will the cap have different impacts across states, it will also affect residents differently within a state.18

Although there is disagreement as to whether federal grants or tax subsidies are the better way of providing financial assistance to SAL governments, one reason states fight hard to keep the deductibility is because federal grants come with substantial control and uncertainty. In contrast, although the SALT deduction does not put tax revenue directly into state coffers, these tax expenditures come with no strings attached—there is no mandate about qualification, and it is not subject to annual appropriation.

The Pros and Cons of Using the Salt Deduction as a Policy Tool

Supporters of the SALT deduction typically view it as a tool to redistribute resources across different parts of the country, essentially functioning as an equalizer. This deduction helps governments in regions with a lower income tax base sustain spending levels by lowering the net costs to taxpayers. Similarly, because federal taxes do not take into account cost of living differences across states, the higher SAL taxes levied in some states partly reflect the higher costs of providing public services. Therefore, if higher taxes and higher income across different geographic areas indicate differences in costs of living, the SALT deductibility can help offset some of those regional differences.19

Another argument that favors the SALT deduction is the potential for double taxation, because the same income is taxed twice. However, this is not a unanimous position, as some observers claim the taxes are not collected by the same level of government. Instead, because different levels of governments levy taxes to provide distinct sets of services, some experts argue that the rationale for double taxation does not hold. The dispute therefore rests on whether the SALT represents taxpayers’ payments toward local public services and, if so, whether local residents are the only beneficiaries of these services.

On the one hand, some believe that because SAL government services mainly benefit residents of a particular taxing jurisdiction, the SALT reflects payments for these public services.20 The vast majority of state general funds are used to provide services such as elementary and secondary education, health care, higher education, corrections, and transportation, which mostly help SAL residents.21 In addition, local residents live in a particular community because they like the level of public services; thus, the federal government does not have strong reasons to subsidize SAL government spending because this reflects local residents’ choices and preferences.

On the other hand, some believe that even though SALT primarily supports local public services, a significant portion of these services have spillover effects. For example, investment in educational programs can over time reduce crime and increase employment, enhancing earnings in local communities and leading to higher income and thus higher federal income tax payments. Without federal subsidies, SAL governments likely would provide these services at a less-than-optimal level, since not all benefits are recognized directly and immediately by local residents. In practice, it is also hard to segregate benefits that are strictly local from those with spillover effects, or to distinguish the extent to which residents choose to live in a certain area because of the level of local services provided (as opposed to other personal and lifestyle reasons). Thus, the higher the spillover effect of SAL funding, the stronger the rationale for supporting the SALT deduction.

Two related issues result from this discussion. First, some question whether limiting the SALT deductibility would indeed reduce the level of SAL government services. The economic literature provides mixed findings on the magnitude of the impact of SALT deductibility on government services or spending levels.22 Some studies point out that although the intent of the federal subsidy is to encourage SAL governments to provide public services that yield spillover effects, in practice, SAL governments can use these funds in any area and there is no guarantee that the services would have a national benefit. In addition, because the deductibility lowers SAL governments’ costs of providing services, they may even oversupply certain public services.23

The second issue is whether states choose tax-based funding sources based on federal deductibility. If only certain, but not all, SAL taxes are deductible for federal income tax purposes, SAL governments may have incentives to finance public services with the deductible ones because the cost of financing public services is lower for local taxpayers. Research results on this issue are also mixed. One the one hand, several studies found measurable effects of the SALT deductibility on the usage of SAL tax instruments; however, such selectivity does not translate to increased SAL revenue or spending.24 On the other hand, when using post-1986 tax reform data (Tax Reform Act of 1986), which eliminated the sales tax deductibility but maintained the property and income tax deductibility, states did not move away from using sales taxes to fund services or reduce their total spending.

Opponents of the SALT deduction, who support eliminating or curtailing it, claim the deduction is not fair. Because non-itemizers, who tend to be lower income taxpayers, do not get to utilize these deductions, the SALT deduction primarily benefits high-income taxpayers. Federal tax deductibility for SALT therefore reduces the amount of income redistribution and the resulting progressivity of the federal income tax system.25

Another critique is that the SALT deduction contributes to inequality across geographical areas, as the unlimited SALT deduction benefits itemizers in high-tax states over taxpayers in low-tax states. Although the high-tax states argue that limiting the SALT deduction will affect their ability to raise taxes because residents’ burdens are already high, lower tax states argue that without the cap, they would be subsidizing the high-tax, high-spending states; the cap would then force these states to rethink their spending priorities. In cases where it is more efficient or reasonable to finance public services with user charges or service fees, the subsidy provided by the SALT deduction may encourage SAL governments to use tax-based financing instead.

Prior to the TCJA, researchers generally believed that the Pease limitation and the individual alternative minimum tax (AMT) reduced the value of the SALT deduction for claimants. The Pease limitation essentially decreased the value of itemized deductions by up to 20% for high-income taxpayers.26 In addition, the calculation of the AMT, a parallel tax system to the regular income tax calculations, disallows the SALT deduction. Of the items that are deductible under the regular income tax system but not deductible under the AMT, the disallowance of the SALT deduction is a major reason taxpayers are subject to paying the AMT.27 In 2014, among the 4.2 million AMT payers, about 80% would not need to pay the AMT if they could claim the SALT deduction under the AMT system.28 If the AMT is eliminated, the aggregate amount of benefit taxpayers would receive from the SALT deduction would double.29

The TCJA repealed the Pease limitation and substantially relaxed the AMT rules; both had the effect of limiting the value of the SALT deduction prior to the TCJA. Under the pre-TCJA rules, about 5 million taxpayers would have been subject to the AMT in 2018; the TCJA rules bring this total down to 200,000, or 4% of the number of taxpayers who would have been affected by the old rules.30

Although the combined effects of repealing the Pease limitation, relaxing AMT rules, and capping the SALT deduction under the TCJA is unknown, previous studies that focus on the distributional effects of the 2001 tax law change provided some directional guidance.31 One of the simulations shows that if both the SALT deduction and AMT were eliminated (the scenario closest to the TCJA), lower income households (defined as those with taxable income of less than $75,000) would be unaffected because they are not itemizers and not subject to the AMT. The repeal of the AMT translates into tax savings for households with income between $200,000 and $500,000, who previously did not benefit much from the SALT deductibility but now can enjoy tax savings from the elimination of the AMT. Households with high income, i.e., those earning more than $500,000, still face the largest increase in tax liability. Households earning between $75,000 and $200,000 consist of half-winners and half-losers. Because the AMT imposes relatively large taxes on married households and filers with children, eliminating the AMT allows them to enjoy tax cuts comparable to unmarried taxpayers and households without kids. In other words, the repeal of the AMT more than makes up for the loss of SALT deductibility since they already lost the value of SALT deduction prior to the 2017 tax law change.

State Responses

States have been creative in finding ways to circumvent the SALT deduction cap. These workarounds include using charitable contributions, payroll taxes, and pass-through business taxes. The charitable contributions solution is the most widely used strategy, and has thus received the most scrutiny from the Treasury.

New York State, which has the highest average statewide SALT deduction across the U.S., is one of the most outspoken critics of the SALT deduction limit and the most proactive in finding measures to mitigate its impact. It introduced all three measures mentioned above. The state estimated that the $10,000 cap, if implemented without any workaround, would cost its taxpayers $14 billion per year.32 By proposing measures to circumvent the deduction limit, the state can still collect its full pre-TCJA tax revenue and allow taxpayers to reduce their federal tax liability.

Charitable Contribution Workaround

The charitable contribution workaround converts the limited SALT deduction into an unlimited charitable deduction. Because the federal charitable deduction remains unlimited after the TCJA, the basic idea of the charitable contribution workaround is to allow taxpayers to donate to state-established funds, making the donations eligible for the charitable deduction on the donors’ federal income tax returns. For instance, New York created two state charitable funds to support health and educational programs, and taxpayers may receive a state income tax credit of up to 85% of their contributions. New York also allows local governments to establish their own charitable funds to bypass the property tax limit, following New Jersey’s initiative.

New Jersey’s charitable fund bypass is administrated via a state credit against residents’ property taxes. It authorizes municipalities, counties, and school districts to create charitable funds that they can use as a revenue source, essentially allowing local governments to accept property taxes in the form of charitable contributions. These municipalities can then give tax credits of up to 90% to the contributors, who can use such credits to offset their local property taxes and claim deductions on their federal tax returns.33

California proposed its charitable fund workaround early, but amended it in June 2018 to align more closely with existing IRS-approved charitable programs.34 The amended bill allows Californians to donate to the state’s Local Schools and Colleges Voluntary Contribution Fund, which allows taxpayers to contribute to school districts, charter schools, child care centers operated by local educational agencies, and community college districts. In return, donors receive an 85% tax credit for the amount contributed.

Oregon’s approach is a charitable contribution with a twist. Its tax credit program does not provide taxpayers with a pre-specified percentage of tax credits in return for donations to the state’s college tuition grant program. Instead, the state’s $14 million Oregon Opportunity Grant tax credits are auctioned annually. Thus, donors only have a chance at securing a state tax break in return for their donation, not a guaranteed credit. It is modeled after Oregon’s existing Office of Film and Television tax credit auction, which has not been challenged by the IRS.35

Payroll Tax Workaround

The payroll tax workaround converts the limited SALT deduction into an unlimited employer payroll tax deduction. Because employers can claim unlimited payroll tax deductions as business expenses, this program converts a portion of the employee-paid state personal income tax into an elective employer-paid payroll tax with an employee wage credit.36 An example is New York’s Employer Compensation Expense Program, which creates a voluntary payroll tax system that the employers can opt into.

Although practitioners believe this measure is more robust than the charitable contribution approach from a legal perspective, businesses do not favor this workaround due to its administrative and conceptual complexity. In addition, this method does not apply to self-employed workers who are not on employers’ payrolls.

Pass-through Business Tax Workaround

The pass-through business tax workaround converts the limited SALT deduction into an unlimited pass-through business expense deduction. Because SAL taxes paid in connection with conducting a trade or business also are considered business expenses, they are unlimited and deductible on federal income tax returns. By taxing the pass-through business entities directly instead of the owners (and then providing owners credits), this approach essentially swaps the limited taxpayer-level SALT deduction with an unlimited entity-level business expense deduction on federal returns, reducing business owners’ federal income tax liability.

In mid-May 2018, New York issued an unincorporated business tax (UBT) proposal, which would impose a 5% tax on unincorporated taxable income for partnerships, allowing the partners to then claim a credit on their personal income taxes of up to 93% of their UBT. This proposal complements the state’s voluntary payroll tax workaround, because the UBT covers workers not in an employer-employee relationship, including high-earning partners of investment or law firms.

Connecticut calls for a 6.99% entity-level tax on the net income of pass-through businesses (including partnerships, S-corporations, and LLCs that are deemed partnerships for federal income tax purposes) and an offsetting state income tax credit for the entities’ members.37 Such credit offsets 93.01% of the state income tax the owners paid on the pass-through income.

IRS Notice and Proposed Regulations for the Charitable Contributions Workaround

When the charitable funds bypass proposals first emerged in January 2018, Treasury Secretary Steve Mnuchin quickly commented that dressing up such deductions as charitable contributions is a ridiculous idea.38 However, states continued to propose mitigating measures, and in late May, the IRS issued a notice criticizing the charitable contribution technique, stating that the Treasury and the IRS would soon issue proposed regulations to address the deductibility of SALT payments for federal income tax purposes.39 The notice warns against the state initiatives allowing taxpayers to donate to SAL government-controlled charitable entities in exchange for tax credits against their SALT payments.

The notice also reminds taxpayers that, when it comes to charitable contributions, the substance-over-form and charitable intent principles are crucial. Charitable contributions qualify for tax deductions only if the donors have a charitable intent and if the funds are truly for charitable purposes. Federal law has the final say about how payments should be characterized for federal income tax purposes.

The IRS’s action did not stop states from challenging the SALT deduction limit. In July, New York, Connecticut, Maryland, and New Jersey jointly filed a lawsuit claiming that the federal government infringed upon states’ rights guaranteed by the Constitution. The federal government countered that the states’ rights are not impaired, they simply do not agree with federal tax policy. If taxpayers in these states believe their rights are compromised, due process requires these taxpayers first pay the taxes and then sue for refunds.

The Treasury issued proposed regulations in August,40 which state that under the charitable contribution bypass programs established by the states, taxpayers can only receive a federal tax deduction equal to the difference between their charitable donations and the state tax credits they receive. The proposed regulations state that if a taxpayer makes a charitable contribution and receives something valuable in return, the taxpayer can only deduct the net value of the contribution, which is consistent with the “quid pro quo” doctrine.41 Thus, if a taxpayer contributes $10,000 to a state charitable fund and receives a $9,000 credit, he can only claim a $1,000 charitable deduction on his federal income tax return—a much smaller effect than the states planned.42 The proposed regulations remain silent on other workarounds to mitigate the cap.

Individual Responses

Although the lawsuit may take some time to settle, high-income taxpayers and estate planners have designed several individual-level workarounds, including using non-grantor trusts to avoid the limitation.43 Essentially, these ideas bypass the $10,000-per-return limit by spreading the deductions across multiple returns. One such novel planning technique involves moving high-value New York properties into multiple LLCs that are set up in zero income tax states, and transfer these interests to separate trusts. Because these trusts are treated as separate income tax-paying entities, each trust can claim a $10,000 deduction. However, the costs of setting up and administrating the trusts could be high. In addition, when the properties in the LLCs are sold, the homeowner will not be eligible to receive a tax benefit for the sale of a primary residence. For mortgage lending purposes, banks may also prohibit listing LLCs as property owners.

A thorny issue relevant to the Treasury Department’s proposed regulations is that over two-thirds of states have existing programs that provide residents tax breaks for charitable donations that aim to encourage donations rather than to enable tax avoidance.44 Most of them exist for education and public health purposes, including funds for education voucher programs, school choice initiatives, and remote hospitals. Prior to the issuance of the proposed regulations, there were mixed opinions on whether these existing programs contradict with the TCJA and therefore would be forced to shut down. However, Mnuchin clarified that the Treasury appreciates the value of state tax credit programs and believes the federal tax benefits of these existing programs would be unaffected because their intent is not to avoid SALT payments.45

Donating to existing state education and public health programs has become a popular tax planning strategy for many taxpayers who expect to be subject to the SALT deduction cap. For example, in Georgia, a taxpayer in the 37% federal income tax bracket can donate $5,000 to these state programs and get a $5,000 credit on his state income tax return. He can also get a $1,850 benefit on his federal income tax return. Taxpayers have been increasing their donations to these state programs, and some studies show that wealth advisors and tax planners have been encouraging their clients to make contributions to such state initiatives, including private school voucher programs and donations to hospitals. Many of them advertise this as a way of “circumventing” or “mitigating” the impact of the SALT cap triggered by the TCJA.46

Conclusion

One year after the TCJA’s passage, the SALT deduction limit remains one of the most contested provisions of the law. Some even believe this issue cost at least six Republican representatives their re-election bids.47 Although removing the SALT deduction cap would cost the federal government more than $600 billion over the next decade, newly elected Democrats from high tax states have begun discussions on either increasing or removing the cap. The partisan nature of the tax reform and the high level of fiscal deficits mean the limited SALT deductibility would have profound revenue implications, and the adversarial relationship between state and federal governments would intensify.

Although the SALT cap has been interpreted as a political move to harm blue states, or a maneuver simply to finance the TCJA, there is no doubt the federal government provides substantial financial assistance to SAL governments. Because the SALT deduction is administrated through federal tax expenditures, the key economic issue regarding SALT deductibility centers on the magnitude of the spillover effects of SAL spending.

Some of the workarounds may prevail on legal grounds, but whether they make good state tax policies is a separate matter. Key state-level issues on both revenue and expenditures need to be addressed. The growing spending on entitlement and the looming budget shortfalls require not only efficient administration but also a reconsideration of spending priorities.

Endnotes

1. IRS, “Notice 2018-54, Guidance on Certain Payments Made in Exchange for State and Local Tax Credits,” May 23, 2018, http://bit.ly/2EuydDF.

2. IRS, “Treasury, IRS Issue Proposed Regulations on Charitable Contributions and State and Local Tax Credits,” August, 23, 2018, http://bit.ly/2A2pe9S.

3. New York et. al v. Mnuchin et. al, U.S. District Court, Southern District of New York, No. 18-06427, July 17, 2018, https://on.ny.gov/2SUlU7N.

4. Emma Beyer, “Trump Administration Asks Courts to Toss SALT Deduction Cap Case,” Bloomberg BNA, November 5, 2018 (subscription required).

5. For other types of federal financial support, see (1) Federal Support for State and Local Governments Through the Tax Code, before the Senate Committee on Finance, 112th Cong. (2012) (statement of Frank Sammartino, assistant director for tax analysis), http://bit.ly/2UOYjap; and (2) Office of Management and Budget, Budget for the United States Government, FY 2018, Special Topics, February 2018, http://bit.ly/2ECkITk, footnote 1.

6. Office of Budget and Management, Budget for the United States Government, FY 2019, Historical Tables, “Table 12.3, Total Outlays for Grants to State and Local Governments,” February 2018, http://bit.ly/2wKRWtk.

7. Increased outlays based on the American Recovery and Reinvestment Act of 2009 (ARRA).

8. There are four category grant subtypes: project categorical grant, formula categorical grant, formula-project categorical grant, and open-end reimbursement categorical grant. For a detailed discussion, see Robert Jay Dilger, Federal Grant to State and Local Governments: A Historical Perspective on Contemporary Issues (R40638) (Washington, D.C.: Congressional Research Service, May 7, 2018), http://bit.ly/2SZNEbb.

9. Dilger, Federal Grant to State and Local Governments.

10. Katherine Barrett and Richard Greene, “How Much Does a Federal Dollar Cost the States?” The Council of State Governments (blog post), May 2, 2017, http://bit.ly/2UU291R.

11. Description of the federal budget process is beyond the scope of this report. Federal outlays are often divided into three categories: discretionary spending, mandatory spending, and net interest. For a comprehensive discussion, see Grant A. Driessen, The Federal Budget: Overview and Issues for FY2019 and Beyond (R45202) (Washington, D.C.: Congressional Research Service, May 21, 2018), http://bit.ly/2EtmPIg.

12. In FY 2016, mandatory grants awarded to SAL governments totaled $467 billion, and discretionary grants to SAL governments equaled $199 billion.

13. Driessen, The Federal Budget.

14. Iris Lav and Michael Leachman, At Risk: Federal Grants to State and Local Governments (Washington, D.C.: Center on Budget and Policy Priorities, March 13, 2017), http://bit.ly/2UU2bH1.

15. Shefali Luthra, “The Skinny on Block Grants – the Heart of the GOP’s Medicaid Plan,” CNN Money, February 2, 2017, https://cnnmon.ie/2A8bPgt.

16. Joint Committee on Taxation, Estimates of Federal Expenditures for Fiscal Years 2017-2021 (JCX-34-18), May 25, 2018, http://bit.ly/2rHBUhP; and JCT, Estimates of Federal Expenditures for Fiscal Years 2016-2020 (JCX-3-17), January 30, 2017, http://bit.ly/2Cm1bUS.

17. In addition to the SALT deduction, there is the exclusion of interest on public purpose SAL bonds. Prior to the TCJA, the JCT estimated that this program cost the federal government $37 billion in revenue in FY 2017 and $39 billion in FY 2018. After the TCJA, the estimates fell to $36 billion for FY 2017 and $32 billion for FY 2018. These amounts do not include qualified private activity bonds.

18. Phillip Oliff and Brakeyshia Samms, “Cap on the State and Local Tax Deduction Likely to Affect States Beyond New York and California,” Pew Charitable Trust (blog post), April 10, 2018, http://bit.ly/2rHVsCR.

19. Kim Rueben, The Impact of Repealing State and Local Tax Deductibility (Washington, D.C.: Urban Institute, State Tax Notes, August 15, 2005), https://urbn.is/2A4A3s7.

20. Martin Sullivan, “Economic Analysis: Repeal of SALT Deduction More About Politics Than Policy,” Tax Notes (blog post), July 11, 2017, http://bit.ly/2ECTlbH.

21. National Association of State Budget Officers, State Expenditure Report - FY 2016-2018 (Washington, D.C.: National Association of State Budget Officers, November 5, 2018), http://bit.ly/2Ev27b5.

22. See discussions in (1) Edward Gramlich, “The Deductibility of SALT,” National Tax Journal 38, no. 4 (December 1985): 447-465; (2) Harley Duncan and LeAnn Luna, “Lending a Helping Hand: Two Governments Can Work Together,” National Tax Journal 60, no. 3 (September 2007): 663-679; (3) Gilbert Metcalf, “Assessing the Federal Deduction for SALT Payments,” National Tax Journal 64, no. 2 (June 2011): 565-590; and (4) Jared Walczak, The State and Local Tax Deduction: A Primer (Fiscal Fact No. 545) (Washington, D.C.: Tax Foundation, March 2017), http://bit.ly/2BrLBFK.

23. Congressional Budget Office, The Deductibility of State and Local Taxes (Washington, D.C.: CBO, February 20, 2008), http://bit.ly/2ECvsBh.

24. See summaries by (1) Frank Sammartino and Kim Rueben, Revisiting The State and Local Tax Deduction (Washington, D.C.: Tax Policy Center, March 3, 2016), https://tpc.io/2QGqAkU; (2) Sullivan, “Economic Analysis.”

25. See (1) Kirk Stark, “Fiscal Federalism and Tax Progressivity: Should Federal Income Tax Encourage State and Local Redistribution,” State Tax Notes 33, No. 13 (September 2004): 923-942; and (2) Duncan and Luna, “Lending a Helping Hand.”

26. The Pease limitation states that if a taxpayer’s AGI exceeds a certain threshold, his itemized deductions are reduced by 3% for each dollar of his income above that limit. The phase-out is limited to 80% of the deductions claimed.

27. IRS, Topic Number 556 – Alternative Minimum Tax, December 10, 2018, https://www.irs.gov/taxtopics/tc556

28. Sammartino and Rueben, Revisiting The State and Local Tax Deduction.

29. Leonard Burman, Eric Toder, and Christopher Geissler, How Big Are Total Individual Income Tax Expenditures and Who Benefits From Them? (Washington, D.C.: Urban-Brookings Tax Policy Center, December 2008), Discussion Paper No. 31, https://tpc.io/2QIqKZj.

30. Bob Carlson, “What You Need to Know about the New AMT,” Forbes, September 29, 2018, http://bit.ly/2QDDJuZ.

31. The Economic Growth and Tax Reconciliation Relief Act (EGTRRA) of 2001. Simulation results are from Kim Rueben, “The Impact of Repealing State and Local Tax Deductibility,” State Tax Notes, August 15, 2005.

32. New York, Preliminary Report on the Federal Tax Cuts and Jobs Act (New York: State Department of Taxation and Finance, January 2018), https://on.ny.gov/2SWrHJP.

33. Ryan Hutchins, “New Jersey Legislature Passes SALT Workaround,” Politico, April 12, 2018. https://politi.co/2R2SIxZ.

34. S.B. 227: Education finance: Local Schools and Colleges Voluntary Contribution Fund, Ca. Education Code § 42127.81 (2018), http://bit.ly/2GsY4P8.

35. See (1) Paul Jones, “IRS Notice Expected to Slow States’ SALT Workaround,” Tax Notes (blog post), June 5, 2018, http://bit.ly/2SZuGl1; (2) Mike Rogoway, “IRS Targets Oregon, Other States Seeking to Circumvent Tax Deduction Limits,” Oregon Live, May 23, 2018, http://bit.ly/2EtnHww; and (3) Higher Education Coordinating Commission, “College Opportunity Grant Tax Credit Auction,” May 2018, http://bit.ly/2BoY5xy.

36. Cynthia Pederson, States’ Workarounds to the SALT Deduction Limitation, The Tax Advisor, August 1, 2018, http://bit.ly/2R037KY.

37. Amy Hamilton, “Connecticut Finds a SALT Workaround That Would Actually Work,” Tax Analysts, February 26, 2018, http://bit.ly/2GtNNlT.

38. Aubree Eliza Weaver, “Mnuchin: Deducting Property Tax as Charity is ‘Ridiculous,’” Politico, January 11, 2018 https://politi.co/2S4bbHD.

39. IRS, Notice 2018-54, “Guidance on Certain Payments Made in Exchange for State and Local Tax Credits,” May 23, 2018.

40. IRS, “Treasury, IRS Issue Proposed Regulations on Charitable Contributions and State and Local Tax Credits.”

41. The proposed rules include a safe harbor that if states provide credits of less than 15% of the donated amount, taxpayers can deduct the full donation on their federal returns.

42. Laura Davison, “IRS Moves to Block New York, New Jersey Plans to Bypass SALT Cap,” Bloomberg BNA Daily Tax Report, August 24, 2018 (subscription required).

43. Lynnley Browning, “How the Rich Can Dodge Trump’s Property Tax Hike,” Bloomberg News, June 15, 2018. https://bloom.bg/2EvB13t.

44. Joseph Bankman et al, State Responses to Federal Tax Reform: Charitable Tax Credits (Fall Church, Va.: Tax Notes, April 30, 2018), http://bit.ly/2QBMyFC.

45. Department of the Treasury, “Press Release: Treasury Issues Proposed Rule on Charitable Contributions and SALT Credits,” August 23, 2018. http://bit.ly/2Gt0A86.

46. See (1) Richard Rubin, “As Treasury Targets Workarounds to Tax Law, Impact May Extend Beyond High-Tax States,” Wall Street Journal, June 27, 2018, https://on.wsj.com/2Af3I1V; (2) Carl Davis, “The Other SALT Cap Workaround: Accountants Steer Clients Toward Private K-12 Voucher Tax Credits,” Institute on Taxation and Economic Policy (blog post), June 27, 2018, http://bit.ly/2UXOuGW.

47. Laura Davison, “SALT Cap Comes Back to Haunt GOP with Key Tax Writers Losing Their Seats,” Bloomberg, November 7, 2018, https://bloom.bg/2USc0Fq.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.