Kuwait risks becoming the custodian of a vast, stranded asset if it cannot align its production pace with the closing window of global oil demand.

Abstract

At current rates of production, Kuwait’s proven oil reserves could produce for 103 years. This unusually long depletion horizon leaves Kuwait exposed to shifts in global oil demand. Despite holding 6% of global oil reserves and among the world’s lowest production costs, in recent years Kuwait has seen production slip below its typical output of 3 million barrels per day (m b/d). The U.S., with oil reserves two-thirds the size of Kuwait’s, produces more than seven times as much oil and natural gas liquids, 20m b/d versus Kuwait’s 2.7m b/d. This means that Kuwait risks seeing a significant portion of its below-ground resources losing value or even becoming stranded if the world shifts away from fossil fuels. However, other scenarios are possible. If climate action creates competitive preferences for lower upstream carbon emissions from oil production, Kuwait could benefit by dint of its low-emissions drilling and output. At the time of writing, Kuwait’s political landscape has shifted in a way that provides an opportunity for accelerating the government’s oil monetization and depletion strategy in ways that could reduce risks of stranded reserves. Kuwait is now pursuing plans to increase production to 3.2 million barrels per day by 2030, aiming to reach 4 million by 2035.[1]

Introduction

Kuwait is a longstanding partner of the U.S. in the Persian Gulf and a major oil producer with ambitions to increase production by the end of the decade. Recent political changes have removed obstacles to economic reform and diversification that for decades had held back development in Kuwait. In response to the broader challenges of the energy transition and rising global uncertainty, in May 2024 Kuwait’s leader, Emir Sheikh Mishal al-Ahmad Al Sabah, suspended Kuwait’s National Assembly and key articles of the constitution for a period of up to four years. This political reset has created space for much-needed economic reforms and has placed pressure on the executive branch of government to deliver in the absence of a legislative body. This pressure is most acute in the oil sector, where aging infrastructure and the need to attract foreign investment in the most economically oil-dependent country in the Gulf have proven politically sensitive.

This report examines the energy landscape in Kuwait and potential policy options for international collaboration and investment in the oil and gas sector. The findings are based on a Middle East Energy Roundtable workshop hosted by the Baker Institute in May 2025.[2]

Background and Political Context to Kuwait’s Energy Sector

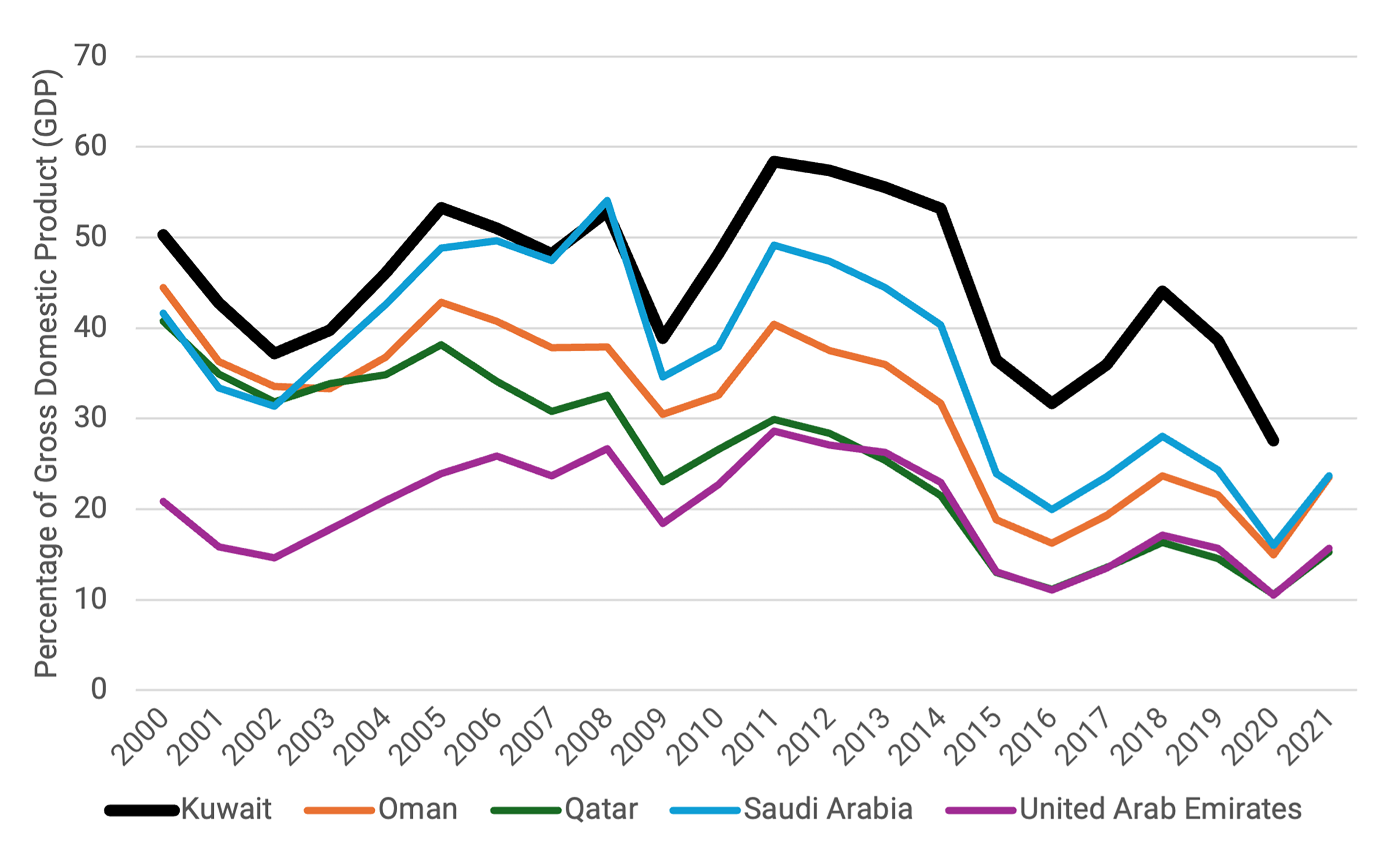

Oil export sales typically account for roughly 90% of Kuwait’s government revenues and total exports.[3] In 2024 oil rents were 43% of total gross domestic product (GDP).[4] These figures mean that Kuwait remains heavily reliant on oil and is one of the least diversified economies in a region of major oil and gas producing states (Figure 1). Article 21 of the 1962 Constitution prohibits foreign ownership of natural resources and there has been little foreign investment in the sector since its nationalization in the 1970s, while Article 152 places restrictions on the granting of concessions for the exploitation of natural resources.[5] Following the liberation from Iraqi occupation in 1991, five international oil companies (IOCs) — BP, Chevron, Exxon, Shell, and Total — worked under technical service agreements to assist Kuwait in restoring production capacity. However, an attempt in the late-1990s and early 2000s to involve IOCs in developing four northern oilfields — known as “Project Kuwait” — ran into political opposition and was shelved indefinitely in 2005.[6]

Figure 1 — Oil Rent as a Percentage of GDP

Note: Kuwait’s economy has consistently been more dependent on oil rents than those of its neighbors.

The fate of Project Kuwait illustrated the challenges facing officials in a setting where any foreign involvement in any aspect of the domestic energy sector risked becoming a flashpoint for political contestation, a dynamic that set Kuwait apart from the other Gulf States.[7] The National Assembly, comprising 50 elected members of parliament (MPs), long functioned as an effective brake on policy implementation as MPs frequently subjected ministers to hostile questioning over the award of public contracts or inquired into the tendering process. Two high-profile examples — the December 2008 cancellation of a $17.4 billion joint venture between Dow Chemicals and Petrochemicals Industries Company, a subsidiary of the Kuwait Petroleum Corporation, and the March 2009 cancellation of plans to construct a new refinery at Al-Zour — damaged Kuwait’s credibility among international investors. An extremely high turnover of oil ministers added to the churn in the sector and the difficulty of planning and implementing strategy.[8]

Two Decades of Political Deadlock

- Systemic Instability: Between 2006 and 2024, deteriorating relations between the government and parliament led to the National Assembly being dissolved 13 times, necessitating 11 different elections.

- Failed Cycles: Only one parliament (2016–20) lasted its full four-year term, while two elections were annulled by the Constitutional Court (2012 and 2023).

- Total Gridlock: Cooperation between the legislative and executive branches effectively collapsed after 2021, culminating in three dissolutions in less than two years (June 2022–February 2024).[9]

- Course Correction: Kuwait was becoming ungovernable due to the worsening stalemate.[10] In June 2022, then-Crown Prince Mishal urged Kuwaitis to “correct the course of national participation so that we do not return to what we were before, because this return will not be in the interests of the country and the citizens.”[11]

On May 10, 2024, the Emir suspended the National Assembly and seven articles of the constitution for up to four years. This was the third interruption of parliamentary activity in modern Kuwaiti history after earlier suspensions from 1976 to 1981 and between 1986 and 1992.[12]

This political reset created a window of opportunity for executive-led action in the energy sector as well as in the broader economy. Of special note, in March 2025 the Cabinet approved a new Financing and Liquidity Law that enabled the government to issue sovereign bonds for the first time since 2017. Known as the “public debt law,” it had for years been blocked by opposition from members of the National Assembly, hampering the state’s ability to keep up with the pace of development in neighboring states in the Gulf.[13] With its approval, Kuwait is authorized to raise up to US$97 billion over 50 years and make wider use of financial instruments to secure funding and manage debt and liquidity.[14]

Freed from legislative gridlock, Kuwait Petroleum Corporation (KPC) is advancing a new strategy: substantial upgrades in upstream capacity, new offshore exploration, and an aggressive foreign investment push. This comes against the backdrop of uncertainty over global oil demand and prices, rising reliance on imports of liquefied natural gas (LNG), and growing international climate scrutiny. With a reserves-to-production ratio that exceeds a century, Kuwait’s traditional oil strategy prioritized reserve preservation. As substitute fuels and energy sources begin to compete with oil, Kuwait’s cautious monetization strategy may be misaligned with the priority of diversifying the most oil-dependent economy in the Gulf. Ramping up output, as KPC plans, fits with this assessment.[15]

The remainder of this report features sections which examine Kuwait’s oil sector and investment profile, uncertainties around long oil depletion horizons mitigated by the country’s carbon competitiveness, the current status of natural gas in Kuwait, and the role of domestic politics in the energy sector.

Kuwait’s Oil Sector and Investment Profile

Kuwait is one of the most oil-rich countries in the world. It has an estimated 101.5 billion barrels of proven oil reserves, making it the No. 7 reserves holder, ahead of No. 8 UAE and behind No. 6 Russia. But despite Kuwait having some of the world’s most accessible oil reserves, it was the world’s 10th largest producer in 2024, behind countries such as Brazil, UAE, China, Iran and Canada.[16] Kuwait’s reserves are concentrated in massive fields that sustain decades of production with minimal lifting energy. Consequently its total production costs — lifting costs plus capital expenditures — are among the world’s lowest at just $5–$7 per barrel, a fraction of the global average of $25–$45 and far below the $35–$60 breakevens in the U.S. and Canada.[17]

As mentioned, at current rates of production, Kuwait’s proven reserves could sustain oil production at its current rate for another 10 decades — without new discoveries — which is double the global reserves-to-production ratio of 53.5 years.[18] The U.S., with oil reserves two-thirds the size of Kuwait’s, produces more than seven times as much oil and natural gas liquids, 20m b/d versus Kuwait’s 2.7m b/d.[19] These statistics illustrate Kuwait’s historically conservative approach to its oil depletion strategy, even compared to neighboring producers in the Persian Gulf.[20]

Operating the sector is KPC, a state-owned company that oversees all upstream, midstream, and downstream operations through its eight subsidiaries, the so-called “K-companies.”[21] The most important is the Kuwait Oil Company (KOC), responsible for oil and gas exploration and production, including operating Kuwait’s dominant asset, the supergiant Greater Burgan Field.[22] With some 70 billion barrels of original oil in place (OOIP), Burgan is the world’s second-largest conventional oilfield, after Ghawar in Saudi Arabia.[23] Burgan has upheld Kuwait’s economy for more than 80 years and has been central to Kuwaiti oil production since its discovery in 1938.[24] After a brief interruption during World War II, large-scale exports restarted in 1946 and continue in the present day.[25] Burgan’s output peaked at 1.7m b/d in 2018 and was reported to be under 1.4m b/d in 2021.[26]

Expanding Offshore Frontiers

After eight decades of strictly onshore production, the Kuwait Oil Company (KOC) has recently secured three major offshore discoveries that transform the country’s resource outlook:

- Al Nokhatha Field (July 2024): This large offshore discovery is estimated at the equivalent of 3.2 billion barrels of light oil and associated gas.[27]

- Al Jlaiaa Field (January 2025): A second major find yielding about 800 million barrels of oil and 600 billion cubic feet (Bcf) of gas.[28]

- Jazah Field (October 2025): A landmark gas discovery containing up to 1 trillion cubic feet (Tcf) of gas and 120 million barrels of condensate crude oil.[29]

These finds have significantly expanded Kuwait’s resource base and show that there is still major growth potential beyond the older onshore fields. Following a 100% success rate during the first phase of offshore exploration, which yielded the three major discoveries, Kuwait is moving into a second phase of development involving the drilling of 18 additional offshore wells.[30] The focus on expanding offshore development requires significant levels of new investment, new drilling methods, and stronger partnerships with international companies that have a long history of offshore development. As noted earlier, because Kuwait maintains that foreign companies cannot own natural resources, this has stymied efforts to involve international partners in the past.

To support these investments, Kuwait is preparing new types of contracts that allow IOCs to work on upstream projects in line with constitutional restrictions, but which offer more attractive terms than the current Enhanced Technical Services Agreements (ETSAs). The new terms would still not grant IOCs legal title to natural resources but instead offer improved incentives and financial returns based on project performance.[31] Kuwaiti officials believe improved terms can attract foreign capital and technology to boost recovery rates in existing fields and develop new production offshore, all of which is needed to reach the 4m b/d goal by 2035.[32]

Kuwait has also invested in both domestic and international refining and petrochemical projects. KPC co-owns refineries in Europe, Vietnam, and Oman, which gives Kuwait secure markets for its crude oil, helping to stabilize revenues and long-term planning amid fluctuating global demand. KPC also owns a network of gasoline stations operating under the Q8 brand, based in London.[33]

Uncertainties Around Long Oil Depletion Horizons

Struggles to Increase Production Capacity

Kuwait has for years voiced a desire to increase production capacity but has yet to achieve those ambitions. Nearly two decades ago, for instance, Kuwait set a goal to achieve a production capacity of 4m b/d by 2020, but political obstacles meant the target went unrealized.[34] In 2025, Kuwait was meeting its OPEC allocation of 2.5m b/d, well below its declared production capacity of 3m b/d.[35] While all four major regional producers were restricted by OPEC quotas, Kuwait’s output remained significantly lower than those of the UAE (4m b/d), Iraq (4.4m b/d), and Saudi Arabia’s 10.6m b/d.[36]

In prior decades, Kuwait also struggled to add production. It took Kuwait nearly 25 years to increase its production by 700,000 barrels per day (see Figure 2). In contrast, the Kuwaiti oil sector’s earlier recovery from the Iraqi occupation in 1990–91 was far swifter, with Kuwait making its first postwar oil export in July 1991 — less than a year after the invasion — and output returned to pre-1990 levels in 1993.[37] Notably, Iraq was able to increase its production by over 2.3m b/d in 10 years after the second Iraq war (Figure 2). Iraq relies heavily on IOCs to extract crude oil, whereas Kuwait is one of the few countries that remains closed to private sector investment in upstream oil production, following nationalization in 1975.[38]

Figure 2 — Oil Production Since 2000

Note: Iraq and the UAE have widened the output gap with Kuwait, where production has stagnated over the past decade.

Impact of Climate Change

Climate change has created new incentives to find oil substitutes, adding to the pressure on Kuwait. These incentives remain relevant in the mid-2020s even as climate action pressure has receded, given the emerging consensus that steep reductions in global fossil fuel consumption in the next decade or so are difficult and probably unlikely. Indeed, Kuwaiti officials have pointed to this consensus and suggested demand for KPC’s oil is likely to outlast that of competitors, due to cost and carbon advantages.[39] Even so, weakness in global oil demand growth is being exacerbated by the emergence of new substitutes for oil, such as battery-electric vehicles, which are beginning to erode oil’s longstanding monopoly as the sole fuel for transportation.

In addition, climate pressure has — paradoxically — incentivized development of new sources of oil, including sources outside of OPEC+ countries, as national governments seek to monetize reserves in light of long-term risks to oil demand. These factors have created greater uncertainty around long-term global oil requirements and prices, leaving governments overseeing century-plus reserves-to-production ratios — like Kuwait –worrying over the potential for declining oil rents and reserves values or even stranded reserves.[40]

In this light, Kuwait’s conservative depletion strategy could pose challenges. As oil demand plateaus and declines, putting downward pressure on oil prices, Kuwait’s export revenues could decline. Recent forecasts have pushed back the potential date for reaching peak global demand and the International Energy Agency’s 2025 World Energy Outlook includes a scenario that shows world oil consumption peaking around 2030 as well as a business as usual scenario that depicts oil demand drifting upward until 2050, when it reaches 113m b/d — oil demand was just under 102m b/d in 2024.[41] Regardless, policymaking assumptions appear to signal the possibility that oil will play a reduced role in petrostate budgets whether or not demand actually peaks, due to expectations of lackluster demand and copious supplies. Cautious views of future oil revenues appear to be encouraging ongoing petrostate economic diversifications now unfolding. In Kuwait, where oil revenue makes up more than 90% of total income, risks around the future of oil demand can feel existential.[42]

Despite its previously conservative approach, Kuwait has expressed interest in increasing oil production levels, with plans to increase production up to 3.2 b/d in the next five years and up to 4 million by 2035. KPC is also anticipating an increase in global demand for Gulf oil in the coming decades, based on several key factors, including resource availability and the region having the lowest-cost barrels in the world, with marginal oil barrel costs between $5–7.[43] Such cost advantages will ensure that Kuwaiti oil remains competitive against higher-cost producers even if global demand declines or prices weaken over an extended time-horizon, likely after the 2030s and possibly much farther toward mid-century.

Carbon Competitiveness

A mitigating factor is Kuwait’s low upstream carbon emissions. If carbon competitiveness emerges as a differentiating factor among grades of crude oil, with future refining slates based on cleaner production processes, Kuwait could plausibly gain a marketing advantage and, eventually, a potential price premium.[44]

Regardless of the extraction method or crude grade, the combustion of a single barrel averages 434 kg of CO2 per barrel. However, the emissions generated during extraction vary significantly by geography:

- Top Global Performers: Norway and the UAE lead with the lowest carbon-intensity at or near 7 kilograms of CO2 emitted per barrel produced.[45]

- Kuwait: Ranks among the global leaders at approximately 8.5 kg of CO2 per barrel emissions.[46]

- Saudi Arabia: Maintains a highly efficient profile at around 10 kg of CO2 per barrel.[47]

- North America (Permian Basin): Despite mitigation efforts, emissions remain significantly higher at approximately 22 kg of CO2 emissions per barrel.[48]

- High-Intensity Producers: Production emissions in Canada, Venezuela, and Algeria are much higher than those mentioned above.[49]

In Norway, emissions reductions have come through technological investment in methane mitigation and carbon capture and reinjection. In the Gulf, the carbon competitiveness is generally due to favorable geological conditions that allow oil to be produced without consuming much energy. KPC, like other major oil firms, aims to augment its advantage by pursuing a 2050 net-zero carbon strategy, which would — in theory — eliminate the company’s emissions from operations.[50] Of course, KPC customers would still be emitting carbon when combusting oil products made with Kuwaiti crude.

Natural Gas in Kuwait

Kuwait is the largest importer of LNG in the Middle East and Africa, despite its position in the top 20 global holders of natural gas reserves. As of 2022, Kuwait held around 63 Tcf of proved natural gas reserves, just under 1% of the global total. Around 70% of Kuwait’s natural gas production is associated with the country’s oil production and thus tied to output levels and OPEC quotas.[51] Oil and natural gas account for the majority of Kuwait’s primary energy consumption, with the share of natural gas increasing from 32% in 2009 to 65% in 2021 — partly based on imports of LNG which began in 2008 — allowing natural gas to begin replacing oil in the industrial and electric power sectors.[52] The gas-for-oil switching has freed up oil for export, where it is sold at world market prices rather than low, government-fixed domestic prices.

Kuwait’s natural gas consumption increased by 52% between 2014 and 2022, as the natural gas-fired Az Zour power plant came onstream.[53] Domestic power plants and water desalination plants, as well as the petrochemical industry and the oil sector, all rely heavily on natural gas. Despite rising natural gas production after 2010, domestic demand for gas has far outpaced production levels, leading Kuwait to become the leading importer of LNG within the Middle East and Africa (Table 1).[54]

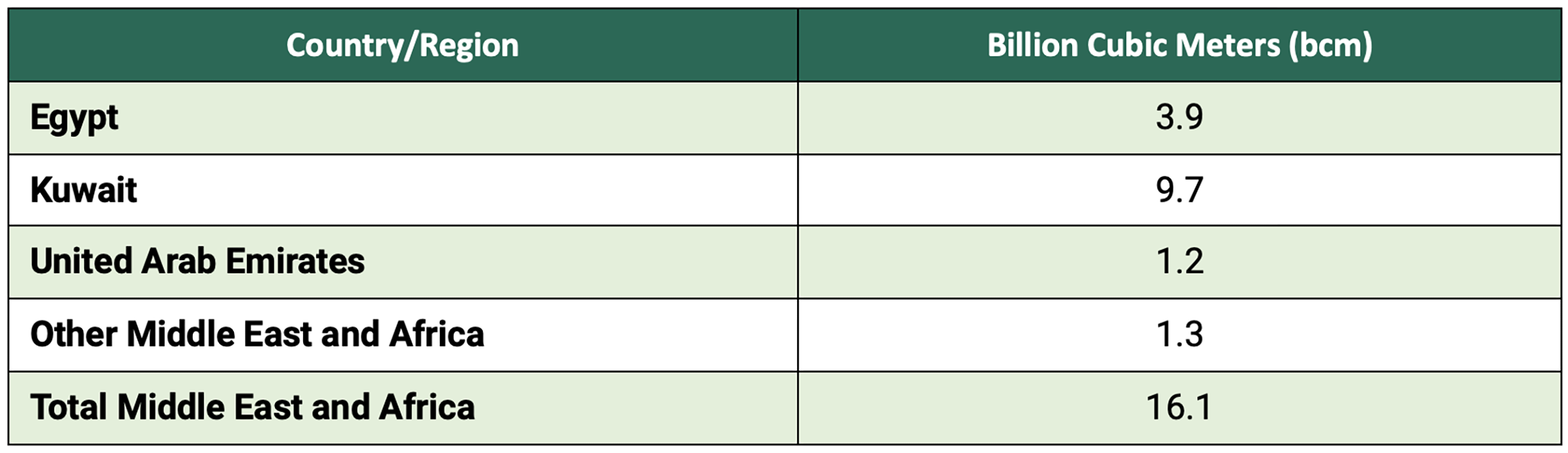

Table 1 — LNG Imports in the Middle East and Africa 2024

To meet the shortfall in gas, since 2020 KPC has signed three 15-year agreements to import LNG from Qatar that amount to almost 7 million metric tons per year.[55] In addition, KPC has purchased LNG cargoes on the spot market to meet surging summer demands for power.[56] If realized, KPC’s upstream expansion plans would go a long way toward mitigating the gas shortage by increasing production of associated gas.

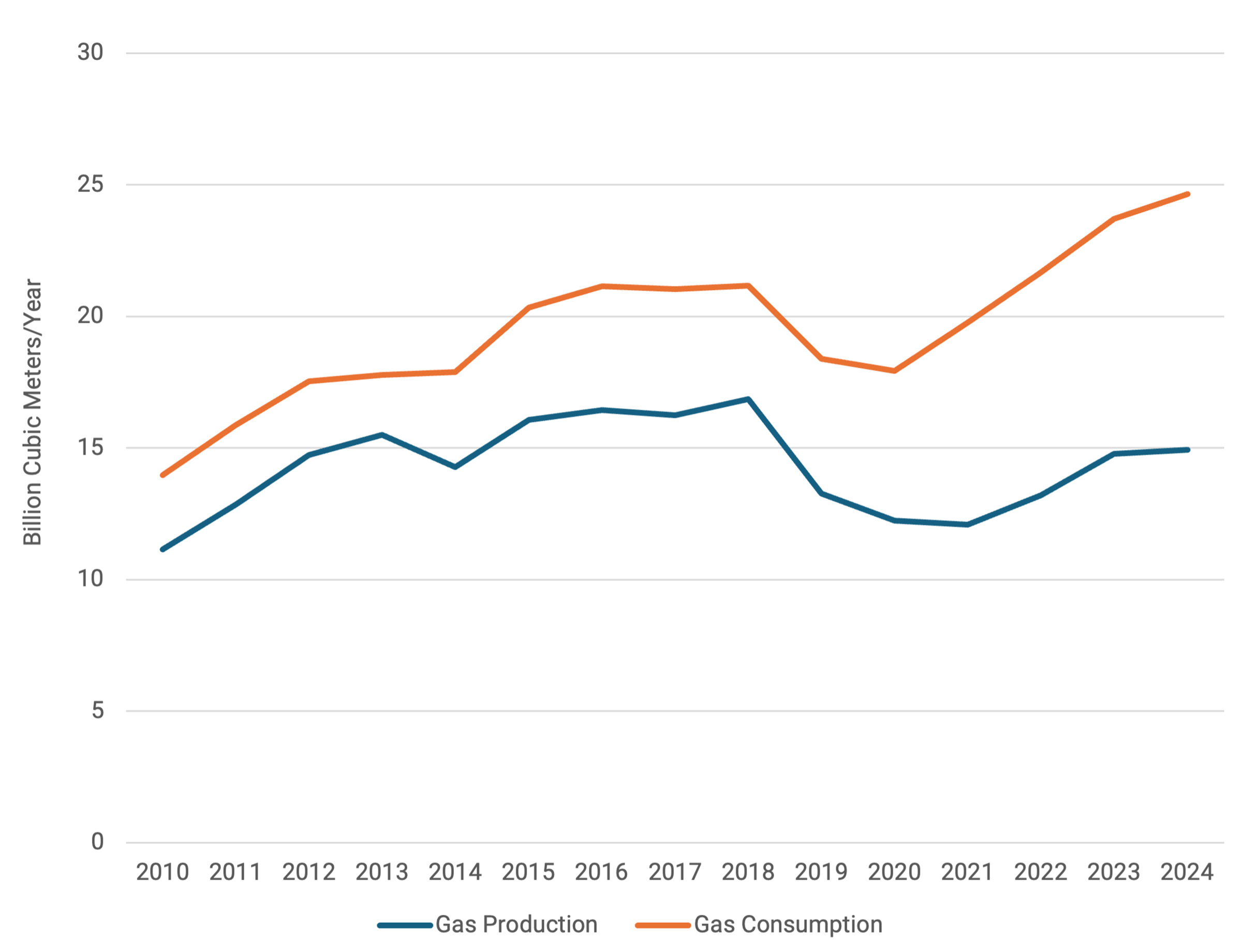

Figure 3 — Kuwaiti Gas Production Versus Consumption Since 2010

Note: Kuwaiti gas demand has outpaced domestic supply since 2008, when imported LNG began to fill the gap.

Kuwait consumed 2.4 Bcf/day in 2024, with around 40% of this demand met through LNG imports and 35% supplied through associated gas production.[57] The remainder was domestic non-associated gas. Natural gas production in Kuwait fell from 691 Bcf in 2019 to 664 Bcf in 2021, reflecting the COVID-19 pandemic-era oil production cuts as mandated by OPEC+. Production levels rose back to their 2019 levels in 2022 when oil production and, therefore, associated gas production, increased.[58]

Because of its reliance on associated gas, Kuwait is vulnerable to OPEC+ crude output reductions, which directly affect gas availability. For example, steep oil production cuts in the early 1980s severely reduced the output of associated gas and required Kuwait to import LNG as a temporary response in 1984.[59] To reduce this risk, Kuwait has been investing in non-associated gas through offshore exploration and onshore projects.[60] Motivated to increase its natural gas production by developing natural gas fields separate from its crude oil production, Kuwait expanded its Jurassic natural gas field production in its northern regions by 110 Bcf in 2024.[61]

As of 2025, production of non-associated gas (serving roughly 25% of Kuwaiti demand), is mainly focused on the Jurassic gas field in northern Kuwait. Currently producing just under 700 million cubic feet per day (MMcf/d) these fields are projected to reach 720 MMcf/d in 2026 and eventually peak at 900 MMcf/d.[62] Exploration in Kuwait has turned up more non-associated gas than anticipated, which could mitigate the reliance on imported LNG.[63] However, seasonal fluctuations in gas-dominated power demand have arisen from record summer temperatures. Power demand growth has brought outages from shortages of generating capacity and aging infrastructure. As Al-Sayegh et al. observe, Kuwait requires a fundamental restructuring of its subsidized electricity pricing, which has distorted domestic demand and placed an increasing strain on natural gas supplies.[64]

Domestic Politics and the Energy Sector

The suspension of the National Assembly for up to four years gives a window of opportunity for the authorities in Kuwait to push through reforms. Without the customary pushback from MPs, the government can now prioritize expanding Kuwait’s oil and gas production and reforming the electricity and water subsidy frameworks, as well as the unhindered allocation of capital toward economic diversification. This window will last through 2028 unless the emir recalls parliament within the four-year timeframe or extends the suspension further.

Any changes to the operational landscape in the oil sector that address demand, streamline efficiency, and improve the investment climate for international companies would be significant, given the resistance to change occasioned by the populist character of Kuwaiti politics and the past tendency of MPs to protect the rentier benefits that their constituents receive.[65]

Reforms Are Underway

Structural and fiscal reforms that had been held back by the years of political standoff — such as the new debt law — are underway and there are signs that projects in the energy sector have started to move forward, such as the KNPC-KIPIC merger.[66] Plans by KPC to monetize its pipeline assets have also been developed as a means to unlock capital for long-term investment, and to bring in foreign investment while maintaining Kuwaiti ownership of the energy infrastructure.[67] Such a move would bring KPC into line with other national oil companies in the Gulf, such as Saudi Aramco, the Abu Dhabi National Oil Company (ADNOC), and OQ in Oman which have moved at pace to extract greater value from existing resources. Partial privatization or leasing existing infrastructure to international investors would create new revenue streams without adding to the government’s balance sheet. But if midstream costs rise, wellhead revenues would fall because Kuwait cannot raise export prices in the globally competitive international crude market.[68] The greater room for maneuver also provides an opportunity for KPC to rationalize initiatives across its subsidiaries and prioritize strategic projects, such as petrochemicals, if greater volumes of gas production duly come onstream.[69]

Offshore Development Needs

After decades of onshore focus, KOC may need international technical expertise in offshore development to bring the newly-discovered fields into production. While the country’s constitution prevents any direct foreign ownership of reserves, KPC is adopting a model that will incentivize companies to invest in Kuwait through joint ventures and technical service agreements. For instance, a new model is currently being implemented that will enable IOCs to benefit economically without having a legal title to Kuwaiti oil. Partnerships with IOCs and service companies in the oil and gas sector may encounter less resistance with parliament suspended. If the process unfolds successfully, Kuwait could begin to overcome the hostile climate for foreign investment that has left the onetime Gulf front-runner lagging behind its neighbors. Progress on addressing bureaucratic obstacles and bottlenecks, such as subsidy reform and demand management, may also rebuild investor confidence in Kuwait, but plans to privatize the electricity sector have been slow and subsidies remain acutely sensitive.[70]

Securing Long-Term Projects

Since privatization and subsidy reform have long been hot button issues in Kuwait, investors will seek assurance from the leadership that decisions taken during the current era of executive authority will not be vulnerable to being undone or reversed if parliamentary politics resumes. The long time-horizons for developing major energy and infrastructure projects, and making investment decisions, means that practitioners and analysts will be assessing both the scale of changes unveiled post-May 2024 and the likely decision-making landscape after 2028 as well. As the end of the suspension of the National Assembly draws closer, short- and long-term assessments of political and economic prospects will be significant factors in determining how projects with expected completion dates into the 2030s will unfold.

Conclusion

Kuwait has a strategic window to modernize policies that have historically constrained investment in the country’s enormous and low-cost oil and gas reserves. Stagnant production levels have extended the lifespan of Kuwait’s oil reserves beyond a century — a timeframe that risks stranded assets as governments and firms worldwide are actively seeking oil substitutes. While the 2024 suspension of parliament facilitates executive action on energy sector reform, unilateral governance carries inherent risks. Bypassing traditional legislative oversight may sow the seeds for future political conflict or legal challenges, particularly once a new National Assembly is seated. After decades of policymaking inertia, the adjustments required to modernize Kuwait’s energy sector have shifted from routine updates to urgent structural necessities. The subsidy framework — which incentivizes overconsumption of electricity — is a primary case in point. Reform is needed not only to temper demand growth but also to spur investment in new capacity, both of which are currently discouraged by state-administered underpricing.

Policymakers should focus on the mounting risks to Kuwait’s oil-dominated rentier governance model. Whether driven by declining domestic production due to chronic domestic underinvestment or a erosion of global oil prices, the era of guaranteed oil rents is approaching an inflection point. Safeguarding Kuwait’s future requires a full reevaluation of oil reserve stewardship, alongside the development of a roadmap and constructive policies for economic diversification. Kuwait risks becoming the custodian of a vast, stranded asset if it cannot align its production pace with the closing window of global oil demand.

Notes

[1] Shaikh Nawaf S. Al Sabah, “Baker Institute Joint Middle East Energy Roundtable Role of Energy Transition in Economic Diversification in the State of Kuwait,” KPC, December 8, 2025, https://www.kpc.com.kw/PublicStatementsDetails?content-id=305.

[2] The Middle East Energy Roundtable (MEER) convenes workshops with a broad range of participants and discussion topics (“Middle East Energy Roundtable,” Rice University’s Baker Institute for Public Policy, https://www.bakerinstitute.org/middle-east-energy-roundtable).

[3] Woroud Aldossari, “Moving Beyond Oil: Kuwait’s Vital Economic Shift,” London School of Economics, December 4, 2024, https://blogs.lse.ac.uk/mec/2024/12/04/moving-beyond-oil-kuwaits-vital-economic-shift/.

[4] Oil rents are extraordinary profits, typically defined as the profit left over after deducting costs of oil production and a reasonable return on investment. Nadim Kawach, “Kuwait’s 2024 GDP Falls $5bn Due to Oil Price Drop,” Arabian Gulf Business Insight, May 6, 2025, https://www.agbi.com/economy/2025/05/kuwaits-2024-gdp-falls-5bn-due-to-oil-price-drop/.

[5] “Kuwait 1962 (Reinst. 1992),” The Constitute Project, https://www.constituteproject.org/constitution/Kuwait_1992.

[6] “Kuwait: Oil Initiative Runs into Parliamentary Sands,” Oxford Analytica Daily Brief, November 8, 2000; “Kuwait: Politics Dog ‘Project Kuwait’,” Oxford Analytica Daily Brief, October 9, 2023; and “Kuwait: Oil Revenues Underpin Economic Reform,” Oxford Analytica Daily Brief, November 22, 2005.

[7] Paul Stevens, “Kuwait Petroleum Corporation (KPC): An Enterprise in Gridlock,” in Oil and Governance: State-Owned Enterprises and the World Energy Supply, eds. David G. Victor et al. (Cambridge University Press, 2012), 363–4, https://www.cambridge.org/us/universitypress/subjects/politics-international-relations/political-economy/oil-and-governance-state-owned-enterprises-and-world-energy-supply?format=HB&isbn=9781107004429; Courtney Freer, The Resilience of Parliamentary Politics in Kuwait: Rentierism, Ideology, and Mobilization (Oxford University Press, 2024), 183–4, https://global.oup.com/academic/product/the-resilience-of-parliamentary-politics-in-kuwait-9780197570364?cc=us&lang=en&.

[8] Michael Herb, The Wages of Oil: Parliaments and Economic Development in Kuwait and the UAE (Cornell University Press, 2014), 170–3, https://www.cornellpress.cornell.edu/book/9781501725173/the-wages-of-oil/#bookTabs=1.

[9] Kristian Coates Ulrichsen, “Parliamentary Elections Are Unlikely to Alter Kuwait’s Political Landscape,” Arab Center Washington DC, October 18, 2022, https://arabcenterdc.org/resource/parliamentary-elections-are-unlikely-to-alter-kuwaits-political-landscape/.

[10] Sean L. Yom, “Will Kuwait’s Next Parliament Be Its Last?,” Journal of Democracy, March 2024, https://www.journalofdemocracy.org/online-exclusive/will-kuwaits-next-parliament-be-its-last/.

[11] “HH the Crown Prince: We Have Decided to Dissolve the National Assembly,” The Times Kuwait, June 22, 2022, https://timeskuwait.com/news/hh-the-crown-prince-we-have-decided-to-dissolve-the-national-assembly/.

[12] Vivian Nereim, “Kuwaiti Emir Suspends Parliament, Citing Political Tumult,” New York Times, May 10, 2024, https://www.nytimes.com/2024/05/10/world/middleeast/kuwait-emir-parliament-suspension.html.

[13] “Kuwait Approves New Debt Law and Trims Pensions, in Signs of Long-Awaited Reform Drive,” Gulf States Newsletter, March 28, 2025, https://www.gsn-online.com/news-centre/article/kuwait-approves-debt-law-and-trims-pensions-signs-long-awaited.

[14] “Kuwait Sets KD30bn Debt Cap with 50-Year Borrowing Plan,” Kuwait Times, March 26, 2025, https://kuwaittimes.com/article/25921/kuwait/other-news/kuwait-sets-kd-30bn-debt-cap-with-50-year-borrowing-plan/; Mohammed Sergie, “Kuwait’s Economic Overhaul Fuels Optimism for Growth,” Semafor, March 28, 2025, https://www.semafor.com/article/03/28/2025/kuwaits-economic-overhaul-fuels-optimism-for-growth.

[15] “Kuwait’s KPC Plans $9-10bn Annual Upstream Capex,” MEES 68, no. 50 (2025), http://archives.mees.com/issues/2140/articles/65197.

[16] Energy Institute (EI), Statistical Review of World Energy 2025, https://www.energyinst.org/statistical-review.

[17] MEER workshop discussion. Additional data compiled from Rystad Energy and Enverus Intelligence Research (“Marginal Cost of U.S. Shale to Move from $70 to $95 WTI by Mid-2030s,” Enverus, September 23, 2025; https://www.enverus.com/newsroom/marginal-cost-of-u-s-shale-to-move-from-70-to-95-wti-by-mid-2030s/).

[18] BP, Statistical Review of World Energy 2021, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf, 16.

[19] Statistical Review of World Energy 2025.

[20] Only sanctions-constrained Iran has a longer reserves-to-production ratio (140 years) than Kuwait’s 103 years. Saudi Arabia’s is 74, UAE’s is 73, Qatar’s is 38, Oman’s is 15. Even Ira’s ratio, hampered by security and investment issues, is shorter: 96 years (Statistical Review of World Energy 2025).

[21] A list of Kuwait Petroleum Company subsidiaries can be found at Kuwait Petroleum Co., https://www.kpc.com.kw/KCompanies. See also, Anthony Cordesman, Kuwait: Recovery and Security After the Gulf War (Westview Press, 1997), 30, https://www.routledge.com/Kuwait-Recovery-And-Security-After-The-Gulf-War/Cordesman/p/book/9780813332444. The “K-companies” include Kuwait Oil Company (KOC), Kuwait National Petroleum Company (KNPC), Kuwait Integrated Petroleum Industries Company (KIPIC), Kuwait Oil Tanker Company (KOTC), Kuwait Aviation Fueling Company (KAFCO), Kuwait Foreign Petroleum Exporting Company (KUFPEC), Kuwait Petroleum International (KPI), and Petrochemical Industries Company (PIC). In 2025, officials commenced the merger of KNPC and KIPIC as part of a broader restructuring of the hydrocarbons sector in Kuwait, and 2026 may see KOC merge with the Kuwait Gulf Oil Company (KGOC, which manages Kuwait’s interests in the Neutral Zone with Saudi Arabia) (Kawach, “Kuwait’s Downstream Oil Merger Nearing Completion,” Arabian Gulf Business Insight, November 28, 2025, https://www.agbi.com/oil-and-gas/2025/11/kuwaits-major-downstream-oil-merger-nearing-completion/).

[22] A supergiant field contains at least 5 billion known recoverable barrels (Barry Friedman, “What Role Will Super-Giant Fields Play in the World’s Future Energy Mix?” AAPG, https://www.aapg.org/news-and-media/details/explorer/articleid/61972/what-role-will-super-giant-fields-play-in-the-worlds-future-energy-mix?srsltid=AfmBOoqocjcBwVxWOEkFte_E9mqmg0QHcyA6DTNf0WFLZ4UE-leKKOUA.)

[23] The term “original oil in place” refers to the total volume of oil in a field prior to the start of production.

[24] Michael Kern, “The World’s 5 Largest Oilfields and Their Impact,” Oilprice.com, August 19, 2024, https://oilprice.com/Energy/Crude-Oil/The-Worlds-5-Most-Largest-Oilfields-and-Their-Impact.html; Farah Al-Nakib, Kuwait Transformed: A History of Oil and Urban Life (Stanford University Press, 2016), 91, https://www.sup.org/books/middle-east-studies/kuwait-transformed.

[25] Reem Alissa, “The Oil Town of Ahmadi Since 1946: From Colonial Town to Nostalgic City,” Comparative Studies of South Asia, Africa and the Middle East 33, no. 1 (2013): 41–58, 43, https://muse.jhu.edu/article/506690.

[26] “Kuwait Targets 3.1mn B/D End-2023 Capacity,” MEES 66, no. 10 (2023), http://archives.mees.com/issues/1996/articles/61889.

[27] “Kuwait Oil Company Announces ‘Giant’ Oil and Gas Discovery,” Offshore Technology, July 15, 2024, https://www.offshore-technology.com/news/kuwait-oil-company-giant-discovery/?cf-view; Robin Mills, “Kuwait’s Big New Offshore Oil Find,” Arab Gulf States Institute, July 24, 2024, https://agsi.org/analysis/kuwaits-big-new-offshore-oil-find/.

[28] “Kuwait Strikes Oil and Gas at Al-Jlaiaa Offshore Field,” Offshore Engineer, January 22, 2025, https://www.oedigital.com/news/521409-kuwait-strikes-oil-and-gas-at-al-jlaiaa-offshore-field.

[29] Dragana Nikše, “‘Landmark’ Gas Discovery Comes to Light Offshore Kuwait,” Offshore Energy, October 14, 2025, https://www.offshore-energy.biz/landmark-gas-discovery-comes-to-light-offshore-kuwait/.

[30] Ahmed Hagagy, “Kuwait Oil Company to Spend $3.9 Billion on Exploration by 2030, Deputy CEO Says,” Reuters, October 29, 2025, https://www.reuters.com/business/energy/kuwait-oil-company-spend-39-billion-exploration-by-2030-deputy-ceo-says-2025-10-29/.

[31] MEER workshop discussion.

[32] MEER workshop discussion.

[33] “Kuwait’s Downstream Revolution and Petrochemicals Ambitions,” The Energy Year, September 17, 2024, https://theenergyyear.com/articles/kuwaits-downstream-revolution-and-petrochemicals-ambitions/.

[34] Carole Nakhle, “Oil in Kuwait: The Time to Catch Up,” GIS Reports, March 19, 2020, https://www.gisreportsonline.com/r/kuwait-oil-time-to-catch-up/.

[35] MEER workshop discussion.

[36] MEER workshop discussion; Statistical Review of World Energy 2025; and U.S. Energy Information Administration (EIA), “What Countries Are the Top Producers and Consumers of Oil?” accessed November 17, 2025, https://www.eia.gov/tools/faqs/faq.php?id=709&t=6.

[37] “Kuwait: Oil Flows,” Oxford Analytica Daily Brief, August 1, 1991; “Kuwait: Economic Prospects,” Oxford Analytica Daily Brief, October 21, 1994.

[38] Nakhle.

[39] MEER workshop discussion.

[40] Jim Krane, “Climate Action Versus Inaction: Balancing the Costs for Gulf Energy Exporters,” British Journal of Middle Eastern Studies 47, no. 1 (2020): 117–35, https://doi.org/10.1080/13530194.2020.1714269.

[41] International Energy Agency (IEA), “Current Policies Scenario,” World Energy Outlook 2025, https://www.iea.org/reports/world-energy-outlook-2025/current-policies-scenario.

[42] Osamah Alsayegh, “How Economic and Political Factors Drive the Oil Strategy of Gulf Arab States,” Rice University’s Baker Institute for Public Policy, January 9, 2023, https://doi.org/10.25613/KPSA-QK94.

[43] MEER workshop discussion.

[44] A refining slate, or crude slate, is the portfolio of crude oil types — for example, light-sweet, heavy sour, shale oil — fed into a refinery (Corrina Ricker, “Crude Oil Used by U.S. Refineries Continues to Get Lighter in Most Regions,” EIA, October 11, 2019, https://bit.ly/4rPc73j).

[45] Mohamed Alzaabi, “Decarbonizing the Barrel: Global Trends in Oil’s Carbon Intensity,” Society of Petroleum Engineers, May 12, 2025; https://jpt.spe.org/twa/decarbonizing-the-barrel-global-trends-in-oils-carbon-intensity.

[46] Kuwait Petroleum Corporation Sustainability Report, 2022–23, https://www.kpc.com.kw/Sustainability.

[47] Mohamed Alzaabi, “Decarbonizing the Barrel: Global Trends in Oil’s Carbon Intensity,” Society of Petroleum Engineers, May 12, 2025; https://jpt.spe.org/twa/decarbonizing-the-barrel-global-trends-in-oils-carbon-intensity.

[48] “Permian Basin Emissions Declining as Production Grows,” S&P Global, December 19, 2025; https://www.spglobal.com/energy/en/news-research/blog/energy-transition/121925-permian-basin-emissions-declining-as-production-grows.

[49] “Permian Basin Emissions Declining”; Mohamed Alzaabi, “Decarbonizing the Barrel: Global Trends in Oil’s Carbon Intensity,” Society of Petroleum Engineers, May 12, 2025, https://jpt.spe.org/twa/decarbonizing-the-barrel-global-trends-in-oils-carbon-intensity.

[50] MEER workshop discussion.

[51] Country Analysis Brief: Kuwait, EIA, last updated July 20 2023, https://www.eia.gov/international/content/analysis/countries_long/kuwait/kuwait.pdf.

[52] Country Analysis Brief: Kuwait.

[53] Country Analysis Brief: Kuwait.

[54] “Kuwait: Analysis,” EIA, last updated July 20, 2023, https://www.eia.gov/international/analysis/country/KWT. Aside from a one-off import of liquefied natural gas (LNG) in 1984, Kuwait began importing LNG in 2009 and the volume of imported LNG has increased steadily ever since.

[55] Yesar Al-Maleki, “Kuwait Secures Qatari LNG Amid New Power Demand Record,” MEES, August 30, 2024, https://www.mees.com/2024/8/30/power-water/kuwait-secures-qatari-lng-amid-new-power-demand-record/28067e90-66d9-11ef-8fe8-63815d8709f8.

[56] Suyash Pande, “Kuwait Procures Six LNG Cargoes to Meet Peak Summer Requirements,” S&P Global, August 7, 2023, https://www.spglobal.com/commodity-insights/en/news-research/latest-news/lng/080723-kuwait-procures-six-lng-cargoes-to-meet-peak-summer-requirements.

[57] Nishant Kumar et al., “Kuwait Plans Fifteen-Fold Renewable Generation Boost, but Targets Need More Time,” Rystad Energy, September 15, 2025, https://www.rystadenergy.com/news/kuwait-fifteen-fold-renewable-generation-boost.

[58] Country Analysis Brief: Kuwait.

[59] “Gulf States: Kuwait,” Oxford Analytica Daily Brief, January 22, 1985.

[60] Kumar.

[61] “Kuwait: Analysis.”

[62] “Kuwait To Tap New Non-Associated Gas Provinces For 2030 Target,” MEES 66, no. 21 (2025), http://archives.mees.com/issues/2111/articles/64537.

[63] MEER workshop discussion.

[64] Alsayegh et al., “Distortionary Effects of Kuwait’s Cheap Electricity and the Case for a Just Reform,” Rice University’s Baker Institute Baker Institute for Public Policy, January 29, 2025, https://doi.org/10.25613/TR3Q-VQ96.

[65] “A ‘rentier nation’ is a state that receives all or a major portion of its income from the use (or ‘rent’) of its indigenous natural resources by foreign governments or individuals, without an increase in the productivity of its domestic economy.” (Alsayegh, “Lessons from Kuwait: How the Country’s Rentier Democracy is Slowing Its Energy Transition,” Rice University’s Baker Institute for Public Policy, April 5, 2023, https://doi.org/10.25613/R1ZE-AM65.)

[66] In 2025, officials commenced the merger of KNPC and KIPIC as part of a broader restructuring of the hydrocarbons sector in Kuwait, and 2026 may see KOC merge with the Kuwait Gulf Oil Company (KGOC, which manages Kuwait’s interests in the Neutral Zone with Saudi Arabia) (Kawach, “Kuwait’s Downstream Oil Merger”).

[67] Nicolas Parasie et al., “Kuwait Said to Mull Raising Up to $7 Billion From Pipeline Deal,” Bloomberg News, September 12, 2025; https://www.bloomberg.com/news/articles/2025-09-12/kuwait-said-to-mull-raising-up-to-7-billion-from-pipeline-deal.

[68] MEER workshop discussion.

[69] MEER workshop discussion; “Kuwait Petroleum Corporation Eyes Private Sector Expansion,” Arab Times, August 21, 2025, https://www.zawya.com/en/business/energy/kuwait-petroleum-corporation-eyes-private-sector-expansion-c0ky5t4g.

[70] Kate Dourian, “Kuwait’s New Energy Strategy Takes Off but Oil’s Still Dominant,” Arab Gulf States Institute, May 14, 2024, https://agsi.org/analysis/kuwaits-new-energy-strategy-takes-off-but-oils-still-dominant/; “Kuwaiti Power Privatization Plan Delayed: Report,” Zawya, March 18, 2025, https://www.zawya.com/en/projects/utilities/kuwaiti-power-privatisation-plan-delayed-report-sl552x13.

This publication was produced by Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by outside experts prior to release. Any errors or omissions are solely the responsibility of the author(s).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.