Author(s)

At the onset of the COVID-19 pandemic, it would have been difficult to blame the Federal Reserve (Fed) for the aggressive monetary expansion it implemented. In late February 2020, equity markets were crashing, and credit spreads were surging at a rate that resembled the early months of the Great Financial Crisis of 2007-2008. That recession left a devastating impact on the economy, and no policymaker wanted to risk that outcome again.

Seeking to fulfill its mandate of price stability and full employment, the Fed initiated a massive injection of liquidity into financial markets by purchasing U.S. Treasury securities and private debt instruments. As a result, the central bank’s balance sheet soared from $2.6 trillion to $4.6 trillion. Financial markets subsequently stabilized, with major equity indexes reaching and exceeding pre-pandemic levels. Credit spreads quickly peaked and began declining to normalized levels. The unemployment rate quickly fell after surging in the early months of the pandemic, and gross domestic product followed a similar pattern.

From this perspective, the Fed, in addition to actions taken by fiscal policymakers, reasonably mitigated further deterioration of financial and labor markets in the early months of the pandemic. The steps taken throughout the subsequent year, however, indicate an adherence to conventional countercyclical monetary policy at a time when the unusual nature of pandemic-driven behavior demanded a customized response. By prioritizing the implications of real interest rates — i.e., interest rates net of expected inflation — the Fed might have responded sooner to the post-pandemic surge in inflation. As the Fed reaches the peak of the contractionary cycle, the real interest rate could again serve as guidance in mitigating the risk of macroeconomic volatility moving forward.

The Rise and Fall of Inflation

In the years preceding the pandemic, inflation remained stable and often fell below the Fed’s 2% inflation target. Concerns over the risk of deflation often superseded concerns over rising inflation. The Japanese deflationary episodes of the 1990s and early 2000s highlighted the possible economic slowdown that might plague the U.S. economy if the Fed failed to sustain a positive inflation rate. These observations indicated the possibility that the Federal Reserve could aggressively expand monetary policy in response to the pandemic to circumvent deflation without risking a surge in inflation.

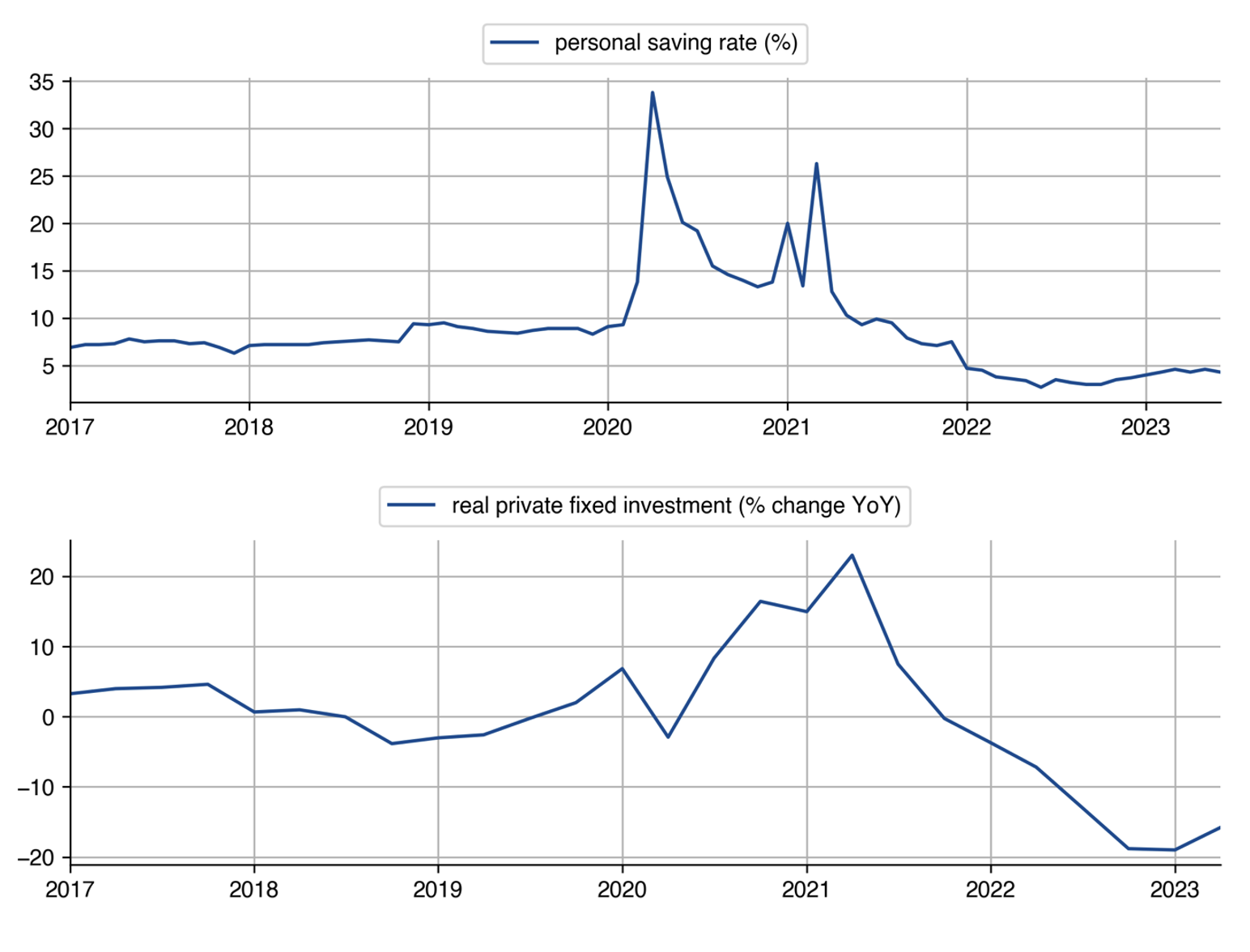

Figure 1 — Personal Savings Rate (top) and Private Fixed Investment (bottom), Percent Change Year-over-year Over the Pandemic-induced Business Cycle

The pandemic influenced behavior and created an economic environment that distorted the expansionary effects of monetary policy in unusual ways. For example, the decline in aggregate demand at the onset of the pandemic largely resulted from a decline in household consumption. This was an intentional restriction on spending, rather than a response to the macroeconomic environment at the beginning of a recession. As a result, household behavior became more insensitive to interest rate changes immediately after the pandemic, dampening the channel of expansionary monetary policy that operates by stimulating consumer demand.

By constraining spending during the pandemic, households’ savings rose dramatically. Some estimates indicate that excess savings rose by $2.3 trillion. This surge in savings expanded financial market liquidity, contributing to a cyclical decline in interest rates — an outcome that influenced financial markets in the same direction as monetary policy. The favorable financial market environment, in turn, caused business investment to increase sharply over that time period, as shown in Figure 1.

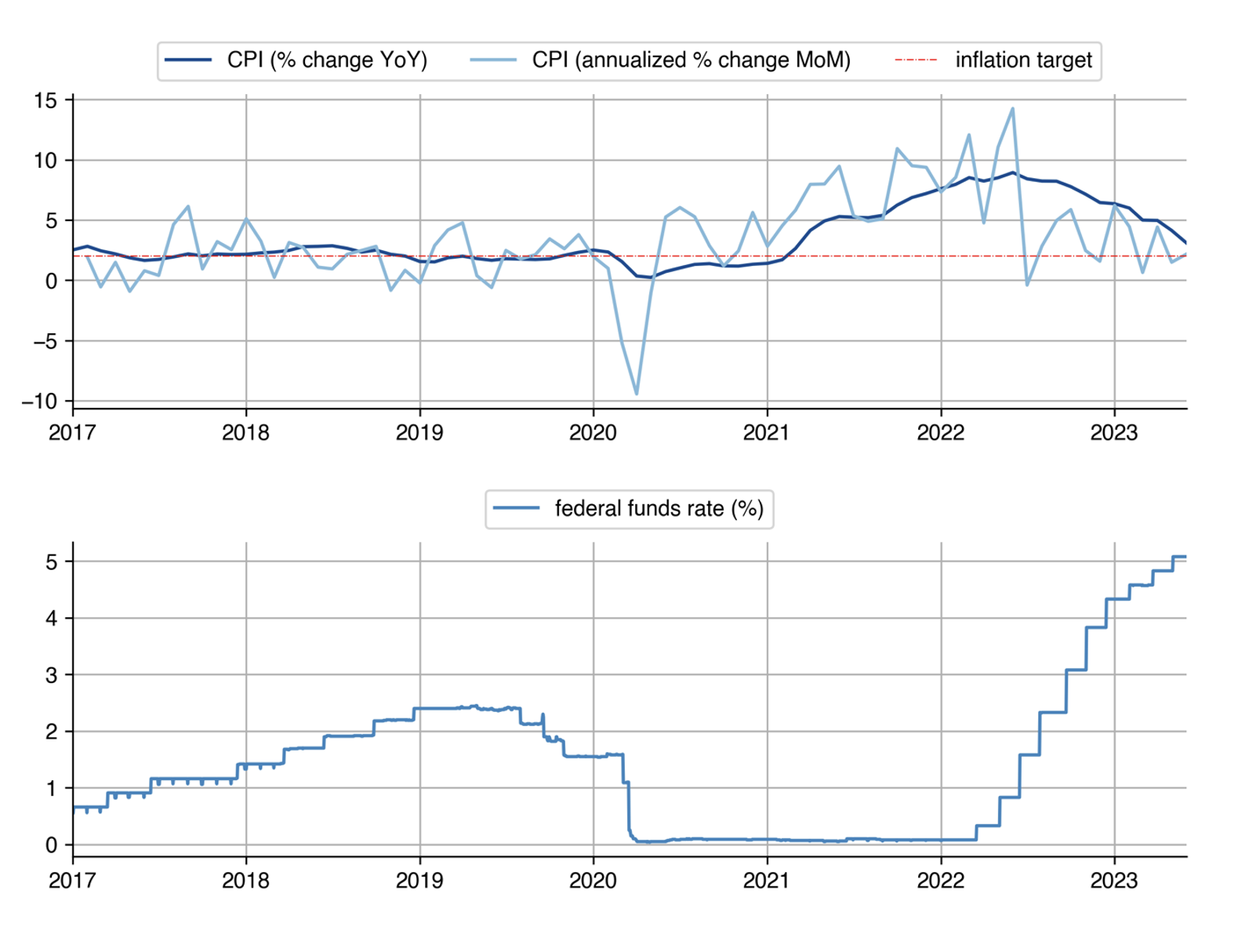

Figure 2 — Percent Change in Consumer Price Index (CPI, top) and Effective Federal Funds Rate (bottom)

By the middle of 2021, efforts to mitigate the spread of COVID eased, and economic activity began rebounding. Households, flush with an abundant stock of savings and supported by extensive fiscal stimulus, began spending at a rate that exceeded pre-pandemic levels. The surge in demand, combined with supply chain issues stemming from worker shortages and logistical disruptions, caused a surge in inflation to 40-year highs.

In the early months of the inflation surge, the Fed patiently gauged the sensitivity of prices to these market fluctuations. Meanwhile, the central bank continued implementing expansionary monetary policy, enhancing stimulus through the financial market environment. The combination of heightened household savings, accommodative monetary policy, and the surge in inflation caused real interest rates to decline.

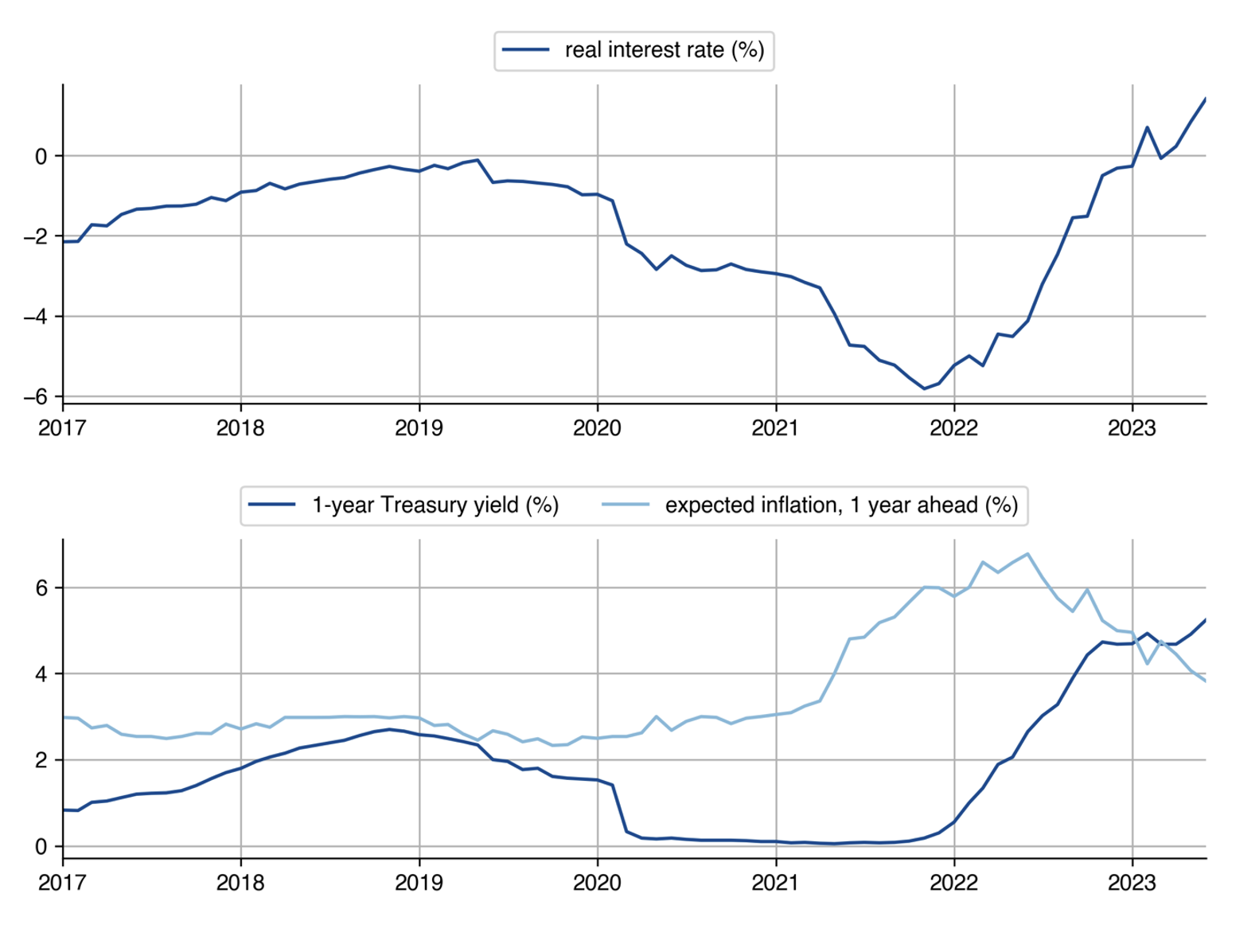

Standard macroeconomic theory suggests that real interest rates, i.e., interest rates net of expected inflation, drive real economic activity, and central bank manipulation of the real interest rate in the short run makes monetary policy effective by influencing consumption and investment decisions. However, by late 2021, the surge in inflation had caused the real interest rate to fall by nearly 5 percentage points — a monumental decline relative to the real interest rate in the preceding years.[1] This decline in real returns was even higher for deposits held in low-interest bank accounts, reducing the incentives to hold cash and intensifying monetary stimulus in the inflationary environment.

Figure 3 — Real Interest Rate (top), Defined as the Net of One-year U.S. Treasury Market Value (bottom) Minus One-year-ahead Inflation Expectations (bottom)

Finally, by early 2022, the Fed was no longer willing to maintain accommodative monetary policy. In March of 2022, it began aggressively increasing the federal funds rate, and inflation began to decline shortly thereafter. Although some debate remains regarding the extent of monetary policy effectiveness in both the increase and subsequent decline in inflation, this tightening cycle would mark a clear end to the favorable borrowing environment.

Balancing Risk at the End of the Cycle

As the inflation rate approaches the Fed’s 2% target, attention shifts to the proper rate of monetary deceleration. If the Fed can reach its target inflation rate in such a way that the economy converges back to trend economic growth without a significant drop, the outcome would be hailed as a so-called “soft landing.” Achieving this goal requires properly timing a peak in rates and a subsequent series of interest rate reductions back to the long-run value.

At any given time, the Fed faces two major obstacles in achieving proper timing of monetary policy implementation. First, the Fed must try to determine the current rate of inflation from the noisy data it receives. The year-over-year (YoY) percent change in the consumer price index gives a stable but retrospective measurement of inflation. Conversely, the annualized month-over-month (MoM) value gives a more instantaneous but also more volatile measurement. Figure 2 shows how the MoM inflation rate appears closer to the inflation target than the YoY rate, but still hovers somewhat above pre-pandemic levels. This provides a case for continued monetary contraction. The second issue involves lags in the effectiveness of monetary policy. Estimates suggest that monetary tightening affects inflation with lags of anywhere from six months to two years — a feature that former Fed Chair Ben Bernanke compared to driving a car while looking in the rearview mirror.

Without a corresponding decline in nominal interest rates over the next several months, declining inflation could cause real interest rates to surge, increasing the risk of an excessive economic slowdown. Figure 3 shows that real interest rates appear to be well above pre-pandemic levels, reflecting, at least in part, the Fed’s contractionary efforts. Given the lags in monetary policy effectiveness, continued interest rate hikes that raise real interest rates would likely cause an extended macroeconomic contraction over the next several months, even if inflation reaches its target sooner — i.e., a hard landing.

Uncertainty over drivers of long-term real interest rates has historically complicated quantitative modeling of monetary policy, and the current macroeconomic environment is no exception. The real interest rate has been declining steadily over the past four decades — a trend that recent research suggests is the result of a demographic-driven surge in savings, relative to the size of the economy. Projections based on the path of demographics in this framework indicate that future real interest rates will continue to decline, at least for the next decade. As a result, taking the pre-pandemic real interest rate as a baseline value could cause monetary policymakers to overshoot the contraction — even by maintaining nominal interest rates at current levels — if a declining long-run trend is the proper baseline. This implies that even reducing nominal rates from current levels could inadvertently prolong the contractionary monetary policy environment.

Several participants of the Federal Open Market Committee, which meets regularly to determine monetary policy implementation, have indicated an inclination to prolong the tight monetary environment. At the same time, all members expect the interest rates to decline persistently over the next few years — a sentiment likely shared by financial markets, as interpreted by the deeply inverted yield curve. Still, with the possibility of a soft landing hinging on the timing and magnitude of the rate decreases over the next few years, central bankers would be prudent to follow the guidance implied by real interest rates on the back end of the inflationary cycle.

Conclusion

In its response to the onset of the pandemic, actions taken by the Fed likely mitigated the deterioration of capital markets and avoided a deflationary episode. Consumer behavior induced by the pandemic caused an unusual macroeconomic environment, in which households significantly shifted consumption over time. This change in behavior, combined with supply chain disruptions and extensive fiscal stimulus, generated a corresponding surge in inflation. The Fed responded with conventional countercyclical monetary policy at a time when a customized response may have resulted in greater price stability.

With the benefit of hindsight, opportunities for the Fed to increase interest rates sooner in the post-pandemic inflationary cycle seem clear. Plummeting real interest rates throughout 2020 and 2021 contributed to a surge in household and business spending, even as inflation began to rise throughout 2021. As the cycle matures, the Fed seeks to implement monetary policy that achieves price stability while avoiding an excessive economic contraction. The high (and rising) real interest rates as inflation approaches its 2% target, combined with the monetary policy effectiveness lags, indicate that the Fed risks overshooting a soft landing by continuing to implement contractionary monetary policy.

Endnote

[1] This result is robust to alternative measures of the real interest rate, including the rate on 10-year U.S. Treasury securities net of the consumer price index growth rate and various real interest rates measured by the Federal Reserve Bank of Cleveland.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.