Author(s)

Challenges to the Fed’s Independence

President Donald Trump has repeatedly called for the Federal Reserve to cut interest rates. He has been critical of Fed Chairman Jerome Powell, even suggesting that he should be removed from his position. Powell’s term expires early next year, and Trump is in the process of seeking a new Fed Chairman. He recently appointed Council of Economic Advisers (CEA) Chairman Steven Miran to the Fed Board to fill an open position for the remainder of its term. And most recently, Trump has attempted to fire Fed Board governor Lisa Cook for alleged mortgage fraud. Cook has refused to accept the firing and hired a high-profile attorney to challenge Trump’s power to dismiss her.

This is all part of a broader issue of focusing on the independence of the Fed. Trump’s attempts to stack the Fed with individuals who share his economic views is one way to impact the monetary policy of the U.S. central bank. But it is not the only threat to Fed independence. Unsustainable fiscal policy and the sizable debt the U.S. has run up in the past two decades pose additional risks.

When the Fed must use monetary policy to counteract a high-spending federal government’s fiscal policy, the Fed’s job becomes more difficult, increasing the risk of a financial crisis. The Fed’s mandate to create stable prices and full employment is hard enough without the added complexity of trying to offset the impact of unsustainable fiscal policies and other economic policy decisions. This brief discusses what the Fed needs to consider in making decisions going forward.

Balancing the Fed’s Dual Mandate

In fulfilling its dual mandate of achieving price stability and full employment, the Fed should consider several key factors.

Inflation Rate

In terms of price stability, the Fed targets an inflation rate of 2%. Since 2022, the U.S. inflation rate rose sharply, then fell, but has failed to reach the Fed’s 2% target. After inflation peaked at about 9% in mid-2022, the highest in four decades, the Fed responded aggressively with rapid interest rate hikes, lifting the federal funds rate from near zero in early 2022 to above 5% by mid-2023. This was the fastest tightening cycle since the 1980s. In addition, the inflation rate gradually eased as federal stimulus payments were trimmed back, the pandemic supply shocks dissipated, and energy prices moderated. This restrictive stance cooled demand, slowed wage growth, and helped bring inflation down toward, but not reaching, the Fed’s 2% target by the end of 2024. The inflation rate has remained above the target rate throughout 2025, with data yielding mixed signals about the future path of inflation.

The latest data shows headline Consumer Price Index (CPI) inflation at 2.9% in August, while core inflation, which excludes volatile food and energy prices, was 3.1%. The Fed still has work to do to achieve its targeted price stability level. In addition, greater tariffs and labor supply issues increase the uncertainty about the path of the price level looking forward.

Effects of Tariffs

Tariffs raise input and consumer costs directly by making imported goods more expensive. Higher duties on imported intermediate goods ripple through to final goods in industries such as manufacturing and construction. Indirectly, tariffs can disrupt supply chains, raise uncertainty, and reduce efficiency, all of which push prices higher. As of the middle of 2025, the data has not definitively shown a tariff related increase in prices, possibly due to tariff front running and pause in the implementation of the reciprocal tariffs, but it has shown a softening labor market. However, the latest revision of GDP data does imply that tariffs are raising prices.

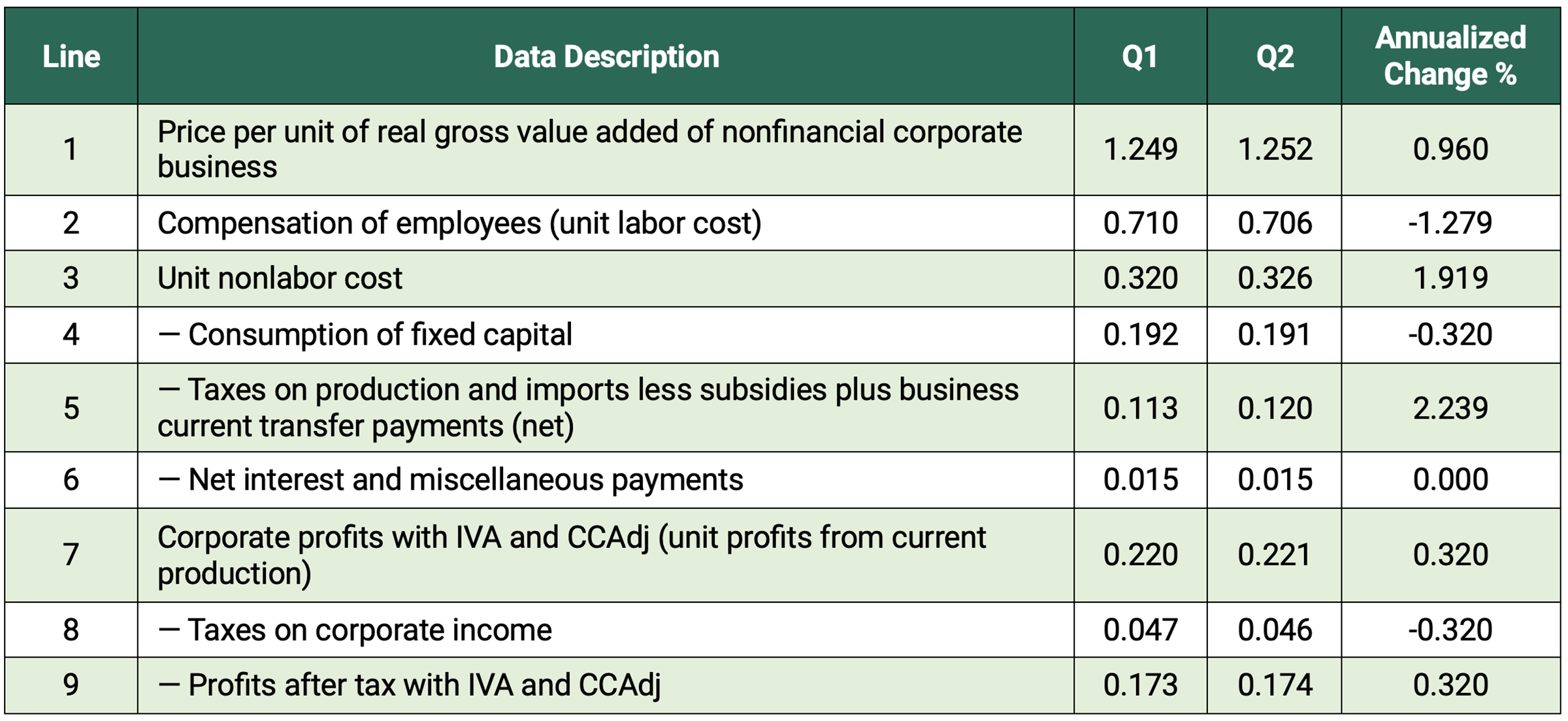

The most recent update to the National Income and Product Accounts (NIPA) data provides an estimate of the impact of tariffs on prices in Table 1.15. Note that in NIPA, tariffs are included in the line labeled taxes on production and imports. Conceptually, the Bureau of Economic Analysis (BEA) treats tariffs like an excise tax — a payment made at the border that becomes part of the domestic value of goods sold. This implies that as tariffs rise the value of nominal GDP rises as well. This is true even though tariffs flow to the government, not to domestic producers. NIPA Table 1.15 is titled the “Price, Costs, and Profit Per Unit of Real Gross Value Added of Nonfinancial Domestic Corporate Business.” Thus, calculating the change in the price level for nonfinancial corporate businesses (NFCB) across quarters yields an estimate of the increase in customs duties.

Table 1 below reproduces the values shown in NIPA Table 1.15. Tariffs show up as a positive contribution to unit prices of roughly 2.24%. This increase is mitigated by a reduction in labor costs of 1.28% and a decline in depreciation expense of 0.32% points. This implies a total unit price change of about 0.96% — based on the formula that changes in unit prices equals change in taxes minus change in labor costs and change in depreciation costs.

Table 1 — Price, Costs, and Profit Per Unit of Real Gross Value Added of Nonfinancial Domestic Corporate Business

Note: “IVA” refers to inventory valuation adjustment and “CCAdj” to capital consumption adjustment.

Other Inflation Drivers

Reduced immigration can also raise prices as it limits labor force growth. Since immigrants disproportionately fill roles in agriculture, construction, health care, and service industries, fewer available workers can mean higher wage pressures as firms compete for scarce labor. A recent Fortune magazine article warns that a surge of inflationary pressures is building in the agriculture sector.

The potential for wage-driven inflation is most likely in the services sector including restaurants, health care, and personal services. These sectors already contribute to the higher than targeted level of core inflation in the economy. However, the data in Table 1 indicates that unit labor costs fell in the second quarter of this year. This is likely the result of a softening labor market as firms reduce costs by substituting capital for labor or seek other ways to minimize the amount of labor in the production of goods and services. This is consistent with the surge in labor productivity reported in second quarter data.

Navigating Economic Crosscurrents

The Fed is expected to avoid spurring an increase in inflation, particularly given that it has currently stalled above the target level of 2%. However, the Fed must also consider balancing the fight against inflation with concerns over slowing employment growth. Keeping interest rates elevated too long could lead to a rapid increase in unemployment and the onset of recession.

The U.S. labor market is flashing warning signs on several fronts:

- Total nonfarm payroll employment rose by just 22,000 in August, significantly below expectations.

- Employment estimates for May and June were revised downward by a combined 258,000 jobs, leading to the unexpected firing of the Bureau of Labor Statistics (BLS) commissioner.

- Hiring freezes are becoming more common, making it difficult for recent graduates and early-career workers to gain traction in the labor market. The unemployment rate for recent graduates is 5.8%, compared to an economy wide unemployment rate of 4.3%.

Equally troubling, long-term unemployment is also increasing. In August, over 1.9 million people had been out of work for more than 27 weeks, accounting for a quarter of the jobless. However, the unemployment rate is still relatively low at 4.3%. This is partly explained by the declining labor force participation rate, which dropped three out of the last four months to 62.3%. With AI’s potential to displace workers and firms’ incentives to seek cost savings, a reduction in the demand for labor seems likely moving forward. However, on the supply side the reduction in immigration and the aging labor force combine to reduce the supply of labor. As noted by Fed Chair Powell, this leaves the labor market in a “curious kind of balance.”

It looks likely that the Fed will begin to cut rates at its next meeting. This will raise the risk of reigniting inflation, but the cooling labor market seems to be a bigger concern at this moment. While a reduction in the short-term interest rate may spark an increase in economic activity, it is unlikely to be a panacea to the problems facing the United States. Long-term interest rates have increased with the last few drops in the Fed’s fund rate. Similarly, as the United Kingdom cut its rates five times since August 2024, interest rates on long term bonds also increased. Put simply, a lack of fiscal restraint cannot be solved with lower short-term interest rates.

While current odds favor a cut by a wide margin, the question becomes how many times and by how much will the Fed reduce interest rates before the end of the year.

Managing the Fed’s Balance Sheet

An important issue facing the Fed is the state of its balance sheet. In a speech delivered at the Dallas Federal Bank, Governor Christopher J. Waller tackled the complexities of the Fed’s expanded balance sheet — now around $6.7 trillion or roughly 22% of GDP, compared to just 6% in 2007. He traced this expansion primarily to two structural shifts:

- The adoption of an ample‑reserves framework.

- The Fed’s extensive use of quantitative easing (QE) during financial crises.

Importantly, he emphasized that a little less than half of today’s balance sheet is made up of currency in circulation and the Treasury General Account. These factors are outside the Fed’s control, which counters the notion that the Fed could simply revert to precrisis levels in terms of the size of its balance sheet, which was $870 billion in 2007.

Waller advocated for a thoughtful strategy to shrink and change the composition of the balance sheet over time. His vision includes allowing securities to mature without replacement, guiding reserve balances down to a more appropriate level — what the Fed calls “ample,” about $2.7 trillion — and trimming total holdings to near $5.8 trillion. Critically, he emphasizes better duration matching to reduce interest rate risk. To achieve this the Fed would have to move out of long-term assets, like agency mortgage-backed securities, toward short-term Treasury bills. Such a transition should be implemented gradually and predictably to minimize market disruption.

The Fed needs to normalize its balance sheet to preserve policy flexibility, reduce financial and political risks, and sustain the credibility of U.S. monetary policy.

Decisions Ahead for the Fed

The Fed’s dual mandate is being tested: inflation has fallen from its 2022 peak but remains above the 2% target, while employment growth is weakening. The central bank is expected to weigh the danger of cutting rates too soon (risking higher inflation) against keeping them elevated too long (risking recession and rising unemployment). The Fed faces the challenge of operating in policy world filled with uncertainty. The recent appeals court ruling striking down Trump’s tariffs injects major unpredictability into U.S. trade and fiscal policy. With the decision stayed until mid-October and a Supreme Court showdown ahead, businesses and markets face weeks of ambiguity over tariff rates and refund liabilities.

This makes the Fed’s decision at its mid-September meeting even more complicated, as it hinges on critical data releases ahead of the meeting. The Federal Open Market Committee will need to weigh whether the greater threat is lingering inflation or a rapidly cooling labor market, all while navigating the uncertainty surrounding the legality of U.S. tariffs and their implications for the federal budget.

Beyond interest rate policy, the Fed faces the challenge of reducing and reshaping its $6.7 trillion balance sheet. As Waller emphasized, gradual normalization is necessary to preserve policy flexibility, reduce interest-rate and political risks, and restore the Fed’s long-term credibility without disrupting markets. This is crucial as it may impact the evolution of long-term interest rates.

This publication was produced on behalf of Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by external experts prior to its release. Any errors are the responsibility of the author(s) alone.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.