Introduction

In December 2021, China’s State-Owned Assets Supervision and Administration Commission (SASAC) approved the creation of the China Rare Earth Group.[1] This entailed the merger of three of China’s dominant “Big 6” rare earth state-owned enterprises (SOEs) into one mega-conglomerate. The behemoth company’s control of up to a quarter[2] of global mineral-bearing rare earth elements (REE),[3] combined with China’s overall dominance in rare earths (with roughly 60% of world production), grants Chinese central planners significant pricing power and influence over world supply.

Our paper provides an overview of the Chinese rare earth industry, the 2021 reorganization and the potential ramifications of China’s role as an outsized supplier of essential minerals and elements during a time of global tensions. Given China’s growing control of rare earths and their criticality for a wide variety of applications — including common household items, energy transition technologies and defense systems — it is essential that U.S. policymakers support more assertive strategies and policies to bolster raw materials supply chains.

Overview

The structure of global REE supply and supply chains is illustrative of pervasive, high-level conflicts of varying intensities as shifts in economic and geopolitical influence unfold. These conflicts entail global imbalances in raw materials flows and import dependencies of both commodities and manufactured components that are gaining increasing attention given their strategic importance for defense systems and non-defense imperatives. Supply and value chains, producers and customers across defense and non-defense applications all could benefit from expanded civilian REE uses — so long as key players can align the enormous suite of intensely competing interests well enough to foster cooperation.

One of the main sources of tension is the pronounced push for alternative energy technologies, which is generating intense additive strain on already vulnerable supply chains. We make an observation in our conclusions that the ultimate “de-riskers” are voters and taxpayers, and that political messaging must be clear. Citizens are being called upon to backstop aggressive mandates and subsidies for alternative energy technologies, like wind and solar, as well as a historic, wholesale conversion of transportation to battery electric mobility. Classic “guns vs. butter” debates are encumbered by historically high debt loads across countries, worries about economic performance and growth, clashing ideas about the roles of markets and government, and discord between economic and environmental priorities. Much of what we lay out in this paper cuts across many other issues regarding minerals and elements of interest. Readers can draw caution flags and lessons for a wide array of materials-dependent energy and defense headlines.

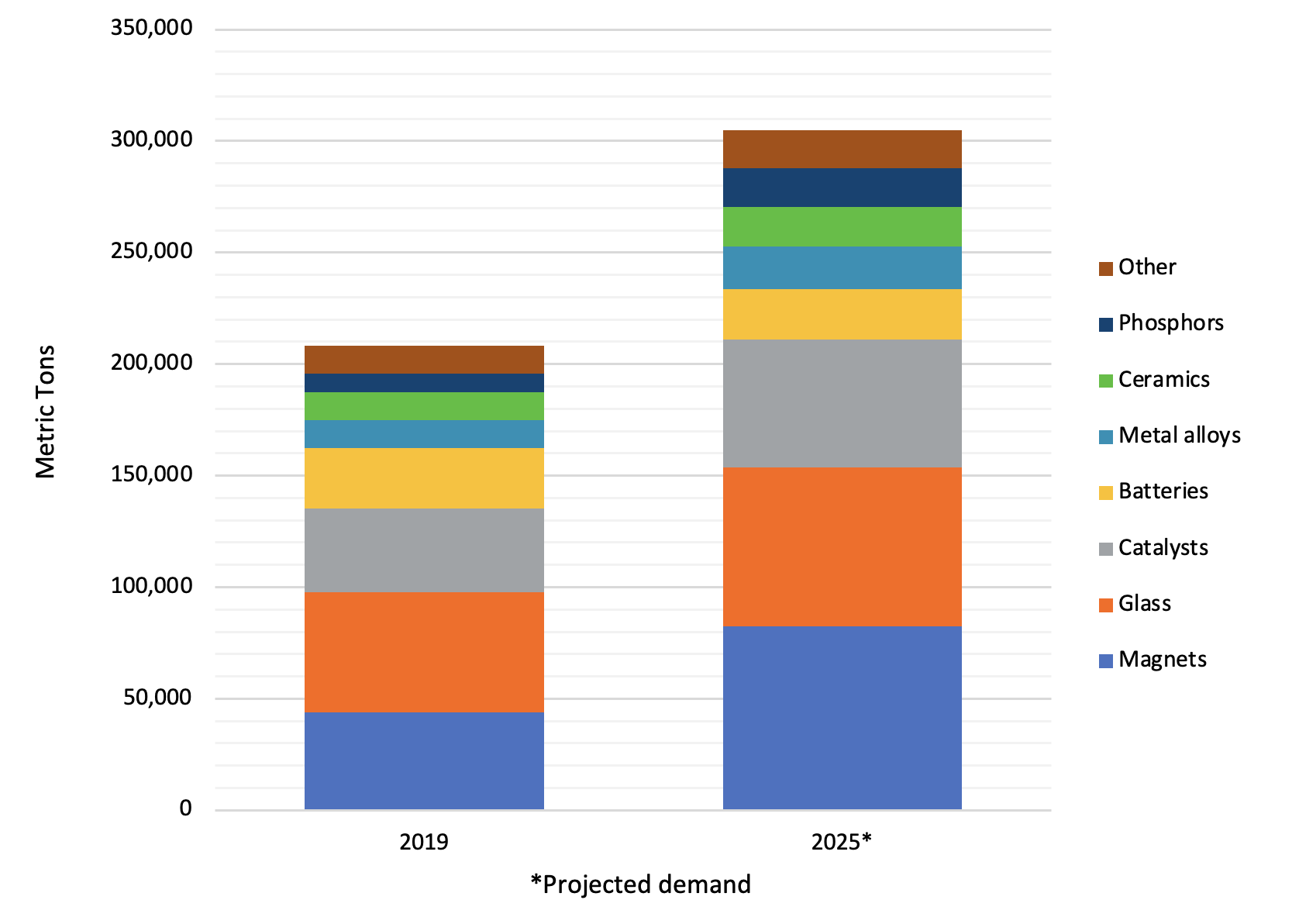

Although the global REE market is small (rare earth oxides, REOs, comprise about 0.01% of total mined tonnage for nonfuel minerals), their importance to a wide variety of strategic technologies cannot be understated. Contrary to their name, the 17 elements that comprise the REE group are actually common in occurrence, though difficult to extract given their typically low concentration in many ores and rapid oxidation.[4] REE are critical in a wide variety of high-tech end-use applications. These include common household items such as digital cameras, computers and integrated smartphones. REE sensitivity especially affects defense. The Congressional Research Service reported that every F-35 Lightning fighter jet requires approximately 920 pounds of REE, while each DDG-51 Aegis destroyer warship would require around 5,200 pounds of REE.[5] Different REE are combined into various components for end uses ranging from permanent magnets for electric motors and guidance and control systems, to displays, catalysts for petroleum refining, and other industrial processes and electronics. While defense applications clearly benefit from broad commercial uses that enhance economies of scale for REE production and REE-dependent components, rapid growth in non-defense uses such as electric vehicles and wind power — without commensurate expansion of REE supply and manufactured components — can induce supply chain stress.

Figure 1 — Current and Projected REO Applications

The COVID-19 pandemic during 2020 and Russia’s invasion of Ukraine in February 2022 highlighted fragilities in global commodity supply chains and trade flows. These events also peeled away layers overlying growing tensions among competing world powers and shifting balances of power and influence. They serve as sobering reminders that relying on dominant suppliers and revisionist actors for vital commodities can create significant pitfalls. In particular, rising trade and geopolitical security tensions with China could threaten REE supply, potentially influencing up to $1 trillion of goods.[6]

The world experienced a wakeup call on the consequences of China withholding REE supply in 2010, an event we address later. Chinese officials would be unlikely to restrict rare earth supplies for purely political reasons during times of relative peace. A 2014 World Trade Organization (WTO) ruling limits their ability to reduce exports while maintaining domestic production. Additionally, supply disruptions would weaken their dominant position as the West develops alternatives. However, in the event of military confrontation between the U.S. and China, increasingly likely given hot spots like Taiwan, the Chinese could be inclined to limit rare earth exports given their end uses in defense technologies and other strategic goods. With the newly consolidated rare earth industry and the sovereign-owned China Rare Earth Group at the helm, Chinese officials are now better equipped to institute and enforce production and export restrictions, manipulating prices in a manner beneficial to their priorities.

China’s 2021 REE industry reorganization is the most recent chapter in the industry’s rather turbulent regulatory history — and likely not the last. Consolidation to a structure dominated by a small handful of firms has been a decades-long priority of the central government. Reducing production and pricing inefficiencies, standardizing mining practices for improved social and environmental sustainability, and increasing the state’s ability to enforce regulations were the primary motivations of the reorganization. Highly pervasive illegal mining, supported by bureaucratic friction between the central and local governments, remains a key issue for Chinese central planning. Many of their central priorities (especially in realms of technological competition and decarbonization) are highly dependent on stable rare earth prices and supplies to meet rising domestic demand. As such, the merger is a signal of Beijing’s resolve to chop off dead wood and overhaul an industry with key players that regularly go rogue.

China’s Rare Earth Dominance

Backstory – The Context is Magnetic

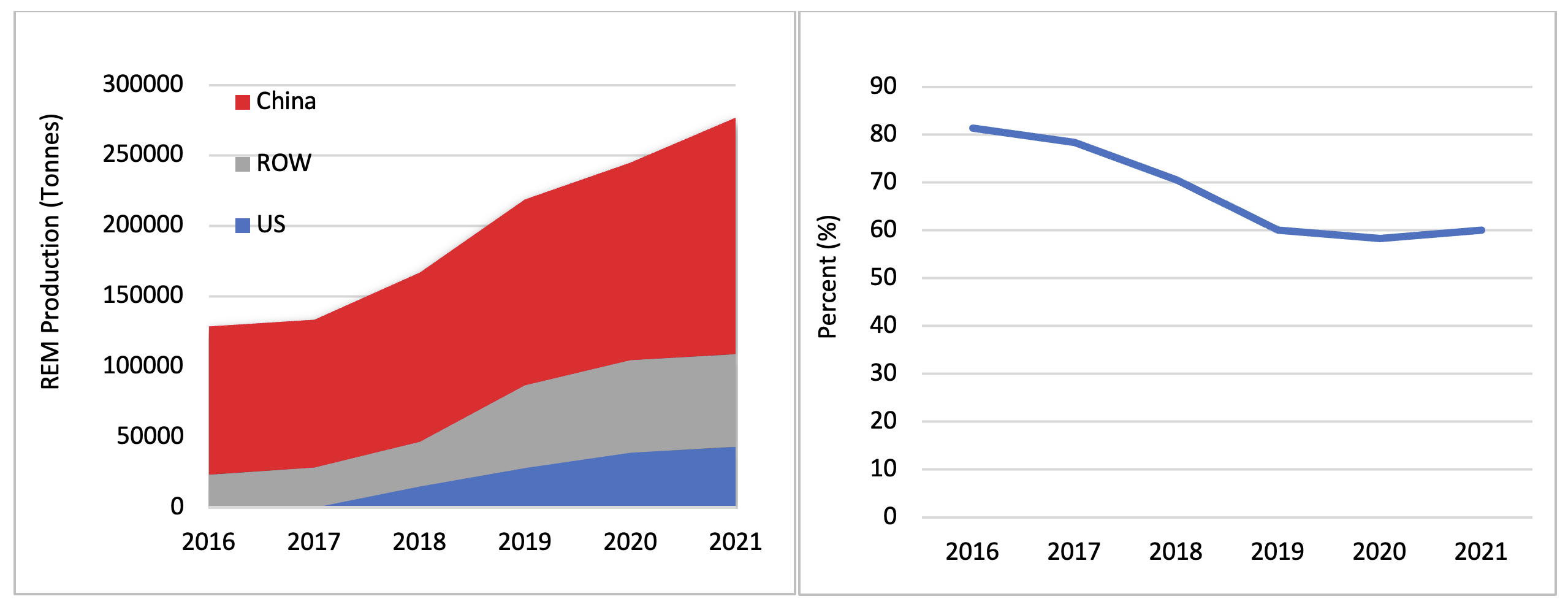

As noted at the outset, China’s share of REE global production is about 60%. China’s mined production share would likely be even higher if it were possible to account for supply from illegal mining operations. Chinese firms retain firm command of upstream production even with declines in market share in recent years.

Figure 2 — World Mine Production of REO (left) and China’s Share (right)

Note ROW means rest of world.

China’s even stronger position in producing rare earth products, such as rare earth permanent magnets, supplements their premier position in global mined supply.[7]

Rapidly accelerating demand for rare earth products further downstream — such as rare earth hydrogen polishing, battery energy storage materials and sintered permanent magnets — was heavily supported by the growth of China’s upstream rare earth extraction industry. The various industries that make up the rare earth ecosystem in China developed symbiotically and in geographical clusters, primarily in resource-rich areas such as Xiongan in Inner Mongolia.[8] Foreign investment and direct outsourcing to China buttressed the industry’s growth.

The outcome is that China’s control across virtually all nodes of rare earth metal supply chains is even more pronounced. China controls 85% of global refined REE supply using its domestic mined concentrates and imports.[9] Chinese firms control the majority of permanent magnet production. China also holds an 87% market share for the industry-standard neodymium-iron-boron (NdFeB) magnet, accounts for approximately half of global supply for the high-performance NdFeB magnets, and dominates advanced-sintered NdFeB magnets (Figure 3) that are required for certain “green” technologies like electric vehicles (EVs) and wind turbines.[10] More than 90% of all EVs sold worldwide in 2017 were equipped with drivetrains that use the industry-standard NdFeB permanent magnet.[11]

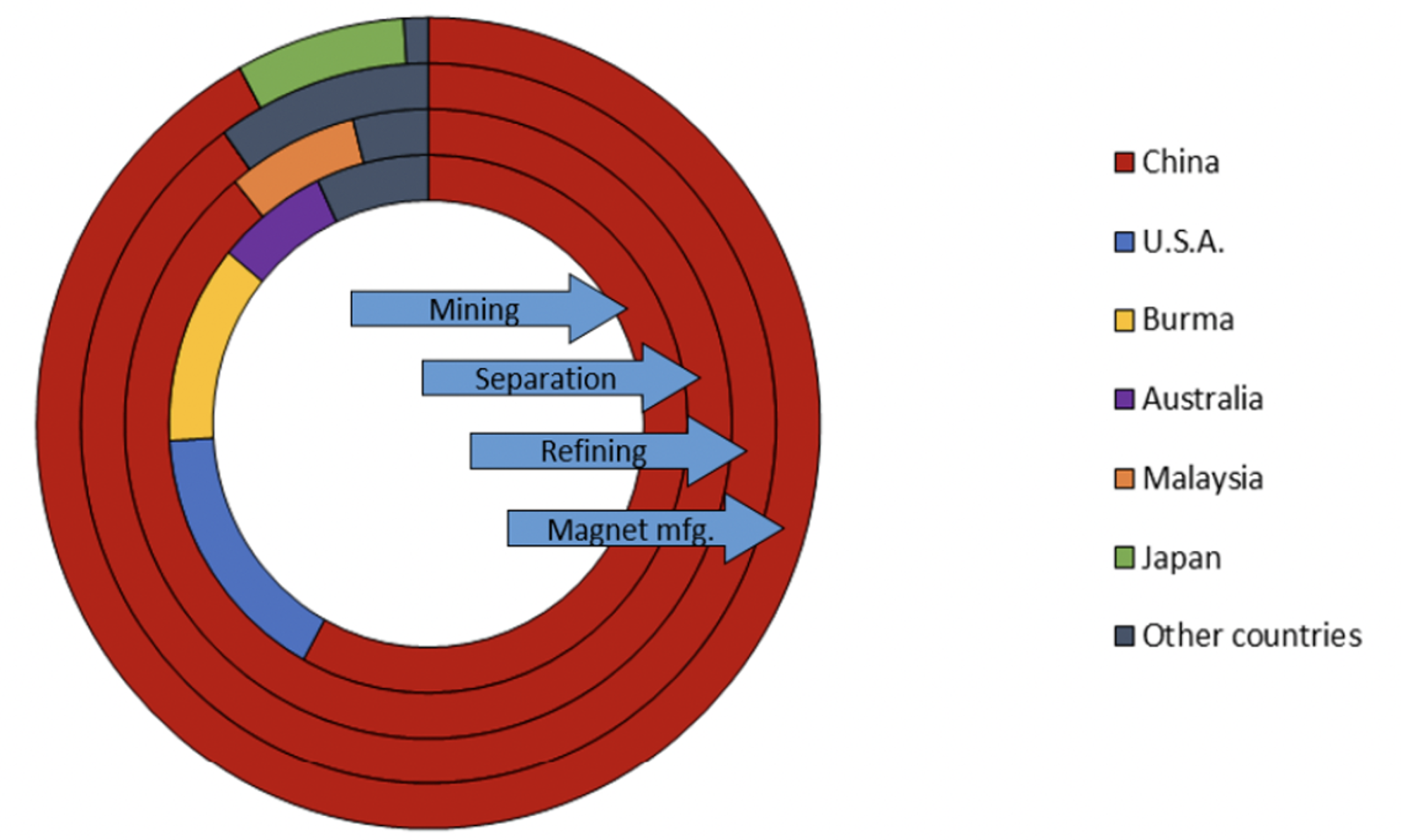

Figure 3 — Geographical Concentration of Supply Chain Stages for Sintered NdFeB Magnets

From center: Rare earth mining, oxide separation, metal refining and magnet manufacturing.

In typical fashion, downstream REE applications provide a higher value-added than upstream industries. Commercial imperatives, along with the geopolitical implications of further downstream control, remain an explicit motivation of Chinese policies affecting the rare earth industry. From high-level Chinese government communiques, which set the broader direction of the industry as a whole, to state-led mergers, downstream expansion figures as a central priority.[12]

Now, the same countries from which inbound investment was sourced — primarily the U.S. (whose laissez-faire market policies were abused by Chinese state-directed incentives) — are fighting to claw back their production.

A Regulatory Progression

China’s strong position reflects decades of regulatory policies through which the Chinese government prioritized developing the rare earth ecosystem from upstream extraction to downstream manufacturing. As early as the 1980s, China’s government began issuing export tax rebates for domestic producers as a means of supporting the young industry.[13] As the industry expanded, so did protectionist policies: In 1990, China declared REE a “strategic resource,” thereby prohibiting foreign investment in the sector.[14] In the decades that followed, the government and rare earth producers regularly met to discuss ways to control production and exports as a means of conserving the country’s mineral resources and protecting the environment.[15] While the government now focuses more on developing downstream capabilities, a shift from their extractive focus decades ago, rare earths still figure prominently in high-level communiques. For instance, China’s most recent Five-Year Plan focuses on developing more value-added production, “such as high-end rare earth functional materials, high-purity special steels, high-performance alloys, high-temperature alloys, [and] high-purity rare metal materials.”[16]

In the past few decades, Chinese regulators have focused more on increasing the industry’s economic, social and environmental sustainability. Several high-profile incidents occurred during this time, including a trade dispute with Japan in 2010 over conflicting claims in the South China Sea. The suspension of REE exports to Japan (detailed later) signaled that Beijing was highly conscious of the geopolitical implications of their control of rare earths, along with the benefits of greater political alignment between governmental and industrial priorities. In general, China’s rare earth policies of the last decade and a half were primarily motivated by a desire to enhance economic growth and maximize returns from the development of its rich endowment of rare earths, while also managing the conflicting desire for sustainable development.[17]

To achieve greater alignment between sovereign state industrial priorities and the sometimes-rogue domestic rare earth industry, Chinese officials have not been shy in utilizing a broad range of policies. Since the 1980s, the Chinese government has used a combination of tax incentives, production and export controls, and forced consolidation to reorganize the Chinese rare earth industry. The administrative expansion over rare earths has delayed “marketization” of the industry, which is highly dependent on government policies for development.[18] The consolidation of three of Chinas “Big 6” rare earth SOEs is simply the latest foray by China’s administrative state, a culmination of decades of attempts to control the rare earth industry.

Production Controls

In the 1990s, China’s leadership tasked the National Rare Earth Development and Application Leading Group (Rare Earth Office) of the Chinese Ministry of Land Resources (MLR) with developing production plans for the rare earth industry. These included setting overall production quotas for the entirety of the domestic industry as well as quotas for individual provinces. However, the Ministry of Industry and Information Technology (MIIT) began setting its own quotas for rare earth production, which appeared simultaneously with quotas from the MLR and caused compliance confusion given that the MIIT set their benchmarks significantly higher than the MLR. In 2010, the two bodies started using the same target as a production cap.

Throughout the history of the quota regime, actual production has significantly outpaced caps set by the MLR and MIIT. This is primarily because provincial governments are in charge of allocating their allotted quotas to individual companies and enforcing production caps.[19] Thus, conflicting interests often create wedges between central and local regulators. Local rare earth industrial clusters, which include a range of operations from extraction to downstream innovation for rare earth products, often demand a supply of rare earth metals (REM) that exceed the quotas.[20] The economic benefits that booming rare earth industries brought to areas such as Inner Mongolia and the Fujian, Jiangxi and Xinjiang provinces pushed some local regulators to overlook overproduction. Proper enforcement of production quotas is a prerequisite for Beijing to control prices, achieve sustainable resource management and manage trade flows (among other priorities). Consequently, policies that better align local production with national production quotas are highly sought after in the capital.

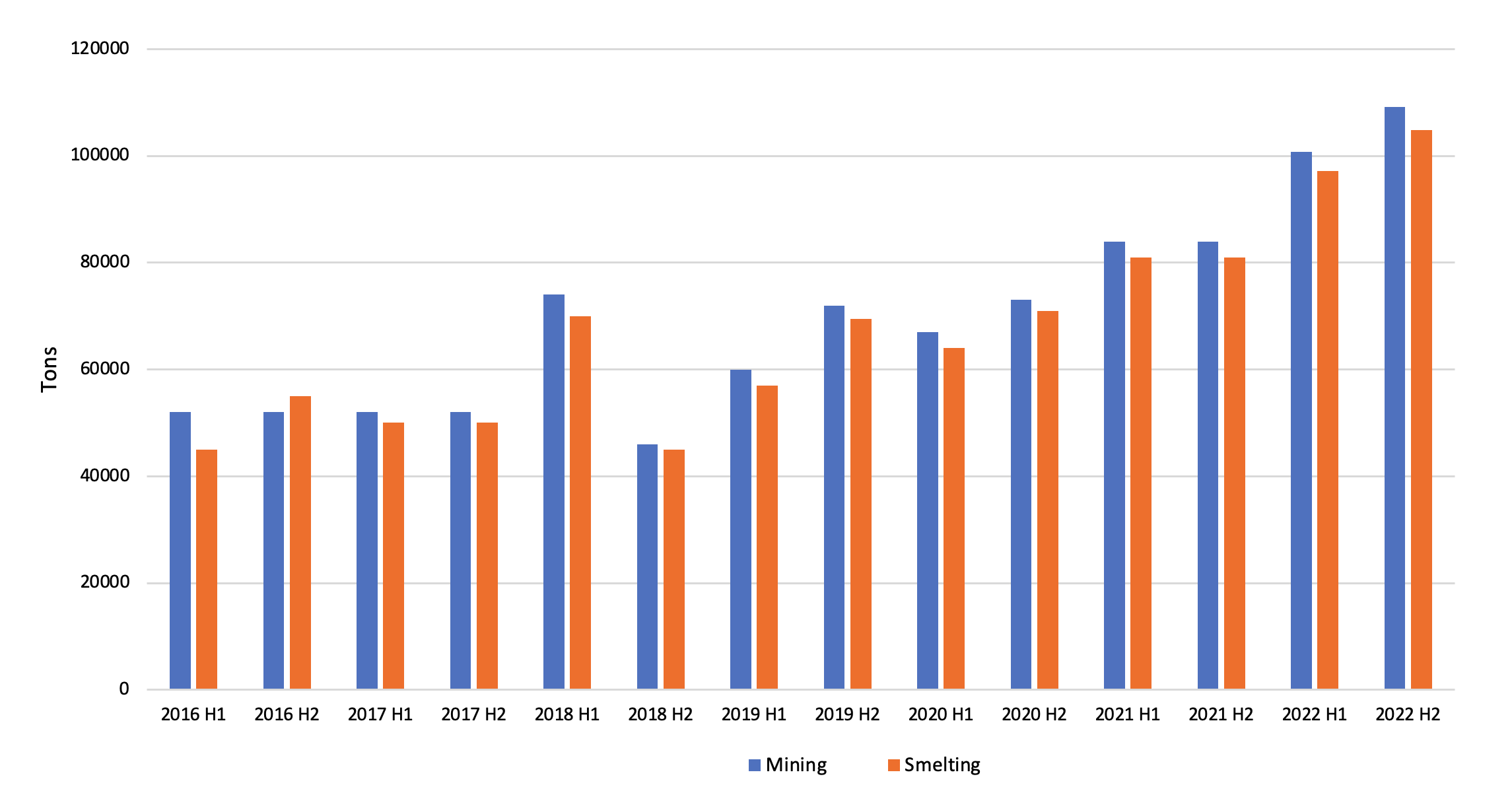

In recent years, the MIIT has consistently raised the domestic production quota to mitigate demand increases. The full-year rare earth mining quota for 2022 was set at 210,000 tonnes, a new record and a 25% increase from 168,000 tonnes in 2021, the previous record.[21] As such, tightening regulations do not necessarily accompany cuts in the production quota as they did in the 2010s. Rather, the state purports to increase output in a sustainable manner aligned with central priorities, a reigning in of sorts for an industry that must grow to meet rising domestic and international demand. The China Rare Earth Group and future super-conglomerates are valuable vehicles to reach these goals, although consolidation comes with significant baggage for the domestic Chinese and international markets alike.

Figure 4 — Chinese Rare Earth Mining and Smelting Production Quotas 2016-Present (MIIT)

Export Controls

Especially during earlier years in China’s rare earth industry, officials in Beijing often resorted to export controls as a means of managing domestic operations. Chinese export controls on rare earths have also been among the most highly controversial in the global mining community given China’s supply dominance.

Following the end of the export rebate regime, China introduced export quotas in 1999 to control total production and illegal activities at its borders and spur downstream expansion.[23]

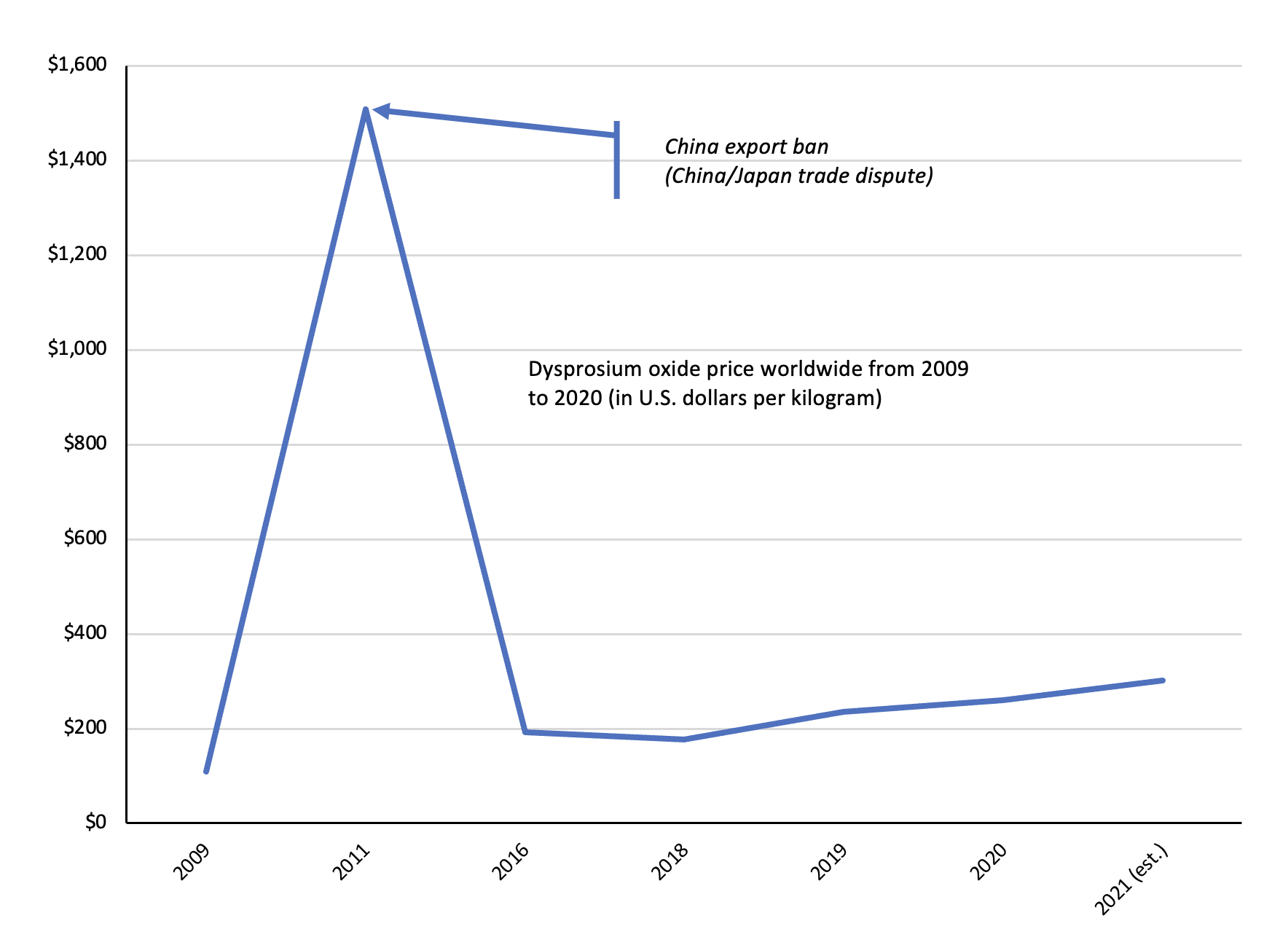

In 2010 Chinese customs officials halted REE shipments to Japan over a flare-up in the South China Sea spawned by territorial claims to the Spratly Islands (recognized as Japanese by international courts, but long claimed by the Chinese). Following this confrontation, the cost of REE skyrocketed. One of the immediate impacts was that Japanese petroleum refiners could no longer import catalysts from China. The Japanese government led negotiations with China to regain access to REE stockpiles, but the incident added to existing tensions in the region and triggered reactions worldwide.[24]

Figure 5 — Example of Price Effect from 2010 Export Ban – Dysprosium

In 2012, the U.S., EU and Japan filed a formal complaint to the WTO alleging that Beijing’s trade restrictions violated international trade rules and had to be removed.[25] In 2014, a WTO panel ruled that Chinese export restrictions were irregularities, and they were discontinued.[26] Following this, Chinese regulators opted for domestic-facing policies in attempts to reorganize the industry, which are more difficult for multinational organizations to challenge. For example, draft controls issued by the MIIT in January 2021 stated the applicability of the Export Control Law (ECL) to rare earth exports, which would be subject to more scrutiny and restrictive permitting from the state if fully adopted.[27] Chinese regulators also instituted a covert value added tax (VAT) rebate-upon-export scheme designed to incentivize downstream exports of products as opposed to ore. For example, rare earth permanent magnet exports receive a 13% VAT rebate equal to a full refund of China’s VAT. In contrast, rare earth concentrate exports do not receive a VAT rebate.[28] China’s bureaus review VAT rebate policies biannually and may change them according to the state’s industrial priorities, a tactic which arguably amounts to trade manipulation. This illustrates how China’s use of unconventional export controls are more difficult to observe and counter in multinational bodies like the WTO. As opposed to earlier export controls, which directly restricted trade, regulators have shifted to an approach based on increasing central oversight and a permitting regime that re-centralizes export licenses to SOEs more amenable to central coordination and enforcement efforts.

Consolidation

Historically, major top-down mergers and acquisitions have not been the primary means of consolidating the Chinese rare earth industry. Rather, the government favors a model dominated by few firms through more restrictive permitting, selective quota allocations and crackdowns on illicit mining activities. As a result, in the half century of the industry’s existence, rare earth enterprises have consolidated considerably. Six firms constitute 90% of China’s domestic operations.

The government has been urging consolidation since the publication of the “Several Opinions of the State Council on Promoting the Sustainable and Healthy Development of the Rare Earth Industry” and the “Situation and Policy of China’s Rare Earth Industry,” both issued by the State Council in 2011 and 2012, respectively.[29] According to these documents, eliminating duplicate projects, avoiding unnecessary competition among firms and achieving greater alignment with government priorities were the underlying motivations of consolidation.[30] Since the 2014 WTO decision, which removed export controls from their quivers, Chinese regulators have intensified their push for consolidation as a means of better managing the domestic industry.[31]

Prior to the 2021 consolidation, the six major rare earth SOEs were China Rare Earth Group Co., Xiamen Tungsten Co., Guangdong Rare Earth Industry Co., CHINALCO, Ganzhou Rare Earth Group and Minmetals Rare Earth Group Co. In previous consolidations, the “Big 6” SOEs absorbed smaller rare earth enterprises that were unable to compete in an environment with more stringent permitting requirements that favored the dominant firms.[32] The 2021 reorganization involved a deeper, strategic restructuring of the industry’s dominant players. The merger of three of the “Big 6” dominant SOEs (CHINALCO’s rare earths division, Minmetals and the southern division of China Rare Earth Group), along with other entities as we describe later, is rather atypical in the sense that it broke the structure of the six dominant pillars upholding the industry.

Barriers to Proper Resource Management

The subnational dynamics of resource endowment versus resource management create significant disruptions to efforts by the central government to control local production. Resource-rich areas in China, especially within the context of REE, typically have lower economic attainment than the coastal provinces. Exploiting REM and developing downstream capabilities emerged as “leverage” in the competition between localities and provinces. Coupled with a deep administrative bureaucracy that conceals rent-seeking behavior and “selective” enforcement by officials to the benefit of local miners, management gaps quickly and consistently emerge.[33]

The preponderance of illegal mining operations around China stands out as the most obvious effect of these dynamics. These miners, who account for upward of 40% of total REM output in China by some estimates, pose problems from a resource management perspective for several reasons. By design, these entities decrease the state’s ability to enforce production quotas, export controls and environmental regulations, making it difficult to align the broader rare earth industry with government priorities. In a more practical sense, illegal miners “seek the higher valued REE — especially the magnet materials neodymium, praseodymium, dysprosium and terbium — and simply dump onto the market the low-value elements regardless of price.”[34]

When they slip under the regulatory radar, illegal firms bypass several costly steps and gain an advantage over their legally sanctioned counterparts. They can circumvent major transactional costs associated with permitting as well as operational costs associated with tightening environmental and labor restrictions and rules. The more stringent the regulatory environment, the more costly it is for legal firms, which causes illegally sourced products to appear at a discount. These financial realities have a compounding effect, further incentivizing illegal production.

Highly pervasive illegal mining can turn the rare earth industry, or any business in any country, into a runaway train, from a regulatory standpoint. It is therefore not surprising that official crackdowns in China on illegal mining have intensified over the last decade. The most recent wave began in 2009 amid concerns that illegal production was causing prices to depress, along with intense environmental degradation.[35] Based on MIIT information, during the period of the 12th Five-Year Plan (2011-2015), regulators closed 14 REE mines and 28 companies, seized more than 36,000 tonnes of illegal rare earth products and imposed 230 million yuan in fines.[36] More recently, MIIT guidelines published in January 2019 indicated that efforts to eliminate illegal mining, production and smuggling of rare earth materials would be escalating.[37] This included establishing a traceability system to stop buyers from using illegal materials, under threat of suspending their licenses. The recent regulatory action suggests a focus on ridding the entirety of the rare earth supply chain of illegal REM.

Many experts agree that global demand for rare earth products will soon outpace supply.[38] As such, market participants should expect pressure from efforts to secure REE supply chains to influence prices and heighten the stakes of illegal mining. Bribes and local-level rent seeking will likely flow as lucrative contract opportunities arise with increasing frequency. Countering this pattern are desires by central state officials to use legal channels to capitalize on and capture price appreciation from increasing demand. Better yet for Chinese political interests would be to realize these gains through dominant SOEs that carry more oversight from both corporate — but ultimately political — administrators. In an era of widening value chains, greater supply flexibility comes at a premium. Thus, centralizing suppliers can be seen as an anti-resiliency measure.

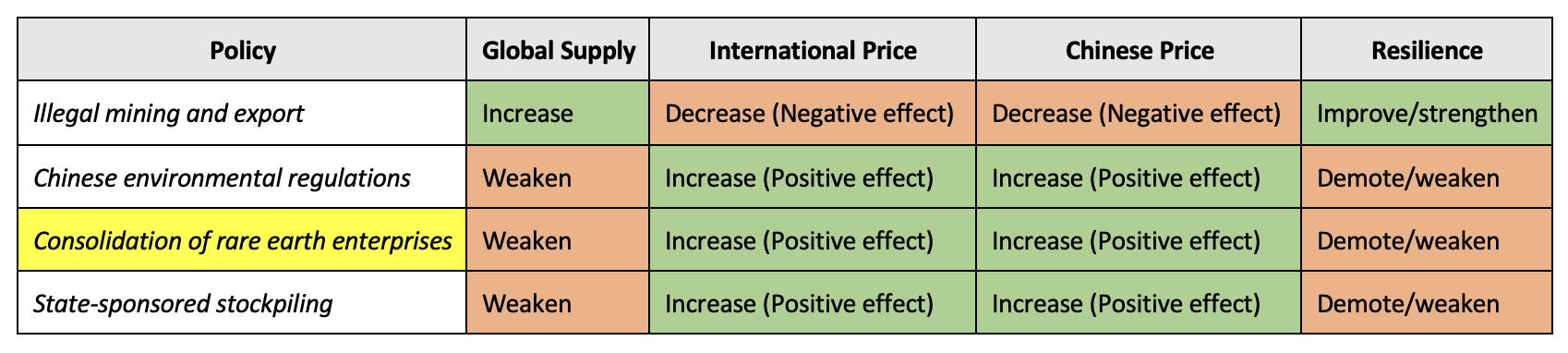

Table 1 — Dynamics Inside the Chinese Rare Earths Supply Chain

Analysis of Recent SOE Merger

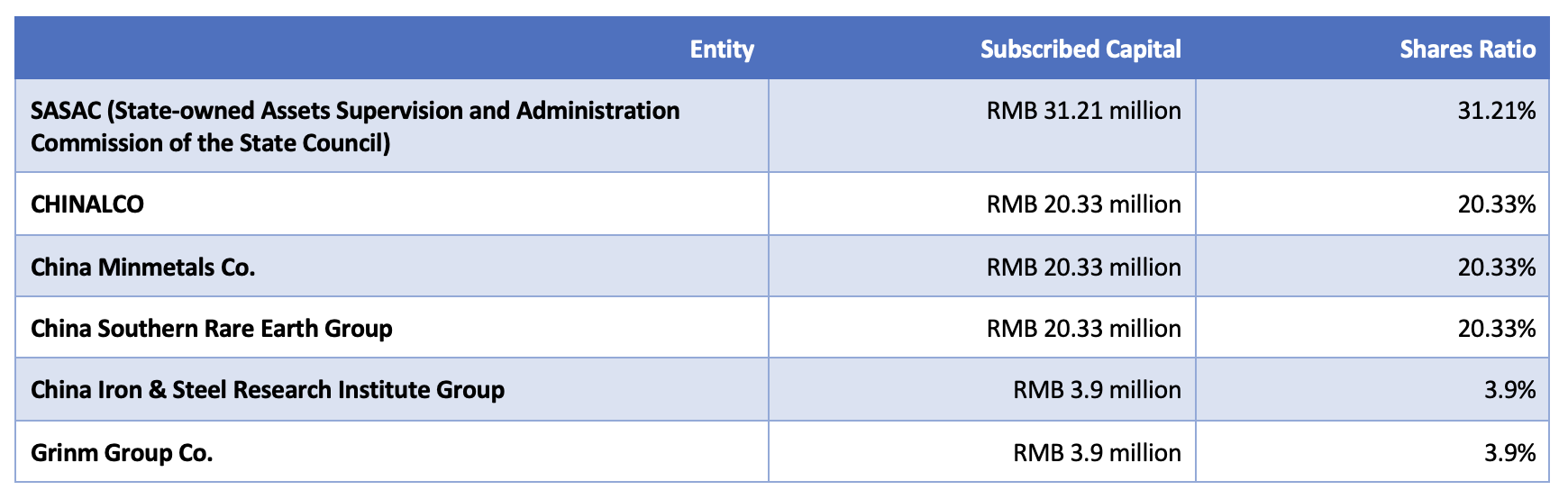

In sum, the creation of the China Rare Earth Group represents a major restructuring of Chinese global rare earth suppliers and manufacturers. The group is a merger of three of China’s “Big 6” SOEs and other associated entities: the rare earth arms of the Aluminum Corporation of China (CHINALCO), China Minmetals Corporation and China Southern Rare Earth Group, as well as research and development (R&D) firms China Iron & Steel Research Institute Group and Grinm Group.[40] The new mega-SOE reportedly will also include the Jiangxi Ganzhou Rare Metal Exchange, a bourse for spot transactions and Ganzhou Zhonglan Rare Earth New Material Technology Co.[41] The deliberately integrated operations of the China Rare Earth Group can be viewed as a direct challenge to the trend of China’s rare earth industry becoming less vertically integrated over recent years, and more reliant on expensive imports of foreign concentrate due to ever-deepening supply and demand imbalances.[42]

In contrast to preexisting operations of the three merged SOEs, China Rare Earth Group will exert control further down the value chain, from extraction to transaction. The same goes for the Chinese government’s ability to oversee operations, as opposed to the limitations faced by state central planners and overseers when the previous six-firm field existed. The ownership structure of the new firm is laid out in Table 2.

Table 2 — China Rare Earth Group Ownership Structure

Filings to the Shenzhen Stock Exchange in September 2021 suggest Minmetals (whose parent company is the SASAC) initiated the restructuring of its rare earth assets with assets from Chinalco and China Southern (of which the city of Ganzhou holds a 94% stake).[44] This suggests that the merger was driven top-down from Beijing, first and foremost, and expedited by opportunistic local officials.[45] China Rare Earth Group will be headquartered in Ganzhou, Jiangxi province, home to two of the three combined rare earth SOEs and also considered a perennial hub for rare earth smelting, separation and processing. From a compliance standpoint, it is crucial that the headquarters remain local to operations, so that localities hosting rare earth projects from the firm retain a vested interest in the project’s success and alignment with central priorities.

From the little public information available, the leadership structure of China Rare Earth Group suggests that the merged firms will share control in a relatively balanced manner and be aligned closely with central government authorities. According to reported information, the chairman of the new SOE will be Ao Hong, deputy party boss of CHINALCO, while Liu Leiyun, chairman of the Minmetals Rare Earth arm, was named chairman of the group.[46] The link between Minmetals leadership and the SASAC is worth mentioning because of the former’s role in initiating the merger. The chairman of Minmetals, Weng Zuliang, is also the secretary of the Leading Party Members Group (LPMG) of the SASAC, and the CEO of Minmetals, Guo Wenching, is the deputy of the LPMG.[47] Wenching, formerly the chairman of MMG Ltd., left his position to focus on other duties as president of the China Metallurgical Group Corporation, one of the largest subsidiaries of Minmetals.[48] In a show of alignment with central priorities, in January 2022 Minmetals held a symposium celebrating the one-year anniversary of President Xi Jinping’s speech on his visit to the Yanqing Sliding Centre.[49] Weng Zuliang and Guo Wenqing attended, and the former delivered a speech underscoring the importance of “maintaining a high degree of consistency with the decisions of General Secretary Xi Jinping.”[50] As leadership structures within the China Rare Earth Group Co. continue to develop, the entity’s relationship with regulators will become clearer. The baseline, however, appears to be strong ideological and regulatory alignment.

On the other side of this partnership, key personalities are rotating in and out as well. Most recently, Jin Zhuanglong, a veteran of the aerospace industry, became the head of the MIIT after the former chief of the ministry was sacked in August 2022 on corruption charges.[51]

With the establishment of China Rare Earth Group Co., China can further entrench itself as a strategic provider of REE to the world. Industry experts estimate the company alone will account for approximately 62% of China’s medium-heavy REE supplies (with enhanced pricing over dysprosium and terbium).[52] Relative to production quotas allocated under a system of six dominant rare earth SOEs, the China Rare Earth Group received a slightly reduced slice of production and smelting quotas as compared to the sum of the three merged entities.[53] The SASAC thus increased its capacity to oversee the operations of almost half of the country’s production, by virtue of their ownership stake in the new entity.

Taken against the backdrop of previous attempts by the Chinese government to oversee rare earth production, the recent merger is another chapter in the industry’s rather turbulent history. We expect that REE assets of the remaining three ‘Big Six’ firms will become the northern counterpart to the China Rare Earth Group Co. This would continue the shift from a scattered to a more centralized and coordinated mining ecosystem that aims to “optimize resources, ensure supply security, and enforce stricter rules” relating to production and exports of REE.[54] China’s reforms are primarily aimed at enhancing the REE industry’s efficiency by better balancing the tension between industry growth and sustainability, and to crack down on illegal mining.[55] With an eye to demand growth for permanent magnets, China intends to dominate the REE chain from exploration and product application to inspection and end-use design.[56]

Politically speaking, managers from the central government have long grappled with local regulators for oversight and genuine enforcement of Beijing’s industrial policies relevant to rare earth enterprises. The creation of the China Rare Earth Group SOE is the most recent step in a decades-long strategy to consolidate domestic REE production into two major firms: one in the north (controlling light REE), and one in the south (controlling medium-heavy REE).[57] As we noted earlier, forced consolidation is a proven means of cutting down on illegal mining and exports, as well as “selective” enforcement by local officials.

From a commercial perspective, the state’s intent with the merger is to decrease price-based low-end competition in order to safeguard the asset value of rare earths, especially as global competitors develop their own rare earth industries.[58] According to the head of the SASAC, their aim is to integrate upstream resources, increase pricing power and use rare earths to the country’s strategic advantage.[59] In their efforts to influence prices of REM, Chinese officials must toe a fine line. On one hand, REM must remain affordable for the domestic market. On the other, much of the industry’s revenue (and state revenue from value-based taxes) is highly dependent on elevated international REM prices. In the past, Chinese officials have expressed concerns about depressed prices and likely retain the same outlook. While the domestic and international prices of rare earths are distinct, the latter inflated by higher licensing costs and taxes, policies affecting the rare earth industry in China would have a significant and parallel effect on both. By virtue of the China Rare Earth Group’s pricing power, officials will have greater influence over pricing and may stabilize and further bifurcate the domestic and international REM prices according to their industrial priorities.

Geopolitical Implications

U.S. dependence on China for REE and downstream rare earth products is especially strong, as very little REE mining and magnet production and none of the REE processing is done in the U.S. To mitigate China’s stranglehold on the rare earth industry, the U.S. industry and policymakers face the challenge of developing a domestic rare earth ecosystem — from extraction to midstream processing to further downstream manufacturing. China currently is the only country in the world with a fully integrated permanent magnet supply chain. In total, Chinese production accounts for approximately 58% of rare earth mining, 89% of rare earth separation, 90% of metallization and 92% of NdFeB global markets.[60]

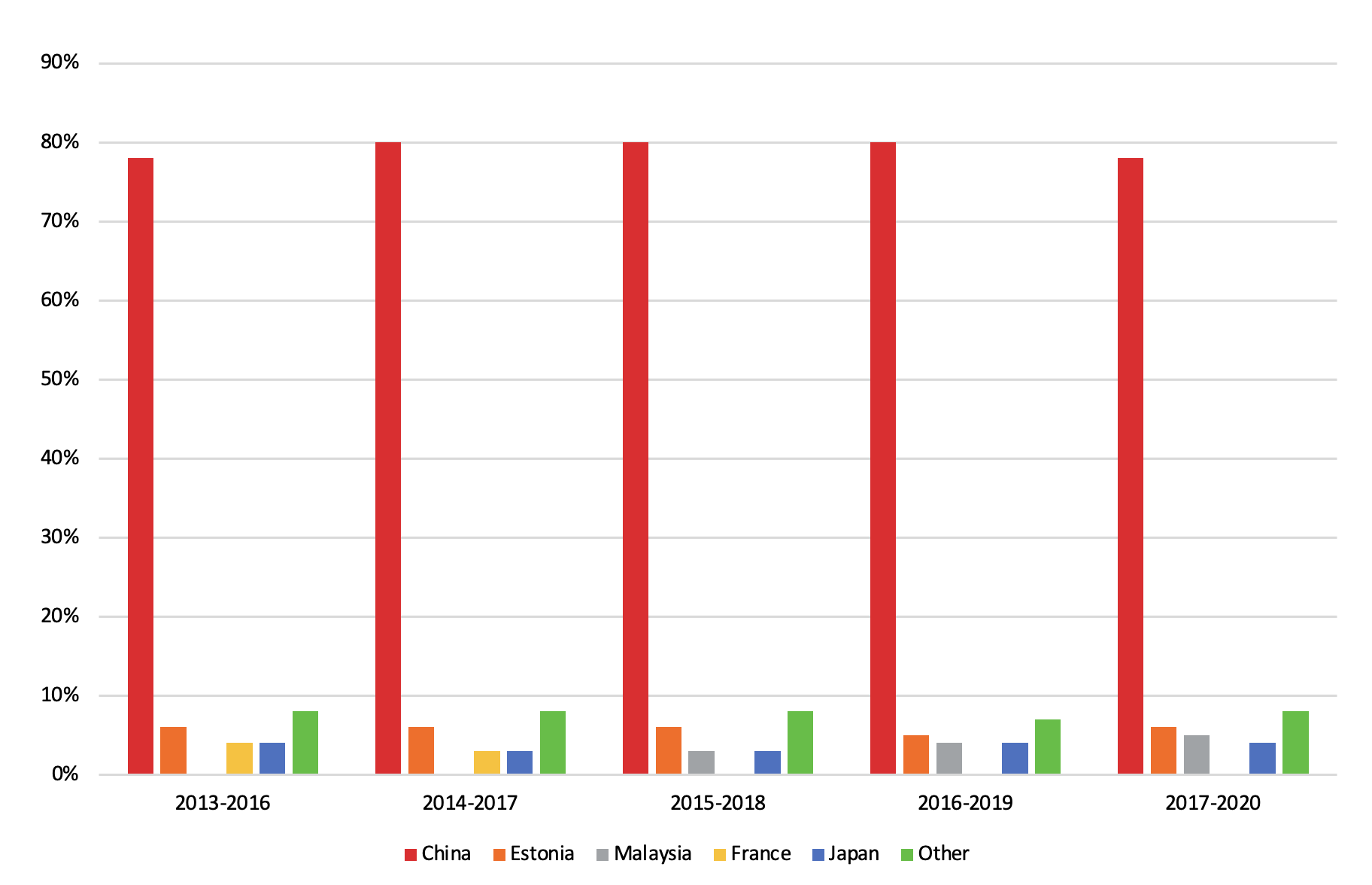

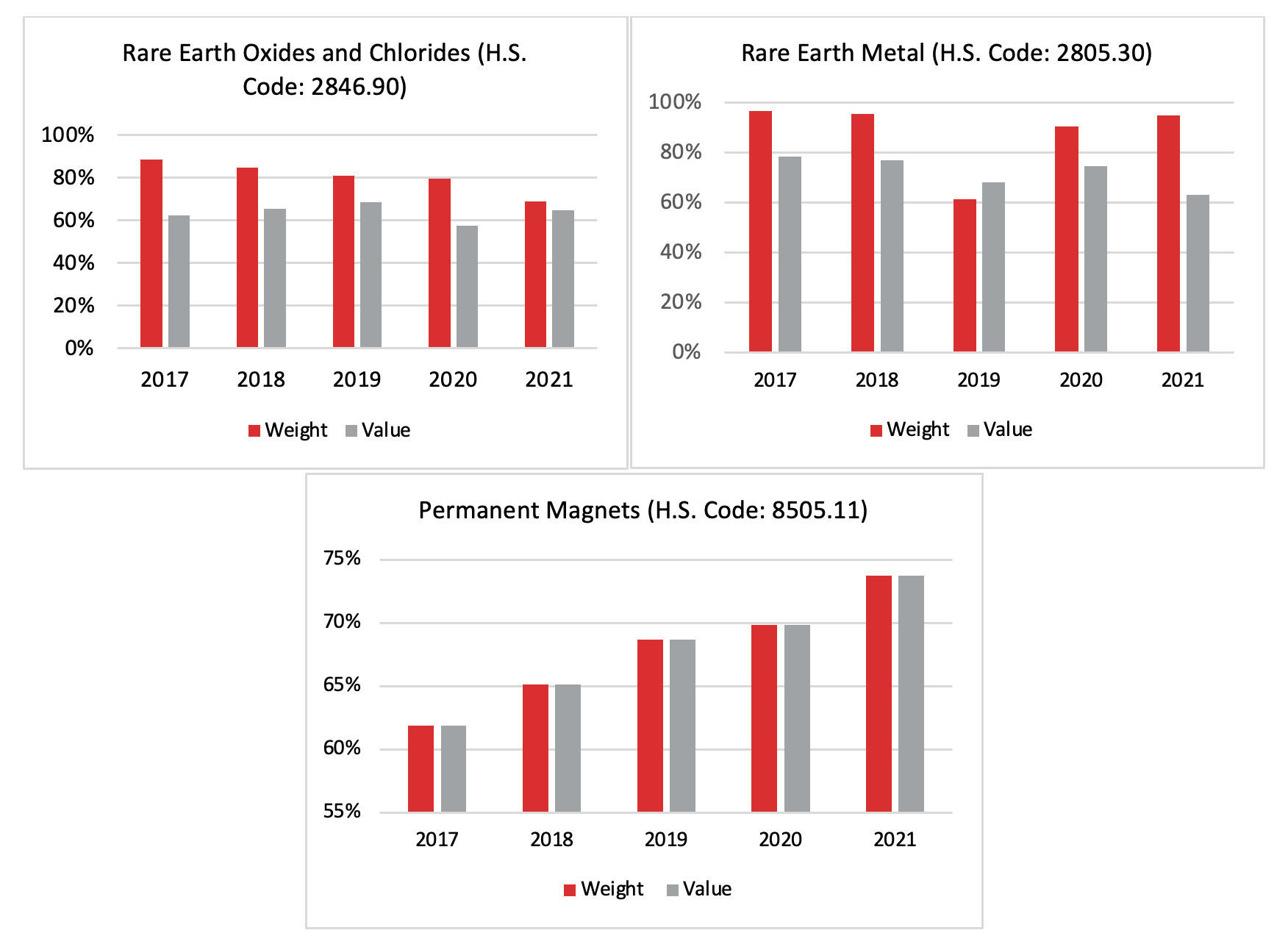

Figure 6 and Figure 7 detail U.S. imports of various products along rare earth permanent magnet value chains, with slight variance due to the differing data collection methodologies between the U.N. Comtrade and the United States Geological Survey. It is important to note that these figures do not take into account rare earth products integrated directly into goods further downstream before they are imported into the U.S. For example, these figures do not account for rare earth magnets manufactured in China and integrated into Chinese-made smart phones that are then exported to the U.S. Therefore, American commercial reliance on Chinese rare earth products is likely significantly understated.

Figure 6 — China’s Share of U.S. Rare Earth Metal Imports

Figure 7 — China as a Percent of Total U.S. Imports

Besides China, the U.S. imports REE from Estonia, France and Japan, but these flows are misleading. In fact, Estonia procures its rare earth feedstocks from Russia, while France and Japan are simply processing links with no domestic mine production of their own, using feedstocks of mixed sources including China and Russia. Because U.S. allies in Europe and Japan currently only possess downstream manufacturing capabilities with no mining output, potential supply disruptions from China could affect allied supplies of downstream rare earth products.

Currently the only domestic producer is MP Materials from its Mountain Pass facility in California (at the edge of the Mohave Desert), which primarily supplies light REE, though there is a planned expansion into heavy REE processing as well as metal conversion, alloying, and magnet manufacturing in their new facility in Fort Worth, Texas.[61] Mountain Pass sends the 42,000 tonnes of REO contained in the concentrate it produces to China for further processing due, in part, to the absence of domestic customers. The company is actively upgrading processing assets on-site as it moves to integrate further down the rare earths value chain.[62] Additionally, Noveon (formerly known as the Urban Mining Company), the only operational U.S.-based permanent magnet manufacturer, produces a small amount of NdFeB permanent magnets.

Besides MP Materials, there are other American enterprises working to develop the domestic rare earth industry. The Texas Mineral Resources Corporation (TMRC) is actively working to develop a rare earth project at Round Top in South Texas, which looks to extract light and heavy REE to be processed on-site.[63] According to the company’s site, the project is still in extremely early stages, as TMRC is still “focused on the exploration and development” of their deposit.[64] Developing domestic separation and other processing capabilities on-site simultaneously cuts down logistical costs and will chip away at China’s current dominance of entire global rare earth value chains.

While the second coming of the U.S. rare earth industry is still in its early stages, this burgeoning activity is encouraging. Still, permitting challenges as well as scaling up to sizeable domestic production and processing will take a good deal of time. For the necessary industrial rare earth cluster to develop, nodes all along rare earth supply chains must develop simultaneously, so they can be pieced together once fully operational. The current high prices of rare earths are conducive to developing the rare earth industry. However, in the event of depressed prices, due either to typical price fluctuations or to Chinese price manipulation, U.S. policymakers must look to other means to encourage development.

Chinese officials are highly conscious of the geopolitical advantage they derive from their REE dominance. The 2010 incident over REE shipments to Japan was a wake-up call to import-dependent customers. Almost a decade later in 2019, threats of restricted supply returned.[65] Xi’s visit to a REE magnet production facility in Ganzhou in 2019 was widely regarded as a sign that restricting REE supply is on the table.[66] A week later, the People’s Daily posted an article explicitly threatening that if “the U.S. side wants to use the products made by China’s exported rare earths to counter and suppress China’s development,” the U.S. should not “underestimate the Chinese side’s ability to safeguard its development rights and interests.”[67] The more recent MIIT draft controls list proposed in January 2021 also suggests that international policy responses significantly influence Chinese domestic policies toward rare earths.[68] Officials in Beijing are particularly focused on how quickly the U.S. would secure alternatives if REE were included on the control list.

Therein lies a paradox: China’s state-supported rare earth enterprises remain at the behest of international market dynamics. Overburdening policy changes and perceived supply insecurity would push buyers away from Chinese suppliers. Any restrictive moves would likely spur proactive value chain restructuring away from Chinese REE. Therefore, Chinese officials would be unlikely to directly restrict trade for political reasons and calls for such are primarily just sword rattling to disguise domestic policies and production controls that bear a more long-term effect on supply coming out of China.

Considering the recent flare-up in U.S.-China tensions over Taiwan, occurring against the backdrop of global turmoil caused by Russia’s invasion of Ukraine, it is important to note that the current dynamics over rare earth trading would not hold in the event of China’s invasion of the island. Will Chinese rare earth enterprises’ responses resemble those of Russia’s Gazprom in the first half of 2022, a game of limbo to balance their own revenue with geopolitical bridge-burning? Or will China act swiftly to cut off rare earth supplies to its adversaries given their end-use applications for defense technologies that maintain U.S. military technological superiority? How would these actions carry across to other alliances such as the North Atlantic Treaty Organization and member countries? China’s deep economic integration with the West suggests that any decisions to alter trade will carry heavy implications for all involved. As a result, their response will be highly dependent on the level of support, especially militarily, that the U.S. and its allies give to Taiwan. In any case, as Chinese officials continue to consolidate the major rare earth SOEs, they gain greater control over the industry and more leverage in their ever-evolving power plays with the West.

The U.S. Policy Response

Key government initiatives in the U.S. are worth highlighting for their focus on developing domestic rare earth capabilities. Only relatively recently did U.S. policymakers start to pay attention to the intersection between geopolitics and market dynamics in the REE industry — primarily starting during the Trump era. In July 2019, then President Trump made a series of presidential determinations (PDs) under Section 303 of the Defense Production Act of 1950 (DPA) that domestic production, separation and manufacturing of rare earths is “essential to the national defense” of the United States.[69] These designations freed up funding from the Department of Defense (DOD) to pursue increased production. On February 24, 2021, President Biden signed Executive Order 14017 on Securing America’s Supply Chains, which requires the secretary of defense to submit a report identifying risks in critical minerals supply chains, including REE, and policy recommendations to address these risks.[70]

Title III of the DPA, which is dedicated to ensuring the timely availability of essential domestic industrial resources, can help buttress domestic rare earth industrial development.[71] Funding from the DPA is essential to sustaining capital flows to highly intensive rare earth extraction and processing projects. In addition, support from the DPA is seen as a signal of legitimacy for projects and companies, from a security and business standpoint, which can spur supplemental investment.

Pursuant to the PDs on rare earth permanent magnet supply chains, the DPA Title III program has issued several awards. Under the PD covering light rare earth separation, the DOD awarded Australia’s Lynas Corp an investment worth $30 million in February 2021 to establish U.S.-based processing capabilities for light REM.[72] The facility will be located in Hondo, Texas, as part of partnership with San Antonio’s Blue Line Corporation. The DOD also awarded $10 million to MP Materials to upgrade their on-site rare earth separation assets and a $35 million contract to MP Materials Corp in February 2022 to design and build a heavy REM processing facility in Mountain Pass. This falls under the PD covering medium and heavy rare earth separation and processing, with the end goal of producing permanent magnets domestically.[73] Additionally, the DOD granted $30 million to Noveon to expand NdFeB magnet production, under the PD for NdFeB production. The DPA has not yet made awards to address the remaining PDs on rare earth metal reduction and alloy processing, or on samarium-cobalt rare earth permanent magnet production.

While these steps are encouraging, many investments are in extremely early stages, and it will likely take several years to deliver products to markets with an unspecified projected demand. With these actions in mind, during the recently concluded Section 232 investigation on the “Effect of Imports of NdFeB Permanent Magnets on the National Security,” the Department of Commerce found that current capacity development may satisfy 51% of domestic direct NdFeB demand, under current projections that are set to increase, due primarily to alternative energy applications such as wind power and battery electric powertrains, which make intensive use of permanent magnets. Moreover, it remains to be seen whether REE production outside of China can compete with their unparalleled low-cost structure.[74] We note that the issue of cost to “reshore” or “friend-shore” critical raw materials and components, as represented by the Lynas procurement, represents an enormous uncertainty in outlooks, ultimately affecting the affordability of many technologies and products deemed essential for energy applications and defense systems well into the future.

The 117th Congress is also focusing on developing domestic rare earths. The CHIPS (Creating Helpful Incentives to Produce Semiconductors) and Science Act of 2022 and the Inflation Reduction Act, passed in late July and early August 2022, respectively, include provisions designed to better commercialize American rare earths. Legislative highlights include tax refunds on production costs, increased funding authority for R&D grants and further increases to DPA funding.

For the U.S. to secure a sustainable rare earth supply chain, rare earth processing and manufacturing technologies must be commercially viable. Herein lies the U.S. government’s main role: mitigating China’s non-market approach that is causing U.S. and allied rare earth industries to hollow out in favor of subsidized and incentivized operations in China. This requires a meticulous approach, utilizing public funding as a jumping-off point for a rebounding domestic rare earth industry rather than a long-term funding scheme that more closely resembles the Chinese command-economic approach. Funding opportunities like the recent DOE-directed grant for rare earth processing from industrial by-products, which holds little commercial potential, should not be regarded as viable industrial strategies for the industry as a whole.[75] While it is worthwhile to explore various avenues to secure a domestic rare earth value chain, more funding should be directed toward advanced novel capabilities that do not play into the Chinese industrial stronghold, given the latter’s dominance of legacy technologies.

In the quest to compete with Chinese rare earth producers’ low-cost structures, a slippery slope will likely emerge in cost-cutting efforts. These same dynamics contributed to the Mountain Pass mine’s closure in 2002 due to a tailings pipeline discharge of thorium under the supervision of the previous owner, Molycorp Minerals, LLC.[76] Where regulatory ambiguities and logistical loopholes exist to circumvent higher-cost sustainable resource management, domestic miners must consider the long-term consequences of these decisions, which can easily ruin promising projects while endangering the surrounding communities and environment in the process.

While long-term supply resilience is a goal, “industrial planners” must proactively mitigate the risks of immediate rare earth product supply disruptions from China. Manufacturers and designers may opt to use REE substitutes, but substitutes do not perform nearly as well.[77] Designers looking to shift away from China-dominated REE may face the task of engineering their products without these materials as the more viable alternative. Recycling offers possibilities, especially from permanent magnets, but a long path lies ahead for this to become viable. Recycling too often is overstated given the outlook for raw materials requirements. Recyclers face the same delays and conundrums in achieving regulatory reviews and permits to move forward as mining and other industrial projects.

Rare earths occur with phosphates in the U.S., which could become a potentially alluring option.[78] Phosphates are extracted for a variety of uses and are of interest for developing a competing battery chemistry (lithium-iron-phosphate or LFP[79]). However, phosphates and REE-containing minerals in sands deposits also bear the radioactive elements thorium and uranium. This presents a persistent dilemma since existing U.S. regulations limit the extraction of these radioactive elements and thereby discourage the pursuit of REE.[80] REE can be harvested from other sources, such as agricultural wastes, and could be captured from deepwater seabeds, affording an exploration frontier. Overall, however, REE exist within an inadequate framework for nonfuel minerals — especially given how critical they are to both legacy and alternative energy technologies, much less non-energy and defense uses.

The U.S. government, of course, has its own part to play. First, strategic planners must honestly distinguish rare earth demand for defense and other strategic purposes from non-strategic demand. While both strategic and non-strategic demand must be balanced in order to stabilize supply, delivery delays for defense purposes carry significant implications for combat readiness, especially in an era of heightened major-power tension. It is also crucial that the U.S. government ensure its strategic stockpiles of REE are filled to aid in these efforts.

Conclusion

The recent merger that created the China Rare Earth Group is a major development for the global rare earth industry. It is the most recent chapter in the Chinese government’s efforts to quell an industry that has been unruly at times. Given that Chinese efforts to directly control exports have been blocked by bodies like the WTO, officials are now opting for domestically oriented policies to manage the industry. The merger of China’s largest rare earths operators is the most recent iteration of decades of forced industrial consolidation meant to cut down on inefficiencies and increase central oversight. These internally facing policies, which carry significant consequences for global REE industries, are more difficult to challenge in international dispute systems than their externally-facing precursors.

Through the reorganization, Chinese regulators can better enforce central policies and mitigate friction with local officials who often encourage and permit rare earth production counter to central regulations. From China’s perspective, consolidation is a means to produce rare earths in a more sustainable fashion by deploying more uniform production and environmental practices, as well as reducing speculative capital flows that increase domestic rare earth prices in China. Greater oversight from the SASAC over the China Rare Earth Group creates more leverage for Beijing’s officials to influence prices by further bifurcating the domestic and international prices of rare earth products and stabilizing the former. It is also likely that demand will increase, propelled by China’s goals to increase alternative energy and defense capacity. Thus, we anticipate this merger will not be the last and that China’s leaders will eventually fold the remaining three northern rare earth SOEs into their own mega-conglomerate, absent any significant deviations in industrial ideology.

Two geopolitical dynamics properly contextualize the risks associated with China’s REE dominance: 1) Chinese tensions with the U.S. and its allies over trade and 2) Chinese positioning on Taiwan.[81] Given China’s REE dominance as a stable global supplier, would Chinese officials self-sabotage during periods of relative peace, pushing Western countries to develop alternatives proactively? Indeed, despite aggressive posturing and threats from Chinese officials and tabloids, China has yet to restrict REE exports as leverage in its trade war with the United States. Aggression toward Taiwan would likely be a completely different story, especially if the U.S. provides military equipment or combat support to Taiwan. With more centralized state oversight and a leadership structure more amenable to central coordination, the China Rare Earth Group increases the state’s ability to influence and possibly even restrict rare earth exports for political reasons.

Whether China would weaponize their leverage over rare earth supply chains in direct conflicts with the U.S. and/or its allies is a matter of speculation and debate. However, one thing is for sure: In such an event, the U.S. must minimize China’s ability to limit sanctions and other collective global responses against potential coercive action. Taking the invasion of Ukraine as an example, Russia’s VSMPO-Avisma’s strong positioning as the leading global aerospace-grade titanium supplier caused several EU member states to oppose sanctions on the company, despite its role in maintaining Moscow’s force posture.[82] In order to respond adequately to Chinese military belligerence, the U.S. must ensure that China’s consolidated rare earth industry does not grant Beijing undue influence over an international response. The U.S. and its allies must act accordingly to divorce their strategic industries from Chinese rare earths.

As a result of these dynamics, U.S. government officials are under pressure to take significant steps. They must mitigate short- and medium-term supply risks from potential disruptions in Chinese supply and simultaneously take a long-term approach to developing a domestic rare earths ecosystem. The former relies more on filling strategic stockpiles, securing alternative supplies from allied countries like Australia and decreasing product reliance on rare earths from an engineering standpoint where possible. The latter involves a more holistic approach of bolstering several nodes along rare earths value chains simultaneously (so they can be connected once fully operational) and involving foreign capital in these efforts when the opportunities present. Private-sector and government funding from allies like Australia, Japan and South Korea can be used to develop “friendly” rare earth supply chains with more secure supply. However, the United States’ sole reliance on allies to correct domestic industrial deficiencies in rare earths would not provide the more robust REE supply chains that are envisioned.

Through congressional authority and executive branch vehicles, the U.S. government can continue to focus on commercializing American rare earths from extraction to downstream manufacturing. R&D funding could focus on several key issues including more efficient and sustainable extraction from commercial and environmental standpoints and more flexible processing to accommodate broad ranges of mineral feedstocks. Here, developments in continuous ion exchange (CIX), RapidSX (and advancement beyond traditional solvent extraction methods) and other separation processes are encouraging, given rare earth deposits typically coincide with deposits of other critical minerals.[83] Through tax breaks and other cost-assistive policies, the U.S. government can also better commercialize domestic rare earth production and chip away at China’s dominance and their non-market approaches to managing the rare earth industry.

A nuanced approach to tariffs may also be in order. China’s trade manipulation (in the form of VAT export rebates that fluctuate based on state industrial priorities) makes non-Chinese rare earth producers less cost effective. Tariffs imposed via Section 203 or 301 investigations can mitigate this gap, but doing so would likely paralyze U.S. industries that are highly dependent on rare earths, especially in the technology sector.[84] The recent determination by the Department of Commerce (DOC), pursuant to a 270-day Section 232 investigation, found that NdFeB imports from China present significant national security risks. However, because of virtually nonexistent domestic NdFeB supply and other holes in the value chain, the DOC’s hands were tied, and they did not institute tariffs on imports. As supply disruptions from China come closer to becoming a reality, it will become increasingly important to regain this element of trade leverage as well as supply independence, in the event of a stoppage in Chinese NdFeB exports. Instituting tariffs on NdFeB imports from China would only be viable once rare earth ecosystems in the U.S. and allied countries mature considerably. Whatever the policy choices may be, regulators in the U.S. must portray a sense of stability and focus in order to increase investor confidence in its burgeoning rare earth industry.

Ultimately, U.S. government and industry decision-makers will face the challenge of winning U.S. voter and taxpayer support for more assertive raw materials supply chain strategies and policies. To make the case, political actors and industry representatives must provide clear definitions of needs and priorities and, as we suggested earlier, be prepared to abandon some non-strategic aspirations, in particular non-defense uses including, perhaps, those linked to alternative energy mandates and subsidies. In the end, it is not certain that voters will accept the burden of “de-risking” a broad swath of raw materials and technology-oriented industrial policies. Defense planners, in particular, must be ready to deal with those outcomes.

Acknowledgements

The authors are grateful for the continued support of this research from Rice University’s Baker Institute for Public Policy, the Center for Energy Studies (CES) and the CES Energy, Minerals & Materials (EMM) program. Jacob Koelsch initiated work on this paper while serving as a research intern for CES/EMM and completed it after joining J.A. Green & Company (JAG). The authors received no information or input from JAG.

Endnotes

[1] Keith Zhai, “China Set to Create New State-Owned Rare-Earths Giant,” Wall Street Journal, December 3, 2021, https://www.wsj.com/articles/china-set-to-create-new-state-owned-rare-earths-giant-11638545586.

[2] Shunsuke Tabeta, “China to Create Rare-Earths Giant By Joining Three State Companies,” Nikkei Asia, October 24, 2021, https://asia.nikkei.com/Economy/China-to-create-rare-earths-giant-by-joining-three-state-companies.

[3] Note that conformity in this report is as follows: general use of terms rare earths and rare earth elements as REE; rare earth oxides as REO; rare earth metals as REM.

[4] See National Minerals Information Center, “Rare Earth Statistics and Information,” U.S. Geological Survey, https://www.usgs.gov/centers/national-minerals-information-center/rare-earths-statistics-and-information.

[5] “Rare Earth Elements in National Defense: Background, Oversight Issues, and Options for Congress,” Congressional Research Service, December 23, 2013, https://bit.ly/3UZ3baP.

[6] “Explainer: China’s Rare Earth Supplies Could be Vital Bargaining Chip in U.S. Trade War,” Reuters, May 30, 2019, https://www.reuters.com/article/us-usa-china-rareearth-explainer/explainer-chinas-rare-earth-supplies-could-be-vital-bargaining-chip-in-u-s-trade-war-idUSKCN1T00EK; "Rare Earth Elements Supply Chain- Snapshot," Texas Comptroller, 2021,

https://comptroller.texas.gov/economy/economic-data/supply-chain/2021/rare-earth.php.

[7] The Effects of Imports of Neodymium-Iron-Boron (NdFeB) Permanent Magnets on the National Security, U.S. Department of Commerce, 2022, https://www.bis.doc.gov/index.php/documents/section-232-investigations/3141-report-1/file

[8] Li Xuanmin, “China Plans World-Class Rare-Earth Cluster in Xiongan New Area,” Global Times, June 19, 2019, https://www.globaltimes.cn/content/1154879.shtml.

[9] Ross Embleton and David Merriman, “Rare Earth Elements: Frequently Asked Questions,” Wood Mackenzie, October 1, 2021, https://www.woodmac.com/news/editorial/rare-earth-elements-frequently-asked-questions/#content.

[10] Damien Ma and Joshua Henderson, “The Impermanence of Permanent Magnets: A Case Study on Industry, Chinese Production, and Supply Constraints,” Macro Polo, November 16, 2021, https://macropolo.org/analysis/permanent-magnets-case-study-industry-chinese-production-supply/; Braeton J. Smith et al., “Rare Earth Permanent Magnets,” U.S. Department of Energy, February 24, 2022, https://www.energy.gov/sites/default/files/2022-02/Neodymium%20Magnets%20Supply%20Chain%20Report%20-%20Final.pdf.

[11] Cristian Tangemann, “Developing Electric Motors Less Dependable on Rare Earth Magnets,” Automotive IQ, January 22, 2020, https://www.automotive-iq.com/electrics-electronics/articles/developing-electric-motors-less-dependable-on-rare-earth-magnets.

[12] “China sets limit on annual rare earth mining volume by 2020,” The State Council, The People’s Republic of China, October 18, 2016, https://bit.ly/3FQJNrX; Smith et al., “Rare Earth Permanent Magnets.”

[13] “Does China Pose a Threat to Global Rare Earth Supply Chains?” Center for Strategic International Studies, n.d., https://chinapower.csis.org/china-rare-earths/.

[14] “Mining the Future: How China is Set to Dominate the Next Industrial Revolution,” Foreign Policy, May 1, 2019, https://foreignpolicy.com/2019/05/01/mining-the-future-china-critical-minerals-metals/.

[15] Pui-Kwan Tse, “China’s Rare Earth Industry,” U.S. Geological Survey, 2011, https://pubs.usgs.gov/of/2011/1042/of2011-1042.pdf.

[16] Ben Murphy, “Outline of the People’s Republic of China 14th Five-Year Plan for National Economic and Social Development and Long Range Objectives for 2035,” Center for Security and Emerging Technology, May 12, 2021, https://cset.georgetown.edu/wp-content/uploads/t0284_14th_Five_Year_Plan_EN.pdf.

[17] Yuzhou Shen, Ruthann Moomy, and Roderick G. Eggert, “China’s Public Policies Toward Rare Earths, 1975-2018,” Mineral Economics 33 (January 2020): 130, https://doi.org/10.1007/s13563-019-00214-2.

[18] Tangemann, “Developing Electric Motors Less Dependable on Rare Earth Magnets.”

[19] Ma and Henderson, “The Impermanence of Permanent Magnets.”

[20] Daniel J. Packey and Dudley Kingsnorth, “The Impact of Unregulated Ionic Clay Rare Earth Mining in China,” Resources Policy 48 (June 2016): 112-116, https://doi.org/10.1016/j.resourpol.2016.03.003.

[21] Siyi Liu and Dominique Patton, “China Hikes 2022 Rare Earth Quota by 25% On Rising Demand,” Reuters, August 17, 2022, https://www.reuters.com/article/china-rareearths-quotas/update-1-china-hikes-2022-rare-earth-quota-by-25-on-rising-demand-idUKL1N2ZT0I4.

[22] Data sources for Figure 4 are: 2016 H1 to 2021 H1 from https://www.reuters.com/article/us-china-rareearth-idUSKBN2AJ18O; 2021 H2 from https://www.globaltimes.cn/page/202201/1250199.shtml; 2022 H1 from https://www.globaltimes.cn/page/202201/1250199.shtml; 2022 H2 from https://www.mining.com/web/china-hikes-2022-rare-earth-quota-by-25-on-rising-demand/.

[23] Tangemann, “Developing Electric Motors Less Dependable on Rare Earth Magnets.”

[24] Based on discussions by lead author M. Michot Foss with Japanese representatives from Ministry of Energy, Trade and Industry (METI) during October 2010.

[25] Doug Palmer and Sebastian Moffett, “U.S., EU, Japan Take On China at WTO Over Rare Earths,” Reuters, March 13, 2012, https://www.reuters.com/article/us-china-trade-eu/u-s-eu-japan-take-on-china-at-wto-over-rare-earths-idUSBRE82C0JU20120313.

[26] “WTO Confirms China’s Export Restrictions On Rare Earths and Other Raw Materials Incompatible With WTO Rules,” European Commission, March 26, 2014, https://ec.europa.eu/commission/presscorner/detail/en/MEMO_14_236.

[27] Sofia Baruzzi, “China’s Export Control Law Explained,” Dezan Shira & Associates, November 9, 2020, https://www.china-briefing.com/news/chinas-export-control-law-explainer-china-briefing-news/.

[28] VAT rebate rates accessed using http://hd.chinatax.gov.cn/nszx/InitChukou.html.

[29] “Several Opinions of the State Council on Promoting the Sustainable and Healthy Development of Rare Earth Industry,” Law Info China, May 10, 2011, http://www.lawinfochina.com/display.aspx?lib=law&id=8741&CGid=; “Situation and Policies of China’s Rare Earth Industry,” Foreign Languages Press Co., June 2012, https://bit.ly/3V18XIO.

[30] Ma and Henderson, “The Impermanence of Permanent Magnets.”

[31] Tangemann, “Developing Electric Motors Less Dependable on Rare Earth Magnets.”

[32] “China’s Rare Earth Consolidation To Cut Supplies,” Argus Media, January 21, 2020, https://www.argusmedia.com/en/news/2054597-chinas-rare-earth-consolidation-to-cut-supplies.

[33] Tangemann, “Developing Electric Motors Less Dependable on Rare Earth Magnets.”

[34] Shen, Moomy, and Eggert, “China’s public policies toward rare earths, 1975–2018.”

[35] “China to Step Up Crackdown on Rare Earth Sector: Ministry,” Reuters, January 4, 2019, https://www.reuters.com/article/us-china-rareearths/china-to-step-up-crackdown-on-rare-earth-sector-ministry-idUSKCN1OY0R3.

[36] “China Sets Limit On Annual Rare Earth Mining Volume By 2020,” Xinhua News Agency, October 18, 2016, https://bit.ly/3FQJNrX.

[37] Baruzzi, “China’s Export Control Law Explained.”

[38] Jacqueline Holman, “Rare Earth Element Prices to Remain Strong as Demand Exceeds Supply: Ionic,” S&P Global Commodity Insights, May 13, 2022, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/energy-transition/051322-rare-earth-element-prices-to-remain-strong-as-demand-exceeds-supply-ionic.

[39] Nabeel A. Mancheri et al., “Effect of Chinese Policies on Rare Earth Supply Chain Resilience,” Resources, Conservation & Recycling 142 (March 2019): 110, https://doi.org/10.1016/j.resconrec.2018.11.017.

[40] Qian Zhou and Sofia Brooke, “China Merges Three Rare Earths State-Owned Entities to Increase Pricing Power and Efficiency,” Dezan Shira & Associates, January 12, 2022, https://www.china-briefing.com/news/china-merges-three-rare-earths-state-owned-entities-to-increase-pricing-power-and-efficiency/.

[41] Felix K. Chang, “China’s Rare Earth Metals Consolidation and Market Power,” Foreign Policy Research Institute, March 2, 2022, https://www.fpri.org/article/2022/03/chinas-rare-earth-metals-consolidation-and-market-power/.

[42] 2022, As Anchors Cut Free, NdPr Oxide Prices Set to Sail Higher, Adamas Intelligence, October 25, https://www.adamasintel.com/ndpr-oxide-price-to-sail-higher/

[43] Mancheri et al., “Effect of Chinese Policies on Rare Earth Supply Chain Resilience.”

[44] Tom Daly, “Minmetals Unit Flags China Rare Earths Restructuring,” Reuters, September 23, 2021, https://www.reuters.com/world/china/minmetals-unit-flags-china-rare-earths-restructuring-2021-09-23/; Avery Chen, “China Creates New State-Owned Rare Earths Giant,” S&P Global Market Intelligence, December 23, 2021, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/china-creates-new-state-owned-rare-earths-giant-68185761.

[45] A SASAC press releases mentions the reorganization as “reinforcing the central government’s direct control” and that “SASAC fulfils the responsibility of stakeholder on behalf of the State Council.” See “SASAC announcement on the establishment of China Rare Earth Group,” International Energy Agency, October 30, 2022, https://www.iea.org/policies/15513-sasac-announcement-on-the-establishment-of-china-rare-earth-group.

[46] “Ao Hong, Chairman of China Rare Earth Group: Further Promote the Substantive Reorganization of Rare Earth Assets,” Shanghai Metals Market, December 28, 2021, https://news.metal.com/newscontent/101707557/ao-hong-chairman-of-china-rare-earth-group-further-promote-the-substantive-reorganization-of-rare-earth-assets; Shunsuke Tabeta, “China Consolidates 3 Rare Earth Miners into ‘Aircraft Carrier,’” Nikkei Asia, December 24, 2021, https://asia.nikkei.com/Business/Markets/Commodities/China-consolidates-3-rare-earth-miners-into-aircraft-carrier.

[47] “Leading Party Members Group of China Minmetals Attends Conference of Central SOEs to Study Spirits of the Sixth Plenary Session of the 19th CPC Central Committee,” China Metallurgical Group Corporation, November 17, 2021, http://www.mcc.com.cn/mccen/focus/_325415/802971/index.html.

[48] “Change to CEO and Chairman,” MMG Limited, January 6, 2022, https://www.mmg.com/media-release/change-to-ceo-and-chairman/.

[49] “China Minmetals Holds a Symposium on Celebrating the One-Year Anniversary of the Important Speech Delivered by General S,” China Chamber of Commerce of Metals, Minerals & Chemical Importers and Exporters, February 19, 2022, https://en.cccmc.org.cn/news/member/ff8080817ed756d8017f43e5a91c16ff.html.

[50] Chen, “China Creates New State-Owned Rare Earths Giant.”

[51] “China Names Commander-In-Chief of C919 Project As New MIIT Head,” CGTN, July 30, 2022, https://news.cgtn.com/news/2022-07-30/China-names-commander-in-chief-of-C919-project-as-new-MIIT-head-1c5yrTHwpgI/index.html.

[52] “China Sets Limit On Annual Rare Earth Mining Volume By 2020,” Xinhua News Agency.

[53] For further information on upstream rare earth productions quotas, please see https://www.miit.gov.cn/jgsj/ycls/xt/art/2022/art_0a6a09d2d7a642e6a0f6a9b11583f4f0.html. For information on China’s production quotas for downstream rare earth products, please see https://www.miit.gov.cn/jgsj/ycls/xt/art/2022/art_4d4e79991d794e4c93559a6efa6d0529.html.

[54] “China Approves Major Rare-Earth Merger to Stabilize Supply Chains,” Global Times, December 2, 2021, https://www.globaltimes.cn/page/202112/1243120.shtml.

[55] Xuanmin, “China Plans World-Class Rare-Earth Cluster in Xiongan New Area.”

[56] “New SOE China Rare Earth Group Established to Strengthen Dominance of Industry,” Pandaily, December 24, 2021, https://pandaily.com/new-soe-china-rare-earth-group-established-to-strengthen-dominance-of-industry/.

[57] “China to Form Two Rare Earth Giants to Strengthen Pricing Power,” Bloomberg News, September 23, 2021, https://www.bloomberg.com/news/articles/2021-09-24/china-s-rare-earth-miners-announce-plan-to-restructure-assets.

[58] “China Sets Limit On Annual Rare Earth Mining Volume By 2020,” Xinhua News Agency.

[59] Mancheri et al., “Effect of Chinese Policies on Rare Earth Supply Chain Resilience.”

[60] “The Effects of Imports of Neodymium-Iron-Boron (NdFeB) Permanent Magnets on the National Security,” U.S. Department of Commerce, 2022, https://www.bis.doc.gov/index.php/documents/section-232-investigations/3141-report-1/file.

[61] “Mountain Pass Rare Earth Mine,” NS Energy, n.d., https://www.nsenergybusiness.com/projects/mountain-pass-rare-earth-mine/.

[62] Stew Magnuson, “U.S. Startups Seek to Claw Back China’s Share of ‘Technology Minerals’ Market (Updated),” National Defense, September 7, 2021, https://www.nationaldefensemagazine.org/articles/2021/9/7/us-startups-seek-to-claw-back-chinas-share-of-technology-minerals-market.

[63] “Round Top Rare Earth and Critical Minerals Project,” NS Energy, n.d., https://www.nsenergybusiness.com/projects/round-top-rare-earth-critical-minerals/.

[64] Access TMRC’s web page detailing their Round Top project using the following link: http://tmrcorp.com/projects/rare_earths/

[65] Keith Bradsher, “China Bans Rare Earth Exports to Japan Amid Tension,” CNBC, September 23, 2010, https://www.cnbc.com/id/39318826.

[66] James T. Areddy, “Xi Jinping Flexes China’s Trade Muscle With Visit to Rare-Earths Hub,” Wall Street Journal, May 21, 2019, https://www.wsj.com/articles/xi-jinping-flexes-china-s-trade-muscle-with-visit-to-rare-earths-hub-11558442724.

[67] Wu Yuehe, “United States, Don’t Underestimate China’s Ability to Strike Back,” People’s Daily, May 31, 2019, http://en.people.cn/n3/2019/0531/c202936-9583292.html.

[68] Sofia Baruzzi, “China Tightens Control Over Management of Rare Earths,” Dezan Shira & Associates, February 25, 2021, https://www.china-briefing.com/news/china-tightens-control-over-management-of-rare-earths/.

[69] Shane Lasley, “Trump: Rare Earths Essential to U.S. Defense,” North of 60 Mining News, September 26, 2020, https://www.miningnewsnorth.com/story/2019/08/01/news/trump-rare-earths-essential-to-us-defense/5845.html.

[70] “Executive Oder on America’s Supply Chains,” The White House, February 24, 2021, https://www.whitehouse.gov/briefing-room/presidential-actions/2021/02/24/executive-order-on-americas-supply-chains/.

[71] “Assessments & Investments – Defense Production Act (DPA) Title III,” Industrial Base Policy, Assistant Secretary of Defense, n.d., https://www.businessdefense.gov/ai/dpat3/index.html.

[72] Shari Biediger, “Rare Earth in ‘God’s Country’: $30M Contract Could Bring Processing Plant to Hondo,” San Antonio Report, February 10, 2021, https://sanantonioreport.org/hondo-texas-lynas-rare-earths/.

[73] “DoD Awards $35 Million to MP Materials to Build U.S. Heavy Rare Earth Separation Capacity,” U.S. Department of Defense, February 22, 2022, https://www.defense.gov/News/Releases/Release/Article/2941793/dod-awards-35-million-to-mp-materials-to-build-us-heavy-rare-earth-separation-c/.

[74] “China Approves Major Rare-Earth Merger to Stabilize Supply Chains,” Global Times.

[75] For further information on the DOE grant, please see https://grants-gov.blogspot.com/.

[76] James Kennedy and John Kutsch, Thorium and the Rare Earth Value Chain – A Nuclear Renaissance Solution, Industrial Minerals, March 2015, https://threeconsulting.com/mt-content/uploads/2021/04/indminthree.pdf

[77] Simon Hadlington, “Rare Element Substitution a Tricky Proposition,” Chemistry World, January 5, 2014, https://www.chemistryworld.com/news/rare-element-substitution-a-tricky-proposition/6936.article.

[78] Poul Emsbo et al., “Rare earth elements in sedimentary phosphate deposits: Solution to the global REE crisis?” Gondwana Research 27, no. 2 (2015): 776-785, https://doi.org/10.1016/j.gr.2014.10.008.

[79] For background on battery chemistries for mobility, see Michelle Michot Foss and Jacob Koelsch, “Need Nickel? How Electrifying Transport and Chinese Investment are Playing Out in the Indonesian Archipelago,” Research Paper no. 04.11.22, Rice University’s Baker Institute for Public Policy, Houston, Texas, April 11, 2022, https://doi.org/10.25613/30S0-Y623.

[80] Based on conversations with and information provided by James Kennedy, Three Consulting. In discussions with M. Michot Foss, Kennedy indicated that the U.S. Nuclear Regulatory Commission, NRC rules on heavy REE byproducts source material are such that once REE reach a level at which NRC considers thorium to be source material, a project is no longer viable. See https://www.nrc.gov/reading-rm/doc-collections/cfr/part040/part040-0013.html. Also see Thorium Energy Alliance for additional information: https://thoriumenergyalliance.com/.

[81] Gabriel Collins and Andrew Erickson, “U.S.-China Competition Enters the Decade of Maximum Danger,” Research paper no. 12.20.21, Rice University’s Baker Institute for Public Policy, December 20, 2021, https://doi.org/10.25613/T3FG-YV16.

[82] EU Blocks Proposal to Sanction Russian Titanium Maker VSMPO-Avisma – WSJ, Reuters, July 21, 2022, https://www.reuters.com/article/eu-sanctions-vsmpo-avisma/eu-blocks-proposal-to-sanction-russian-titanium-maker-vsmpo-avisma-wsj-idINFWN2Z25IM. In more recent news, treatment of key metals like titanium remains ambiguous. Henry Foy and Sam Fleming, “EU to propose sanctions on Russia’s mining industry”, Financial Times, December 6, 2022, https://www.ft.com/content/09424014-da48-44fb-b602-10a55f001fc6.

[83] “USA Rare Earth Successfully Completes Phase I Rare Earth Separation and Processing Test Work,” Global News Wire, May 26, 2020, https://www.globenewswire.com/news-release/2020/05/26/2038432/0/en/USA-Rare-Earth-Successfully-Completes-Phase-I-Rare-Earth-Separation-and-Processing-Test-Work.html; For information on RapidSX separation technology, please see https://ucore.com/rapidsx/.

[84] Ari Hawkins and Doug Palmer, “White House Security Probe Could Escalate China’s Magnet Monopoly, Industry Warns,” Politico Pro, August 8, 2022, https://subscriber.politicopro.com/article/2022/08/white-house-security-probe-could-escalate-chinas-magnet-monopoly-industry-warns-00050296?utm_source=substack&utm_medium=email.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.