Introduction

It has been widely reported that the US-China Phase 1 Trade Agreement1 requires China to purchase $50 billion of energy products in the next two years. When the details of the agreement were released, media reports focused on whether it is even possible for China to import this much energy from the US over the next two years. Notably, these concerns were expressed even before the full impact of the novel coronavirus on the Chinese economy, and consequently Chinese energy demand, were known. Given the events of the past couple of months, there are serious questions about whether the energy component of the agreement is already doomed to failure.2

Even if China could purchase and take $50 billion of US-sourced energy products in CY 2020 and 2021 as required by Chapter 6 of the agreement, doing so would bring little if any benefit to either the US or China. However, with a mutual understanding between the two sides that commitments to long-term purchases from new facilities “count” toward fulfilling China’s obligations under Chapter 6, both countries could benefit. Moreover, the energy purchase provisions of the Phase 1 Trade Agreement could be satisfied and rightly considered a success, establishing a foundation upon which the two countries could build future trade agreements.

A Double Coincidence of Wants: Refocusing Short-term to Long-term

The United States as a Seller

The development and construction of large-scale energy commodity export facilities typically takes multiple years. In the case of a large liquefied natural gas (LNG) export facility, construction alone typically takes up to four years3 and requires billions of dollars of capital (both equity and debt). Financing of these projects is usually dependent on the project sponsor signing creditworthy customer(s) to long-term contracts requiring offtake, or at least payment, making them “bankable.”

The Phase 1 Trade Agreement requires China to complete its energy purchases within two years. This short time horizon means that virtually all such purchases would be of cargoes from projects that have already been built. However, those projects generally already have long-term offtake commitments, so the volume commitment will largely be met through swaps and spot sales.

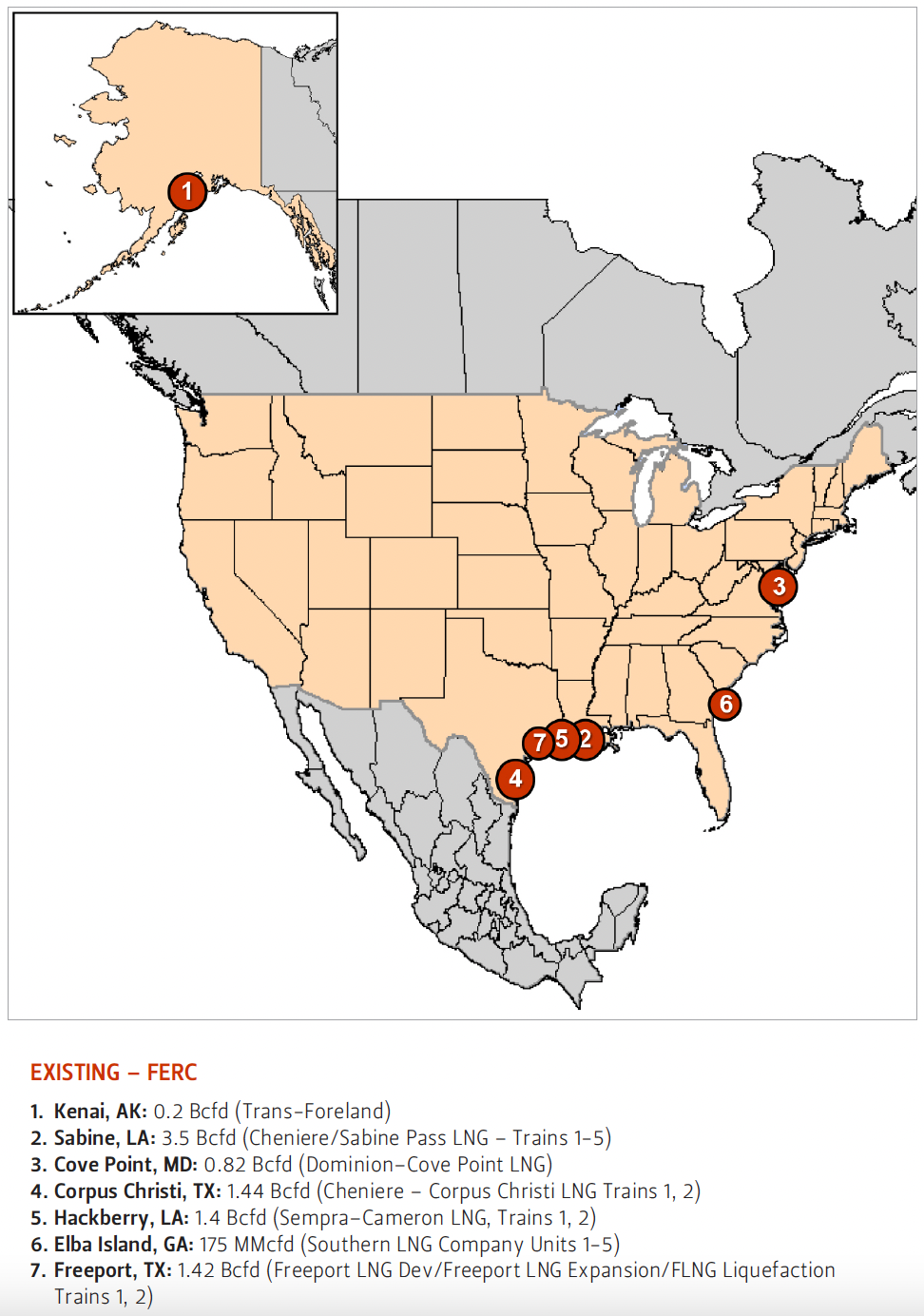

Figure 1 — Existing LNG Export Terminals in North America (as of March 19, 2020)

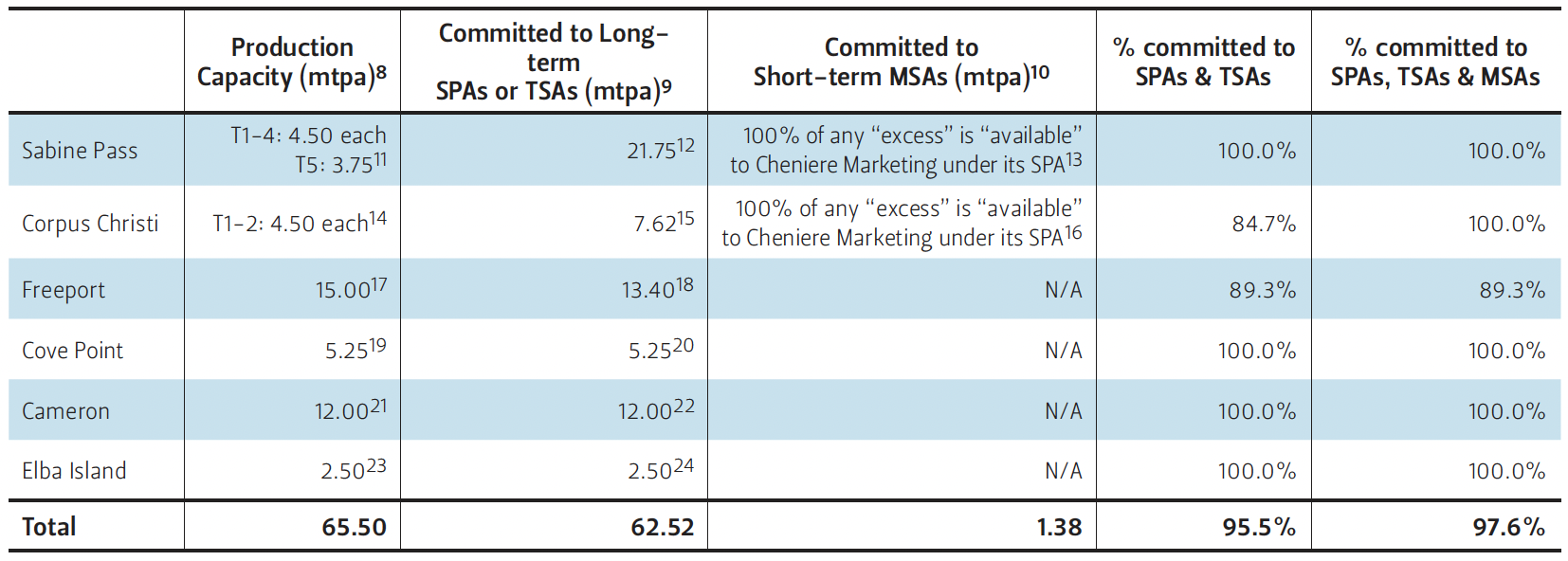

As illustrated in Figure 1, there are seven existing LNG export terminals in the United States (and in all North America for that matter), six of which are in operation. Table 1 shows that the operating export terminals, collectively, have already sold over 95% of their publicly stated production capacity.4 Thus, the requisite $50 billion of energy commodity purchases from the US under the Phase 1 Trade Agreement would, with regard to LNG, be met by China through repurchases of cargoes (or capacity allotments) that have already been sold by US producers. Cargoes would be swapped and resold, and flows would be readjusted, likely yielding little if any increase in net energy exports from the US.5

Worse yet, most of the revenue gains from Chinese imports of US LNG would likely not accrue to US exporters. Incremental revenues from swaps and resales would likely flow to the entities that have already contracted to purchase and lift cargoes, and not to the US LNG producer. Almost all LNG currently exported from the US is either sold free-on-board (FOB)6 or delivered by the operator pursuant to a terminal services agreement. Either way, the US LNG producer typically ceases to have any involvement with (or profit from) the LNG once the vessel is loaded at the US port. In fact, under the rapidly evolving competition laws in Japan and other Asian and European countries, it could arguably be unlawful for an FOB seller to profit from a post-lifting diversion of an LNG cargo.7 Hence, the reselling of cargoes already committed to be taken would, in most cases, yield little if any benefit to the US. Even if increased spot purchases resulted in the taking of cargoes that might otherwise be canceled (whether due to low prices, reduced demand, or something else), the vast bulk of infrastructure that would be used to produce, transport, liquefy, and store natural gas is already in place for the next two years. Thus, the US-China Phase 1 Trade Agreement, even if fully complied with by China, could result in little or no net investment or job creation for the energy industry in the US.

Table 1 — U.S. LNG Liquefaction Export Facilities Commitments (as of March 1, 2020)

China as a Buyer

Just as the benefits to the US as a seller are unclear, so too are the benefits to China of spending $50 billion to import LNG and other energy products over the next two years. China, like other large energy-consuming nations, benefits from having multiple secure sources of energy at competitive prices. New facilities, underpinned by long-term purchase commitments, could provide an additional competitive source of supply for China and other customers for up to 30-40 years, some 15-20 times the duration of the Phase 1 Agreement. However, buying spot LNG on the secondary market would largely result in swaps and the rearrangement (but not increase) of cargoes from existing supply sources to Asia.

China’s $50 billion of short-term purchases from the US will not be tied to any investment in new facilities, given its short-term nature. This stands in contrast to an arrangement that ensures long-term purchase commitments. If the Phase 1 Agreement were restructured to allow China to meet its commitments through long-term purchases from US suppliers, the purchases would effectively underwrite the development of a full-fledged supply chain providing benefits to the Chinese economy for many years to come. Moreover, as already noted, given LNG sales from the US are typically FOB or pursuant to terminal service agreements, purchases by Chinese buyers (short-term or long-term) would provide destination flexibility for cargoes loaded in the US. But a long-term offtake commitment would allow the Chinese buyer to capture the arbitrage value between cargoes from the US and cargoes from other locations around the world for the duration of the contract, thus providing a long-term value proposition that is very attractive in an evolving LNG market.

Recent events raise another salient concern with any requirement of China to purchase $50 billion of energy products in the next two years. Compressing purchases into a short time horizon leaves the Phase 1 Trade Agreement hostage to any short-term exogenous event that impacts Chinese demand. As we write, the coronavirus has restricted the movement of people and the flow of goods, thereby negatively impacting economic growth in China and around the world. The concomitant decrease in energy demand will likely make a $50 billion purchase in the short-term even more challenging. Some have suggested that China could be backed into a corner where it needs to declare force majeure—an excuse for not satisfying a contractual obligation because of certain unforeseen events that are beyond the party’s control—from the obligation to purchase $50 billion of energy products over the next two years.25

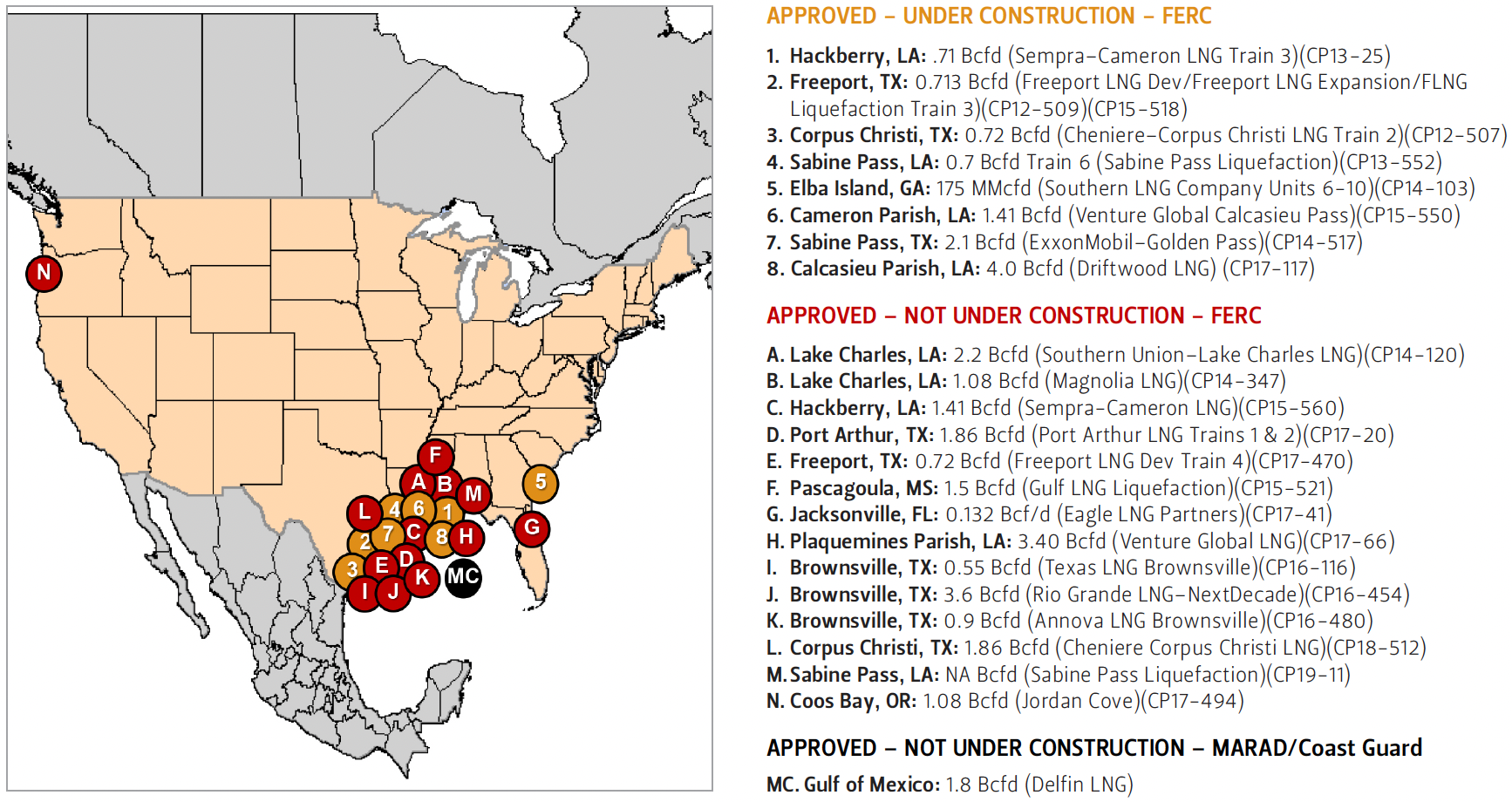

Figure 2 — Approved (Not Built) LNG Export Terminals in North America (as of March 19, 2020)

Ensuring Dual Success of the Phase 1 Trade Agreement and Reducing the Risk of a China Coronavirus Force Majeure Claim

Fortunately, the Phase 1 Trade Agreement could still be a success in the energy domain, paving the way for additional agreements in the future. This would, however, require a fairly minor change in interpretation—namely, allow long-term purchases to count toward the import commitments under the Phase 1 Agreement. Ultimately, this would allow the agreement to produce substantive benefits for both the US and China, and reduce the risk of default or declaration of force majeure by China based on short run considerations.

While global energy demand is challenged in the near term, sustainable economic growth is a long-term consideration, and access to secure energy resources is critical. In the US, the LNG pump is primed and there is no shortage of opportunities for Chinese purchase commitments to push projects forward rapidly. As shown in Figure 2, there are over a dozen pending LNG export projects in the US, some of which could achieve financing and proceed to a final investment decision this year if a buyer, such as a major Chinese state-owned oil and gas company, would enter into a binding long-term (typically 20 or more years) LNG sales agreement for a sizable volume of LNG. The launch of such a new (or expanded) project would result in tens of billions of dollars of new investment in US energy infrastructure and the addition of thousands of new jobs, potentially starting in 2020.

From China’s perspective, purchasing spot cargoes gives it no certainty about the availability of reliable long-term supply, which is germane to aspirations of secure sources of energy for continued economic growth. But if China were to contractually underpin the launch of a new LNG liquefaction facility, it would have an additional committed supply source for decades. Moreover, in an FOB purchase arrangement, it would have economic flexibility, an important consideration in any energy security paradigm. Relevant to current events, a commitment to a long-term purchase of energy from a new US export facility would also allow China to get past any near-term economic impacts of the coronavirus while also generating benefits for the US in terms of additional investment and employment.

As an example, if China were to enter into a long-term LNG purchase agreement for the output from two “trains” with a typical size of 4 million tonnes of LNG per annum,26 the revenue paid by the Chinese purchaser to the US exporter could reach $1.5 billion to $2.5 billion annually, or $30 billion to $50 billion over the life of a contract.27 If the two countries agreed to such an interpretation of the Phase 1 Trade Agreement, two such purchases could satisfy the entirety of the $50 billion purchase requirement and would have an almost immediate positive impact on investment and job creation in the US.

Concluding Remarks

Trade negotiators for the US and China should recognize that a long-term purchase from a new (or expanded) US export project would benefit both countries more than spot purchases from existing, already-contracted projects and resellers. If long-term purchase agreements executed and binding before the end of 2021 “counted” toward the energy purchase requirement in Chapter 6, both countries would benefit, and the US-China Phase 1 Trade Agreement could rightly be considered successful on the important energy component. This would, in turn, serve as a good basis on which the two countries could build future agreements expanding their relationship on economic and energy matters. In addition, such an agreed interpretation of the Phase 1 Trade Agreement could assist both countries in their fight against the economic distresses caused by the coronavirus—China would be relieved from buying energy it does not currently need, and the US would receive the benefit of an increase in job creation and investment.

Endnotes

1. Economic and Trade Agreement Between the Government of the United States of America and the Government of the People’s Republic of China, January 15, 2020, https://ustr.gov/countries-regions/china-mongolia-taiwan/peoples-republic-china/phase-one-trade-agreement/text.

2. See, e.g., “Can China Actually Buy US$50bn of US Energy Products?” Westpac Banking Corporation, Action Forex, January 14, 2020, https://www.actionforex.com/contributors/fundamental-analysis/263838-can-china-actually-buy-us50bn-of-us-energy-products/; “Unrealistically High: Experts Doubt China Can Fulfill its Targets in ‘Phase One’ of the US Trade Deal,” Fortune, January 16, 2020, https://fortune.com/2020/01/16/us-china-trade-deal-details-purchases/.

3. The Phase 1 Trade Agreement allows China to fulfill its purchase obligation by taking several energy products, including LNG, liquefied petroleum gas (LPG), liquefied butane, and other products. US-China Phase 1 Trade Agreement, Annex 6.1, Part 3, p.6-22. This article focuses on LNG, but the principles of encouraging long-term purchases as a means of producing jobs and investment in the US apply to other fuels as well.

4. Kenai LNG, opened in 1969, has a liquefaction capacity of 1.6 mtpa. However, it is in the process of being converted to a facility for the import of LNG. See FERC dockets PF19-2-000, CP09-34-000.

5. Kenneth Medlock, Ted Temzelides, and Woongtae Chung, Mercantilism’s Groundhog Day: The US-China Trade War and Some Regional Energy Market Implications, Rice University’s Baker Institute for Public Policy, Houston, Texas, February 4, 2020.

6. See, e.g., Incoterms 2020, International Chamber of Commerce, available at https://2go.iccwbo.org/incoterms-2020-eng-config+book_version-Book/.

7. “Survey on LNG Trades,” The Japan Fair Trade Commission, June 2017, http://www.jftc.go.jp/en/pressreleases/yearly-2017/June/170628.html; Memorandum of Cooperation between the European Commission, on behalf of the European Union, and the Ministry of Economy, Trade and Industry of Japan on Promoting and Establishing a Liquid, Flexible and Transparent Global Liquefied Natural Gas Market, July 11, 2017.

8. Includes facilities expected to be in commercial operation on or before June 30, 2020. Production capacity is based on the capacity of each such facility as publicly stated by the facility owner. In practice, facility production may differ from stated operating capacity based upon maintenance, weather, and other factors. Figures in MMBtus are converted to approximate MT of LNG using the ratio: 1 million mt LNG = 49,257,899 MMBtu. https://www.unitjuggler.com/convert-energy-from-MMBtu-to-MtLNG.html. Note, the exact conversion may vary depending on the assumed heat content of LNG.

9. Includes publicly announced LNG Sale and Purchase Agreements (SPAs) or Terminal Service Agreements (TSAs) with deliveries scheduled to commence on or before December 31, 2020.

10. Includes publicly announced LNG Master Sales Agreements (MSAs) in effect on or before December 31, 2020.

11. See Cheniere website at https://www.cheniere.com/terminals/sabine-pass/trains-5-6/.

12. Shell (BG), GasNatural Fenosa, Korea Gas Corporation (KoGas), and GAIL (India) Ltd. each contracted to purchase 182.5 Tbtus annually for 20 years from trains 1-4. Shell (BG) and Total have each agreed to purchase additional firm and seasonal volumes of approximately 2.11 mtpa and 0.27 mtpa, respectively. https://d1io3yog0oux5.cloudfront.net/_56be4fcd932918c28ab26b977b8f1e0d/cheniere/db/ 708/6010/pdf/Chenire_02_22_16_-_Credit_Suisse_Energy_Summit_-_FINAL.pdf; “Train 5 capacity of 3.75 mtpa has been contracted with foundation customers on a long-term FOB basis under sale and purchase agreements (SPAs) with Total and Centrica.” https://www.cheniere.com/terminals/sabine-pass/trains-5-6.

13. “Any excess capacity not sold under long-term SPAs to foundation customers is available for Cheniere Marketing to purchase as described under its SPA.” https://www.cheniere.com/terminals/sabine-pass/trains-5-6/; “Through its subsidiary, Cheniere Marketing, LLC (together with its subsidiaries, “Cheniere Marketing”), it is developing a portfolio of long-, medium-and short-term SPAs offering LNG on an FOB or DAT basis. Cheniere Marketing has purchased LNG from the SPL Project and other locations worldwide and transported and unloaded commercial LNG cargoes. Cheniere Marketing is expected to have access to excess LNG from the SPL Project and the Corpus Christi LNG terminal not sold under long-term sale and purchase agreements to third parties.” See https://lngir.cheniere.com/.

14. Cheniere stated it does not expect Corpus Christi Train 3 to reach substantial completion until 1H 2021. So, Train 3 is excluded from this analysis. See https://www.cheniere.com/terminals/corpus-christi-project/liquefactions-facilities-trains-1-3/.

15. “For the first two LNG trains, 7.62 of the 9.0 mtpa has been contracted to third party, foundation customers on a long-term FOB basis under sale and purchase agreements (SPAs). Foundation customers include Pertamina, Endesa, Iberdrola, GasNatural Fenosa, Woodside, and EDF.” Id.

16. “Any excess capacity not sold under long-term SPAs to foundation customers is available for Cheniere Marketing to purchase as described under its SPA.” Id. Cheniere Marketing has announced long-term LNG SPAs with CPC Corporation for 2.0 mtpa starting in 2021 and PGNig for 1.45 mtpa starting in 2019. https://d1io3yog0oux5.cloudfront.net/_56be4fcd932918c28ab26b 977b8f1e0d/cheniere/db/708/6225/pdf/02 +25+20+4QFY+19+Earnings+vF.pdf.

17. See Freeport LNG website at http://freeportlng.com/our-business/gas-liquefaction/. Freeport’s stated figures include train 3, which Freeport has stated is expected to enter commercial operations Q2 2020. Id.

18. “We have contracts to supply baseload LNG to Osaka Gas, JERA (an alliance between Tokyo Electric and Chubu Electric), BP Energy, Toshiba, and SK E&S: a total of 13.4 mtpa of production capacity under 20-year use-or-pay liquefaction tolling agreements. The project's EPC contractor envisages that the three production units will commence commercial operations sequentially between Q3 2019 and Q2 2020.” Id.

19. “The Cove Point facility” has a “nameplate annual capacity of 5.25 million tonnes of LNG ....” https://www.reuters.com/article/usa-trade-tokyo-gas/cove-point-lng-facility-in-u-s-set-for-planned-outage-in-autumn-idUSL3N1T 828O?feedType=RSS&feedName=companyNews& utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+reuters% 2FcompanyNews+%28News+%2F+US+%2F+Company+News%29, available on https://www.dominionenergy.com/company/moving-energy/dominion-energy-transmission-inc/facilities-projects-and-programs/cove-point.

20. “Dominion sold the project’s capacity for 20 years to a subsidiary of GAIL (India) and to ST Cove Point, a joint venture between units of Japanese trading company Sumitomo Corp and Tokyo Gas. Tokyo Gas has a contract to buy 1.4 million tonnes a year of Cove Point LNG for 20 years, while Kansai Electric Power has contracted to take 800,000 tonnes a year.” Id.

21. Although Cameron LNG indicates that it is authorized from the U.S. Department of Energy (DOE) to export up to 14.95 mtpa, Cameron LNG’s website also states: “The Cameron LNG liquefaction-export project includes three liquefaction trains with a projected export of 12 million tonnes per annum of LNG .…” https://cameronlng.com/2019/12/cameron-lng-achieves-first-lng-production-from-train-2/. “Initial production of LNG from trains 2 and 3 at Cameron, or startup, is currently set for the first quarter of 2020 and second quarter of 2020, respectively.” https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/042919-initial-production-from-cameron-lng-second-third-trains-pushed-back-until-2020- mcdermott-international. Construction has not commenced on trains 4-5. https:// cameronlng.com/lng-facility/timeline/.

22. Cameron LNG’s DOE order states that 100% of the 12 mtpa of export capacity is contractually committed to GDFSuez (now Total), Mitsubishi and Mitsui. https://www.energy.gov/sites/prod/files/2014/02/f7/ord3391.pdf. See also, https://www.mitsubishicorp.com/jp/en/bg/natural-gas-group/project/cameron-lng/; https://www.euro-petrole.com/cameron-lng-liquefaction-export-facility-begins-production-at-train-2-n-i-19950; and https://www.lngworldnews.com/sempra-gdf-suez-mitsubishi-and-mitsui-sign-cameron-lng-tolling-agreements-usa/.

23. https://www.kindermorgan.com/pages/business/gas_pipelines/projects/elbaLNG. The project owner has reportedly indicated that it plans to have the entire facility in operation by the end of the first half of 2020. https://www.reuters.com/article/kinder-morgan-de-lng-terminal/update-2-kinder-morgan-to-have-all-elba-island-lng-units-in-service-by-mid-2020-ceo-idUSL2N271245.

24. Shell is committed to take 100% of the capacity of the Elba Island liquefaction project for 20 years. https://www.kindermorgan.com/pages/business/gas_ pipelines/projects/elbaLNG.

25. “China’s Virus May Break Phase One of China-US Trade Deal,” Radio Free Asia, February 7, 2020, https://www.rfa.org/english/commentaries/energy_watch/hina-virus-may-break-phase-one-deal-02072020110356.html.

26. For comparison, this is roughly the size of the existing trains at Sabine Pass, Corpus Christi, and Cameron. Trains at Elba Island are smaller; those at Cove Point and Freeport are slightly larger. See Table 1.

27. Forward LNG prices vary based on several factors, including the date and place of delivery and the date on which the estimation is made. However, at the time of writing, the March 2020 CME Group (Platts) Japan-Korea Marker (JKM) contract for LNG delivered in March 2024 is $5.735 per MMBtu. https://www.cmegroup.com/trading/energy/natural-gas/lng-japan-korea-marker-platts-swap.html. For an 8 mtpa LNG purchase obligation, this price would could result in annual revenues in the $1.5-2.5 billion range stated above. Transportation costs, fuel losses, and other factors would affect the revenues that would accrue to the LNG producer.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.