The case of Terra, a once-prosperous blockchain network in the cryptocurrency world that suffered one of the biggest falls in the history of crypto, has policymakers pushing for regulations to diminish the risk of similar collapses. However, the notion of increased regulation has others wondering if new policies will impede the natural Darwinism of the free market and stifle innovation in entrepreneurial pursuits.

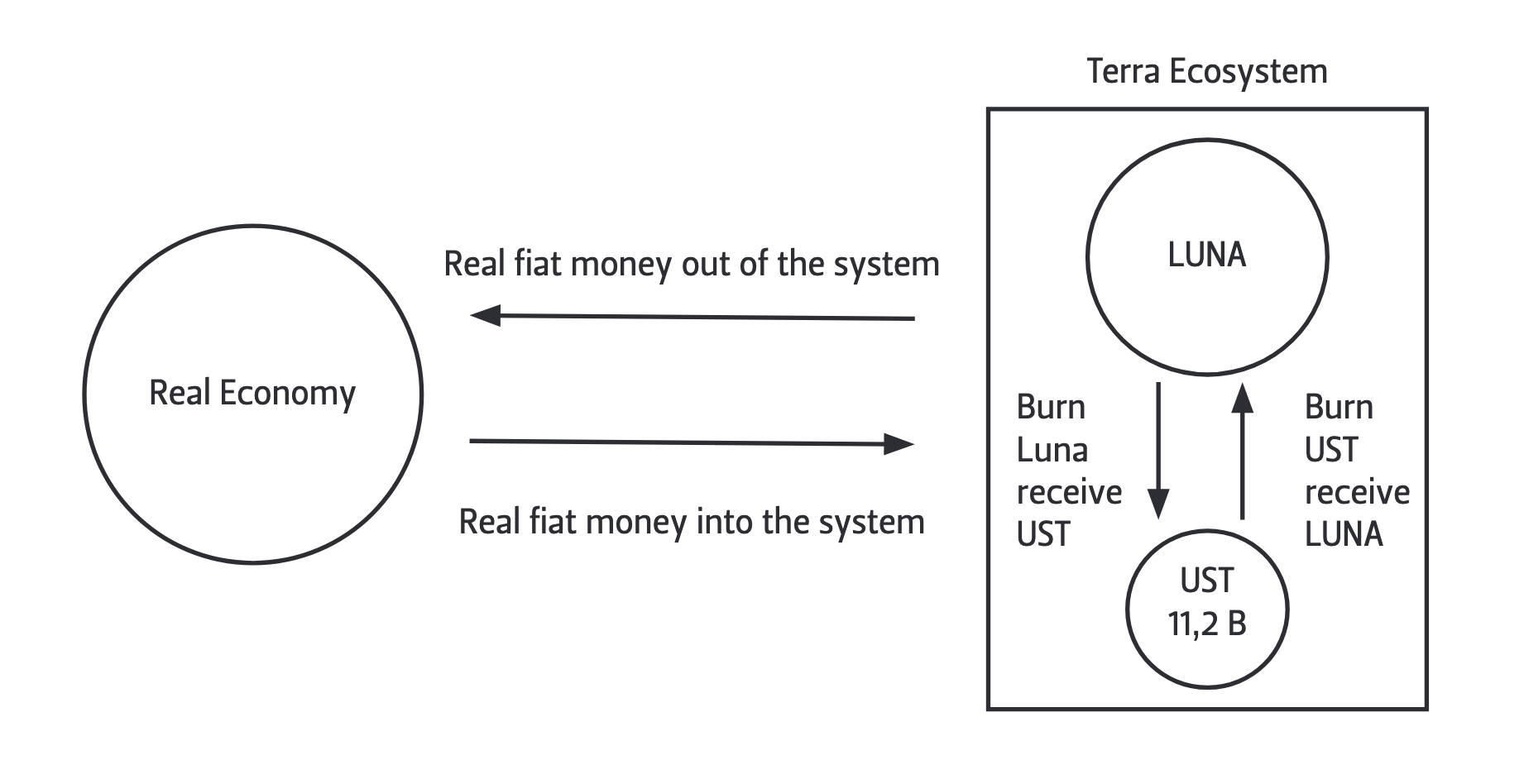

Terra is a blockchain ecosystem with its own non-fungible tokens (NFTs), decentralized finance (DeFi) platforms, and Web3 applications. Two of Terra’s native tokens, Luna (LUNA) and TerraUSD (UST), are the apparent cause of the ecosystem’s demise. UST is a stablecoin with a worth pegged to the U.S. dollar, indicating that one UST should be valued at $1. This value was achieved with UST’s sister token, LUNA, using a smart contract–based algorithm that would burn LUNA tokens in order to mint new UST tokens.

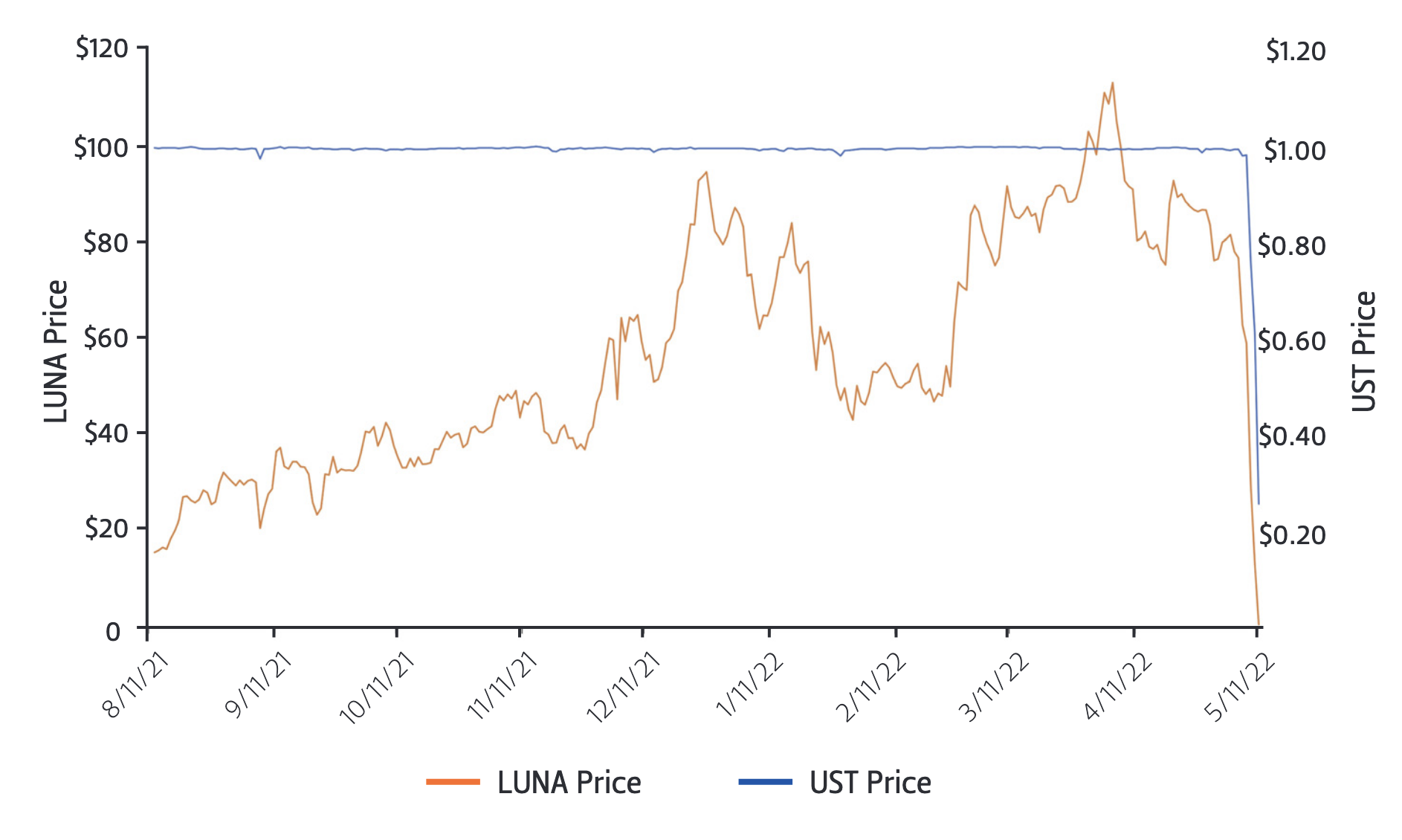

The balance had been maintained until the collapse began on May 7, 2022, when the price of the stablecoin began to deviate below $1. It was officially de-pegged from the dollar on May 9, after falling to 35 cents.1 On May 12, Terra saw even more devastating blows: the blockchain network was halted twice in one day,2 and the price of LUNA, once having reached a high of $116, dropped to $0.000017.3

The consequence of the situation is that officials, including U.S. Treasury Secretary Janet Yellen, have urged Congress to regulate crypto stablecoins, noting the “risks to financial stability.”4 It seems that the government is in a reactive position and lagging behind in regulations regarding crypto. A compounding risk factor includes the finding that the majority of investment in the crypto space are made by Gen Z and millennial buyers,5 which, according to one study, makes compulsive investments and withdrawals such as those seen in the midst of Terra’s quick demise more likely.6

In November 2021, the President’s Working Group on Financial Markets (PWG), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) released a joint report outlining recommendations for the regulation of stablecoins.7 The agencies expressed concern over risks to market integrity, investor protection, illicit finance, and risks to the broader financial system as stablecoin usage increases.8 Existing rules may be able to address some of these concerns where stablecoin falls into categories regulated by the U.S. Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC), and the Treasury.9 However, the report found, the risk to the broader economy, including stablecoin runs, payment system concerns, and the concentration of economic power, requires legislative action to create more oversight.10

Figure 1 — Representation of the Terra Ecosystem

To mitigate the concern that a loss of user confidence could lead to runs that might harm the users of stablecoin and the broader financial system, the agencies recommended that legislation require issuers to be insured depository institutions.11 Still, a bill to amend the Federal Deposit Insurance Act to provide for the classification and regulation of stablecoins by adding them to the definition of “deposit” died in the 116th Congress.12

The recently introduced Stablecoin Transparency of Reserves and Uniform Safe Transactions (TRUST) Act would allow issuers to opt in to bank regulation or choose from other regulation schemes, but falls short of requiring federal deposit insurance.13 The Stablecoin Innovation and Protection Act of 2022 would only allow nonbanks to issue stablecoins if they keep a segregated account with an FDIC-insure institution equaling 100% of the value of the stablecoins outstanding;14 alternative legislation introduced in Congress as the Stablecoin Transparency Act would require stablecoin issuers to hold reserves in securities or non-digital currency and publish monthly reserve reports audited by a third party.15

Figure 2 — LUNA and UST Price Movement

Furthermore, the agencies recommended that legislation require federal oversight of wallet providers to address concerns about the concentration of economic power and payment system risk, including disruptions to the payment chain that could affect the broader economy.16 To accomplish this, the agencies suggested that legislation require wallet providers’ compliance with restrictions that limit affiliation with commercial entities and use of users’ transaction data, keeping wallet providers from lending customers stablecoins and requiring compliance with risk- management, liquidity, and capital stipulations.17 These types of requirements are closely aligned with federal banking regulations, but so far no proposed bill has fully addressed all of these concerns.

The cryptocurrency exchange Coinbase has called for a single regulatory solution to increase clarity and transparency.18 However, this does not seem likely, given that the current recommendations and proposed bills instead would insert stablecoin regulations into existing regulatory frameworks governed by the SEC, OCC, Federal Reserve Board (FRB), FDIC, and Treasury.

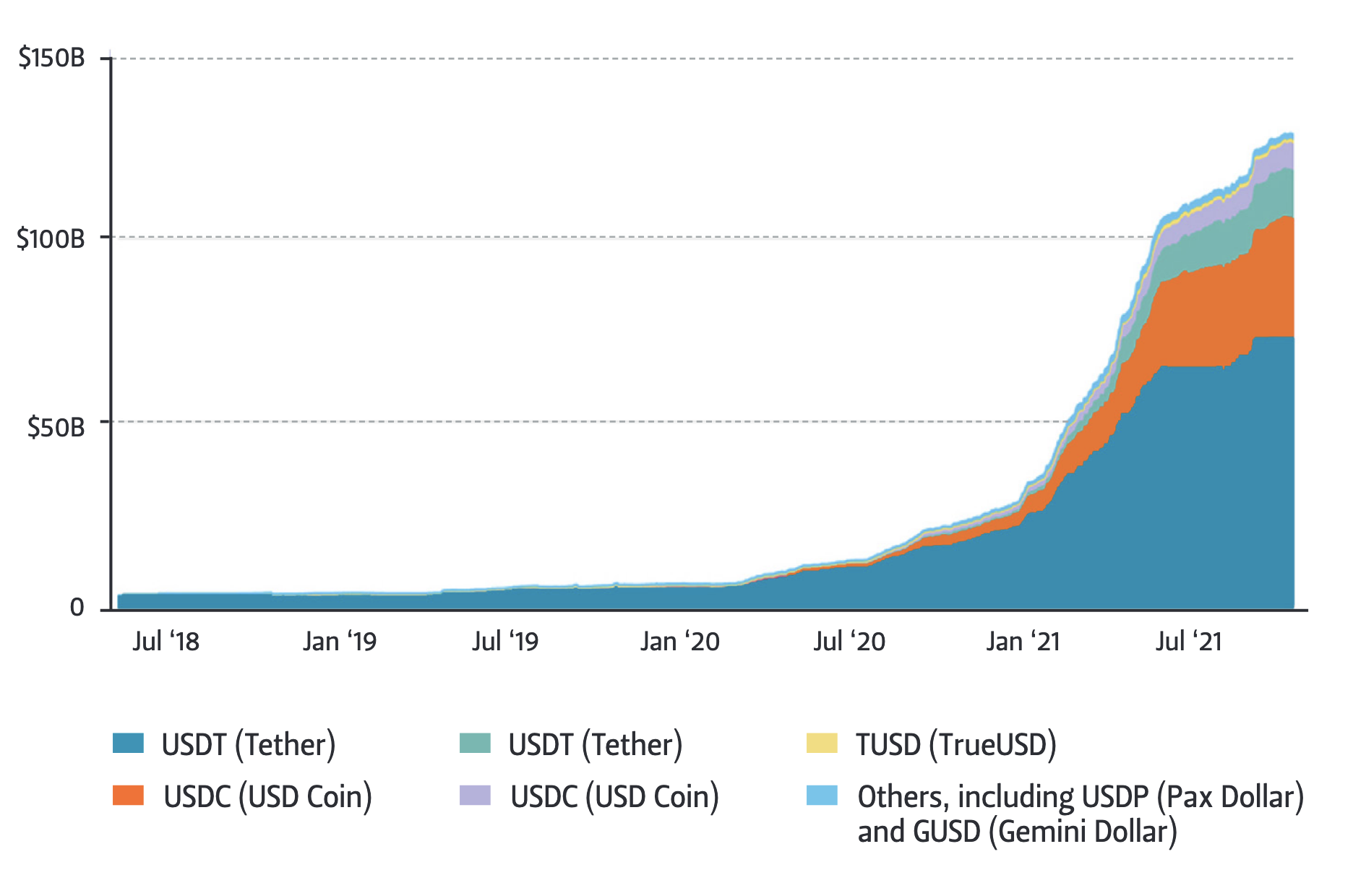

Figure 3 — Top Stablecoins by Market Capitalism

The industry is calling for clarity above all.19 Current proposed legislation largely addresses this concern by providing clear definitions of digital assets and specifying which laws apply to them.20 However, existing legislation that functions to regulate aspects of stablecoins and other cryptocurrencies should be updated to provide clear definitions for more transparency and clarity.

In June 2022, U.S. Senators Kirsten Gillibrand (D-NY) and Cynthia Lummis (R-WY) introduced the Responsible Financial Innovation Act in an effort to provide clarity to the cryptocurrency and blockchain industries. Also known as the Lummis-Gillibrand Bill, the bipartisan legislation draws its framework from traditional asset taxation and banking laws to create a clear regulatory structure for digital assets and stablecoins. Both senators have stressed the importance of clearly defining digital assets and providing clarity on certain topics, such as whether the assets are to be considered securities or commodities, so that businesses and consumers can know which laws affect them. Notably, the bill suggests that most digital assets are commodities and therefore assigns regulatory authority to the CFTC, which regulates commodities

markets. Also included in the bill are stipulations for studying three key digital asset regulation points that remain unclear: (1) the digital yuan (China’s central bank digital currency) and its security implications; (2) the possible need for self-regulatory organization (SRO); and (3) the opportunities and risks of investing retirement savings in digital assets.

These proposed regulations have the potential to demystify important aspects of the blockchain and cryptocurrency market. However, possible regulatory measures are likely to affect the characteristics of blockchain, with both positive and negative impacts. Moving forward, policymakers should weigh the advantages and disadvantages to determine whether regulation—and, if so, what regulation—would be beneficial for the market.

Endnotes

1. Krisztian Sandor and Ekin Genç, “The Fall of Terra: A Timeline of the Meteoric Rise and Crash of UST and LUNA,” May 20, 2022, https://www.coindesk.com/learn/the-fall-of-terra-a-timeline-of-the-meteoric-rise-and-crash-of-ust-and-luna/.

2. Sandor and Genç “The Fall of Terra.”

3. Coinbase, “Terra (LUNA) Price, Charts, and News,” accessed July 4, 2022, https://www.coinbase.com/price/terra-luna.

4. Paul Kiernan, “Yellen Renews Call for Stablecoin Regulation After TerraUSD Stumble,” Wall Street Journal, May 10, 2022, https://www.wsj.com/articles/yellen-renews-call-for-stablecoin-regulation-after-terrausd-stumble-11652208165.

5. Frank Gogol, “94% of Crypto Buyers Are Gen Z/Millennial, but Gen X Spends More,” Stilt (blog), March 16, 2021, https://www.stilt.com/blog/2021/03/vast-majority-crypto-buyers-millennials-gen-z/.

6. Hee Jin Kim et al., “Comparison of Psychological Status and Investment Style Between Bitcoin Investors and Share Investors,” Frontiers in Psychology 11 (November 2020), https://www.frontiersin.org/articles/10.3389/fpsyg.2020.502295/full.

7. U.S. Department of the Treasury, President’s Working Group on Financial Markets, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency, Report on Stablecoins, November 2021, https://home.treasury.gov/system/files/136/StableCoinReport_Nov1_508.pdf.

8. Report on Stablecoins.

9. Report on Stablecoins.

10. Report on Stablecoins.

11. Report on Stablecoins; 12 U.S.C. § 1813(c)(2).

12. Stablecoin Classification and Regulation Act of 2020, H.R. 8827, 116th Cong. (2020).

13. Paul H. Kupiec, “The Stablecoin Trust Act Is a Good Start but Falls Short in Key Areas,” Hill, April 27, 2022, https://thehill.com/opinion/finance/3467546-the-stablecoin-trust-act-is-a-good-start-but-falls-short-in-key-areas/; Stablecoin TRUST Act of 2022, 117th Cong., 2D session, https://www.banking.senate.gov/imo/media/doc/the_stablecoin_trust_act.pdf.

14. Stablecoin Innovation and Protection Act of 2022, 117th Cong., 2D session, https://gottheimer.house.gov/uploadedfiles/dd._stablecoin_innovation_and_protection_act_of_2022.pdf.

15. Stablecoin Transparency Act of 2022, S. 3970, 117th Cong. (2022).

16. Report on Stablecoins.

17. Report on Stablecoins.

18. Niel Roland, “US Banking Authorities Aim to Set up Crypto Framework to Satisfy Interest by Banks, Consumers, Hsu Says,” MLex, 2022, https://bit.ly/3NWAJTu.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.