Introduction

One of the most contentious tax policy issues is the nature of the taxation of business income. Of particular interest is the use and structure of what economists describe as source-based taxes on capital income—taxes assessed on the return to capital investments that are based on where the investment is made (rather than the residence of the investor). The most prominent example is the corporate income tax, which may be the most common form of taxation in the world: a 2016 survey found that 174 of 188 countries utilized the tax (Tax Foundation 2016). Nevertheless, the corporate income tax is also one of the most criticized of tax instruments—with the longstanding and ongoing debate on corporate tax reform in the United States, including the discussions of the provisions enacted last year in the Tax Cut and Jobs Act (TCJA), providing an excellent current example.

This brief addresses the arguments for and against source-based capital income taxation, focusing on the factors that countries must balance in thinking about the extent to which they should rely on a corporate income tax as a significant source of revenue. Although the arguments generally apply to the United States, the results are much broader in scope, and in fact we focus on the case in which a relatively small open economy is attempting to attract foreign direct investment (FDI) from the United States and other countries while still raising some revenue from its corporate income tax. We describe a framework for evaluating the desirability of source-based taxation, illustrating both analytically and with a simulation model how countries can balance the relative importance of various key considerations in setting corporate income tax policy. Our analysis utilizes and updates the analytical and simulation framework initially introduced in McKeehan and Zodrow (2017).

Benefits of a Source-based Capital Income Tax

When investments are relatively immobile—and in particular when their location is relatively insensitive to taxation—firm-level source-based capital income taxes offer governments an opportunity to raise revenue while minimally affecting a firm’s investment decisions. These limited distortions of investment decisions can make source-based capital income taxes preferable to other forms of taxation, since nearly all available tax instruments distort some aspect of economic decision-making and thus reduce the productivity of the resources available in an economy. Consequently, the potential prevalence of immobile investments is a key motivation for firm-level income taxes. Immobile investments can arise under a variety of circumstances. For example, investments may require the input of immobile resources (e.g., natural resources) or rely on other location-specific attributes (e.g., knowledge externalities in Silicon Valley or the existence of well-developed supply chains). Alternatively, investments may be immobile due to customer demands; for example, some investments in the service industry cannot relocate away from their customers. In combination, these considerations typically imply that some potentially significant portion of the capital income tax base is immobile, making source-based capital income taxation efficient in comparison to alternative revenue instruments.

Moreover, if immobile investments are foreign owned, taxing their returns may be especially attractive from the perspective of a country’s residents. Taxing the income earned by immobile foreign-owned investments provides an opportunity to raise revenue for residents, with the cost being borne by nonresidents and without introducing significant economic distortions. In this case, capital income taxes can be preferable to taxes that are less distortionary but entirely borne by residents. They may be even desirable in the absence of required government services, as taxing capital income and returning the revenue directly to citizens can improve domestic welfare.

Interestingly, for some foreign investors, tax policy in their home country can effectively increase the immobility of their foreign investments. Most prominently, this arises when investors receive a credit for taxes paid in a foreign country. Under a foreign tax credit system, an investor subject to a tax rate τH in their home country who pays tax rate τ on income Y earned in the source country in which the investment is made has a home country tax liability of (τH - τ)Y. Consequently, any increase in τY results in an equivalent decrease in tax liability at home, a phenomenon often described as the “treasury transfer effect” because the source country tax increase effectively transfers revenue from the home country to the source country. Since under these circumstances an increase in τ does not affect the investor’s final after-tax return on investment, taking into account the foreign tax credit system, this increase should not affect the investor’s investment decision, including the location of investment. The investment is thus immobile in the sense that a source country tax increase does not induce an outflow of capital.

However, with the recent enactment of the TCJA, the United States has joined most of its trading partners in utilizing a “territorial” international tax system that generally does not impose a residual domestic tax on foreign-source earnings. Nevertheless, given the increasing use of income shifting to international tax havens, the United States and many other countries with territorial tax systems are adopting or extending various minimum tax rules, tax base erosion provisions, and controlled foreign corporation (CFC) rules. As a general rule, such provisions currently tax the return on foreign investments that are attributed to countries with sufficiently low tax rates, and typically incorporate a foreign tax credit system. Consequently, for sufficiently low-tax countries, the relevance of foreign tax credits and the treasury transfer effect described above may be increasing.

Finally, one additional consideration can motivate capital income taxation regardless of the mobility of capital: capital income taxes may act as a backstop to labor income taxes. Capital income taxes that are much lower than labor income taxes create incentives for individuals to attempt to disguise their labor income as capital income. For example, small business owners may work extra hours without compensating themselves for their labor directly, instead capturing the benefits of their extra effort as increased profits, which are then subject to the lower capital income tax rate. In such scenarios, capital income taxation at higher rates can reduce the incentives for labor income sheltering and ensure that income taxation is applied more uniformly and thus more equitably across individuals and industries.

To summarize, the combination of investments that are relatively immobile, especially those that are foreign-owned, and the possibility of raising revenues through a treasury transfer effect from countries that utilize a foreign tax credit, coupled with a desire to limit individual labor income sheltering, provides a rationale for the continued use of source-based capital income tax systems internationally. However, source-based capital income tax systems are not without economic costs, which we discuss in the next two sections.

Costs of a Source-based Capital Income Tax

As stressed above, the benefits of source-based capital income taxation primarily arise when capital investments are immobile. Not surprisingly, the main counterargument—which is strongly emphasized in current debates regarding the corporate income tax—is that capital income taxes can be very costly for open economies when capital investments are highly mobile. In this case, increasing the capital income tax rate can drive out investment, reducing the welfare of residents of the taxing jurisdiction. In the extreme case of perfect mobility, where capital can move costlessly across international borders, capital will leave the country until the after-tax domestic rate of return equals the internationally determined rate of return, implying that capital bears none of the burden of the tax. Instead, the burden of the source-based capital income tax is borne by relatively immobile production inputs, which may include labor that suffers lower wages or the owners of other immobile factors such as land or natural resources who experience lower returns.

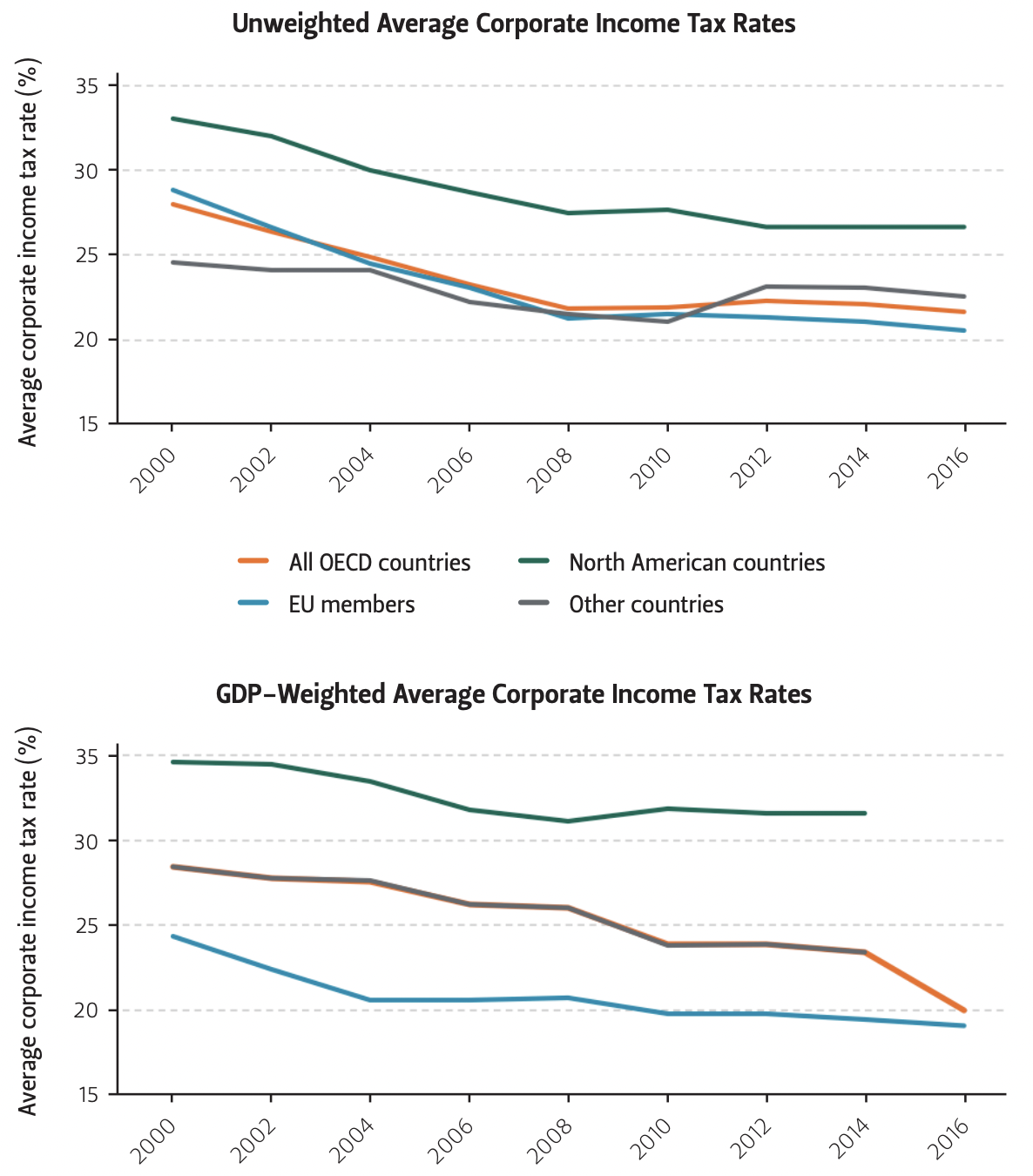

Moreover, it seems likely that the mobility of capital investments has been increasing over time (Zodrow 2010). First, increasing globalization has lowered the cost of moving both physical and financial investments across international borders. Second, firm profitability increasingly relies on the use of intangible assets such as patents, licenses, trademarks, specialized labor including management skills, and brand recognition. These intangible assets can often be moved internationally at a very low cost and without regard to the location of physical production, and are typically characterized as almost perfectly mobile. Because of the increasing importance of such highly mobile assets, the distortionary cost of source-based capital income taxes may be increasingly borne by domestic residents and the owners of immobile domestic assets. Indeed, the increasing importance of mobile investments may explain why corporate income tax rates have generally fallen over the last 30 years (see Figure 1).

Figure 1 — Average Statutory Corporate Income Tax Rates in OECD Countries

Source Organisation for Economic Co-operation and Development, 2017; OECD.Stat, Tax Database, Table II.1 (“Central government and personal income tax rates and thresholds”) and Table I (“Gross domestic product [GDP]” [output approach]).

Source-based capital income taxes that take the form of corporate income taxes have some additional costly distortionary effects. By definition, corporate income taxes are only applicable to taxable corporations. Partnerships, LLCs, LLPs, sole proprietorships, and other pass-through entities (including S corporations in the United States) do not pay the corporate income tax. Instead, the individuals owning the firms are subject to capital income taxes that are based solely on their own personal rates, which typically results in a lower total tax liability than would be owed under the corporate income tax. Consequently, corporate income taxes tend to distort the form of business organization, favoring pass-through entities over corporations. Further, corporate income taxes allow deductions for interest payments but not for payments to equity holders, creating a tax bias favoring debt-financed investment. While these distortions are not inherent to all forms of source-based capital income taxation, they occur under the corporate income tax, adding to concerns about excessive reliance on source-based capital income taxation.

International Income Shifting and Source-based Capital Income Taxation

The choice of the structure of capital income taxation is even more complicated due to recent increases in the extent of international income shifting, as recently documented for the United States by Clausing (2016). Source-based capital income taxes create incentives for corporations to misrepresent the location where income is generated. Using firm restructuring, transfer pricing, earnings stripping, judicious location of licenses and patents, and other forms of tax planning, corporations can increase the proportion of income assigned to low-tax countries, significantly reducing their corporate income tax liability.

Income shifting has several implications for capital income taxation. The most obvious is that it reduces the size of the domestic tax base and thus implies that higher rates are needed to raise the same amount of revenue. For example, Clausing (2016) estimates that income shifting decreased corporate income tax revenues in the United States by between $77 billion and $111 billion in 2012, which corresponds to between 32% and 46% of corporate income tax revenues in that year. Moreover, concern about income shifting may lead governments to reduce their corporate tax rates. In addition, implementing income shifting schemes is costly and thus implies that firms spend resources on tax avoidance rather than on productive activities, which raises the economic cost of capital income taxation. However, despite these considerations, income shifting can motivate governments to increase capital income tax rates. This occurs because income shifting lowers the effective tax rate paid by firms that engage in such activities and consequently mitigates the capital flight costs associated with relatively high levels of capital income taxation. Moreover, if firms that engage in income shifting also use more mobile capital, then income shifting implies that the burden of the capital income tax is borne to a larger extent by immobile capital, increasing the relative efficiency of capital income taxation.

The complex impacts of income shifting have led to complex policy responses. Some policies have sought to limit the extent of income shifting, a trend exemplified by the growing use of CFC rules and the anti-base-erosion provisions outlined in OECD (2013) as well as those enacted in the TCJA. In contrast, other policies may actually facilitate income shifting as a mechanism that alleviates the capital flight associated with capital income taxation; the “check-the-box” rules in the United States, which allow firms to easily choose corporate or pass-through status and facilitate certain forms of income shifting, exemplify this type of policy response.

Weighing the Costs and Benefits of Source-based Capital Income Taxation in a Simulation Model

To capture the various arguments for and against source-based capital income taxation, we constructed a computational model of a small open economy in McKeehan and Zodrow (2017), which should be consulted for details of the model and its calibration. We provide a brief overview of the simulation model below.

The computational model incorporates two production sectors designed to capture many of the costs and benefits of a source-based capital income tax. Sector one, the domestic sector, uses immobile, location-specific capital (LSK) in production in addition to perfectly mobile capital and locally provided labor. Sector two, the multinational sector, uses labor and two alternative forms of perfectly mobile capital, ordinary capital and firm-specific capital (which includes intangible assets and the unique managerial skills to utilize them effectively). Firms in the multinational sector have the ability to shift some capital income to a tax haven country, and may be subject to a foreign tax credit system. Additionally, the good produced by the multinational sector flows freely across borders, so the price of this good is set in international markets. In contrast, everything produced in the domestic sector is assumed to be sold locally, so that the price of the domestic good is determined in the domestic market.

To capture individual behavior, we model a representative individual who chooses labor supply and consumption purchases based on market prices and wages. This individual can earn income from both market wages and capital investment, and may be able to disguise a portion of wages as capital income, although this activity is costly.

Accounting for individual and firm behavior, the government must raise a set amount of revenue. To raise this revenue, the government relies on three tax instruments: a capital income tax (τ), a labor income tax (τL ), and a tax that targets the capital income earned by immobile, location-specific capital (τLSK). To study the optimal choices among these taxes, we consider the behavior of a government that has the best interests of its representative individual in mind and chooses these rates to maximize this individual’s welfare. Under this circumstance, the tax that targets the return to immobile, location-specific capital (τLSK) is always preferable, so we constrain the government’s ability to tax this return.

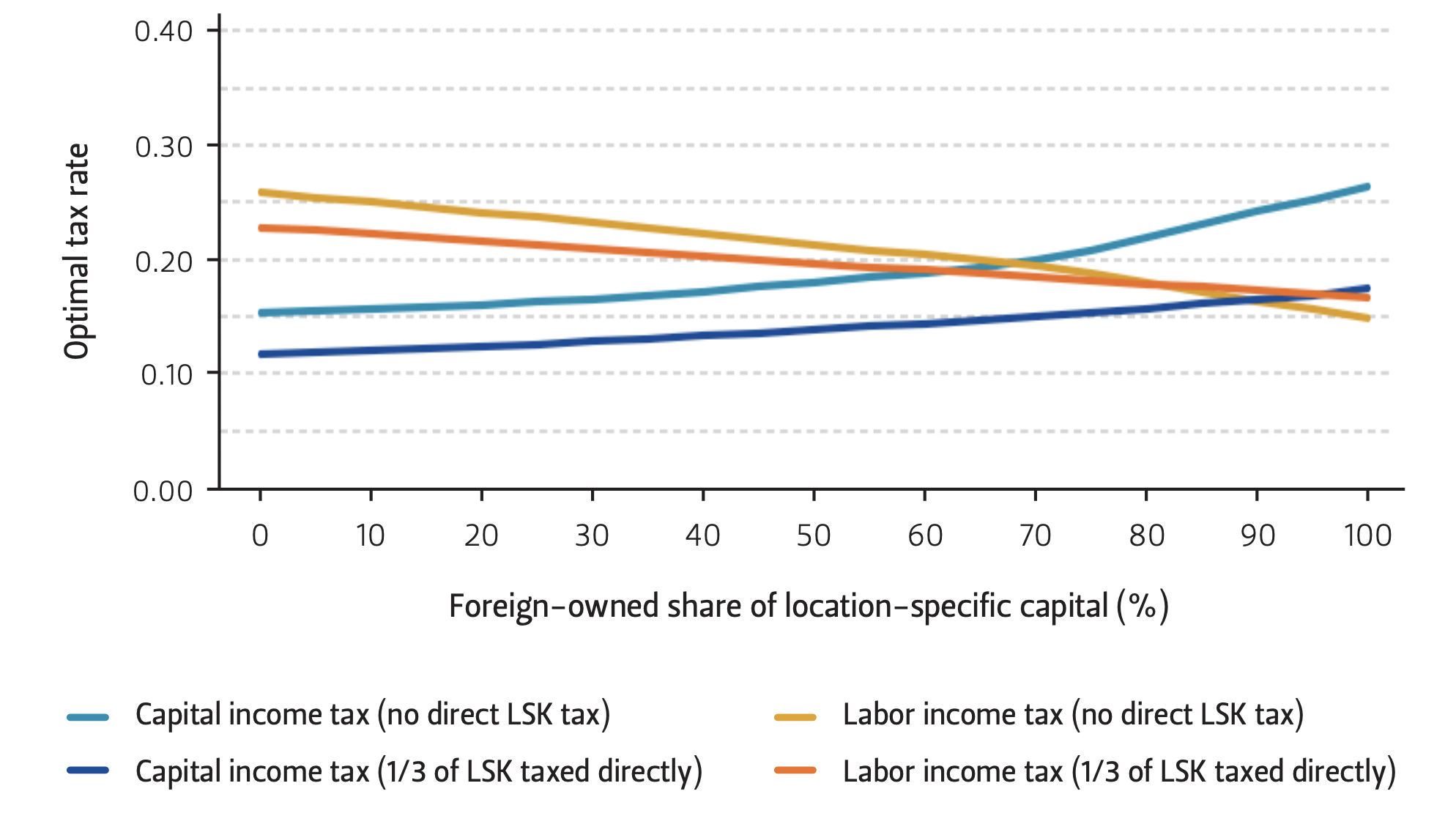

As discussed in the previous sections, the opportunity to tax foreign-owned, immobile investments is one of the strongest motivations for taxing capital income. The computational model confirms this point. Figure 2 illustrates how optimal capital income and labor income taxes change as the share of location-specific capital owned by nonresidents changes, and shows that optimal reliance on capital income taxation rises as the foreign-owned share of location-specific capital increases. However, the degree to which taxation optimally shifts from labor income to capital income changes significantly when the government has the opportunity to tax location-specific capital directly. Since direct taxation of location-specific capital raises revenue (and is always preferable to either alternative), the availability of such a tax generally lowers both taxes. More importantly, directly taxing location-specific capital lowers the sensitivity of the optimal capital income tax to the extent of foreign ownership. This suggests that the opportunity to target taxes toward immobile capital investments undermines one of the key motivations for a general capital income tax. A separate tax on the economic rents earned by the natural resource sector is the primary example of such a tax.

Figure 2 — Optimal Taxation and Foreign Ownership of Location-specific Capital

Source Authors’ analysis.

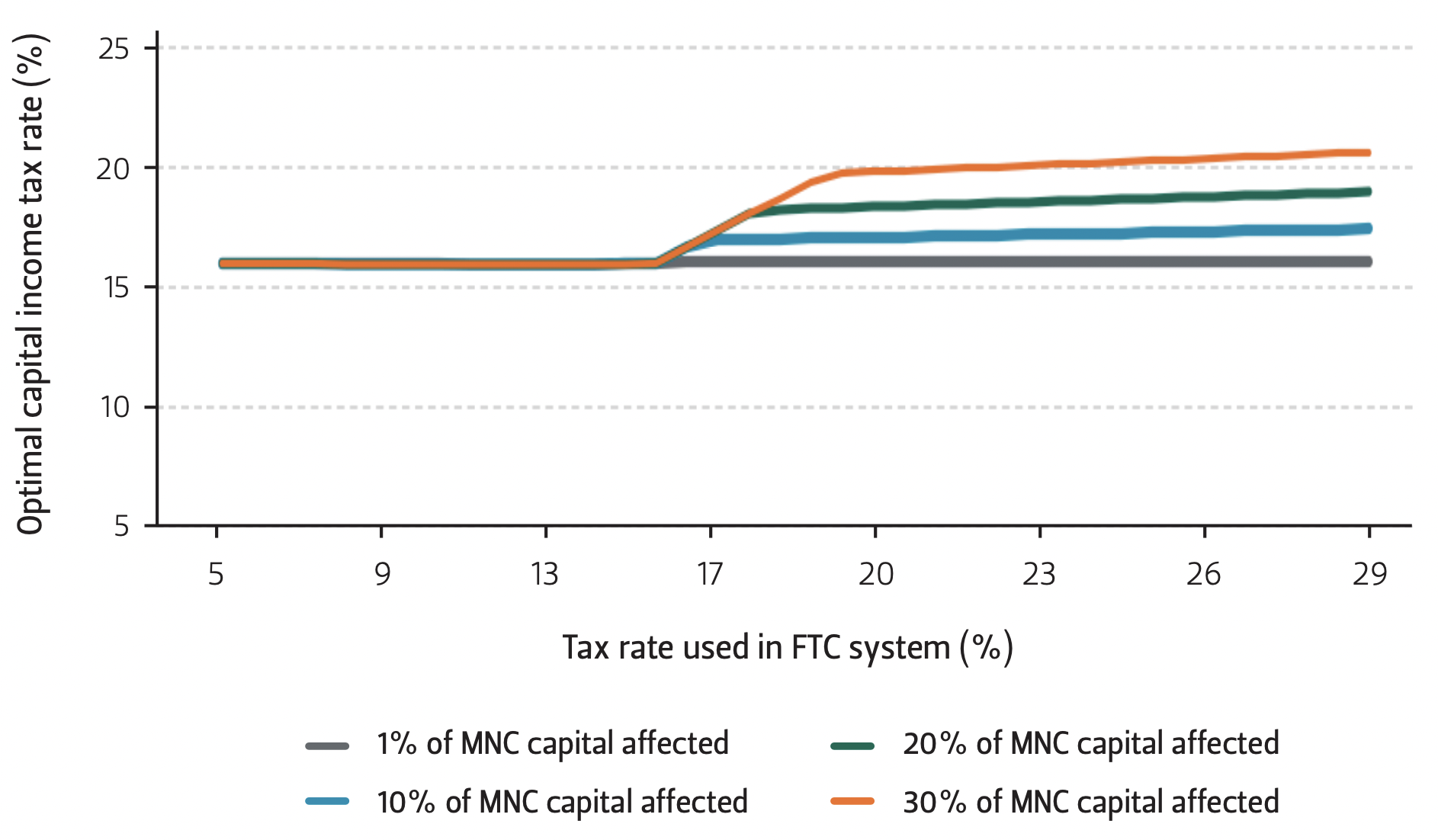

As discussed above, investments may not be inherently immobile, but effectively immobile because other countries use foreign tax credit (FTC) systems. In this case, it is unlikely such immobile investments could be targeted, since this would require tax rates that varied based on the home country of the corporation. To explore the importance of foreign tax credits, we vary both the extent of credit systems, and the tax rate used in those systems. As illustrated in Figure 3, neither the tax rate nor the extent of crediting should affect local decisions until the foreign tax rate exceeds the domestic tax rate. However, a tax rate in the foreign tax system with an FTC that exceeds the domestic rate increases the optimal domestic capital income tax rate, and the extent to which domestic capital is affected by FTC systems becomes important. Indeed, as Figure 3 illustrates, once the FTC rate is sufficiently high, the extent to which the multinational corporations’ (MNC) capital is eligible for foreign tax credits becomes a key determinant of the optimal tax rate.

Figure 3 — Capital Income Taxation and Foreign Tax Credit Systems

Source Authors’ analysis.

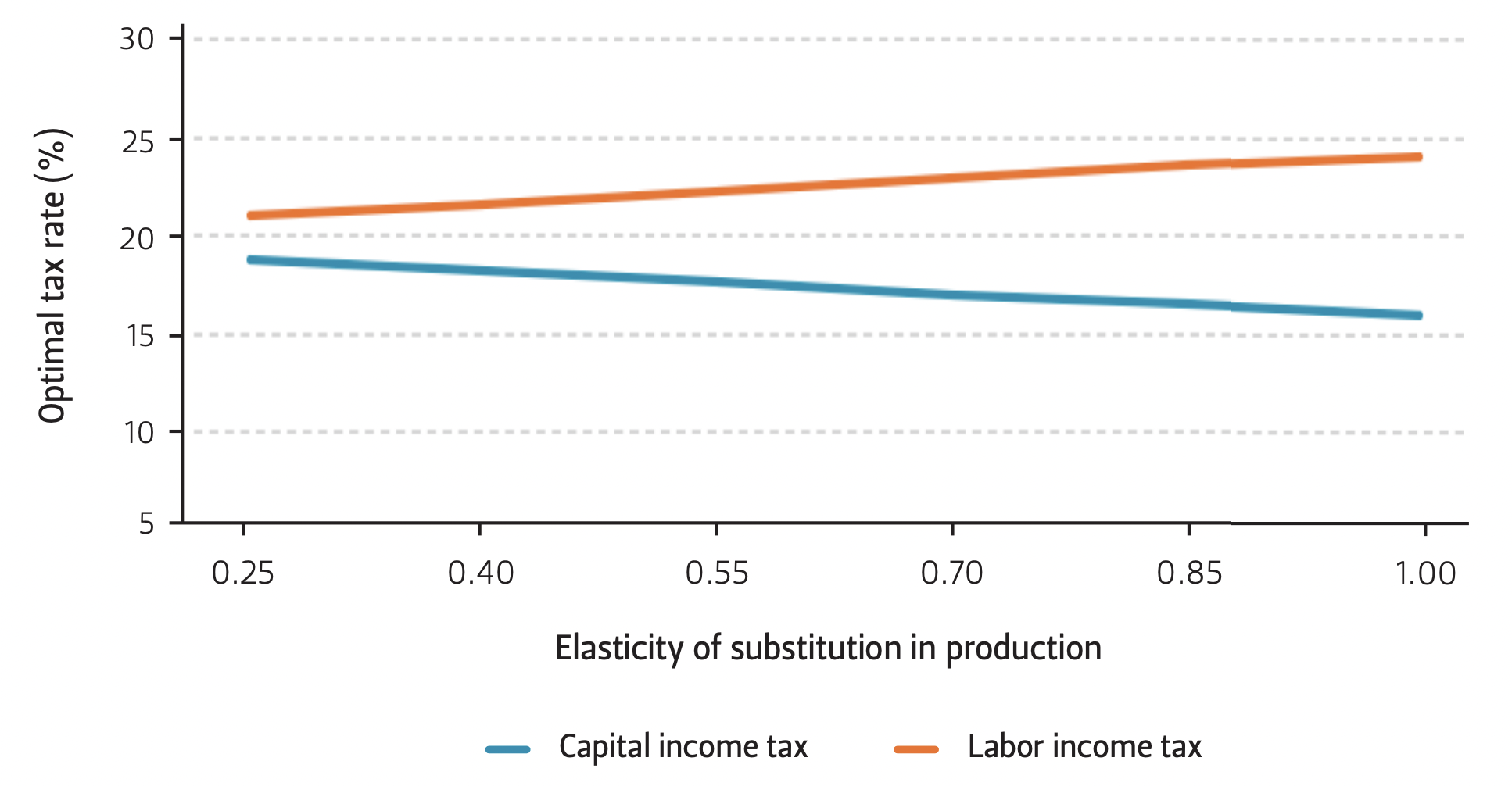

While immobile capital investments, particularly foreign-owned immobile investments, may motivate source-based capital income taxation, the computational model also illustrates the costs associated with this approach. With mobile capital investment, taxing capital income can drive out investment and distort domestic production. A key parameter that determines the extent of this distortion is the elasticity of substitution in production. This elasticity reflects how easily firms can adjust production inputs in response to changes in their market prices, and thus the extent to which the mix of inputs used in production changes in response to taxation. As Figure 4 illustrates, the optimal capital income tax rate falls as the elasticity of substitution in production increases.

Figure 4 — Optimal Taxation and the Elasticity of Substitution in Production

Source Authors’ analysis.

Conclusion

In this brief, we review the arguments for and against a source-based capital income tax—a tax on capital income based on the location of investment. We show that to the extent that domestic capital is immobile, a source-based capital income tax can be relatively non-distortionary. In this case, source-based capital income taxes may be preferable to other forms of taxation, particularly if the immobile capital is owned by nonresidents. However, given recent increases in capital mobility and in income shifting that have occurred with increasing globalization of the international economy, the effects of the taxation of the income earned by mobile capital, especially returns to highly profitable firm-specific capital that may be subject to income shifting, have been the focus of recent tax reform efforts in the United States and elsewhere. We show that as the proportion of capital that is mobile increases, capital income taxation becomes increasingly costly, and other taxes, such as labor income taxes, become more desirable. Accounting for these arguments in a simulated model of an open economy, we demonstrate that there is no universal prescription for the optimal taxation of capital income.

Instead, the simulation model reveals that optimal tax rates can vary widely based on the economic characteristics of the host country as well as the nature of the tax system of the home country of the investing firms. Consequently, policymakers must choose capital income tax rates based on the specifics of their domestic economy, paying attention to the mobility of capital, the flexibility of domestic production, the extent of foreign investment, and the home-country tax systems that apply to these foreign investors.

References

Clausing, Kimberly A. 2016. “The Effect of Profit Shifting on the Corporate Tax Base in the United States and Beyond.” National Tax Journal 69 (4): 905-934.

McKeehan, Margaret K., and George R. Zodrow. 2017. “Balancing Act: Weighing the Factors Affecting the Taxation of Capital Income in a Small Open Economy.” International Tax and Public Finance 24 (1): 1-35.

Organisation for Economic Co-operation and Development. 2013. “Addressing Base Erosion and Profit Shifting.” Paris: OECD.

Tax Foundation. 2016. “Corporate Income Tax Rates around the World, 2016.” Washington, D.C. https://taxfoundation. org/corporate-income-tax-rates-around-world-2016/.

Zodrow, George R. 2010. “Capital Mobility and Capital Tax Competition.” National Tax Journal 63 (4): 865-901.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.