Author(s)

Over the last three years, the U.S. has experienced several significant pandemic-driven economic rollercoasters that would typically have taken place across several decades. These include the highest unemployment rate since the Great Depression, the shortest recession ever recorded, a series of massive government policy responses, and a rapid recovery from the brief recession — all followed by the highest inflation rates since the 1980s, subsequent rounds of Federal Reserve interest rate increases, and, in 2023, worries for a looming new recession. While these unprecedented waves of economic events have certainly shifted U.S. consumer behaviors, whether they are cause for significant future concern is unclear.

This issue brief reviews recent U.S. consumer spending, saving, and credit use trends, including something old (the patterns we are familiar with), something new (the phenomena that have developed recently), and something borrowed (the outlook for consumer credit markets). Finally, the brief concludes with steps that concerned consumers can take to prepare for future economic uncertainties and policy developments.

Something Old: Credit Card Usage Remains High

Gross domestic product (GDP) is a common way to measure the size of a nation's overall economy.[1] Not surprisingly, U.S. GDP contracted during the pandemic before subsequently rebounding. Among all components of GDP, household consumption has regularly been the largest. Over the last two decades, consumption has remained not only a dominant factor but also a consistent one — the size of the U.S. economy decreases and expands over the business cycle, but consumption has always accounted for about two-thirds of U.S. GDP.[2] In other words, consumers are the backbone of the U.S. economy.

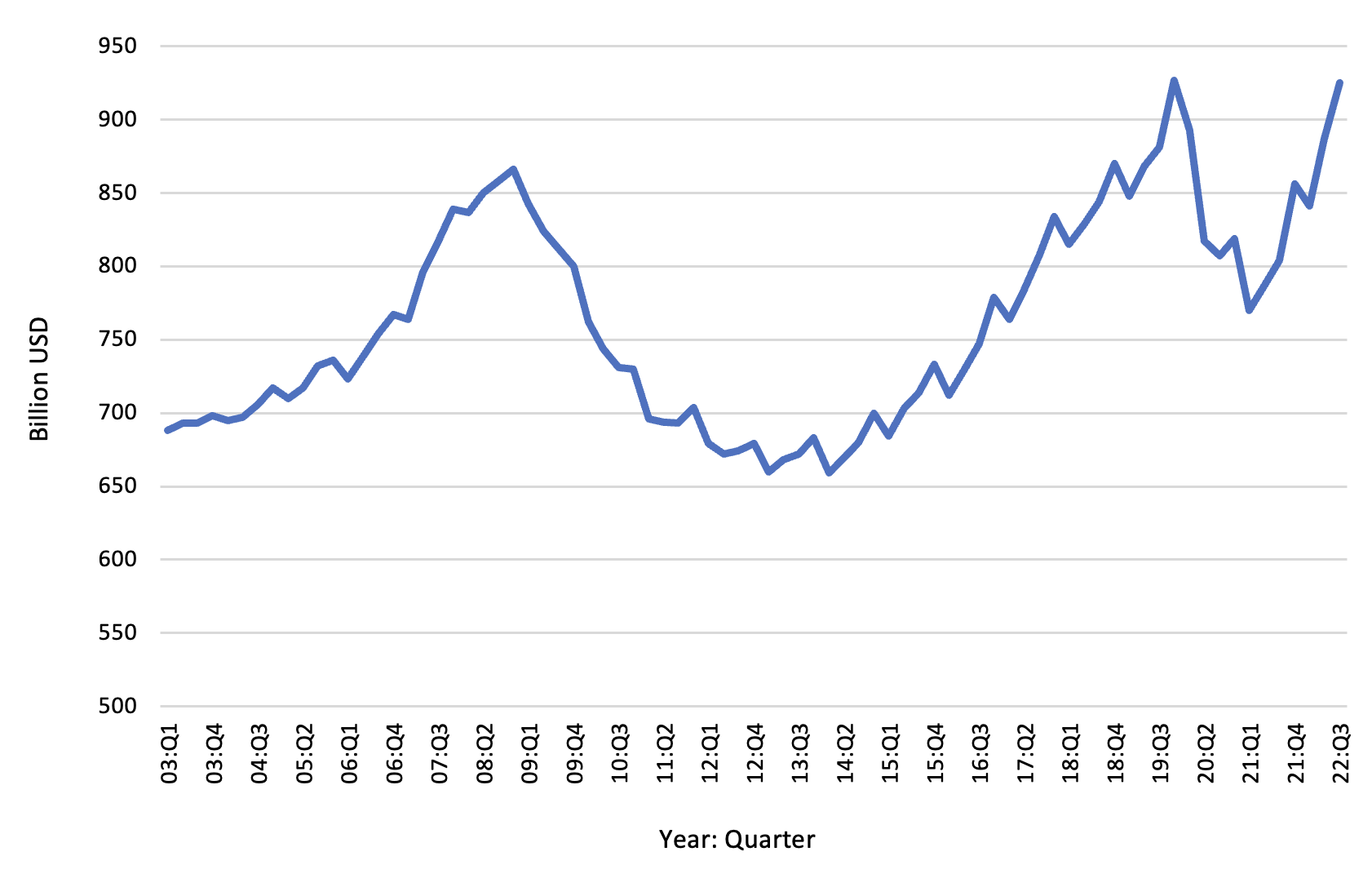

Credit card usage remains a major payment method for U.S. consumers.[3] According to a survey from the Federal Reserve Bank of New York, the application rate for credit cards among survey respondents had already returned to the pre-pandemic level by mid-2022.[4] In addition, consumer credit card balances surged by 15% year-over-year in the third quarter of 2022, the largest increase in more than two decades. [5]

It is not news that U.S. consumers carry credit card balances, but the high growth rate is astonishing given that the average interest rate on credit card borrowing has climbed above 19%.[6] From a glass-half-full perspective, it may appear that U.S. consumers are optimistic about the economy and confident about their financial conditions. However, some observers caution the situation may not be entirely positive for several reasons.

Specifically, although the overall credit card application rate has surpassed the pre-pandemic level, the distribution of applications is not even across all consumer groups. The application rate for people with credit scores over 760 was higher than the pre-pandemic level, while consumers with credit scores below 680 had a lower application rate than before.[7] Worse, some experts speculate that inflation may have caused lower-income households to rely more heavily on credit cards to keep up with consumption. In addition, a separate Federal Reserve survey of lending officers showed about 40% of commercial banks have been gradually tightening lending standards for businesses and commercial real estate entities.[8] These restrictive lending terms for credit cards and other personal loans are likely to trickle down to consumers in 2023, although the pace may be slower.

Figure 1 — Credit Card Balance: 2003-2022

Something New: Saving Levels Are Up

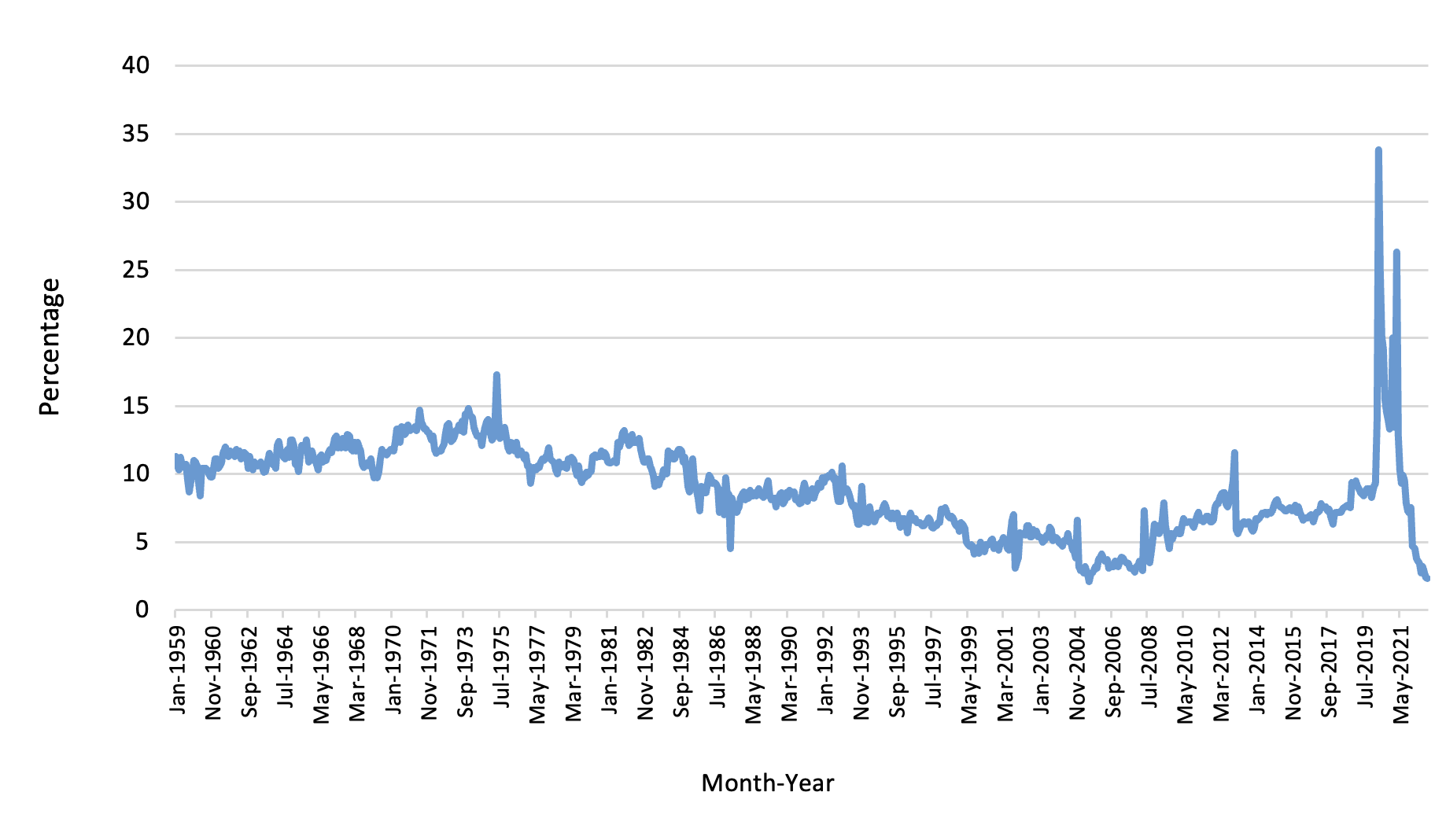

The U.S. personal savings rate declined throughout 2022 after a pandemic-driven surge in 2020. The personal savings rate — defined as the percentage of disposable income after paying taxes over total income — hit a historical low at 2.4% in September 2022, remaining stable in October 2022, rising to 2.9% in November.[9] The December level increased to 3.4%. In comparison, the personal savings rate averaged 7% for the most recent decade ending in 2019.

Some economists are concerned because the last time the savings rate hovered so low was in 2005, preceding the Great Recession. In addition, because the savings rate is defined as income remaining after paying for items such as food, clothing, shelter, electricity, and taxes, a low savings rate means consumers have limited discretionary funds left after paying for necessities. On the contrary, sizable savings usually serve as financial cushions that allow households to smooth their consumption during sudden drops of income such as job losses. In other words, ample savings make households more resilient to shocks.

Figure 2 — Personal Savings Rate: 1959-2021

The personal savings rate soared during the pandemic when consumers stayed home and were unable to spend. The subsequent funds from three stimulus checks, various government aid, mortgage forbearance, suspension of student loan repayment, and the strong stock market in 2021 provided extra resources for households, generating “excess savings.” According to the Federal Reserve, excess savings are essentially savings that were above what consumers would have saved, using the pre-pandemic trend as a baseline. [10]

The Federal Reserve estimated that through the summer of 2021, U.S. households accumulated $2.3 trillion in excess pandemic savings. These funds equipped consumers with greater spending power once the economy reopened — which some journalists vividly described as “revenge spending.”[11] This increased demand for more services and goods in turn fueled more hiring, a strong labor market, and low unemployment rates — but inflation followed.

As Sir Isaac Newton famously pointed out in physics, “What goes up must come down.” The same adage also applies to savings rate. As the pandemic began to recede and numerous government monetary support programs ended, households decumulated about a quarter of their excess savings between late 2021 and late 2022; however, they still possess a fair amount of excess savings, the Federal Reserve notes.

A noteworthy aspect of savings levels is that higher- and lower-income households accumulated these excess savings from different sources and at different magnitudes. According to the Federal Reserve, households in the lower half of the income distribution held $350 billion in excess savings, or an average of $5,500 per household as of mid-2022. The major sources of their excess savings were stimulus checks and other government relief funds. Most of these programs have already expired.

In contrast, households in the upper half of the income distribution held $1.35 trillion in excess savings as of mid-2022. The Federal Reserve indicated this group might not have changed their consumption behaviors much through 2021, because they did not benefit as much from stimulus checks as lower-income households. Instead, their excess savings mostly came from appreciation in housing values and a robust stock market. In other words, they began spending down their excess savings a little bit later than lower-income households did. Their excess savings were also bigger. These factors all gave this group a longer runway for using up their excess savings.

Financial industry experts predict consumers will exhaust their savings between the end of 2023 (for lower-income households) and the end of 2024 to 2025 (for upper-income households).[12] However, some observers — including the Federal Reserve — caution that these funds may not shield lower-income households through economic downturn for as long as the numbers show. This group’s excess savings mostly came from stimulus checks, but they may have already used the funds to pay down debts or invested in other assets. In other words, although these funds still appear on household balance sheets, the corresponding new assets (or reduction of liabilities) may not be as liquid as savings account funds, should households need immediate cash.

Something Borrowed: Delinquencies Confound, Interest Rates Increase

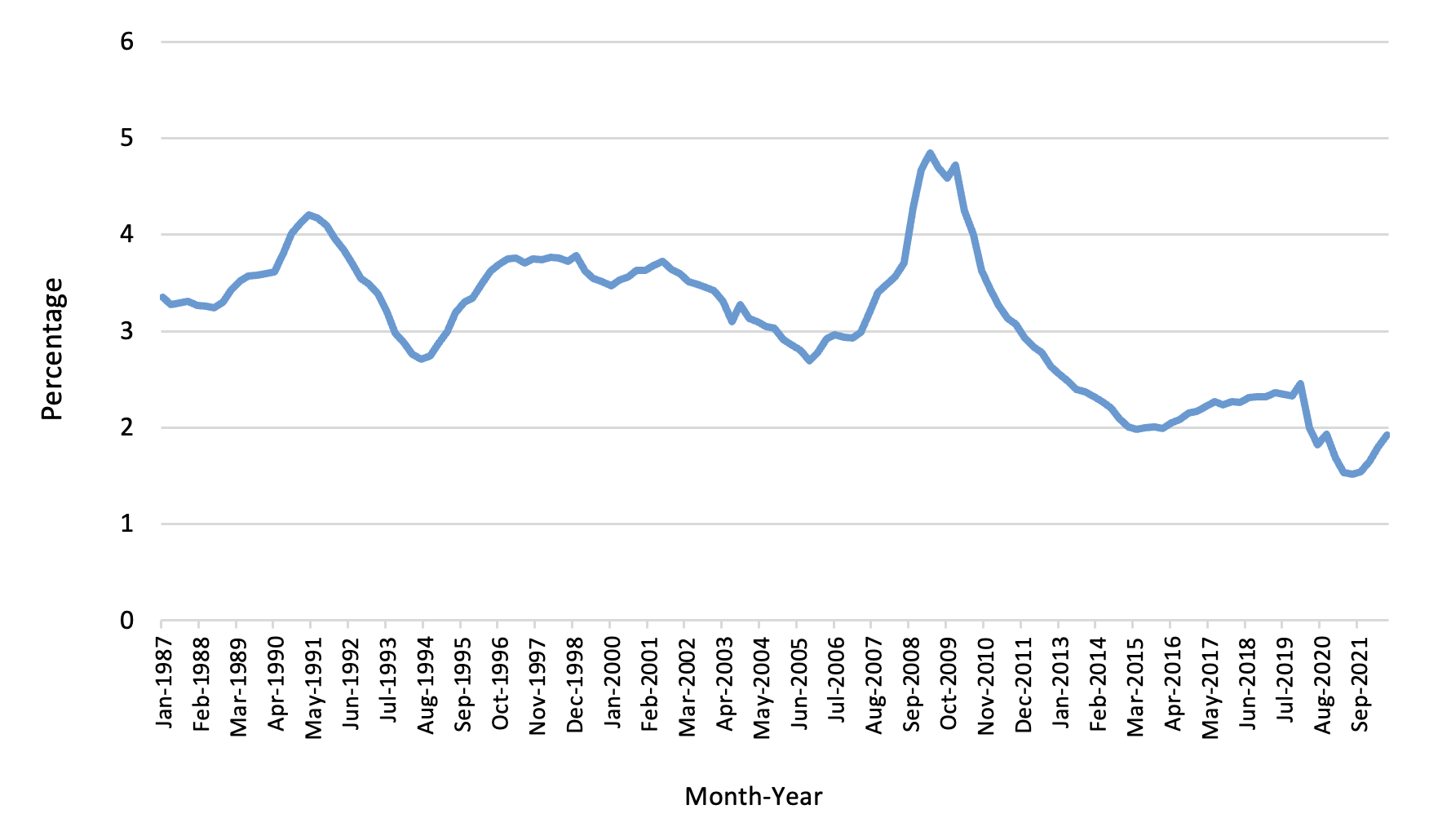

In its December 2022 forecast, TransUnion, a major credit rating agency, predicts that consumer loan delinquencies will surge in 2023.[13] Specifically, TransUnion believes that delinquencies of credit card payments will increase from 2.1% in 2022 to 2.6% by the end of 2023, a 24% increase. Unsecured personal loan delinquencies are also forecast to increase, from 4.1% to 4.3% over the same period, while both personal loan and credit card payments will likely witness the highest delinquencies since 2010.

Because delinquency rates usually reflect the overall health of the economy, they are seen as indicators regarding how close the economy is to approaching a turning point. As such, some practitioners believe an increased delinquency rate is an alarming signal. For instance, during the Great Recession, the credit card payment delinquency rate was 4.77%. During the short-lived 2020 recession, the delinquency rate was roughly 2.5%, which is comparable to the delinquency rate TransUnion has forecast for 2023.

Others do not think that overall consumer financial health is highly concerning. In mid-2021, the delinquency rate reached a record low of 1.47%. This was attributable to government pandemic response programs and the lack of spending opportunities. During the first three quarters of 2022, delinquency rates were about 1.65%, 1.80%, and 1.92%, respectively. The ratios were trending up, but they were still below the long-term average of 3.06%.[14] As such, more optimistic observers believe that the economy is not yet at the brink of recession.

Figure 3 — Consumer Delinquency Rates (30+ Days Past Due): 1987-2021

The recent Federal Reserve actions of increasing interest rates have definitely affected some types of credit more than others. The most affected ones include unsecured personal loans, consumers who have borrowed at variable rates (e.g., through a Home Equity Line of Credit) and those who are currently seeking loans.[15] As anticipated, the application rates for mortgage refinancing plummeted this year, dropping from 21.4% in October 2021 to 8.9% in October 2022.[16] Mortgage loan application rates also declined to 6.7% in October 2022 from 8.5% in October 2021.

The Federal Reserve takes a more optimistic view and states that increasing, but still low, credit card payment delinquency rates are consistent with the gradual draw-down of excess savings that households accumulated during the pandemic. Today, household balance sheets in the bottom half of the income distribution are still relatively healthy. However, the decumulation of savings will not last forever and households do need to plan for future financial turbulences.

Should We Be Blue? Steps Concerned Consumers Can Take

American consumers have witnessed several conflicting trends in recent years. On the one hand, high inflation and increasing interest rates have created economic headwinds, causing concerns of recession and debates among economists as to whether a soft landing is likely.[17] On the other hand, recent consumer savings and credit card application statistics do not support the inevitability of an economic downturn.

These seemingly incompatible patterns have a lot to do with the excess savings U.S. households accumulated over the last three years as well as the distribution of these extra funds. Recent studies show that if a recession happens, lower-income households may not be as prepared as higher-income households, primarily because these households have smaller amounts of excess savings and draw them down faster. In addition, their credit card balances are increasing more rapidly, and the government programs that funded their excess savings during the pandemic have mostly stopped.

In response, experts suggest that households begin to tighten up spending and save more. For instance, the tried-and-true financial planning advice of paying off the highest interest debt first is especially meaningful in the current environment. From a policy perspective, the last-minute omnibus government-spending package that passed in December 2022 included legislation that provides tax-favored saving mechanisms for both retirement and emergency saving accounts.[18] Consumers should take advantage of these tax advantages. In short, while the labor market is still robust, improving the management of household finances may well be the perfect New Year’s resolution for many consumers.

Endnotes

[1] The formal definition of GDP is the “value of the goods and services produced by the nation's economy less the value of the goods and services used up in production. GDP is also equal to the sum of personal consumption expenditures, gross private domestic investment, net exports of goods and services, and government consumption expenditures and gross investment.” See Bureau of Economic Analysis, “News Release: Definitions,” November 30, 2022, https://www.bea.gov/news/2022/gross-domestic-product-second-estimate-and-corporate-profits-preliminary-third-quarter.

[2] Bureau of Economic Analysis, “National Income and Product Accounts,” last visited January 13, 2023, https://apps.bea.gov/iTable/?reqid=19&step=2&isuri=1&categories=survey.

[3] “Findings from the Diary of Consumer Payment Choice,” Federal Reserve Bank of San Francisco, June 23, 2022, https://edubirdie.com/blog/findings-from-the-diary-of-consumer-payment-choice.

[4] Federal Reserve Bank of New York, “Survey of Consumer Expectations Credit Access Survey: Credit Cards Demand Persists Despite Overall Slowdown,” November 21, 2022, https://www.newyorkfed.org/microeconomics/sce/credit-access#/experiences-credit-applications9.

[5] Federal Reserve Bank of New York, “Household Debt and Credit Report: Q3 2022, Total Household Debt Rises to $16.51 Trillion on Higher Mortgage, Credit Card Balances,” November 2022, https://www.newyorkfed.org/microeconomics/hhdc.

[6] Alexandre Tanzi and Jonnelle Marte, “US household Debt Jumps Most Since 2008 Even as Card Rates Surge,” Bloomberg, November 15, 2022, https://www.bloomberg.com/news/articles/2022-11-15/us-household-debt-jumps-most-since-2008-even-as-card-rates-surge.

[7] Jonnelle Marte, “US Consumers Are Still Applying for Credit Cards Despite Higher Rates,” Bloomberg, November 21, 2022, https://www.bloomberg.com/news/articles/2022-11-21/us-consumers-applying-for-credit-cards-despite-higher-rates.

[8] Board of Governors of the Federal Reserve System, “Senior Loan Officer Opinion Survey on Bank Lending Practices: October 2022,” November 7, 2022, https://www.federalreserve.gov/data/sloos/sloos-202210.htm.

[9] Bureau of Economic Analysis, “Personal Savings Rate,” last visited February 1, 2023, https://www.bea.gov/data/income-saving/personal-saving-rate.

[10] Aditya Aladangady, David Cho, Laura Feiveson, and Eugenio Pinto, “Excess Savings during the COVID-19 Pandemic,” Board of Governors of the Federal Reserve System, October 21, 2022, https://www.federalreserve.gov/econres/notes/feds-notes/excess-savings-during-the-covid-19-pandemic-20221021.html.

[11] Andrea Felsted, “Retailers Should Prepare for a Revenge Christmas,” Bloomberg, October 10, 2022, https://www.bloomberg.com/opinion/articles/2022-10-07/2022-might-actually-be-the-year-of-revenge-christmas-for-consumer-economy#xj4y7vzkg.

[12] Peter Coy, “We Can’t Keep Spending Like This,” The New York Times, December 2, 2022, https://www.nytimes.com/2022/12/02/opinion/saving-rate-decline-economy.html.

[13] TransUnion, “2023 Consumer Credit Forecast,” December 14, 2022, https://newsroom.transunion.com/2023-consumer-credit-forecast/.

[14] Board of Governors of the Federal Reserve System, “Charge-Off and Delinquency Rates on Loans and Leases at Commercial Banks,” November 23, 2022, https://www.federalreserve.gov/releases/chargeoff/delallsa.htm.

[15] Chris Horymski, “Debt Delinquency Rates Are Rising, but Still Near Historic Lows,” Experian, September 26, 2022, https://www.experian.com/blogs/ask-experian/research/delinquency-rates/.

[16] Federal Reserve Bank of New York, “Survey of Consumer Expectations Credit Access Survey: Credit Cards Demand Persists Despite Overall Slowdown.”

[17] For the debate about the likelihood of a soft landing, see (1) Jeff Horwich, “U.S. Job Marching Holds Up, Keeping a Soft Landing in Sight,” Federal Reserve Bank of Minneapolis, December 1, 2022, https://www.minneapolisfed.org/article/2022/us-job-matching-holds-up-keeping-a-soft-landing-in-sight, and (2) Max Zahn, “What ‘Soft Landing’ Means for the Economy and the Chances It Will Happen,” ABC News, December 13, 2022, https://abcnews.go.com/Business/soft-landing-means-chances-happen/story?id=94086706.

[18] Erica York and Garrett Watson, “Improved Tax Treatment of Saving Included in Year-End Federal Spending Deal,” Tax Foundation, December 21, 2022, https://taxfoundation.org/omnibus-federal-spending-bill-retirement-savings-tax/.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.