Author(s)

This paper is a work in progress and has not been through editorial review. It also appears in the University of Cambridge’s Energy Policy Research Group’s working paper series as EPRG 2217. View the full working paper (PDF).

Non-technical Summary

Saudi Arabia told the world in 2021 that it would strive for “net zero” greenhouse gas emissions by 2060, giving the kingdom 39 years to transform one of the earth’s most emissions intensive societies. At nearly 600 million tonnes, Saudi Arabia’s domestic carbon dioxide emissions in 2020 ranked ninth in the world, just behind South Korea and ahead of Canada. On a per capita basis, Saudi Arabia emits more CO2 than even the United States—17 metric tons a year versus 14 in the US—on average incomes just 75% as large.

But Saudi Arabia also has numerous advantages in decarbonization. The kingdom has an enormous resource base in renewable energy and feedstocks for clean fuels, as well as vast reservoirs of geological pore space that can be used for storing carbon. It has concentrated emissions sources that are clustered in close proximity to geological storage. Saudi firms and universities hold an impressive reservoir of human engineering talent and demonstrated expertise in transporting and converting energy, and in leveraging geology. The Saudi government also has a high level of funding and policymaking autonomy without veto wielders.

Combined, these factors provide a strong competitive advantage in carbon reduction. If it achieves a modest level of domestic success, the kingdom could later market carbon storage or offsetting services for other governments with fewer such attributes.

This paper lays out one potential step-by-step path toward decarbonizing Saudi Arabia, imagining a sweeping restructuring of a fossil fuel-driven society and economy. Transformational changes would alter energy consumption, electricity generation and storage, transportation and industrial operations. Many reforms made under the aegis of the Saudi “net zero” goal would serve other useful but unrelated purposes.

The paper also examines the credibility of the net-zero announcement and desirability of decarbonization for the Saudi regime and economy. What does Saudi Arabia gain by joining a movement that ostensibly seeks to end the combustion of oil, Saudi Arabia’s main export commodity and the source of roughly 80% of its government budget? As recently as the 2021 COP 26 in Glasgow, delegates from Saudi Arabia (among others) lobbied a UN committee to temper language urging a swift transition to cleaner energy.[1] That same year the Saudi oil minister vowed that his country would produce “every molecule” of its oil and gas reserves.[2] Are such actions compatible with the kingdom’s net zero goal?

And, given that prior grandiose energy initiatives were shelved soon after announcement, how seriously should observers treat the Saudi net zero commitment? At minimum, determining the regime’s level of compliance will require taking stock of whether Saudi Arabia reaches interim milestones toward the 2060 goal.

The Saudi government’s declaratory embrace of domestic decarbonization does not necessarily signal a change in climate strategy. Policymakers in the kingdom appear comfortable advocating diverging climate policies for Saudi Arabia, on the one hand, and for the rest of the world on the other.

Ultimately, the reward for successful implementation of Saudi Arabia’s Net Zero 2060 ambition could establish the kingdom as a credible player in the global climate arena, revitalizing the kingdom’s influence and allowing Saudi policymakers to shape the energy transition in ways that could retain a greater long-term role for hydrocarbons.

Abstract

Saudi Arabia’s stated goal of reaching net zero by 2060 puts the kingdom in a paradoxical position. The Saudi leadership proposes to decarbonize an oil-intensive society and economy while selling oil to the world. As such, the credibility of the Saudi commitment will remain an open question until concrete progress toward restructuring the kingdom’s energy system is demonstrated. Modest initial steps toward net zero include investments in renewables alongside pricing reforms of energy products and services. Another ongoing push involves oil-to-gas switching in the kingdom’s power sector, which can be augmented by carbon capture and storage and, eventually, gas-to-hydrogen substitution. Doubts and difficulties aside, Saudi Arabia holds major advantages in decarbonization. These include unused land with copious solar radiation, as well as geological storage near carbon emissions clusters. The kingdom is also equipped with relevant knowledge and investment capital. Fully compensating for reduced oil export rents may not be possible if worldwide carbon neutrality plans come to fruition. Despite the short-term benefits of high energy prices after the Russian invasion of Ukraine, economic and geopolitical decline is a likely medium-term outcome for the kingdom. However, there are also opportunities including replacing oil revenues with those arising from carbon disposal for countries and firms lacking the kingdom’s competitive advantages.

Introduction

In October 2021, Saudi Arabia told the world it would eliminate or offset its greenhouse gas emissions by 2060, adopting the same “net zero” target date as governments in China, Russia, Indonesia and Nigeria. A year earlier, the kingdom’s national oil company, or NOC, Saudi Aramco, announced it would decarbonize its own operations even earlier, by 2050.[3]

The gargantuan task of decarbonizing Saudi Arabia is evident in a few simple statistics. A country that ranked 41st in the world by population and 20th by economic activity consumed more oil in 2020 than any country outside the United States, China and India. On a per capita basis, Saudi Arabia emits more CO2 than the United States—17 metric tons a year versus 14 in the US—on average incomes just 75% as large.

A serious program to decarbonize Saudi Arabia would impose a sweeping restructuring of a fossil fuel-driven society and economy in less than four decades. Transformational changes would alter energy consumption, power generation and storage, transportation and industrial operations.

The Saudi government has hinted at its decarbonization path, with government statements and reports mentioning initiatives, favored technologies and investment targets. This paper extrapolates from those hints to lay out a plausible path toward decarbonizing Saudi Arabia’s energy and emissions systems. This work also examines potential secondary effects on the kingdom, as well as its competitive advantages and disadvantages.

Briefly stated, a net zero program might see demand-side reforms revoking fuel and utility subsidies, driving efficiency gains and technology switching, some of which would be legally mandated. The Saudi transport sector might shift toward electric vehicles, trading petroleum fuels whose export underpins the economy for a network of charging stations.

On the supply side, the transformation would push oil from the kingdom’s electricity generation sector, replacing it with new solar and perhaps nuclear power plants alongside electricity storage. An expansion of the power grid would supply the transport sector and extend electrification to replace fossil fuels in industry.

Desalination plants, refineries, petrochemical plants and other emitters in the kingdom’s industrial zones would see their emissions captured, compressed and piped to underground storage, perhaps in depleting oilfields or in vast aquifers below the western half of the Arabian Peninsula. Longer term, carbon capture would facilitate replacing natural gas with low-emission fuels based on hydrogen, including ammonia and methanol.

The reward for successful implementation of Saudi Arabia’s Net Zero 2060 ambition could be significant. A kingdom struggling to retain geostrategic importance as the world’s central banker of oil would leverage domestic decarbonization to establish credibility in the global climate arena, revitalizing the kingdom’s influence and allowing Saudi policymakers to shape the energy transition in ways that could retain a greater long-term role for hydrocarbons.

Saudi Aramco’s 2021 sustainability report suggests such an ambition. “Developing low-carbon products and solutions helps to sustain and diversify demand for oil and gas through competitive technologies,” the report states.[4]

Net zero success might also be economically counterproductive. A vigorous decarbonization push by Saudi Arabia could inspire other petrostates to pursue dramatic reductions of their own, perhaps making a more serious effort than some governments may find optimal. More broadly, any encouragement by Saudi Arabia toward decarbonization could inspire reductions in oil combustion outside the kingdom, which, all else constant, would reduce oil prices and rent flows to the kingdom. Therefore, a Saudi role that motivates global momentum toward climate action might be viewed negatively inside domestic policymaking circles.

For this reason and others, it remains possible that the Saudi leadership will not earnestly pursue its commitment to full decarbonization. Credibility of past Saudi environmental policy declarations has been lacking, which suggests a level of comfort with disregarding official targets. For instance, the Saudi government did not pursue a 2012 announcement to build 23.9 GW of renewables by 2020, nor a 2018 memorandum of intent to build 150-200 GW of renewables by 2030; while a 2011 plan to build 16 nuclear power reactors within 20 years was also shelved. [5] As of mid-2022, Saudi Arabia reported an renewables installation of just 700 megawatts.[6]

Decarbonization commitments of other regional governments have had mixed effects on energy policy. The UAE’s net zero goal appears to have led Dubai’s utility to convert the just-built Hassyan coal-fired power plant to run on natural gas.[7] But Turkey’s decarbonization commitment does not seem to be constraining policy. Ankara’s ongoing expansion of its coal-fired power generation was unaffected by President Erdogan’s declaration of intent to reach net zero by 2053.[8]

Therefore, any demonstrated lack of determination by Riyadh in pursuit of its decarbonization goals might also signal to other oil-exporting governments that climate commitments need not be adhered to in the near term.

Only by observing interim progress can the sincerity of the Saudi net zero commitment be determined. One milestone comes in 2030, the date by which the kingdom has pledged to reach its Paris Agreement goal of a reduction of 278 million tonnes of CO2 per year (below a 2019 baseline of 580 million tonnes).[9] Some $187bn has been earmarked toward 2030 climate targets including GHG reduction.[10]

Inherent Contradictions

The specter of the world’s premier petrostate making a serious bid at full decarbonization is not without its contradictions. Saudi Arabia’s net zero pursuit comes alongside plans to ramp up production and export of oil, the source of more than a third of the world’s fuel-based emissions.[11] Saudi Aramco in 2020 announced capital investment aimed at boosting production capacity from 12 to 13 million barrels per day by 2027. [12] Leadership messaging on the energy transition has been mixed. Regular statements underscore the view that fossil fuels must remain a key part of the future energy mix and oppose a global transition away from fossil fuels.

Saudi Arabia’s updated Paris climate pledge, or NDC, more than doubles its emissions reduction target to 278 million tonnes of C02 equivalent through massive installations of renewable power and hydrogen production along with efforts to capture and sequester emissions. But the document also exemplifies the policy dichotomy, declaring that cutting Saudi emissions by 2030 is contingent upon “a robust contribution from hydrocarbon export revenues to the national economy.”[13] And, as mentioned above, Aramco states that it seeks to leverage transition technologies to “sustain and diversify demand for oil and gas.”[14]

Clearly, the kingdom’s planners are counting on oil and oil-based products remaining important exports for decades. This is borne out by forecasts depicting a long and slow energy transition. Even scenarios modeling a rapid transition retain demand for oil as a petrochemical feedstock and fuel for heavy and specialized transport. Saudi Arabia’s Paris NDC makes no suggestions for abating or mitigating combustion emissions from the kingdom’s oil exports.

Further contradictions are evident in contrasting attitudes toward an energy transition inside versus outside the kingdom. There are numerous tangible benefits from a major shift to renewables inside the kingdom. Replacing carbon-based power and transportation with cheaper clean electricity allows for increased hydrocarbons exports and revenues, since domestic oil and gas consumption is heavily subsidized and exports are priced on global benchmarks. Indeed, several utility scale renewables installations were under construction, as will be discussed. Reducing subsidies and imposing other market-based economic reforms remains attractive regardless of decarbonization goals.

Outside the kingdom, however, a transition from combustible fuels to clean electricity—coupled with efficiency mandates and bans on internal combustion engine vehicles—threatens Saudi Aramco’s oil income. If no replacement is found for oil’s contribution to the Saudi government budget, usually between 80% and 90% of the total, the kingdom’s patronage-based governance model will be undermined.

In 2022, however, that was not the case. The Russian invasion of Ukraine and a stronger-than-expected pandemic recovery provided Saudi Aramco with record revenues of nearly $88 billion in the year’s first half, including nearly $1 billion per day in the spring.[15] Longer term, however, changes in vehicle propulsion promised by automakers and nearly three dozen national governments look likely to shave down oil demand (although one 2019 estimate suggests a worldwide ban on ICE engines in light vehicles would only cut oil demand by around 15 million b/d).[16]

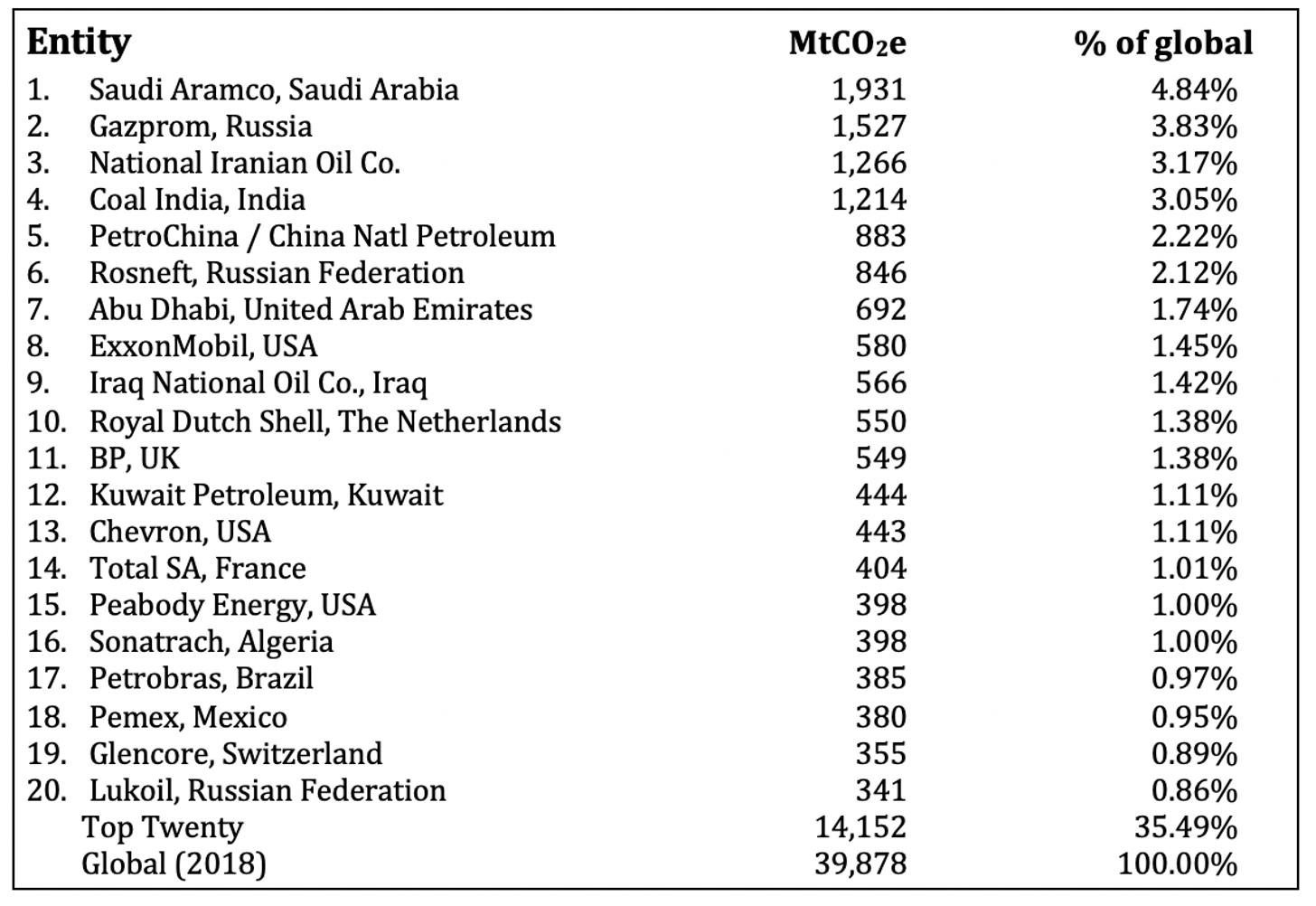

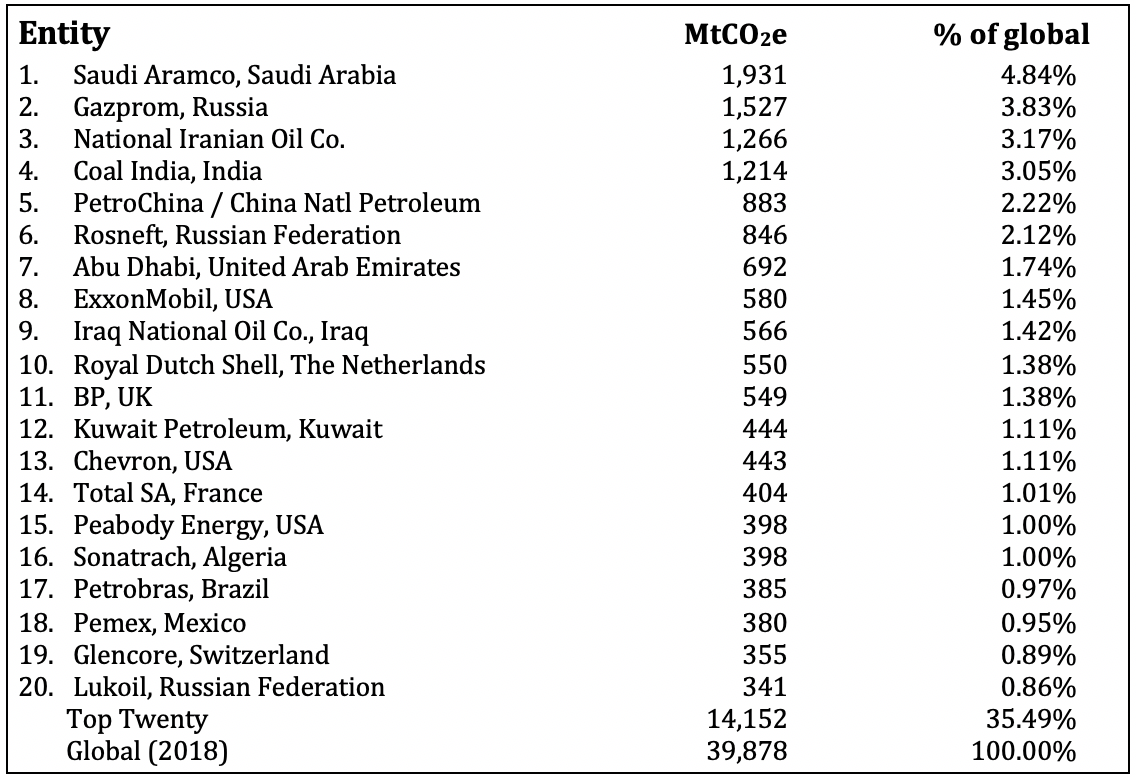

Within Saudi Aramco a similar internal-external conflict is apparent. Saudi Aramco is the largest single commercial entity producing carbon-based fuel in the world. (Fig. 2, below) Combustion of Aramco’s oil and gas accounted for roughly 5% of global emissions in 2018,[17] and about 4% of total historic atmospheric accumulations since Saudi oil production began in 1938.[18] The success of global climate action hinges on halting or abating GHG emissions from combustion of oil and gas marketed by Saudi Aramco.

But abatement plans of Saudi Aramco ignore the so-called Scope 3 or combustion emissions. The plans focus on much smaller emissions from Aramco’s “wholly owned and operated assets” (Scope 1 and 2 emissions).[19]

Oil and gas production are the source of roughly 14% of GHG emissions within Saudi Arabia and Aramco has agreed to eliminate or offset those emissions by 2050. Such a commitment is aimed not at constraining the NOC’s business model but enhancing the competitiveness of Aramco’s oil exports. Carbon has emerged as a new arena for competition among global oil producers, particularly as global oil production plateaus and begins to decline.

“When it comes to oil and gas, the future now clearly belongs to the lowest cost, least-carbon intensive producers,” CEO Amin Nasser has stated. “We intend to be one of those producers.” [20]

Rent windfalls in 2022 provided capital for NOCs like Aramco to invest in reducing their emissions and providing clean energy for the domestic market. However, that did not appear to be happening.

NOCs with large resource bases had invested less in diversification and transition technologies than shareholder-owned counterparts. Research from Wood Mackenzie shows that, as of early 2022, Aramco had not announced any capital commitment to decarbonization or transitioning to clean energy.[21] (In 2021 Aramco’s $315 million in “sustainability” research amounted to a third of its R&D budget but just 1% of its $32 billion capital spending.[22]) The lack of decarbonization investment extended beyond Aramco to NOCs in Qatar, UAE, Iran, Algeria, Russia and Mexico. None of the world’s major state-owned oil firms had dedicated more than 5% of investment capital toward decarbonization or renewables. By contrast, shareholder-owned IOCs had allocated an average of 15% and European IOCs 20%.[23] Some IOCs have introduced net zero plans that go well beyond Aramco’s to include Scope 3 emissions.[24]

Investment allocations comprise another important indicator in tracking adherence to net zero commitments by Saudi Arabia and by Saudi Aramco.

Current GHG Emissions Accounting

The task of decarbonizing Saudi Arabia should not be underestimated. At nearly 600 million tonnes, Saudi Arabia’s domestic CO2 emissions in 2020 ranked ninth in the world, just behind South Korea and ahead of Canada. At 17 tonnes per capita, Saudi emissions were nearly quadruple the world average. As shown in Fig. 1 below, power generation accounted for 40% of the kingdom’s emissions, with another 40% from industry (including refining and petrochemicals) and the oil and gas sector. Transport added a further 19%, with the building sector contributing just 1%.[25]

Figure 1: Saudi CO2 emissions by sector since 1970

Figure 2: Top 20 global sources of fossil fuels and implied GHGs emitted during combustion in 2018.

Steps to Net Zero in Saudi Arabia

Hydrocarbon exporting and carbon-intensive economies are those most exposed to economic damage from the energy transition. The disruption involved in replacing fossil fuels with renewables and low- or zero-carbon substitutes is expected to be costly, particularly in the initial decades, before allowing for a potential return to profitability in later decades.[26]

The carbon intensity of the Saudi economy also presents policymakers with a number of inexpensive opportunities to reduce emissions while improving economic competitiveness. Chief among these is a reduction in oil use. In 2021, the kingdom consumed an average of 3.6 million barrels per day of oil and gas liquids.[27] Almost a third of that was burned to produce electricity, roughly 430,000 b/d of crude oil and 600,000 b/d of refined products, on average.[28] In most of the world, oil combustion in power generation was displaced decades ago by cleaner and cheaper substitutes. Expunging oil from the domestic power sector is attractive for reasons of competitive cost and efficiency, as well as environment.

How might a plan to reach net zero in the kingdom start? The following sections propose one potential pathway that begins with subsidy reform and efficiency improvements, then shifts toward decarbonizing power and transport. Further steps target the industrial and oil and gas sectors. Of course, retracting subsidies on energy products and services is politically difficult and could divert actual decarbonization to start elsewhere.

Eliminate Subsidies to Improve Efficiency

Under the net zero plan, subsidized energy prices inside the kingdom, serving to encourage fossil fuel consumption and emissions, will come under intense pressure for reform. The net zero goal aligns with already strong aspiration for rationalized prices and energy efficiency.

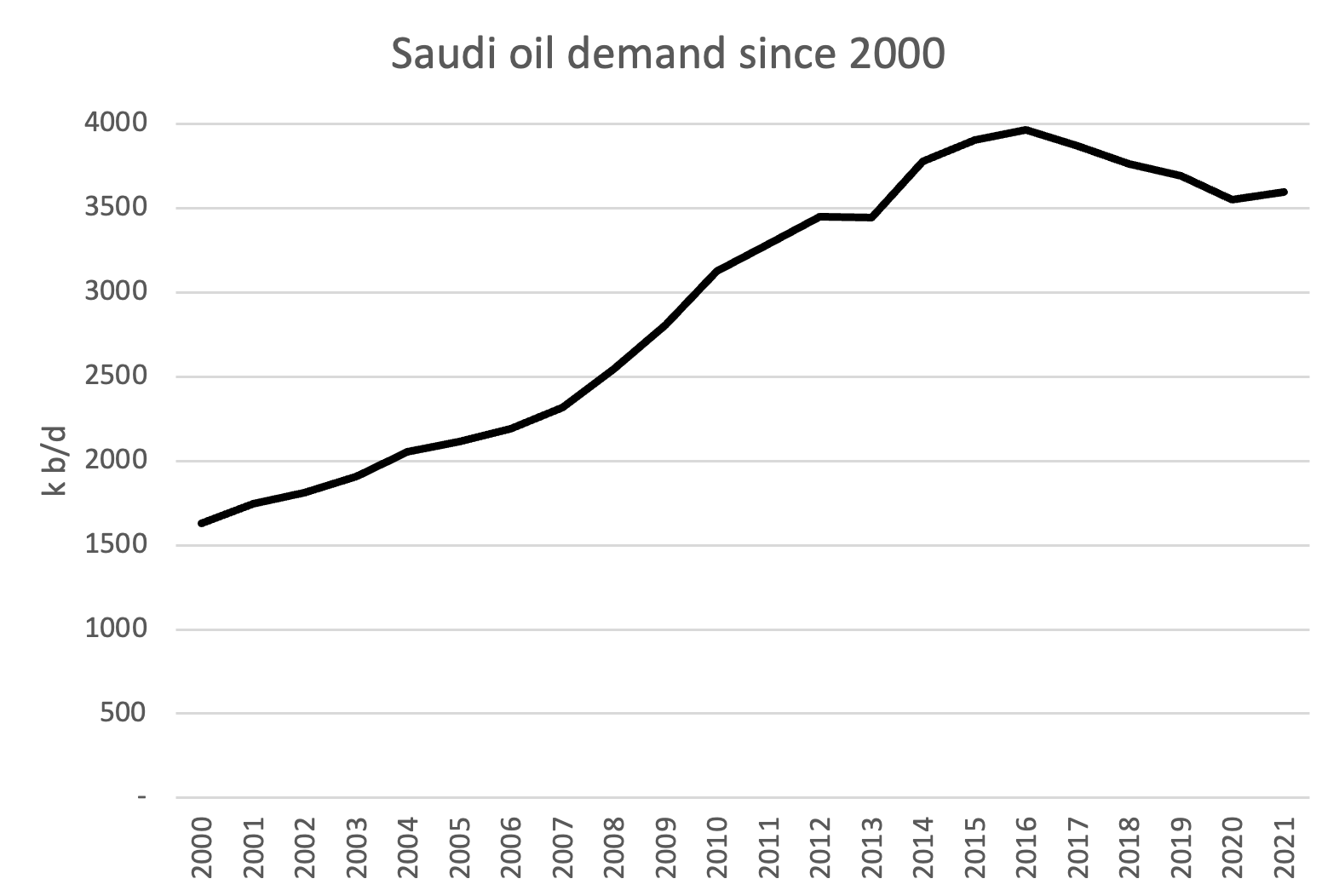

Major increases in administered prices were imposed in 2016 and 2018, which succeeded in dampening demand for transport fuels and electricity. Saudi demand for oil appears to have peaked in 2016 and dropped by almost 10%, or 367,000 b/d, through the end of 2021.[29] (Fig. 3)

Figure 3: Domestic demand for oil and natural gas liquids has slipped since subsidy reforms of 2016 and 2018

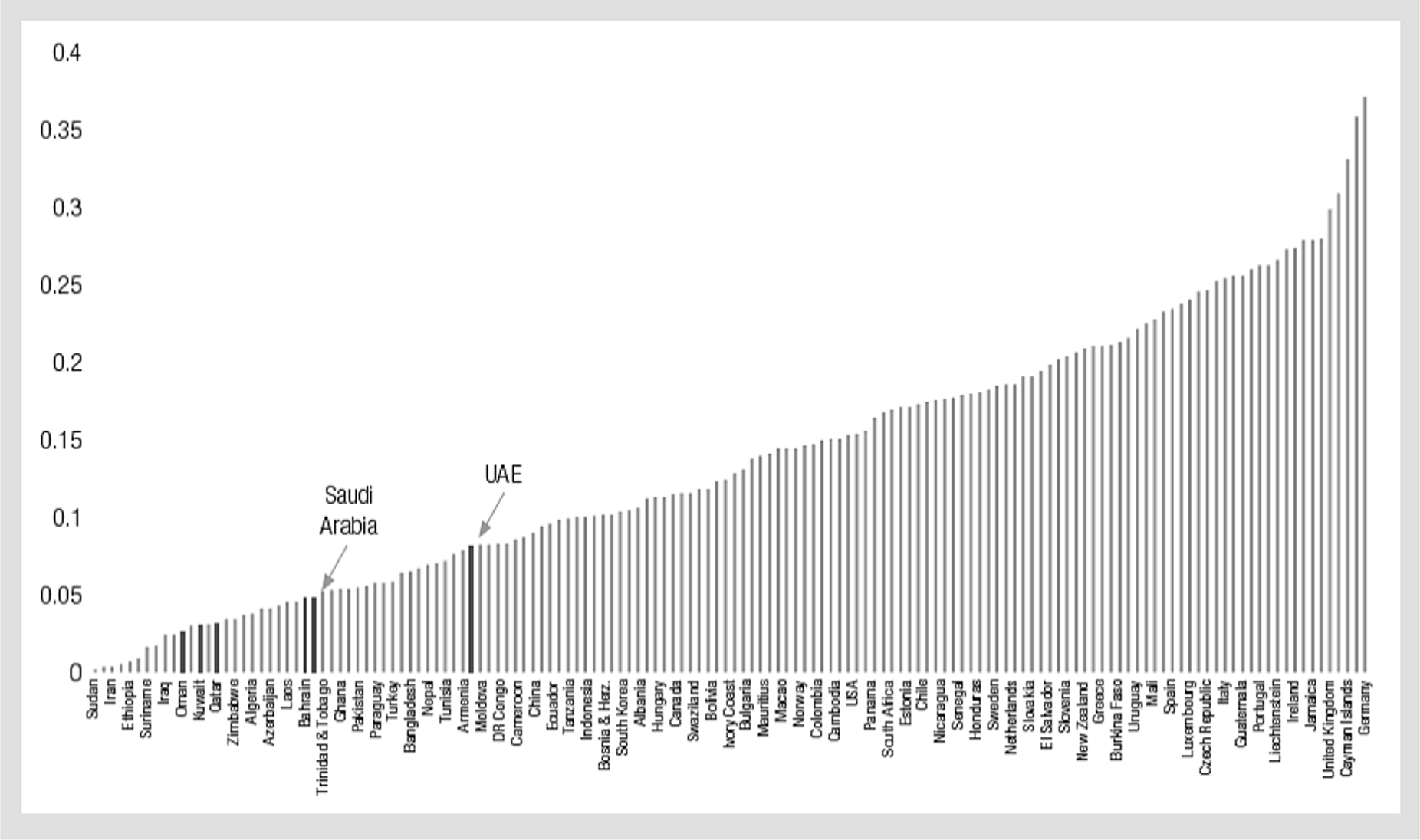

Saudi energy prices are still well below global averages. Saudi gasoline was cheaper in August 2022 than all but 18 other countries, averaging 62 US cents/liter ($2.35/US gallon). Diesel in the kingdom, at 17 cents/liter (63 cents/gal) was cheaper than everywhere except Libya, Venezuela and Iran. Residential electricity prices, starting under 5 US cents/kilowatt-hour, were a third of the US average and just 15% of those in Britain.[30] (Fig. 4)

Further increases would align Saudi energy prices closer to world prices, encouraging efficiency and technology switching. Higher prices would also reduce the financial penalty on Saudi Aramco for domestic sales. Weakening domestic demand would allow surplus oil to be exported at market prices or used as feedstock for higher value-added petrochemicals or fertilizer. While subsidy reforms are already a priority among Saudi technocrats,[31] public opposition has slowed implementation,[32] even with cash compensation under the Citizens Account Program.

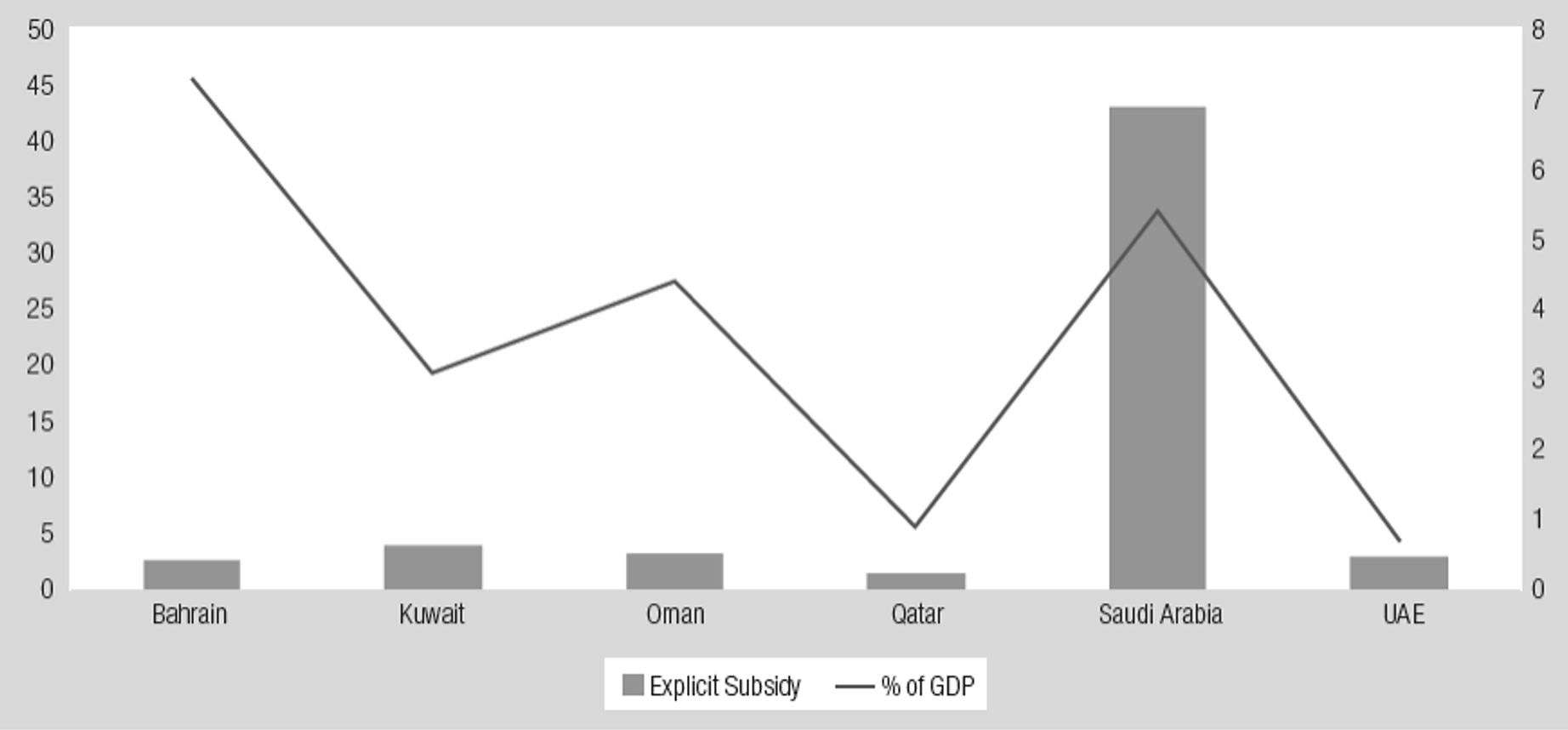

The Saudi net zero goal provides a rationale for further price increases, which could give policymakers political cover for reforms of distortionary subsidies valued at more than 5% of GDP. (Fig. 5) The IMF and World Bank have urged continued subsidy retractions, with the World Bank stating in 2022 that the energy efficiency improvements flowing from subsidy reforms are “the single most important element of moving to net zero emissions.”[33]

Figure 4: Power prices in US cents per kWh. Prices remained low by world levels in Saudi Arabia and its GCC neighbors (depicted in red), all of which were in the lowest quintile

Figure 5: Subsidized energy products and services (in USD billions, left axis) accounted for more than 5% of 2020 Saudi GDP (in % of GDP, right axis)

Power Sector Decarbonization

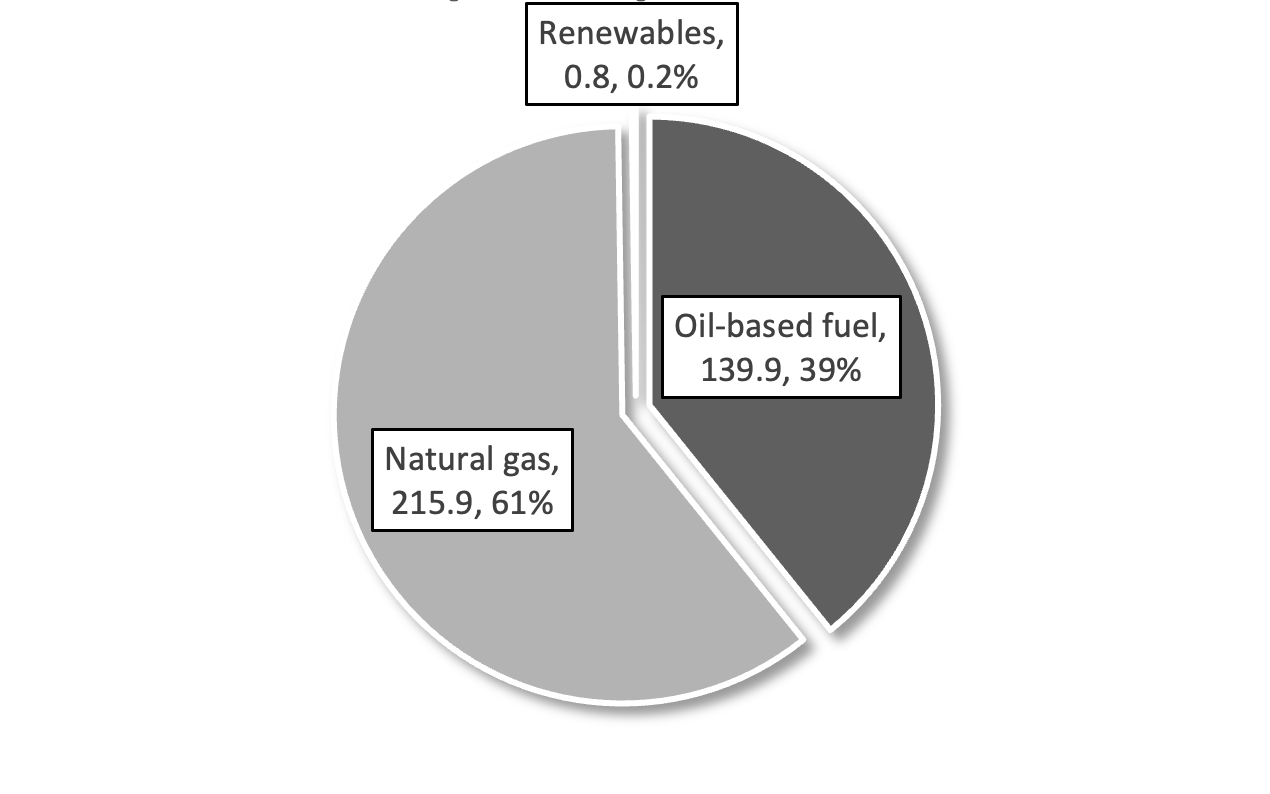

A sincere net zero plan would make an early effort to decarbonize the power sector, followed by a concerted shift in energy consumption away from direct fossil fuel combustion and toward electricity. As shown in Fig. 1, 40% of the kingdom’s emissions flow from power generation, split between natural gas (61%) and oil-based fuels including crude oil and heavy fuel oil comprising nearly all the rest. (Fig. 6) Further, some 70% of power production is used to cool buildings.[34]

Figure 6: Saudi Arabia generated 357 terawatt-hours of power in 2021, less than one TWh of which (about 0.2%) was generated using renewables.

Much of this decarbonization can be achieved from a massive expansion of renewables alongside oil-to-gas switching. Eventually, nuclear power could play a role. The kingdom’s comparative advantage in solar generation is well known. But Saudi Arabia is also home to uranium deposits that the government plans to leverage in a future nuclear power program.[35]

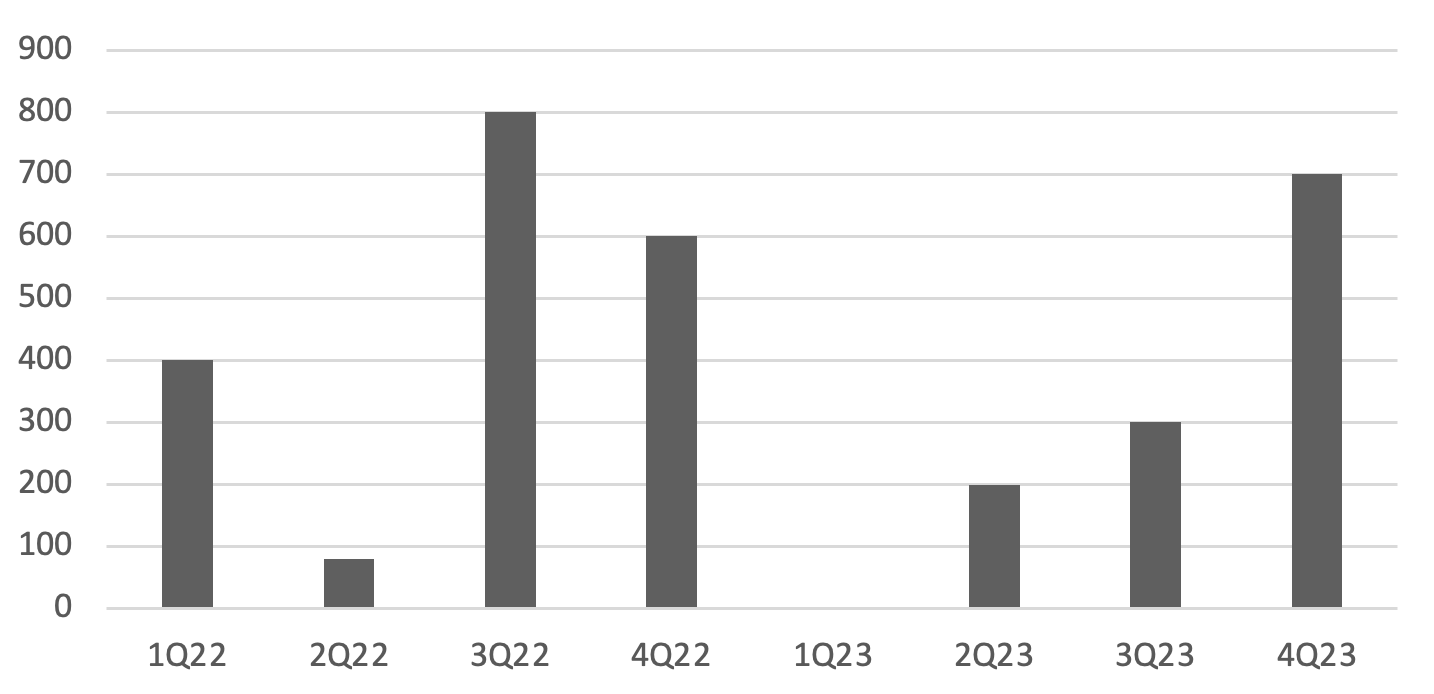

Solar power development is underway. Contracts for nearly 5GW of renewables capacity had been awarded as of Spring 2022 (Fig. 7) and another 15 GW were to be granted by the end of 2023. These projects represent the initial stages of a pledged 58.7 GW renewables installation announced by Saudi energy minister Prince Abdulaziz bin Salman; part of a goal for renewables to generate half the national power supply by 2030, with natural gas covering the other half.[36] (A World Bank study projects an installation of 40 GW of solar PV, 16 GW of wind power, and 2.7 GW of concentrating solar power.[37])

Figure 7: Saudi renewables capacity awards planned for 2022 and 2023, a total of 3.1 GW

Reaching the 50% goal in just over seven years is unlikely. In 2021, just 0.2% of Saudi electricity was generated from renewable sources.[38] Investments far beyond those cited in Fig. 7 will be required.

While the kingdom’s plans to deal with its emissions-rich power sector will help achieve its net zero target, there are rational economic reasons for replacing costly and dirty oil-fired generation with cheaper solar, wind and natural gas.

Saudi Arabia, like its GCC neighbors, enjoys the world’s lowest cost solar generation, due to copious solar radiation and large amounts of vacant land close to load centers. Recent power purchase contracts between developers and government-owned utilities have breached the 2 US cents per kilowatt-hour threshold.[39] Daily peak demand corresponds relatively well with solar power production, particularly in inland areas. Coastal areas are more problematic for solar due to humid evenings encouraging consumption after dark.

Wind generation appears less competitive, with the exception of consistent wind resources in western Saudi Arabia near 8 meters per second. Overall wind potential is low, with speeds averaging just over 5 m/s, well below the global average for windy regions of 11m/s.[40]

Beyond just building out renewables to replace oil-fired generation, the kingdom will also need to neutralize the emissions of its remaining gas-fired power plants. This involves replacing gas with renewables (which allows gas to be used in higher value applications in petrochemicals, fertilizer and hydrogen), or capturing the emissions of combusted gas. The energy minister also hinted at solutions for this as well. “We believe that carbon capture, utilization and storage, direct air capture, hydrogen and low-carbon fuels are the things that will develop the necessary ingredients,” Prince Abdulaziz said in 2021.[41]

The kingdom will also need to generate more electricity overall. That is because power demand, already growing at an average rate of nearly 5% per year over the last decade[42] will expand further as other sectors are electrified. Growth will be tempered by success with efficiency initiatives mentioned above.

Coping with intermittency will require backup generation and demand-side management tools such as load-shedding discounts. Backup generation candidates are natural gas with CCS, electricity storage systems like batteries, and—eventually—clean fuels like biogas or hydrogen. Nuclear power can also be paired with battery storage and used both as a replacement for thermal generation and a source of backup for renewables.[43]

Transport

The second most obvious candidate for decarbonization is the transport sector, responsible for 19% of the kingdom’s CO2 in 2020. Decarbonization of both power and transport sectors would eliminate roughly 60% of Saudi emissions.

Light-duty vehicles, which make up just over half of the kingdom’s transport energy demand (Fig. 8), represent the initial market for electrification. The kingdom and some of its neighbors had already embarked on electric vehicle strategies, including attracting manufacturers. Saudi Arabia’s venture with Lucid Motors was expected to assemble 155,000 cars a year and sell 100,000 EVs to the Saudi government, while Saudi firm Electromin announced it had been contracted to install vehicle charging points.[44] The government’s Saudi Green Initiative set a goal of 30% vehicle electrification in Riyadh by 2030.[45]

In the neighboring UAE, manufacturer M Glory began building an assembly plant for 55,000 EVs per year in Dubai[46] while China’s NWTN agreed to build a similar-sized plant in Abu Dhabi.[47]

Despite initial progress, decarbonizing the transport sector is more difficult than eliminating emissions from the electric power sector. While some transport modes work well with electrification – personal vehicles, public transport buses and trains, delivery fleet vehicles and bicycles – others do not. Efficiency measures[48] can reduce emissions from long-distance freight transport, aircraft and shipping, but total elimination may require offsets.

Research suggests some heavy transport modes may be more efficiently converted to hybrid (bio)diesel or hybrid gasoline systems, or perhaps hydrogen fuel cells or even compressed (bio)gas. Shifting between transport modes—for example moving heavy diesel truck traffic to electrified rail—is another crucial component.[49] Air carriers are already experimenting with biofuels, while hydrogen (ammonia) and methanol (mainly from biomass) are among future potential sources in shipping.[50]

It bears noting that Saudi Arabia’s net zero goal does not require it to concern itself with international aviation and shipping, which are tallied on external accounts. As Fig. 8 shows, domestic shipping and aviation represent small contributions to Saudi transport emissions.

Figure 8: Energy demand in the Saudi transport sector.

Subsidy reforms in 2016 and 2018 have reduced the average 7% yearly growth rate of Saudi fuel demand and improved fleet efficiency. Oil demand in the kingdom declined by an average of 1% per year between 2016 and 2021, BP data show.

Industry

Industrial emissions in Saudi Arabia—including the oil and gas sector itself—comprise the final 40% of the kingdom’s emissions. Decarbonizing industry is well known as a challenging proposition. However, Saudi Arabia has declared its intention to develop two of the most promising industrial decarbonization technologies, CCS and hydrogen.[51]

One of the most difficult industries to decarbonize is the petrochemical business, which, in Saudi Arabia is largely based around ethylene, a plastics precursor. Ethylene is produced using high temperature steam to crack hydrocarbons, derived from oil (naphtha) or gas (ethane).

In one sense, petrochemical production represents a climate-compliant use for hydrocarbons. The oil and gas feedstocks are converted—usually to plastic—rather than combusted, and their carbon content is retained within the final product. Of course, any carbon sequestered can be released if plastics are incinerated.

The process of cracking naptha or ethane is the main emission source since it requires burning fossil fuels, mainly natural gas, to produce process heat. Creating a single kilogram of ethylene creates about 2 kg. of carbon dioxide emissions along with other pollutants. Globally, ethylene production was the No. 4 source of industrial emissions in 2020, emitting 230 million metric tons, nearly as much as Spain.[52]

Options for decarbonizing petrochemical plants include using clean electricity or hydrogen as heat sources, or capturing and sequestering emissions using CCS. Aramco is also experimenting with direct crude-to-chemicals conversion which would eliminate some energy-intensive processes.

The geographic clustering of Saudi Arabia’s industrial sector, along with advantageous geology, simplifies decarbonization. Most Saudi industry is concentrated in three regions, as depicted on the map below (Fig. 9). Such clustering is ideal for capturing, gathering and storing emissions underground. Industrial clusters can become hubs for stripping carbon from flue gases, by reducing infrastructure requirements and costs for CCS, and for future re-fueling of plants with clean fuels like hydrogen.

Figure 9: Large stationary emissions sources by type in Saudi Arabia.

Carbon Capture and Storage

Saudi Arabia, like other fossil fuel-linked countries and firms, has been a proponent of carbon capture and storage. This is due to the technology’s attributes as both a source of fossil fuel demand and a method for abating its emissions. Both attributes serve to preserve fossil fuels in a climate compatible energy mix. Capturing and sequestering carbon is also a key component of Aramco’s blue hydrogen and blue ammonia ventures.

The kingdom also has numerous physical characteristics rendering it an ideal location for CCS.

Two capture projects already exist in the kingdom. Saudi chemical firm SABIC has captured CO2 since 2015 at an ethylene glycol plant. The 500,000 metric tonnes of carbon captured per year is not stored underground but used as a feedstock for fertilizer, methanol, and liquefied CO2 used in the food and drink industry.[53] A second facility operates at Uthmaniyah, which captures and sequesters up to 800,000 metric tons/year of CO2 from a natural gas processing facility.[54]

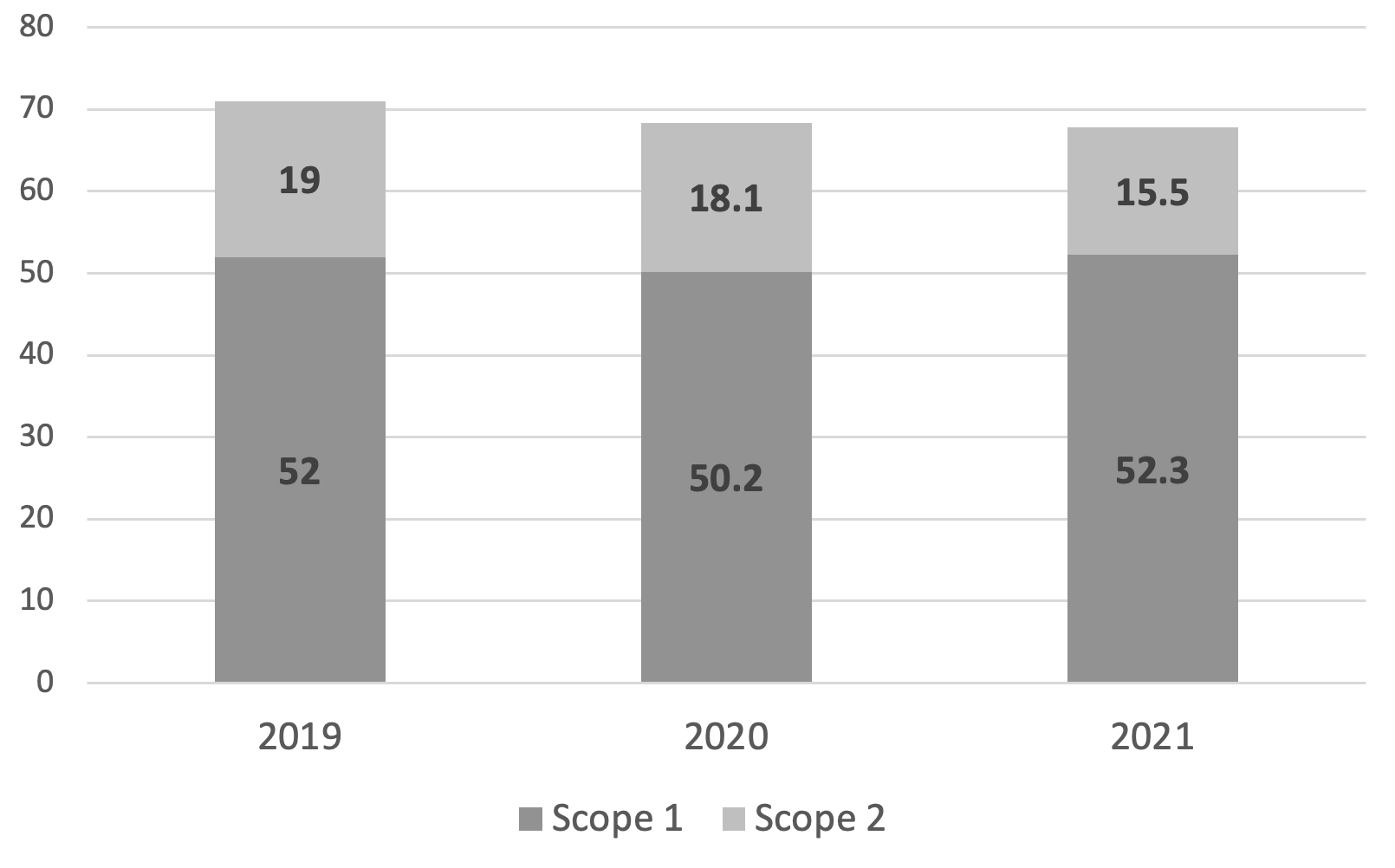

Saudi Arabia’s 2021 UN climate pledge details plans to transform the emissions-rich industrial cities of Jubail and Yanbu into centers of carbon capture. Aramco plans to capture 11 million tonnes per year by 2035 en route to achieving the promised elimination or offsetting its direct and supply chain emissions (Scope 1 and 2).

Aramco’s 2021 sustainability report estimated Scope 1 emissions at 52.3mn tonnes of CO₂ equivalent, and Scope 2 emissions at 15.5mn tonnes, for a combined 68mn tons. (Fig. 10)[55] Without CCS, Aramco’s emissions would rise, given plans to increase oil production capacity to 13mn b/d, alongside expansions in refining and gas production.

Figure 10: Saudi Aramco's 2020 Scope 1 and 2 emissions accounting from its 2021 sustainability report.

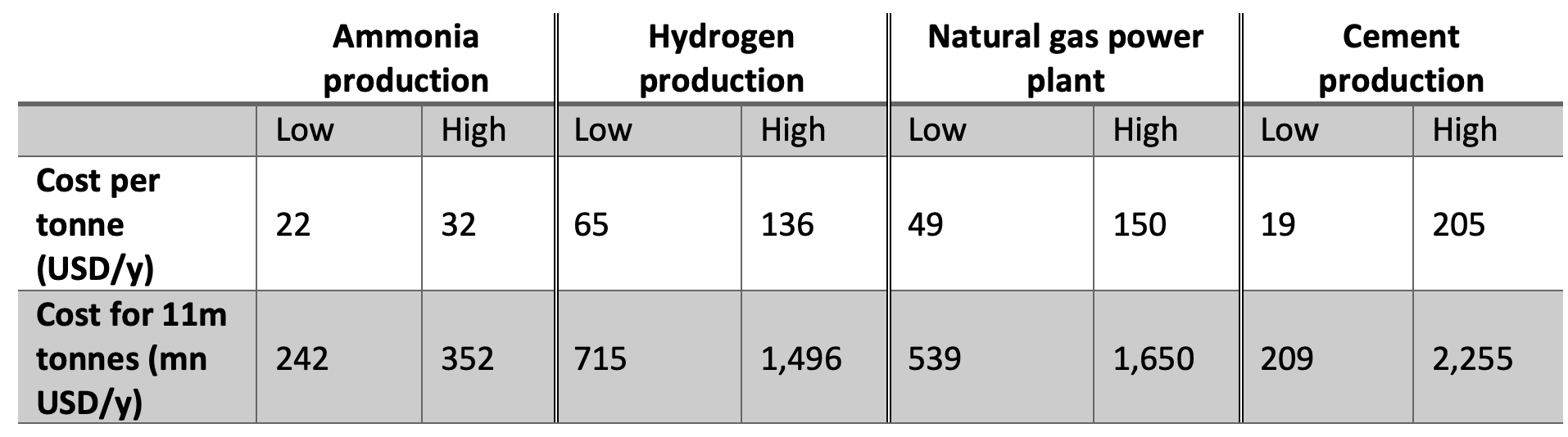

Were the kingdom to pursue capture of 11m tonnes of CO2 per year at recent US cost estimates, initial capture costs would range from $200 million to $2.2 billion per year, depending on purity of the waste stream. (Table 1) High purity CO2 streams that do not require separation from other waste gases are cheapest to capture. Transport and sequestration would add additional costs. One study estimated these costs at $17-$23/tonne in the US context.[56]

Table 1: CCS costs in the US context for industrial carbon streams of various CO2 concentrations. Estimates do not include cost of transport or sequestration, or cost reductions from learning by doing, efficiency improvements, or technological advances.

Saudi geology and industrial expertise is ideally suited for capturing and storing waste products from oil and gas. The kingdom already holds necessary expertise in pipeline and project engineering, and is well supplied with geological pore space for storing captured carbon. Depleting oilfields are found throughout the Eastern Province, with others just southeast of Riyadh. The eastern half of the Arabian Peninsula contains multiple stacked aquifers with suitable structures for long-term CO2 storage, while aquifers along the peninsula’s western edge are also likely to provide excellent seals to sequester CO2.

Other underground formations in Saudi Arabia, the UAE and Oman are ideal for CCS using mineral alteration technologies that convert gaseous CO2 into solids for permanent sequestration.[57]

Decarbonized Fuels (Hydrogen and Ammonia)

Hydrogen is another favored route for oil companies seeking climate-compliant approaches to preserving the more profitable “fuel supply chain” model of energy provision. Exports of hydrogen or derivatives like ammonia and methanol are more compatible with the hydrocarbon commodity trade than renewables, which require no fuel.

Saudi Arabia is among the cheapest places in the world to develop hydrogen due to large natural gas reserves, copious solar radiation, ample geological storage, and unused surface land near population centers.[58]

Two types are of interest: “blue” hydrogen, which splits natural gas into hydrogen and a sequesterable carbon stream; and “green” hydrogen, which uses renewable power to electrolyze water into hydrogen and oxygen. Hydrogen can be burned directly as a fuel in industrial boilers and power plants (and even vehicles) or used in fuel cells to power electric vehicles. Hydrogen gas can also be rendered more transportable if converted to liquid ammonia with the addition of nitrogen, and “cracked” back into hydrogen at the destination.

A third type, turquoise, may also be relevant. Turquoise hydrogen is produced through pyrolysis using oil or natural gas as a feedstock. Rather than creating CO2 emissions, the process creates solid carbon that could be converted into fibers for use in industrial and other applications to replace steel or aluminum.[59]

Zero-carbon hydrogen could be the industrial fuel for a decarbonized Saudi Arabia, as well as an export commodity for industrial or transportation use. Aramco has already announced its intent to produce potentially enormous volumes of blue hydrogen and blue ammonia (up to 11 million tonnes/year by 2030) from domestic natural gas.

Meanwhile, a plan for green hydrogen in northwest Saudi Arabia suggests that costs, particularly on electrolysis, could be a short-run hurdle. The Helios Green Fuels project would invest $5 billion to produce just 237,000 tonnes of hydrogen per year, which works out to $2-$3 per kilogram over 10 years.[60] Perhaps as a result, Aramco’s sustainability report notes a preference for blue hydrogen. “Despite the interest and possibility of producing hydrogen from multiple energy sources, in the short- and medium-term, hydrocarbons will remain the primary feedstock for the production of hydrogen,” it states.[61]

Saudi Governance and Advantages and Credibility

Saudi Arabia is starting the energy transition from a strong position. As outlined above, the kingdom has advantages in the low cost and carbon intensity of oil production, both of which augur for the sector’s long-run survival in a declining market. The kingdom has advantages in decarbonization: a relevant knowledge base, ideal geology, and renewables-rich geography. It draws motivation for change from its front-line exposure to climate damage.

Wealth is another advantage. Cyclical windfalls provide investment capital. Investments in future-oriented sectors represent an ideal way to share oil rents with coming generations.

What about the advantages inferred by kingdom’s monarchical rule? Since governance is autocratic, there is no legislature or veto-wielders who can block the ruler’s directives. Autocratic rule also reduces the government’s need to tailor policy to short-term election cycles, which allows policymaking on a long-term horizon ideal for responding to climate change.

Further, the Saudi system enjoys great continuity. Ruling sheikhs hold onto power until they die or are incapacitated, upon which power transitions to a son or brother. Streamlined successions help to ensure present day initiatives will be shepherded by tomorrow’s ruler, providing certainty for investors. Saudi Arabia’s de-facto ruler, Crown Prince Mohammed bin Salman, sees himself governing for the next half-century. The crown prince is preparing the groundwork for long-term rule, which includes setting the kingdom on a new energy path.

However, autocratic rule has disadvantages. It tends to be more capricious than democratic rule. It is true that policymaking tends to move more slowly in democratic systems than autocratic ones, since democratic policymakers contend with multiple veto points and representative institutions. The political economy literature on “credible commitment” in governance suggests that once decisions are made under a democratic system, such policy—enshrined in laws or legal rights—tends to be more durable and credible than the decrees or pronouncements made by an unelected sovereign. The lack of institutional oversight means autocrats can discard past priorities or even make strategic U-turns.[62]

Therefore, the shackles binding Gulf rulers to their own national policy commitments are weak. It is difficult to oblige rulers to adhere to decisions if rewards from deviation outweigh those from compliance.[63] As a result, credibility is an important consideration when evaluating present day pronouncements about a 39-year process of emissions elimination.

Effects on Saudi Geopolitical Stature and Economy

Saudi Arabia’s economy and governance exhibit a further weakness that shapes its climate policy. They depend on the survival of two key transport technologies: the internal combustion engine and the jet turbine. Those two technologies uphold oil’s near-total monopoly on the transportation fuel market.

The more the fuel monopoly comes under challenge by alternate fuels and technologies—whether EV batteries, fuel cells or biofuels—the less secure the Saudi governance model becomes.

High oil prices at the time of writing in Fall 2022 were encouraging a gradual consumer shift away from oil, while major vehicle manufacturers were announcing the phase-out of gasoline and diesel engines. Governments, including those of China and the United States already incentivize EV adoption, with China also supporting phase-in of electric trucks.[64] Continuation or strengthening of these trends will hasten the shift away from oil.

Uncertainty around the future of oil is reflected in scenarios produced by the International Energy Agency. The IEA in 2021 projected world oil demand in 2040 ranging anywhere from 44 million barrels per day to 104 million b/d.

Transition-driven losses are forecast as to weigh heaviest on hydrocarbon exporters and carbon-intensive economies (Fig. 11), As mentioned, however, the low-cost asset base in Saudi Arabia suggests an increasing share of a dwindling oil market.[65] Even so, government finances would be strained if declining oil prices outweighed countervailing gains in market share.

The loss of oil’s monopoly hold on transport portends an eventual decline in the geopolitical stature of oil producers, including Saudi Arabia, and the drifting apart of the United States and its partner regimes in the Gulf. Even if oil demand continues to grow in the developing world, those countries are unlikely to match the level of strategic backing on offer from Washington. For producer countries, new tactics and strategies will be needed to recapture strategic interest of global powers, and to cope with the transition away from fossil fuels.[66]

Saudi Arabia’s Myriad Opportunities from Net Zero

Given these trends, how should Saudi Arabia approach climate action? The Saudi strategy at climate talks has long been based on obstructing progress and removing draft treaty language deemed threatening to fossil fuel demand.[67] As recently as the 2021 COP 26 in Glasgow, delegates from Saudi Arabia, Australia and Japan urged a UN committee to temper language urging a swift transition to cleaner energy.[68] A few months earlier, the Saudi oil minister told a group of bankers that the kingdom would produce “every molecule” of its oil and gas reserves.[69]

The Saudi government’s declaratory embrace of domestic decarbonization does not necessarily signal a change in climate strategy. Policymakers in the kingdom appear comfortable advocating diverging climate policies for Saudi Arabia and for the rest of the world.

As discussed, decarbonizing the kingdom serves policy goals besides conforming with the global climate action agenda. By contrast, global decarbonization—particularly a transition to renewables-led mass electrification—is viewed as economically harmful for the Saudi economy and its rent-distributive governance. Saudi policymakers espousing net zero for the kingdom have a national interest rationale for opposing hydrocarbon substitution elsewhere.

The Saudi net zero initiative sidesteps discussion of Saudi oil exports. That is ostensibly because exported oil would be consumed outside Saudi borders and appear on another country’s carbon account. The regime may also require oil rents to fund government priorities in economic diversification and decarbonization.

Within the kingdom, the crown prince’s declaration of intent to decarbonize signals that the public will be asked to relinquish long-held subsidies once considered fundamental rights. Such concessions from the public are considered difficult in the rentier autocratic setting, but opposition is more easily managed when heads of state can point to “outside pressure” to deflect blame.[70] Implementing net zero allows Saudi policymakers to reduce domestic consumption of fossil fuels, particularly oil, which will be retained for higher value use. The net zero goal also justifies continued improvements in efficiency of buildings, appliances and vehicles.

Progress in these ventures allows Saudi Arabia to buttress its external influence. “Green economy” soft power could manifest itself in shaping the direction of the global energy transition. For instance, Saudi Arabia might steer climate action toward a more accepting role for CCS and for modifying oil and gas infrastructure for fuels like hydrogen and green/blue ammonia.

In that way, countries that import Saudi energy commodities might remain tethered to fuel-based energy systems with supply chains leading back to the Middle East, rather than shifting to renewables systems which need no fuel and connect to supply chains only during manufacturing.[71]

Developing large-scale CCS might also lead to creation of a “carbon management” services sector. Saudi firms could market subsurface pore space alongside negative emissions techniques like direct air capture or mineral alteration. Carbon disposal services could be sold to foreign firms and governments seeking to offset emissions.

Still, the CCS-hydrogen route to decarbonization remains uneconomic. The late entry of oil-producing countries and firms into the energy transition means that their preferences have been eclipsed by inexpensive renewables-led decarbonization. Even so, the CCS-hydrogen path is more viable for industrial decarbonization and appeals to oil and gas producers, including those in the United States, who want to retain profitable fuel supply businesses.[72]

For Riyadh to gain credibility, it must demonstrate that it is more than a climate spoiler. Progress on the kingdom’s net zero commitment serves as a demonstration of good faith. It also serves as a source of future trade advantage. At the moment, emissions-intensive economies are disproportionately exposed to emerging carbon border tariffs like those being formulated by the European Union. One recent estimate shows Saudi Arabia facing a major loss of income and exports from proposed EU tariffs.[73]

The lower the carbon footprint of the Saudi economy and its exports—whether manufactured goods or crude oil—the more competitive they will be when assessed in importing countries. A declining carbon footprint also enhances attractiveness for foreign investors seeking low-emission supply chains—minimizing their co-called Scope 2 and 3 emissions.

Finally, decarbonizing Saudi Arabia helps reduce risks in a region acutely exposed to climate damage. A 2-degree warming scenario could bring average surface temperature increases of 4 or 5 degrees in the Arabian Peninsula, essentially making parts of the region uninhabitable in summer.[74] For the viability of human settlement in the Gulf, mitigating climate change is imperative.

Conclusion

Saudi Arabia has a clearer path toward net zero than many countries. It has an enormous resource base in terms of renewable energy and feedstocks for clean fuels, as well as geological pore space for carbon storage. It has concentrated emissions sources that are geographically clustered. It has an impressive reservoir of human engineering talent and demonstrated expertise in leveraging geology and deploying energy conversion and transportation infrastructure. High oil prices have replenished its currency reserves and provided investment capital. Riyadh has determined autocratic leadership without veto wielders in its governance system. Combined, these factors provide a strong competitive advantage in decarbonization.

There are also external factors. The kingdom faces a long but near-certain path to geopolitical obscurity and economic decline by continued reliance on petroleum and refined products exports. Retaining its stature on the international stage requires a major role in energy systems of the future, and demonstrating alternate pathways to decarbonize. It will be exceedingly difficult for Saudi Arabia to reach net zero by 2060. But the kingdom has the motivation, the money and the tools to achieve it.

Acknowledgements

The author would like to thank David Reiner at the University of Cambridge Energy Policy Research Group, the World Bank’s Jon Strand, and the Baker Institute’s Michael Maher for their useful comments on this paper. An earlier version of this paper was presented at the 2022 Gulf Research Meeting at the University of Cambridge. For their helpful comments, the author would like to thank Andreas Rechkemmer and Logan Cochrane of Hamad bin Khalifa University and Renato Lima de Oliveira of the Asia School of Business.

References

[1] Justin Rowlatt and Tom Gerken, “COP26: Document leak reveals nations lobbying to change key climate report.” BBC News, Oct. 21, 2021; https://www.bbc.com/news/science-environment-58982445

[2] Summer Said and Benoit Faucon, “Ahead of COP26, Saudi Arabia Resists Calls to Cut Oil Investment.” Wall Street Journal, Oct. 22, 2021; https://www.wsj.com/articles/ahead-of-cop26-saudi-arabia-resists-calls-to-cut-oil-investment-11634911150

[3] Saudi Aramco, “Aramco Expands Climate Goals, Stating Ambition to Reach Operational Net-Zero Emissions by 2050,” Press release (Dhahran: Saudi Aramco, October 23, 2021), https://www.aramco.com/en/news-media/news/2021/ambition-to-reach-operational-net-zero-emissions-by-2050.

[4] Saudi Aramco, “Saudi Aramco Sustainability Report 2021: Energy Security for a Sustainable World,” Company report (Dhahran: Saudi Aramco, 2022)., p. 5 (emphasis added)

[5] “Nuclear Power in Saudi Arabia.” World Nuclear Association, April 2022; https://world-nuclear.org/information-library/country-profiles/countries-o-s/saudi-arabia.aspx

[6] Claudia Carpenter, “Saudi Arabia set to double renewables tenders as Middle East growth may pick up.” S&P Global Commodity Insights, July 25, 2022; https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/natural-gas/072522-saudi-arabia-set-to-double-renewables-tenders-as-middle-east-growth-may-pick-up

[7] Fareed Rahman, “Dubai’s Hassyan power plant to be fueled by natural gas to reduce emissions.” The National, Feb. 3, 2022; https://www.thenationalnews.com/business/energy/2022/02/03/dubais-hassyan-power-plant-to-be-fuelled-by-natural-gas-to-reduce-emissions/

[8] Laura Pitel and Nimet Kıraç, “Turkey’s new power plant exposes ‘huge contradictions’ of net zero pledge.” Financial Times, July 26, 2022; https://www.ft.com/content/1aa8c98b-ff80-461b-bad6-b3232377f904

[9] Government of Saudi Arabia, “Kingdom of Saudi Arabia - Updated First Nationally Determined Contribution,” UN climate pledge (Glasgow: United Nations Framework Convention on Climate Change, 2021), https://unfccc.int/NDCREG.

[10] “Saudi Arabia 2060 net zero target keeps crude in the picture.” Financial Times, Oct. 23, 2021; https://www.ft.com/content/399f3cb5-2256-4f3c-9443-48ee18263d41. “Saudi Arabia Sets Out Its Stall for Net-Zero 2060.” MEES, Oct. 29, 2021; http://archives.mees.com/issues/1927/articles/60204

[11] IEA data show global fossil fuel emissions in 2018 were distributed as follows: Coal 44.1%; oil 34.4%; natural gas 21.5%.

[12] Vivienne Walt, “Saudi Energy Minister Says the Country Will Pump More Oil, Despite Net-Zero Goals.” Time, Feb. 6, 2022; https://time.com/6145137/saudi-arabia-energy-minister-prince-abdulaziz-bin-salman-interview. Robert Kennedy, “‘Dangerous and delusional’: Critics denounce Saudi climate plan.” Al Jazeera, Oct. 26, 2021; https://www.aljazeera.com/news/2021/10/26/green-or-greenwashing-saudi-arabias-climate-change-pledges

[13] Government of Saudi Arabia, “Kingdom of Saudi Arabia - Updated First Nationally Determined Contribution,” 3.

[14] Saudi Aramco, “Saudi Aramco Sustainability Report 2021: Energy Security for a Sustainable World.”, p. 5 (emphasis added)

[15] “Aramco announces record second quarter and half-year 2022 results.” Saudi Aramco press release, Aug. 14, 2022. Abeer Abu Omar, “Saudi Arabia’s Making $1 Billion From Oil Exports Every Day.” Bloomberg, May 26, 2022; https://www.bloomberg.com/news/articles/2022-05-26/saudi-arabia-s-oil-exports-hit-the-highest-level-since-2016

[16] Lewis M Fulton, Amy Jaffe, and Zane McDonald, “Internal Combustion Engine Bans and Global Oil Use,” Academic paper (Davis, California: University of California-Davis, 2019), https://escholarship.org/uc/item/52j400b1.

[17] Climate Accountability Institute, Carbon Majors Dataset, “Top 20 Emitters 2018.” https://climateaccountability.org/pdf/CarbonMajorsPDF2020/Figures%20&%20Tables/Figures%20&%20Tables/TopTwenty%20CO2e%202018%20Table.png

[18] Climate Accountability Institute, Carbon Majors Dataset, “Saudi Aramco.” https://climateaccountability.org/pdf/CarbonMajorsPDF2020/Each&Every/1.%20Saudi%20Aramco%201938-2018%204p.pdf

[19] Aramco’s sustainability report addresses Scope 3 emissions briefly, saying that “To date, we have not reported Scope 3 emissions from our supply chain or from customers’ use of our products.” Saudi Aramco, “Saudi Aramco Sustainability Report 2021: Energy Security for a Sustainable World.” 39.

[20] Saudi Aramco. p. 8

[21] Wood Mackenzie, “National Oil Companies: Strategies for the Energy Transition,” Consultancy research report (London: Wood Mackenzie, March 2022).

[22] Saudi Aramco, “Saudi Aramco Sustainability Report 2021: Energy Security for a Sustainable World.” p. 44

[23] Wood Mackenzie, “National Oil Companies: Strategies for the Energy Transition.”

[24] As of June 2022, oil companies with net zero plans including Scope 3 (combustion) emissions include Shell PLC, TotalEnergies SE, Equinor ASA, Occidental Petroleum Corp., Eni SpA, Suncor Energy Inc., Williams Cos. Inc., and Neste Oyj. For a full list of oil firms and their climate pledges, see Bill Holland, “Path to Net-Zero: European, US Oil and Gas Companies Split on Scope 3 Emissions,” S&P Global Market Intelligence, June 8, 2022, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/path-to-net-zero-european-us-oil-and-gas-companies-split-on-scope-3-emissions-70485873.

[25] EDGAR - Emissions Database for Global Atmospheric Research, “CO2 Emissions of All World Countries,” Government-sponsored research (Brussels: European Commission, 2022), https://edgar.jrc.ec.europa.eu/report_2022. doi:10.2760/173513, JRC126363

[26] Peter Martin and Yanting Zhou, “No Pain, No Gain: The Economic Consequences of Accelerating the Energy Transition,” Consultancy research report (London: Wood Mackenzie, January 2022).

[27] BP, “BP Statistical Review of World Energy 2022,” (London: BP, June 2022), https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html.

[28] Power sector consumption estimates from MEES, “Saudi May 2022 Key Oil Data.” Vol. 65 N0. 29, July 22, 2022.

[29] BP, “BP Statistical Review of World Energy 2021,” statistical report (London: BP, July 2021), https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/xlsx/energy-economics/statistical-review/bp-stats-review-2021-all-data.xlsx.

[30] Data from GlobalPetrolPrices.com; Gasoline prices, Aug. 22, 2022: https://www.globalpetrolprices.com/gasoline_prices; Diesel prices, Aug. 22, 2022: https://www.globalpetrolprices.com/diesel_prices; Electricity prices, December 2021: https://www.globalpetrolprices.com/electricity_prices.

[31] Jim Krane, Energy Kingdoms: Oil and Political Survival in the Persian Gulf, Center on Global Energy Policy Series (New York: Columbia University Press, 2019).

[32] Vivian Nereim, “Saudi Arabia Eases Subsidy Cuts with Gasoline Price Ceiling.” Bloomberg, July 10, 2021; https://www.bloomberg.com/news/articles/2021-07-10/saudi-arabia-softens-subsidy-cuts-with-gasoline-price-ceiling

[33] World Bank, “Gulf Economic Update: Achieving Climate Change Pledges,” NGO report (Washington: World Bank, Spring 2022), 25.

[34] World Bank, “Gulf Economic Update: Achieving Climate Change Pledges.”

[35] Aziz El Yaakoubi, “Saudi Arabia calls for flexibility in energy transition.” Reuters, Jan. 12, 2022; https://www.reuters.com/article/energy-saudi-idAFL1N2TS0IE

[36] See: “Saudi Arabia Awards 1GW Of Solar Projects,” MEES Vol. 65, No. 10; March 11, 2022; http://archives.mees.com/issues/1945/articles/60661; also: Hebshi Alshammari, “Saudi Arabia aims to generate 50% of power from renewables by 2030.” Arab News, Jan. 20, 2021; https://arab.news/8yk8z

[37] World Bank, “Gulf Economic Update: Achieving Climate Change Pledges.”

[38] BP, “BP Statistical Review of World Energy 2021.”

[39] Informa Energy & Utilities, “Saudi Arabia achieves two new world record solar tariffs.” April 9, 2021; https://energy-utilities.com/saudi-arabia-achieves-two-new-world-record-solar-news111675.html

[40] Saudi Arabia, Global Wind Atlas. (Undated. Accessed June 14, 2022) https://globalwindatlas.info/area/Saudi%20Arabia

[41] Akshat Rathi, “How Saudi Arabia Is Planning to Reach Net Zero by 2060.” Bloomberg, Oct. 23, 2021; https://www.bloomberg.com/news/articles/2021-10-23/how-saudi-arabia-is-planning-to-reach-net-zero-by-2060?sref=Q77DYrNe

[42] BP, “BP Statistical Review of World Energy 2021.” 30% vehicles in Riyadh will be powered by electricity by 2030, says Al-Rasheed.” Arab News, Oct. 24, 2021; https://www.arabnews.com/node/1953596/business-economy

[43] Peter R Hartley, “The Cost of Displacing Fossil Fuels: Some Evidence from Texas,” The Energy Journal 39, no. 2 (2018).

[44] Alkesh Sharma, “PIF-backed EV maker Lucid to produce 150,000 cars a year at its Saudi factory.” The National, May 18, 2022; https://www.thenationalnews.com/business/economy/2022/05/18/pif-backed-ev-maker-lucid-to-produce-150000-cars-a-year-at-its-saudi-factory

[45] Vivian Nereim, “Saudi Arabia to Start Electric-Vehicle Push in Capital Riyadh.” Bloomberg, Oct. 23, 2021; https://www.bloomberg.com/news/articles/2021-10-23/saudi-arabia-to-start-electric-vehicle-push-in-capital-riyadh

[46] Alvin Cabral, “UAE company opens new electric vehicle manufacturing plant in Dubai Industrial City.” The National, March 28, 2022; https://www.thenationalnews.com/business/2022/03/28/uae-company-opens-new-electric-vehicle-manufacturing-plant-in-dubai-industrial-city

[47] “Abu Dhabi's Kizad signs lease with NWTN for electric vehicle assembly plant.” The National, Sept. 6, 2022; https://www.thenationalnews.com/business/road-to-net-zero/2022/09/06/abu-dhabis-kizad-signs-lease-with-nwtn-for-electric-vehicle-assembly-plant

[48] The 2021 Saudi NDC suggests phasing out inefficient used light-duty vehicles and implementing aerodynamic regulation for heavy-duty vehicles.

[49] Magdala Arioli, Lew Fulton, and Oliver Lah, “Transportation Strategies for a 1.5 °C World: A Comparison of Four Countries,” Transportation Research Part D: Transport and Environment 87 (October 1, 2020): 102526, https://doi.org/10.1016/j.trd.2020.102526.

[50] Most methanol is made from natural gas via steam reformation. Low carbon methanol can also be made from biomass such as crop and forestry residue. Maersk has 12 methanol-fueled container ships on order and intends to source more than 700,000 tonnes of biomass methanol by 2025. See: “A.P. Moller-Maersk engages in strategic partnerships across the globe to scale green methanol production by 2025.” Maersk press release, March 10, 2022; https://www.maersk.com/news/articles/2022/03/10/maersk-engages-in-strategic-partnerships-to-scale-green-methanol-production

[51] “Saudi Arabia Urges Colorblind Approach to Hydrogen.” MEES, May 13, 2022. “Petro Rabigh Signs Up To CCUS.” MEES, April 8, 2022.

[52] Sanjeev Kapur, “The Energy Transition and Decarbonization in the Ethylene Industry.” Apex PetroConsultants (consultancy report/blog), March 30, 2021; https://www.apexpetroconsultants.com/blog/energy-transition-decarbonization-in-ethylene-industry

[53] “Creating the world’s largest carbon capture and utilization plant.” SABIC press release,

[54] Anthony Wright, “Challenges and opportunities for CCS in Saudi Arabia.” Natural Gas World, Sept. 8, 2021; https://www.gasworld.com/challenges-and-opportunities-for-ccs-in-saudi-arabia/2021674.article

[55] Saudi Aramco, “Saudi Aramco Sustainability Report 2021: Energy Security for a Sustainable World.” p. 32 and 46. See also: “Saudi Arabia Sets Out Its Stall for Net-Zero 2060.” MEES, Oct. 29, 2021; http://archives.mees.com/issues/1927/articles/60204

[56] Jonathan M. Moch, William Xue, and John P. Holdren, “Carbon Capture, Utilization, and Storage: Technologies and Costs in the U.S. Context,” Policy brief (Boston: Belfer Center, Harvard University, January 2022), https://www.belfercenter.org/publication/carbon-capture-utilization-and-storage-technologies-and-costs-us-context.

[57] Vahrenkamp, Volker and Afif, Abdulkader and Tasianas, Alexandros and Hoteit, Hussein, The Geological Potential of the Arabian Plate for CCS and CCUS - An Overview (April 8, 2021). Proceedings of the 15th Greenhouse Gas Control Technologies Conference 15-18 March 2021, Available at SSRN: https://ssrn.com/abstract=3822139 or http://dx.doi.org/10.2139/ssrn.3822139

[58] Leigh Collins, “Green hydrogen now cheaper than blue in Middle East, but still way more expensive in Europe.” RECHARGE magazine, Feb. 24, 2022; https://www.rechargenews.com/energy-transition/green-hydrogen-now-cheaper-than-blue-in-middle-east-but-still-way-more-expensive-in-europe/2-1-1173423

[59] “From Fuels to Feedstock,” Rice University Carbon Hub. Undated web page; https://carbonhub.rice.edu/disruptive-approach

[60] One person familiar with the Helios project suggested an equivalent amount of energy could be garnered by drilling two oil wells for roughly $10 million, about 1/500th of the cost.

[61] Saudi Aramco, “Saudi Aramco Sustainability Report 2021: Energy Security for a Sustainable World.” p. 40-1

[62] The “credible commitment” literature is substantial, but an important work establishing this principle is: Douglass C North and Barry R Weingast, “Constitutions and Commitment: The Evolution of Institutions Governing Public Choice in Seventeenth-Century England,” The Journal of Economic History 49, no. 4 (1989): 803–32. A useful discussion of “credible commitment” in climate policy can be found in: Steffen Brunner, Christian Flachsland, and Robert Marschinski, “Credible Commitment in Carbon Policy,” Climate Policy 12, no. 2 (March 1, 2012): 255–71, https://doi.org/10.1080/14693062.2011.582327.

[63] James Forder, “The Theory of Credibility and the Reputation-Bias of Policy,” Review of Political Economy 13, no. 1 (2001): 5–25.

[64] Colin McKerracher, “China’s Electric Trucks May Well Pull Forward Peak Oil Demand.” Bloomberg, Oct. 11, 2022; https://www.bloomberg.com/news/articles/2022-10-11/china-s-electric-trucks-may-well-pull-forward-peak-oil-demand

[65] Wood Mackenzie, “National Oil Companies: Strategies for the Energy Transition.”

[66] For more on this topic, see: Jim Krane, “Last Man Standing: Saudi Aramco and Global Climate Action,” in Governance and Domestic Policymaking in Saudi Arabia: Transforming Society, Economics, Politics and Culture, ed. Mark C. Thompson and Neil Quilliam (London: IB Tauris, 2022), 257–89; Jim Krane, “Climate Action versus Inaction: Balancing the Costs for Gulf Energy Exporters,” British Journal of Middle Eastern Studies, 2020, 1–19.

[67] Jim Krane, “Climate Strategy for Producer Countries: The Case of Saudi Arabia,” in When Can Oil Economies Be Deemed Sustainable?, ed. Giacomo Luciani and Tom Moerenhout (Singapore: Springer Singapore, 2021), 301–27, https://doi.org/10.1007/978-981-15-5728-6_12.

[68] Justin Rowlatt and Tom Gerken, “COP26: Document leak reveals nations lobbying to change key climate report.” BBC News, Oct. 21, 2021; https://www.bbc.com/news/science-environment-58982445

[69] Summer Said and Benoit Faucon, “Ahead of COP26, Saudi Arabia Resists Calls to Cut Oil Investment.” Wall Street Journal, Oct. 22, 2021; https://www.wsj.com/articles/ahead-of-cop26-saudi-arabia-resists-calls-to-cut-oil-investment-11634911150

[70] For a discussion of academic theory around energy subsidies as rights, see Krane, Energy Kingdoms: Oil and Political Survival in the Persian Gulf.

[71] For an explanation of supply chain differences between oil and renewables, see: Jim Krane and Robert Idel, “More Transitions, Less Risk: How Renewable Energy Reduces Risks from Mining, Trade and Political Dependence,” Energy Research & Social Science 82 (2021): 102311. Also: Jim Krane and Robert Idel, “On the Reduced Supply Chain Risks and Mining Involved in the Transition from Coal to Wind,” Energy Research & Social Science 89 (2022): 102532.

[72] “Greater Houston Partnership Launches Regional Energy Transition Strategy.” Greater Houston Partnership press release, June 29, 2021; https://www.houston.org/news/greater-houston-partnership-launches-regional-energy-transition-strategy

[73] UNCTAD, “A European Union Carbon Border Adjustment Mechanism: Implications for Developing Countries,” NGO report (New York: United Nations Conference on Trade and Development, 2021), https://unctad.org/system/files/official-document/osginf2021d2_en.pdf.

[74] World Bank, “Gulf Economic Update: Achieving Climate Change Pledges.” Also see: Fiona MacDonald, “One of the World’s Wealthiest Oil Exporters Is Becoming Unlivable.” Bloomberg Green, Jan. 16, 2022; https://www.bloomberg.com/news/articles/2022-01-16/kuwait-a-wealthy-oil-exporter-is-becoming-unlivable?sref=Q77DYrNe

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.

{kind=link}