By Woohyeon Kim, Elena Marks, Marah Short, Hannah Crowe and Vivian Ho

Since late 2013, individuals have been able to shop for and purchase private health insurance through the Marketplace via Healthcare.gov. Through the Marketplace, Texans can learn what plans are available to them, examine the features of the plans, determine whether they qualify for tax credits to lower their premiums, and purchase the plan that is best suited to their needs.

During the first year of the Affordable Care Act’s Health Insurance Marketplace, consumers learned that many plans offered limited provider networks. This issue brief examines the availability of Marketplace plans in Texas, the number of in-network hospitals in the plans, and other plan characteristics influencing premiums. Our analysis focuses on Marketplace Silver plans, because they provide the benchmark by which premium-reducing tax credits are determined and because the majority of Texans who purchased Marketplace plans chose a Silver plan.

Methodology

The state of Texas is divided into 26 rating areas, representing 25 different Metropolitan Statistical Areas (MSA) and one rating area comprised of 177 rural counties that are not within an MSA. Private health insurance companies could choose to offer plans in none, any, or all 26 rating areas. The Marketplace plans that are available to a particular individual depends on the rating area in which he or she lives.

We obtained a list of all Marketplace insurers and plans available in each of the 26 rating areas in Texas and their cost structures from the website Healthcare.gov. To determine the number of hospitals in each plan’s network, in August of 2014, we consulted the website of each insurer. We counted the number of hospitals listed for each plan using the insurers’ list of covered facilities when it was available on the website. For plans without a comprehensive list, we utilized the zip code search function on the plan’s website to calculate the number of hospitals. We limited our search to hospitals within 50 miles of any zip code inside the given rating area to assure that facilities were within a reasonable traveling distance of potential customers.

Texas Health Insurance Plans by Rating Area

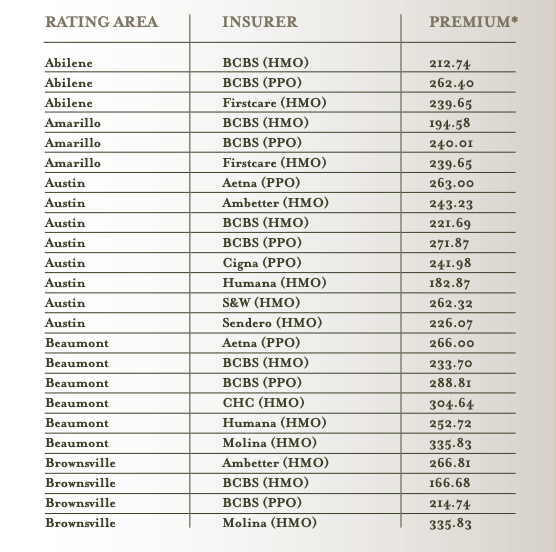

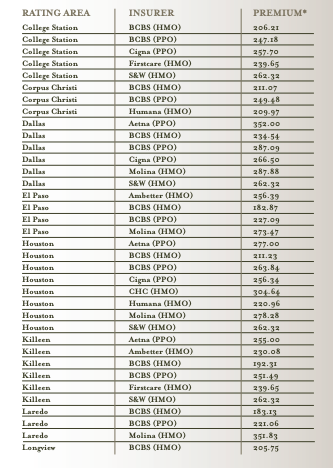

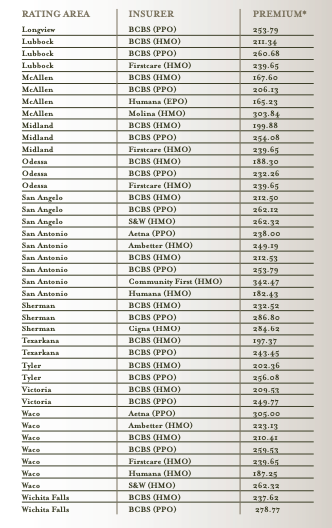

Table 1 lists the insurers offering plans in each rating area and the premium for a Silver plan for a 30 year old. Larger cities such as Austin, Dallas, Houston, and San Antonio have more insurers and more plans available through the Marketplace than do smaller Texas cities. For example, there were 5 insurers selling Silver plans in Dallas and 7 insurers offering Silver plans in Houston. In contrast, customers shopping for Silver plans in Longview and Victoria had only 2 insurance plans to choose from, both sold by Blue Cross Blue Shield.

Table 1 — Silver Plan Premiums for a Single 30 Year Old by Rating Area

Some insurers offered more than one Silver plan within a single rating area. In these cases we report the premium of the lowest priced plan. Offering two Silver plans allows an insurer to vary premiums, deductibles, copayments, and the out-of-pocket maximum in a manner to attract customers who expect either high or low needs for healthcare in the coming year. If these two plans also happen to be the lowest priced Silver plans in a rating area, they effectively limit the size of the tax credits available to customers for purchasing higher priced plans being offered by competing insurers. The federal formula that determines the size of tax credits in each rating area is based in part on the second lowest priced plan.

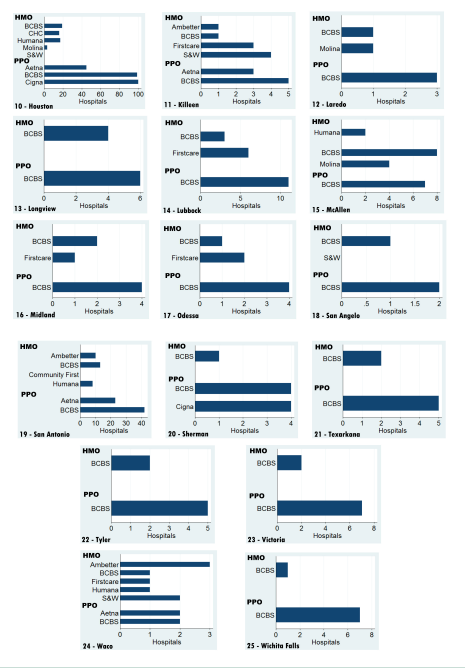

Marketplace Plans and Hospital Network Size

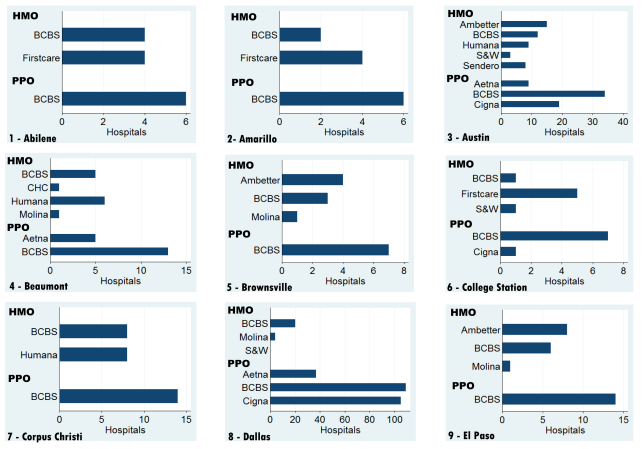

Figure 1 presents information on the hospital network size of each insurer’s Silver plans. The network size is the same for all Silver plans offered by an insurer in a rating area. Among the 304 Silver plans available in Texas, the size of the hospital networks vary greatly, with larger networks in larger cities. While Houston and Dallas both have networks with approximately 100 hospitals, the median size of networks in Texas is four hospitals.

Figure 1 — Hospital Networks of Insurance Plans by Rating Area

There are two insurers that offer plans that do not include a single hospital within their MSA. Community First Health offered plans to the San Antonio area that cover urgent-care clinic visits but do not provide coverage for visits to any hospitals. The closest hospital within the Scott & White plan offered in Dallas is approximately 70 miles away near Waco. In areas with limited hospital availability, individuals may face higher out-of-pocket costs if they must visit a nearby out-of-network hospital for an emergency. The number of hospitals included in some plans may have increased since we gathered these data.

Marketplace Premiums, Network Size, and Market Competition

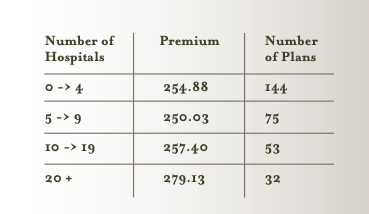

Many have opined that insurers limited the size of their networks to reduce their costs. If so, we would expect to see that cost reduction reflected in the prices that consumers pay for limited network plans. Table 2 below shows the relationship between the number of hospitals in a Silver plan’s network and the average premium (pre-tax credit) for a 30 year old. The data show that the 32 plans with more than 20 hospitals have an average premium that is 8.5% higher than the 53 plans with 10-19 hospitals. The difference in premiums among the plans with 0-4, 5-9 and 10-19 are negligible, and actually the 75 plans with 5-9 hospitals are less expensive than the 144 plans with 4 or fewer.

Table 2 —Hospital Network Size by Premium and Number of Plans

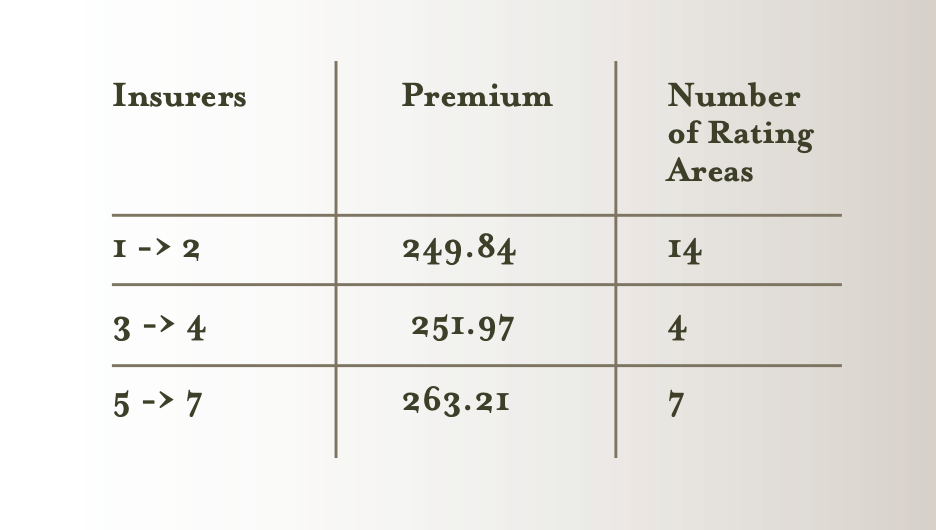

The economics of market competition suggest that rating areas with more insurers offering plans should have lower average premiums. However, Table 3 indicates that rating areas with more insurers have slightly higher premiums.

Table 3 — Number of Insurers per Rating Area and Silver Plan Premiums

This pattern is also evident in Table 1. For example, only BCBS and Firstcare offered Silver plans in Amarillo, and premiums varied between $194.58 and $240.01. In contrast, seven insurers offered plans in Houston, with premiums ranging from $211.23 to $304.64. Insurers may have been expecting sicker populations to enroll in large cities, because healthier people might already have coverage from large employers. Large markets also contain more hospitals offering the most advanced medical treatments, which can raise medical costs.

Looking Forward

Insurers were cautious about entering the Marketplace its first year due to uncertainties about the cost of covering the customers who would enroll. Currently there is at least one insurer in each rating area. But in the upcoming enrollment period beginning November 15, 2014, the number of insurers offering plans is predicted to increase. U.S. Health and Human Services Department Secretary Sylvia Burwell stated that there is an expected 25% increase in the number of insurers for 2015 plans. Texas is expected to have 16 insurers offering plans, up from 12 in 2014, and will be one of the states with the most insurers. However, it is not yet clear which rating areas the insurers will enter, which will determine nature of competition.

Hospital networks vary greatly in size, and this may not change much in 2015. Many insurers will likely continue to use limited network size and high deductibles as a means to control costs and prevent large increases in plan premiums. Yet we should still expect premiums to increase for 2015, as they do every year to reflect rising health care costs. In 2013 and 2014 private insurance premiums increased at a slower pace than previous years, but they did increase. It is important that individuals re-evaluate their plan options to ensure they make the choice which best fits their needs. Features such as the premium, deductible and network coverage may change in their currently selected plan, and new plans may be available in their rating area.