Introduction

Despite important advantages, such as its proximity to the United States, a still-advantageous access to U.S. markets through the U.S.-Mexico-Canada (USMCA) trade accord, and solid industrial base built over more than three decades — Mexico’s economy has been consistently experiencing slow growth. Since 1990, average economic growth has remained approximately 2.2% per annum, according to data from Mexico’s National Institute of Statistics and Geography (INEGI).

However, in the last seven years under former President Andrés Manuel López Obrador (2018–24) and current President Claudia Sheinbaum (2024–present), economic growth rates have decreased further. Between 2018 and 2024, Mexico’s average growth rate was approximately 0.9% per year, the lowest since the administration of Miguel de la Madrid in the 1980s. In 2025, economic growth stood at 0.8%. Thus, despite an increase in exports since June 2025, the Mexican economy seems to be locked in low gear. For 2026, current forecasts demonstrate that this year will follow the current trend, with expected growth not exceeding 1.3%.

These long-term trends and the recent decline in economic growth raise two primary questions:

- Why is the Mexican economy underperforming?

- Are the reasons underlying the slow growth rate structural?

This brief argues that Mexico’s slow growth is driven by structural factors, which require significant policy changes in order to increase the country’s economic growth rate. Moreover, the brief also addresses how recent political decisions are expected to sustain Mexico’s current low growth trend. While these observations may not be novel, examining these issues together demonstrates that Mexico is unlikely to experience greater growth if these fundamental barriers are not addressed both collectively and broadly.

Formal and Informal Economy

The economic speeds of Mexico’s formal and informal sectors differ and increasingly so. Although the country grew its industrial base and became a strong exporter of manufactured goods, this transition to an export-oriented economy has not yet been fully realized nor has it encompassed every economic sector. The country’s informal economy demonstrates the in-process nature of this transition.

Long-term data from INEGI illustrates that over half of all workers have remained in the informal economy, which is generally comprised of jobs not regulated, protected, and taxed by the government. More specifically, data from INEGI estimates that approximately 54.4% of the country’s workforce were in the informal economy in 2024. As a result, the Mexican economy continues to face challenges due to a high level of informal employment. These workers tend to be among the least productive, as they largely lack the capital, skills, and technology to integrate into the formal economy and do not have access to the formal economy’s employment protections.

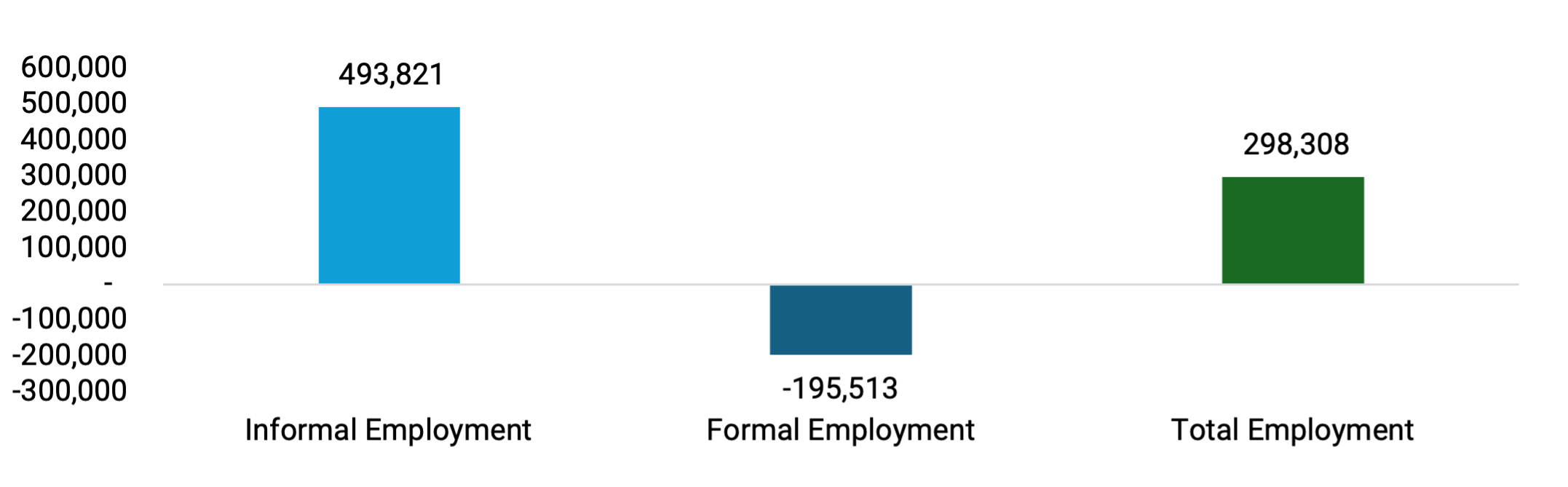

Moreover, current informal employment levels place significant limits on Mexico’s ability to raise additional revenue to expand sustainable social welfare programs and invest in infrastructure, education, science and technology, and health. Underinvestment in education, science, technology, and infrastructure will likely continue to stem formal sector growth and has also recently contributed to a sharp decline in formal employment (Figure 1). Without addressing the structural barriers underlying this cycle, it will be difficult to resolve.

Recently, rising informal employment appears to be driven in part by the tightening of revenue collection practices, which has led to many small businesses transferring their economic activity from the formal sector to the informal sector. Growing rates of informal economic activity are also a result of the higher business costs associated with constitutional reforms, which is coupled with significant minimum wage increases over the past seven years that have not aligned with productivity gains thus far.

INEGI’s data from 2026 shows that Mexico’s generation of formal employment decreased in 2025. This is compounded by the economic challenge of generating enough jobs for both current and incoming workers (Figure 1). A future strategy should focus on retaining workers in the formal economy and mitigating external forces that may increase informal employment, especially as workers in the informal economy can remain in these positions for months or even years.

Figure 1 — Mexico’s Job Creation Rates in 2025 by Employment Type

While not yet thoroughly studied, it is hypothetically possible that Mexico’s challenges with organized crime may have contributed to many businesses shifting their operations to underground operations to reduce their exposure to outright extortion. This issue has become more acute, especially for small- and medium-size enterprises (SMEs).

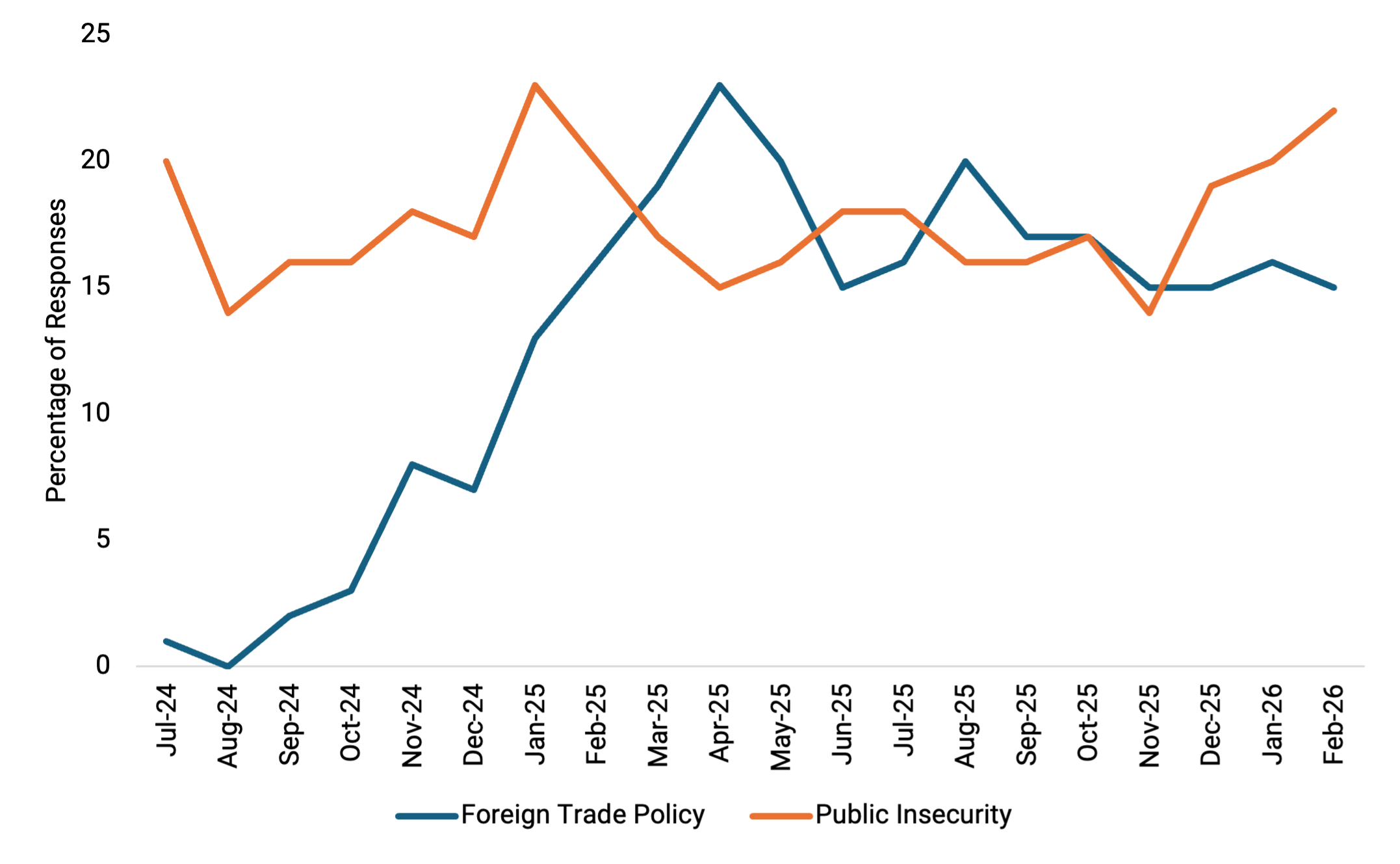

Despite the Trump administration’s intensified protectionist trade policies, private sector economists have recently ranked public insecurity as the primary factor threatening economic growth. According to the Survey of Private Sector Forecasters published by Banco de México (Banxico), public insecurity shifted to the top concern from December 2025 to February 2026, shifting foreign trade policy to second place (Figure 2).

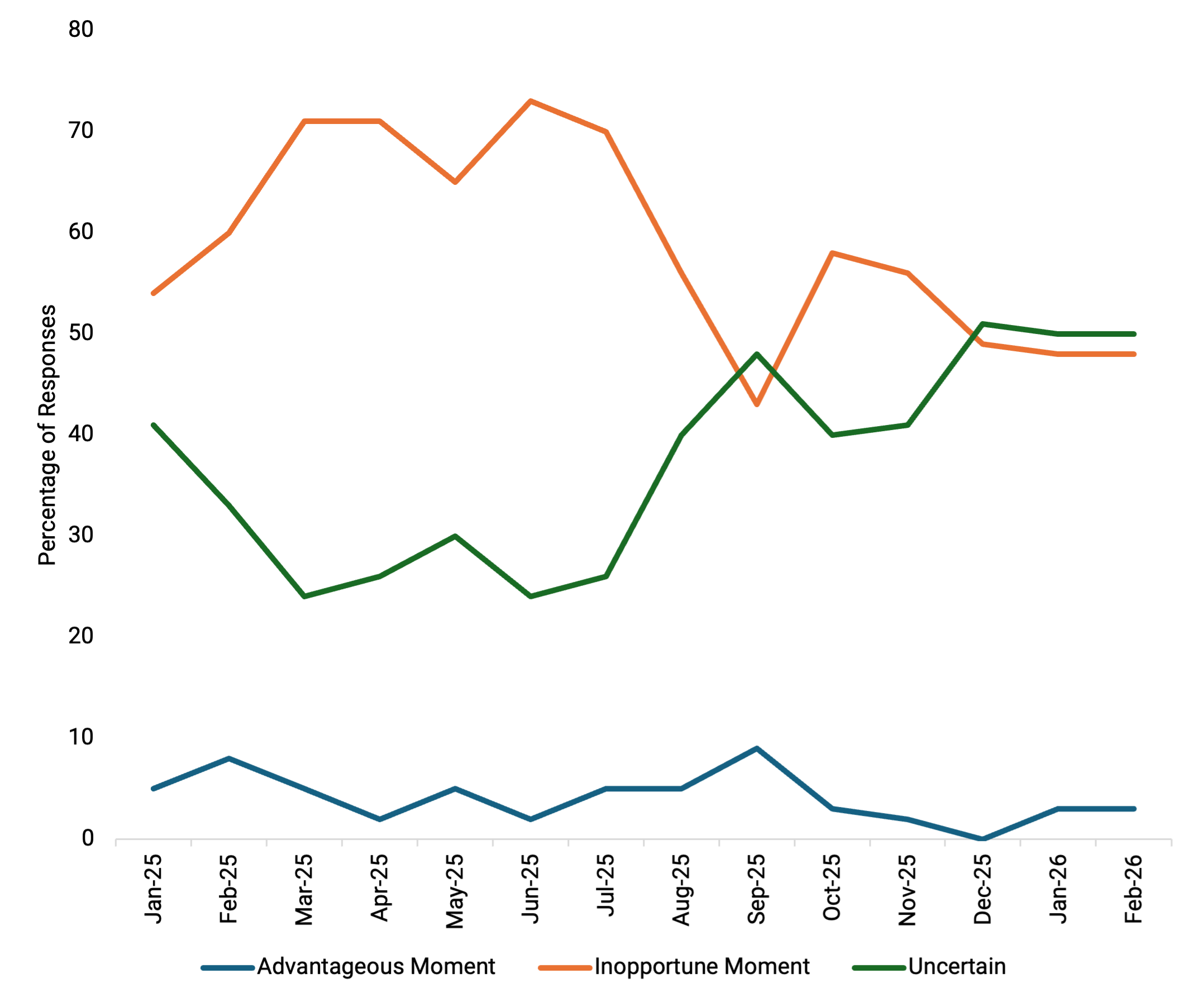

Furthermore, in December 2025, 49% of respondents considered it an inopportune moment to invest, while 51% were uncertain, with no respondents seeing it as an advantageous moment (Figure 3). This level of economic doubt has only occurred nine other times since 1999 — six of which were between 2019 and 2020, when Mexico experienced a mild recession that later deepened during the COVID-19 pandemic.

Figure 2 — Survey Responses on Main Factors Threatening Mexico’s Economic Growth, July 2024–February 2026

Figure 3 — Survey Responses on Timing for Investments in Mexico, July 2024–February 2026

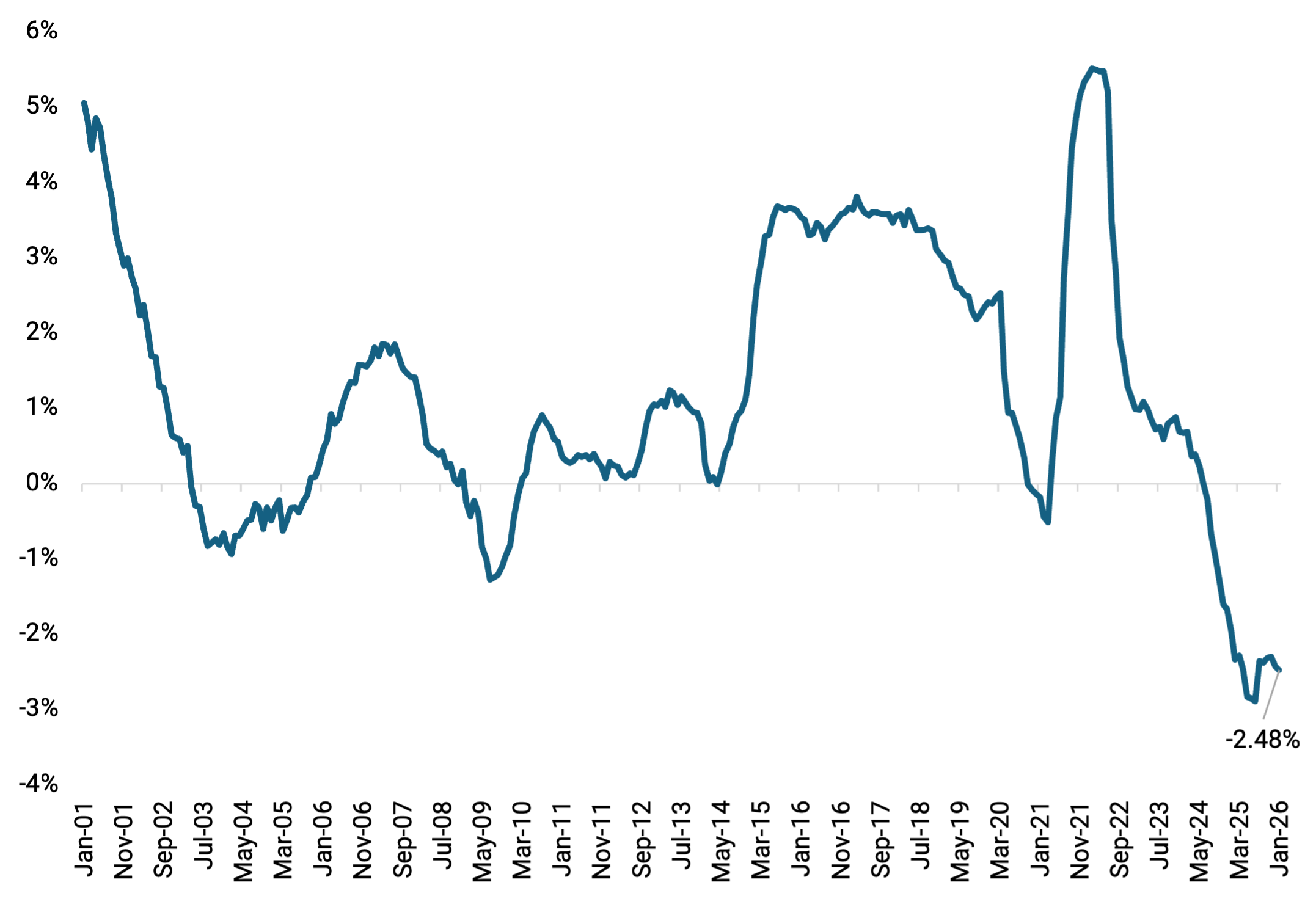

The reduction in formal employment has occurred alongside a decline in the number of employers registered with the Mexican Social Security Institute (IMSS). This marks 19 consecutive months of annual contraction as of January 2026, the longest decline since the period between April 2003 and September 2005, which extended for 30 months (Figure 4).

Figure 4 — Annual Growth of IMSS-Affiliated Employers, January 2001–January 2026

Workforce Productivity

Mexico’s rising informal economy rate is related to the country’s challenges with workforce productivity. In fact, Mexico is currently positioned toward the end of the Organization for Economic Cooperation and Development’s (OECD) 2022 list of countries’ workforce productivity, with Colombia being the only country to precede Mexico.

Mexico’s low ranking is, at least partially, contributable to reductions in investments that fuel workforce productivity: 1) education and skills, 2) technology and innovation, and 3) infrastructure. These and other factors constraining Mexico into a low growth trajectory are difficult to address. The tightening of current fiscal policy also plays a role, as the budget allows for little flexibility to shift resources to these important variables that could increase the country’s productivity and, in turn, its economic growth.

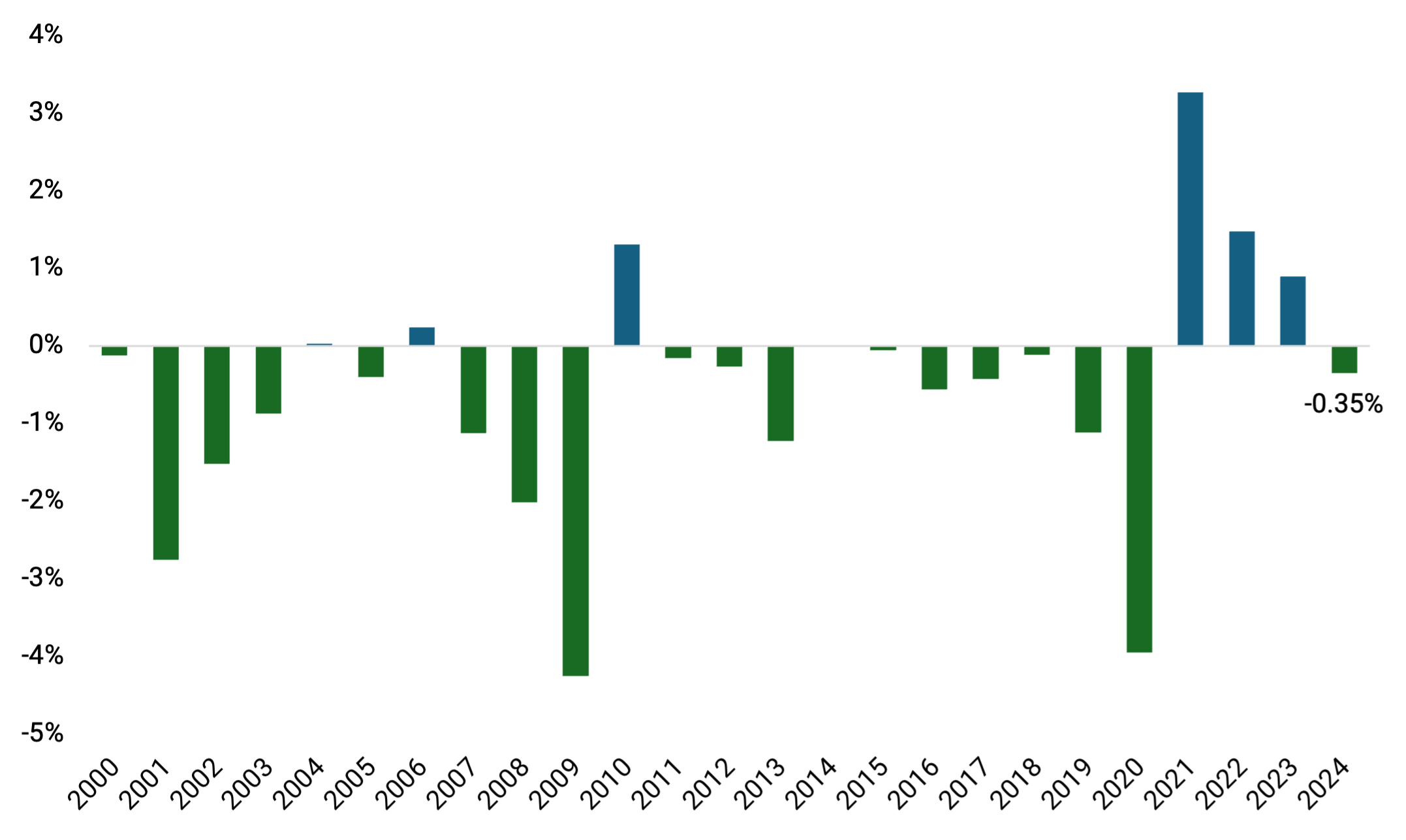

According to INEGI’s 2024 “Measure of Informality,” the formal economy generated 74.6% of the country’s total GDP, despite comprising less than half of the workforce at 45.6%. Conversely, the informal sector — which employs 54.4% of workers — contributed 25.4% to GDP. This disparity highlights a concentration of labor in low-productivity activities, which acts as a structural limit to economic growth. In 2024, total factor productivity declined 0.35%, led by secondary and tertiary economic sectors (Figure 5). While official 2025 productivity data is pending, rising informality rates suggest a continued decline. Reductions in productivity have also been shown to compromise worker well-being, limit the tax base, and jeopardize long-term economic growth.

Figure 5 — Annual Growth Rate of Total Factor Productivity (TFP), 2000–24

Note: A contraction in Total Factor Productivity (TFP) indicates a loss of structural efficiency. This implies that, to maintain a constant level of production, the economy should increase the intensity of its input use (capital, labor, and materials). In essence, factor returns decrease, raising operating costs and reducing competitiveness. Also, INEGI reports TFP in growth rates because it is not a tangible, measurable object, but rather an efficiency residual. By using percentages, noise from inflation and sector size is excluded, allowing for a direct observation of whether the economy is gaining or losing innovation capacity relative to the previous year.

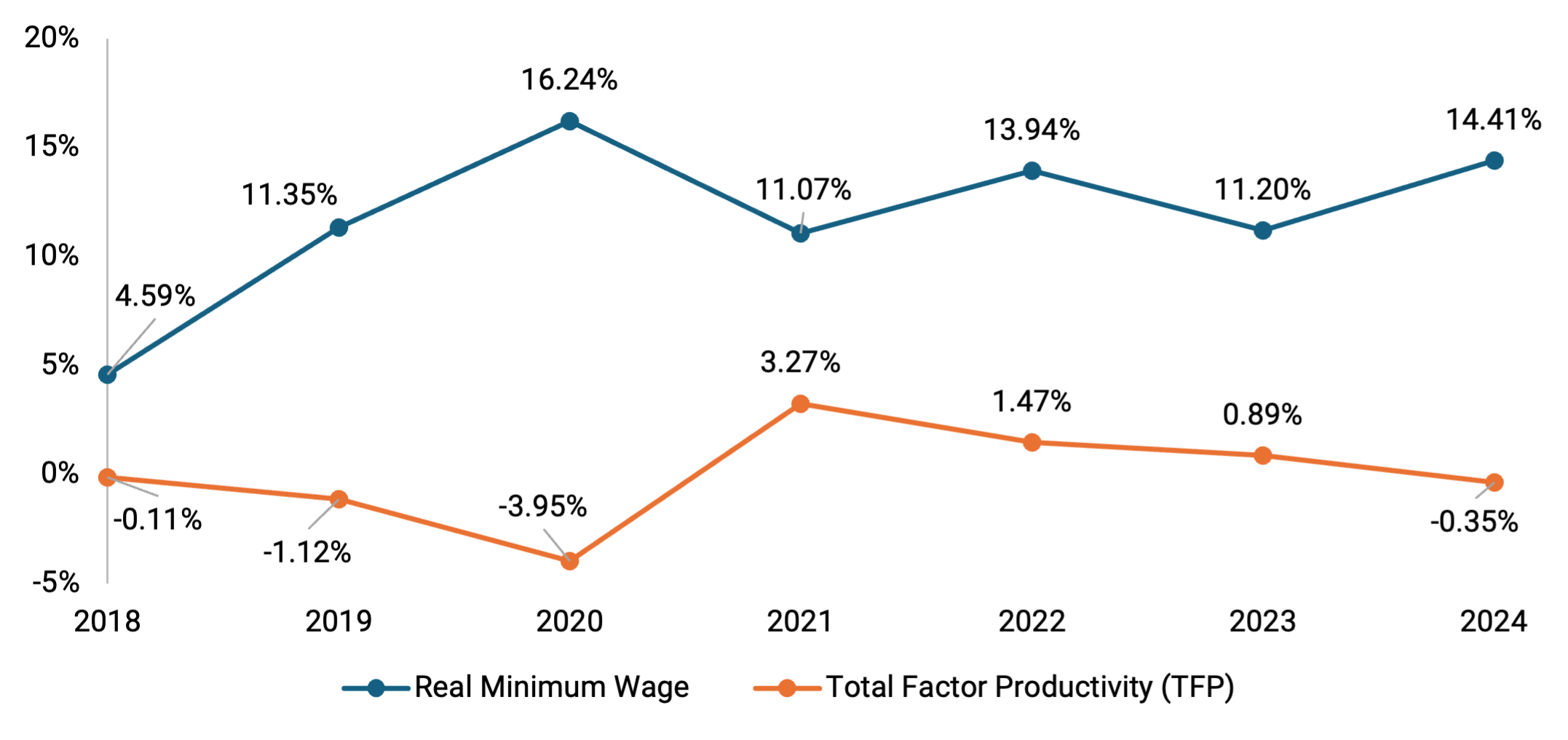

Mexico’s recent decisions to increase wages, compensations, and benefits, while addressing a longstanding issue, may also be driving Mexico’s low economic growth. The previous (2018–24) and current administrations (2024–30) have consistently pursued a raise in the minimum wage and has recently enacted a constitutional reform to reduce the work week from 48 to 40 hours as well as increasing the number of paid holidays. While these changes carry several benefits, such as bringing Mexico into further alignment many other OECD members’ labor practices, increases in wages and compensation packages should also lead to increases in worker productivity. Otherwise, the gap could negatively affect companies, especially SMEs. The growing gap between low productivity and wages, salaries, compensations, and other benefits are likely to further discourage investment, especially in SMEs.

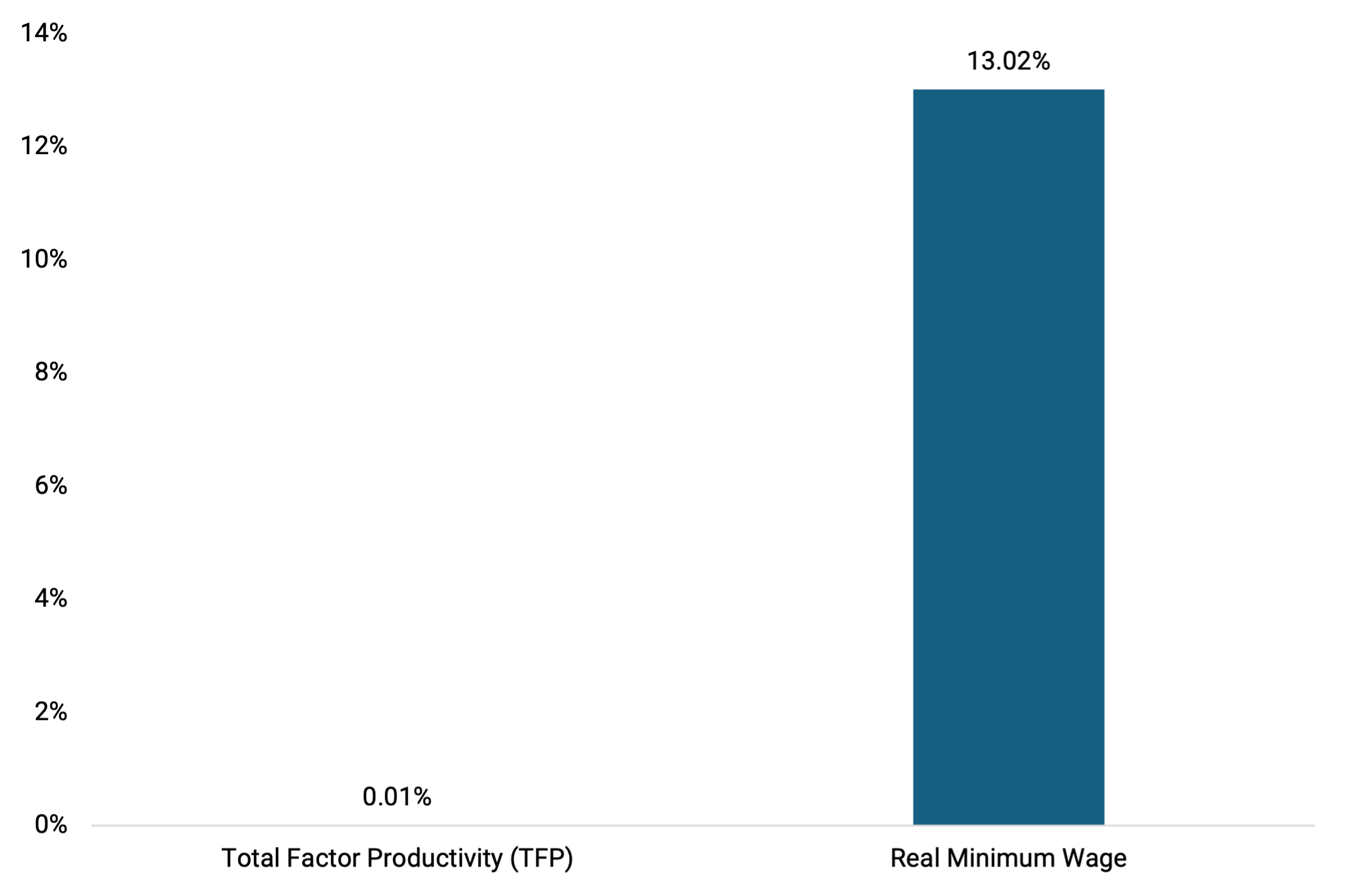

Since 2018, minimum wage has risen 256.54% in current prices and 145.32% in constant prices. On average, between 2019 and 2024, which includes the latest date available, productivity has risen on average 0.01% per year, and labor productivity has diminished on average 0.04% (Figure 6). Over the same six-year period, the real minimum wage has increased on average 13.02% per year (Figure 7).

Figure 6 — Comparison of Annual Growth Rates Between Minimum Wage and TFP, 2008–24

Figure 7 — Comparison of Average Annual Growth Rates Between Minimum Wage and TFP, 2019–24

Note: This figure illustrates the geometric mean of the authors’ calculations.

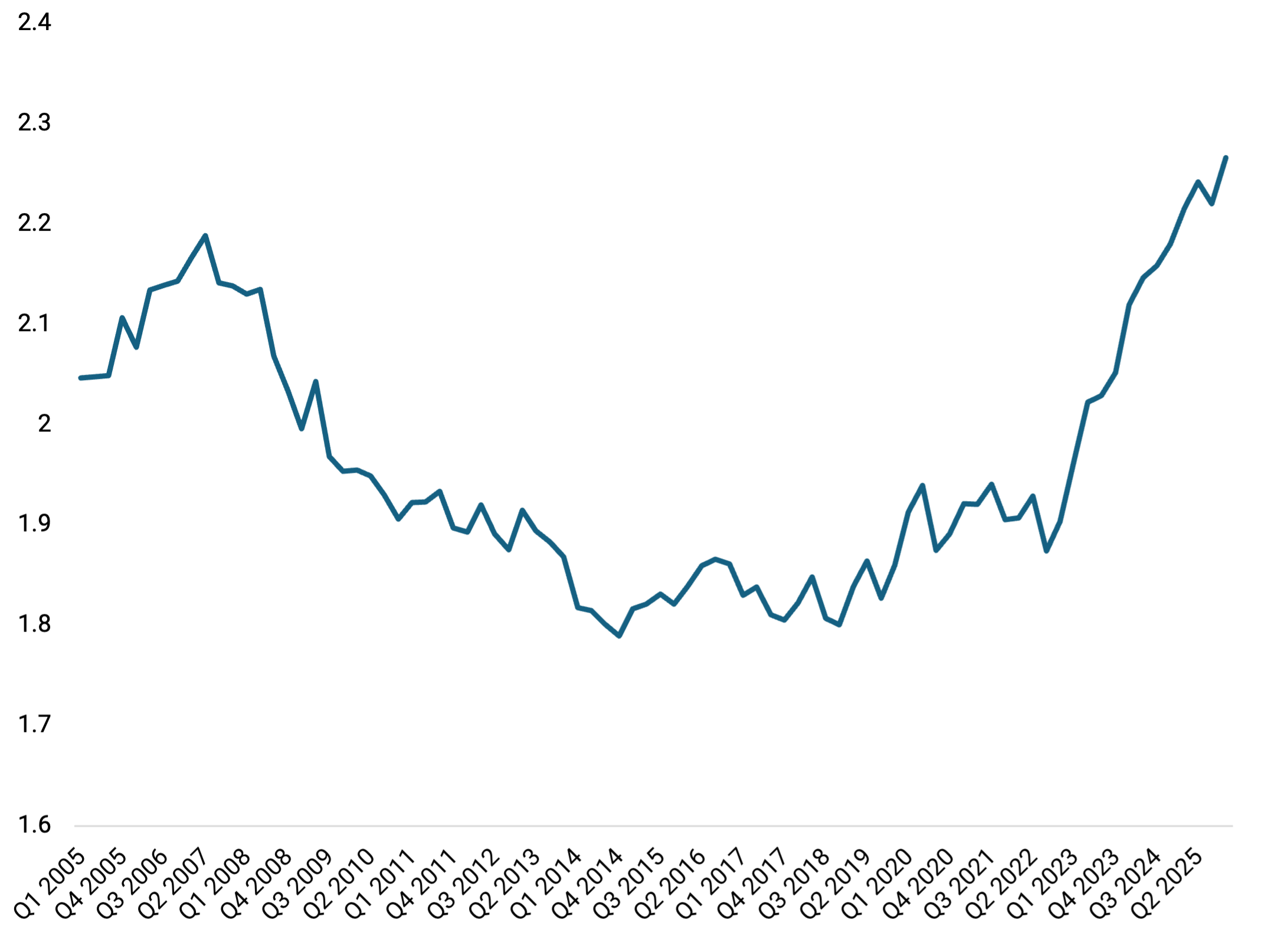

The substantial annual increase in the minimum wage since 2018 has significantly increased real hourly income in recent years (Figure 8). However, labor productivity in Mexico has declined during the same period, indicating inefficient worker output. Altogether, these trends constrain the country's competitiveness and long-term economic growth.

Figure 8 — Real Hourly Income, 2005–25

Note: The left axis refers to U.S. dollars based on their 2018 exchange rate with the peso. More specifically, prices and average FIX exchange rate (18.82 pesos per U.S. dollar) are based on the second half of July 2018 and are held constant. Regions are as defined by Banxico.

Another barrier to productivity growth is the lack of infrastructure investment. Because fixed investment has declined, this may further diminish total productivity, which negatively affects economic growth as well as Mexico’s potential to remain the United States’ most important trading partner.

Private and Public Investment

Since 2016, Mexico has experienced a lack of investment, both private and public. However, these investments experienced an increase at the end of the López Obrador administration due to the 2024 presidential election and the need to complete his infrastructure projects. More recently, productive investment has not kept pace with expectations. This represents an important element that is contributing to the slow growth of the country’s economy, as private investment boosts technology, research, and development, expands employment, and stimulates industrial growth and consumption.

The multiplier effect of private investment is essential for the economy’s overall health. Mexico’s challenges with maintaining the flow of capital has reduced its economic activity, creating a cycle of underinvestment and low growth. Complicating this scenario is the Mexican government’s decision to restrict investment in strategic sectors where the capital to invest is not available, including energy and other infrastructure.

Mexico is also facing low levels of public investment, especially in the last decade. Thus, its basic infrastructure, including roads, highways, ports, airports, power grids, and water systems are largely underfunded. Moreover, the fiscal budgets of its schools, universities, and health care system have successively been constrained, particularly from 2018 to 2024. Higher public investment in these key sectors would have a multiplier effect, as maintained and improved infrastructure would lower business costs and encourage more investment. This would also then attract more firms and increase job creation, increasing the skill level and well-being of Mexico’s workforce.

Long-standing underinvestment both in the public and private sectors diminishes innovation and productivity, creating a structural constraint for the overall economy. For example, Mexico’s energy sector has experienced underinvestment in power generation, which, if continued, will further discourage foreign direct investment (FDI). The rapid development of artificial Intelligence (AI) and substantial investment in U.S. data centers have driven strong demand for Mexican computer equipment. However, this has yet to translate into increased FDI in the sector, suggesting that Mexico is not currently capitalizing on robust increases in the U.S. investment.

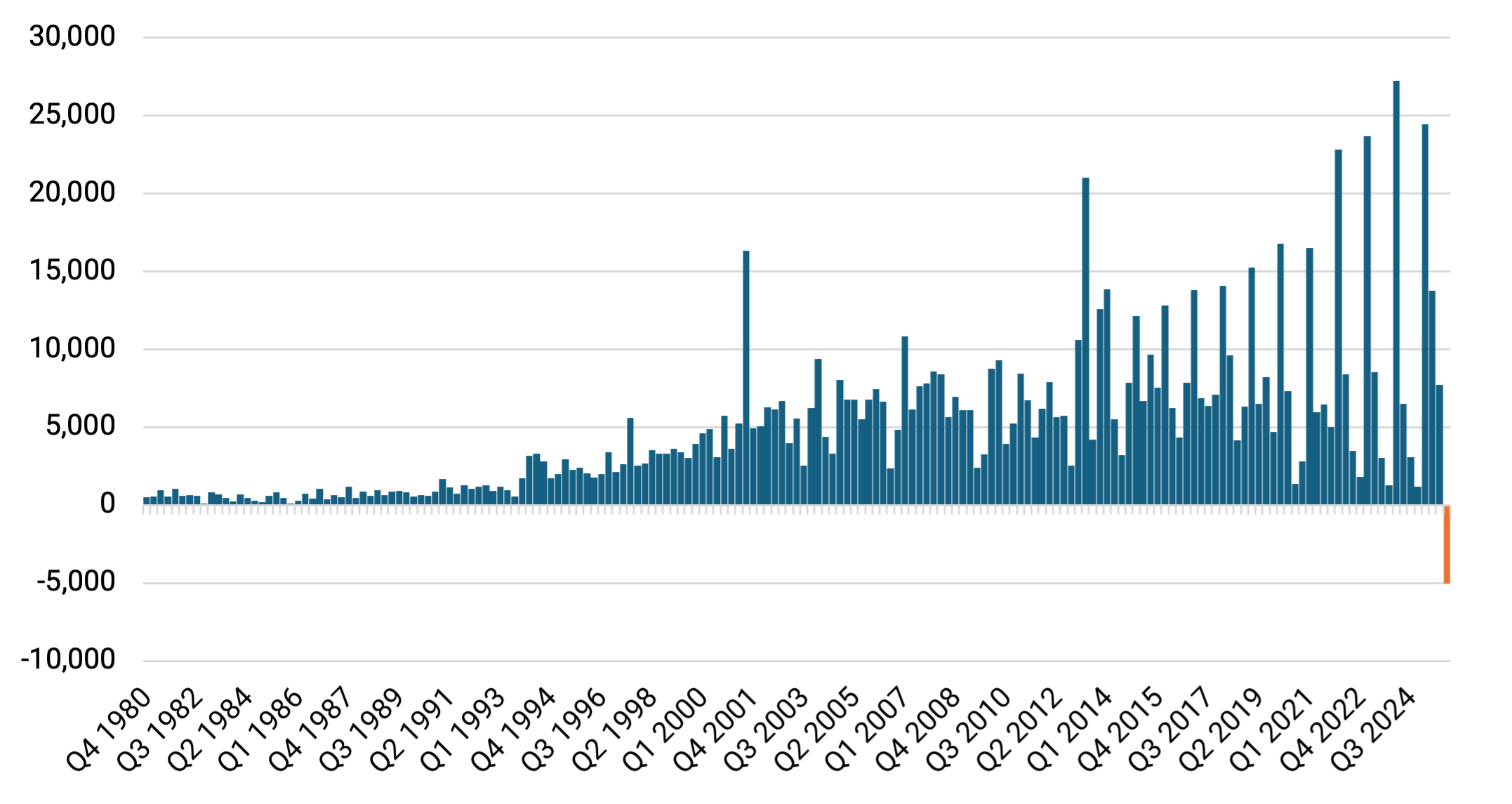

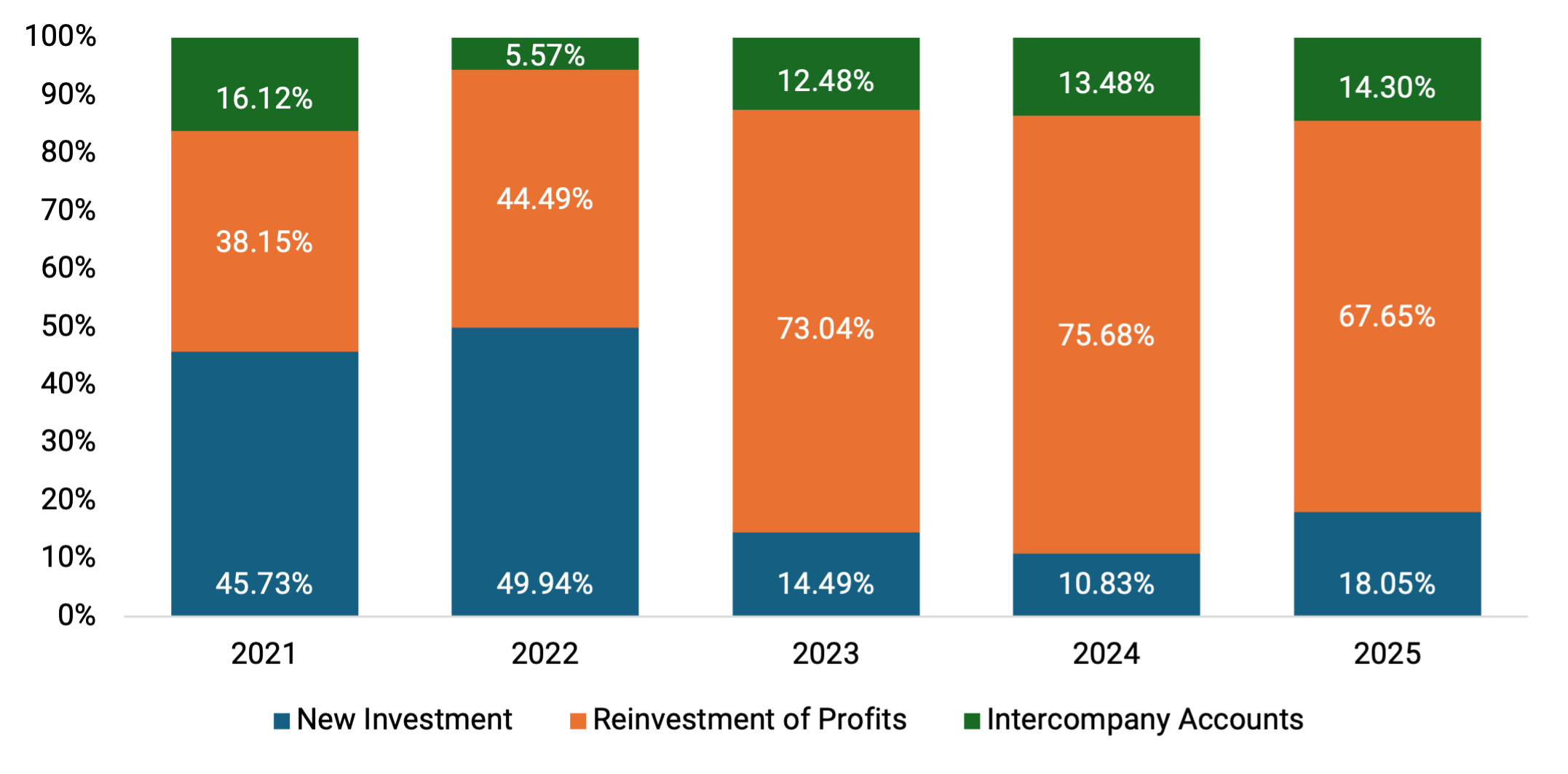

Although FDI in Mexico totaled $40.87 billion U.S. dollars in 2025 — a 7.74% increase in comparison to 2024 — the year concluded on a subdued note. The fourth quarter of 2025 saw a net divestment of $5.02 billion, the first such occurrence on record (Figure 9). Furthermore, new investments accounted for only 18.05% of the total in 2025, a significant decline from the 45–50% levels seen in 2021 and 2022 (Figure 10).

Figure 9 — Foreign Direct Investment by Quarter, 1980–2025

Figure 10 — Foreign Direct Investment by Type, 2021–25

Note: The percentage indicates the share of the total of foreign direct investment for each listed year.

Current incentives in the oil and power sectors are unlikely to effectively encourage companies to participate in these crucial industries. Moreover, a substantial percentage of public funds over the previous and current administrations has been allocated toward largely unproductive projects, such as the new airport outside Mexico City, various rail projects in the Southeast, and a new refinery in Tabasco, among others. None of these projects have yet to bear a profit or are unlikely to become profitable in the near future. However, subsidies sustaining these projects will continue into the mid-term future, further limiting the government’s ability to expand public investment. Below, subsidies to state-owned companies are also discussed, as they too constrain the possibility of increasing public investment.

Finally, the total investment numbers are also a point of concern. In 2024 and 2025, total public and private investment declined considerably. In 2025, public spending on fixed investment decreased by 28.4%, the largest reduction since 2021. In October 2025, the Ministry of Finance and Public Credit announced a 2026 budget of 960 billion pesos for fixed investment. While this represents a 22% increase in real terms, it remains below 2024 spending levels.

Furthermore, the government may be forced to further tighten its budget to prevent a widening fiscal deficit, as current economic assumptions for revenue and expenditure are likely overvalued. Consequently, the materialization of the 2026 fixed investment target remains at risk. In early February, the Mexican government announced 722 billion pesos of additional investment for 2026; although due to its classification as mixed investment, the additional funds’ impact on public finances remains uncertain.

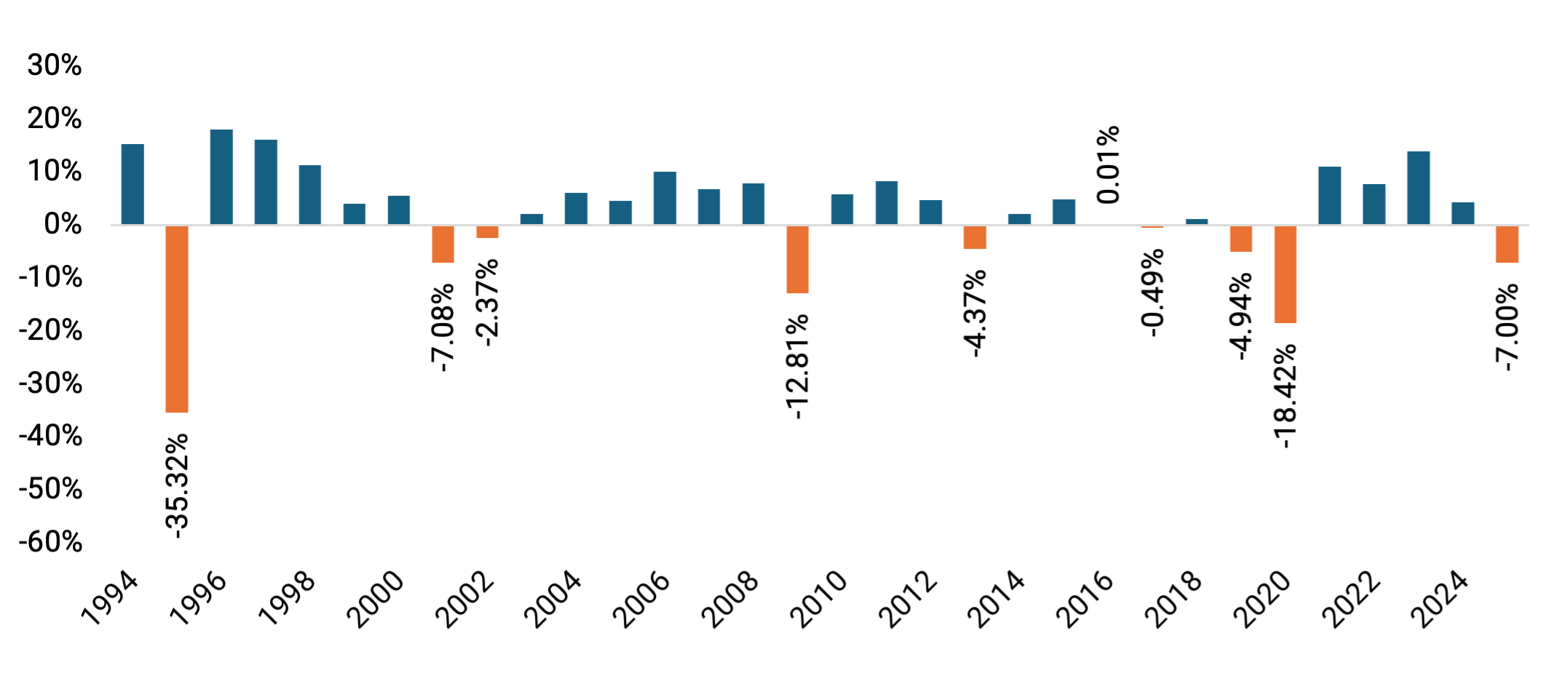

Gross fixed investment, which encompasses both public and private sectors, shows a 7% year-to-date (YTD) decline through November. This contraction has only been exceeded during comparable periods in 1995 (-35.32%), 2001 (-7.08%), 2009 (-12.81%), and 2020 (-18.42%) — all of which occurred during economic recessions (Figure 11). Lowered gross fixed investment rates affect output capacity and reduces potential GDP and long-term economic growth. Given these figures, the types of investments that can unlock Mexico’s economy will likely not materialize in the near term.

Figure 11 — Annual Growth of Gross Fixed Investment, 1994–25

Note: The figure covers January to November of each listed year.

Fiscal Position

Mexico’s fiscal position has been in decline. Although both the previous and current administrations have collected considerably more revenue than those in the past years, the federal budget is becoming increasingly rigid. In other words, there is little to no flexibility to increase public investment, as the number and amount of items already committed in the budget continue to rise. There are several reasons for Mexico’s constrained budget:

- Rigid federal budget.

- Rising debt.

- Subsidies to state-owned corporations.

Rigid Federal Budget

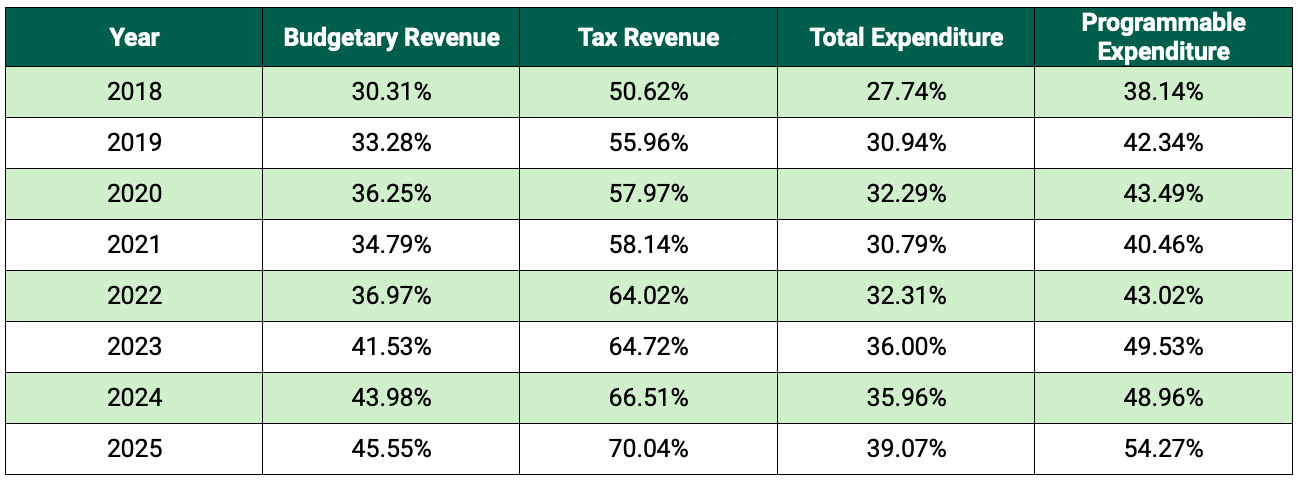

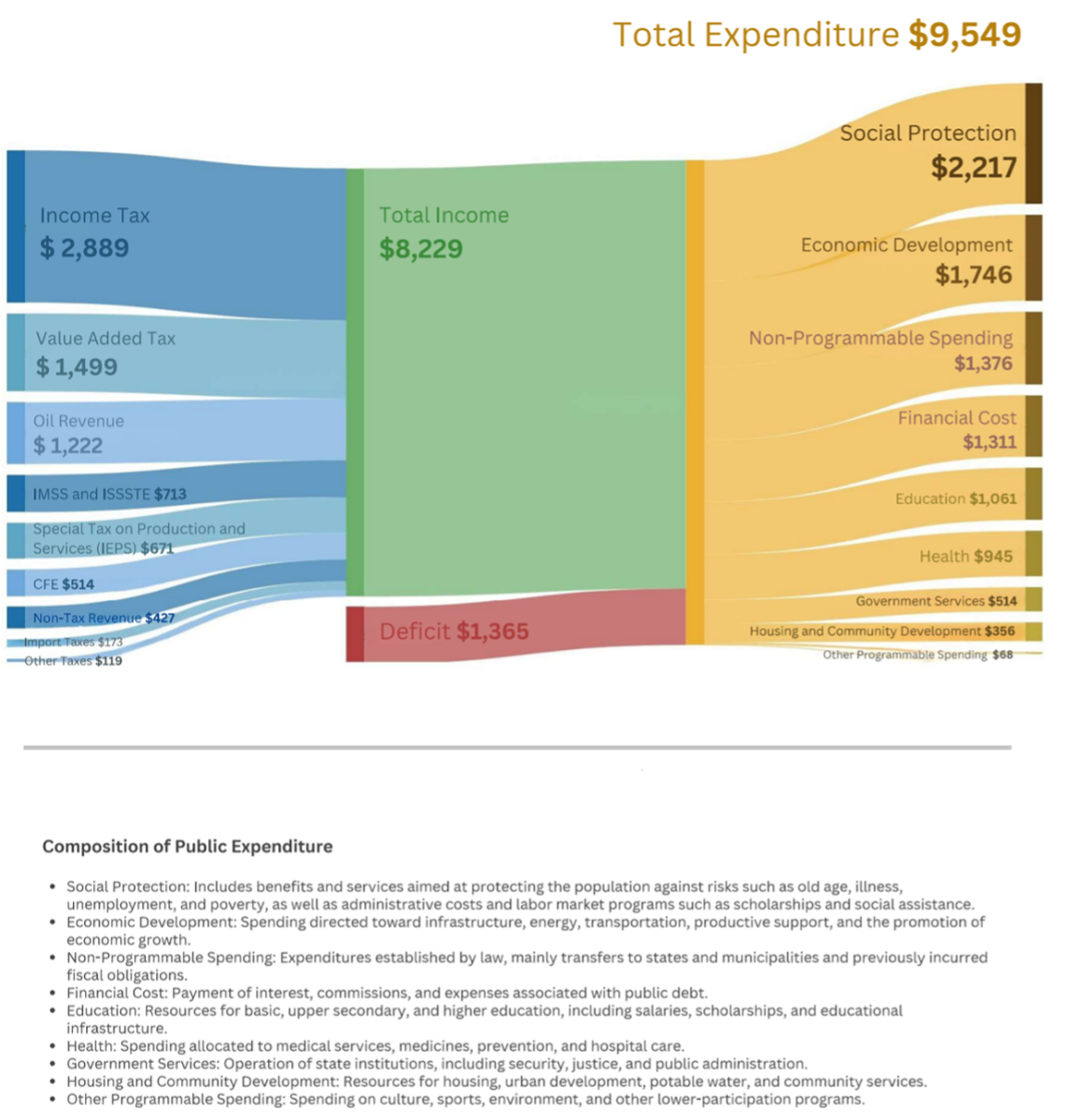

While the Mexican government has increased revenue collection in recent years, expenditure rigidity has also increased substantially over the last seven years, potentially compromising the health of public finances. In 2025, 70% of tax revenue was committed to social programs, pensions, and debt servicing costs, leaving only a small fraction for vital sectors such as health care, education, defense, and infrastructure (Table 1 and Figure 12).

This budgetary rigidity limits economic growth, while heightening the risk of credit rating downgrades, and it also can create pressure for a fiscal reform to increase revenue. However, given Mexico’s high levels of labor informality and aggressive tax enforcement, such a reform could further weaken employment, deepening its economic stagnation.

Table 1 — Rigid Spending as a Share of Revenue and Expenditures, 2018–25

Note: Rigid spending includes debt servicing costs, social programs, and contributory and noncontributory pensions.

Figure 12 — Public Sector Revenues and Expenditures as a Share of Total Expenditure, 2025

Note: Monetary amounts are in billions of pesos. The applications, Flourish and Canva, were used to create this graphic.

Altogether, Mexico’s recently increased revenue collection is primarily allocated to social programs, debt, and pensions, yet the country is forced to borrow funds to cover an expanding budget deficit, one that has not been managed effectively and would be difficult to remedy. Notably, while social programs and pensions create greater liquidity in the economy, these funds are largely for consumption, which does not contribute to long-term economic growth.

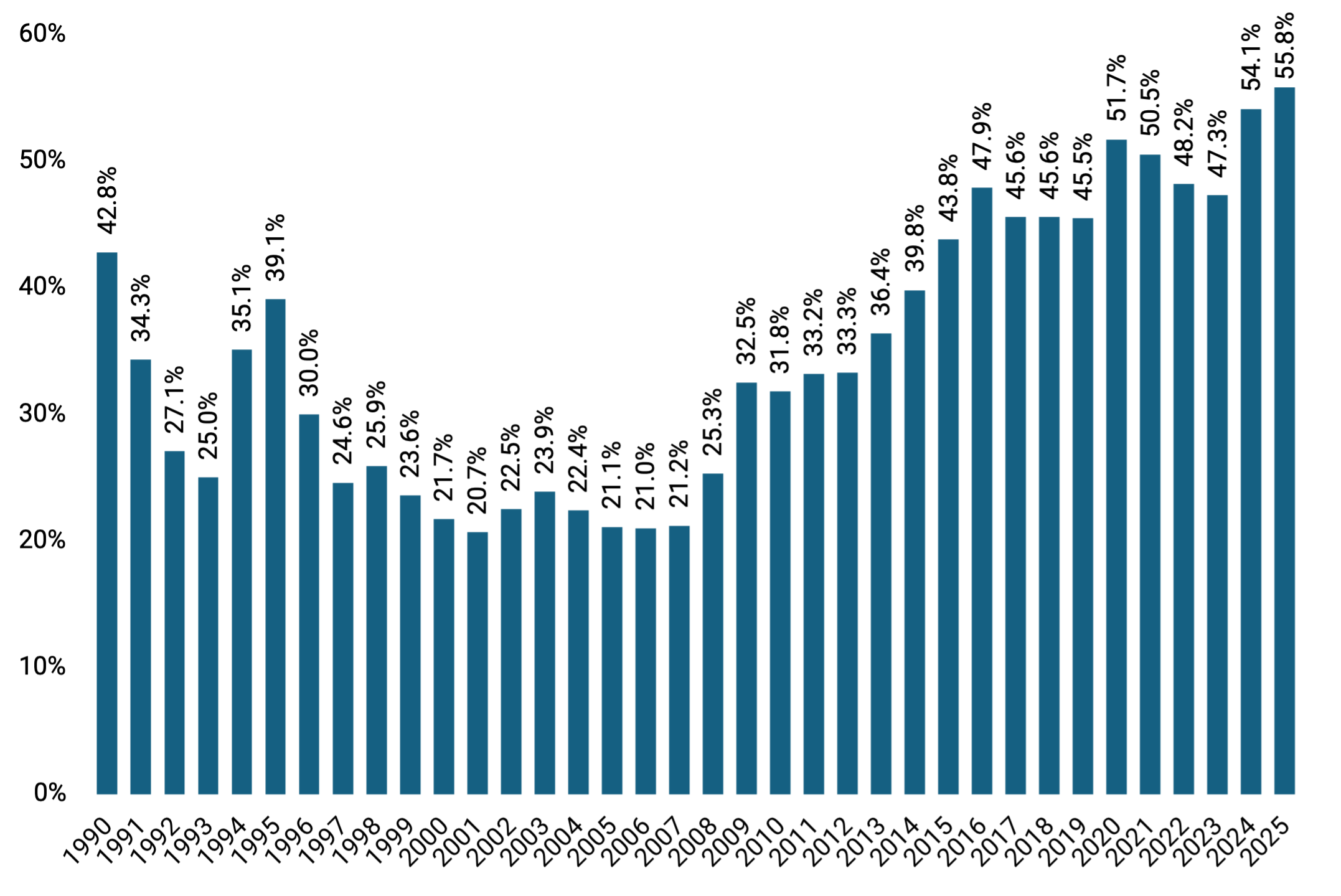

Rising Debt

Currently, the Mexican government’s commitments included in the fiscal budget are not easily reversed. As a result, the budget deficit remains high, despite the Sheinbaum administration’s efforts to reduce its size. Moreover, to meet the country’s rigid budget expenditures, the government has borrowed funds more extensively, particularly in the last two years.

If current spending rates hold, the total debt as a percentage of GDP may approach 60% by the end of the current administration in 2030 (Figure 13). This is an important threshold; if the government does not effectively manage its spending or implement structural reforms to encourage growth, international markets are likely to view Mexico’s fiscal position more negatively. Such structural reforms are likely to come at a political cost to the government and its ideological project. Any significant structural reforms, therefore, are expected to face considerable resistance from the governing coalition.

Figure 13 — Gross Debt-to-GDP Ratio, 1990–2025

A growing national debt increases the inflexibility of the federal budget, as the government has to dedicate a greater percentage of revenue to debt servicing. This is in addition to sustaining expanded cash transfer programs and raising both self-sustaining and noncontributory pensions. Although there appears to be some remaining capacity for debt growth, the main concern is that the debt is predominantly directed toward nonproductive investments rather financing the budget deficit and other current expenditures.

A minimal amount of the income from additional debt, if any, is allocated to mid- and long-term productive investments. Importantly, as Mexico nears the 60% threshold for the debt to GDP ratio, no significant course correction efforts have yet to be taken, despite the risks of negative impacts from international market responses. Rather, the Mexican government is likely to continue its borrowing practices into the near future.

Subsidies to State-Owned Corporations

Subsidizing state-owned companies also comprise a sustainable portion of debt allocations, which continue to draw substantive resources from the federal budget. Yet, Mexico’s government is committed to ensuring substantial control of certain economic sectors it considers strategic. That includes the energy industry, particularly oil and power generation. The energy sector’s current constitutional, legislative, and regulatory conditions largely constrains and disincentivizes private and foreign investment. The record shows that investors tend to have low confidence in the energy sector becoming profitable soon.

Moreover, both Pemex, the national oil company, and the Federal Electricity Commission (CFE), the national power utility, are heavily subsidized, adding significant weight to the federal budget. These subsidies, which constitute an important line item of the overall federal budget, are likely to continue in the near term, as the government’s recently published regulatory framework does not appear to have gained traction in the investment community. Without further reforms to invite, incentivize, and promote private and foreign investment in the energy sector, Mexico will likely face challenges in meeting its energy needs as well as new investors’ demands. This too will constitute yet another structural brake on Mexico’s growth.

Sticky Inflation

Inflation rates in Mexico have remained manageable but sticky. Inflation increased in January 2026 to 3.79%, well above Banxico’s 3% target. Moreover, core inflation stood at 4.52%, with food and beverage inflation at 6.13% for the same month.

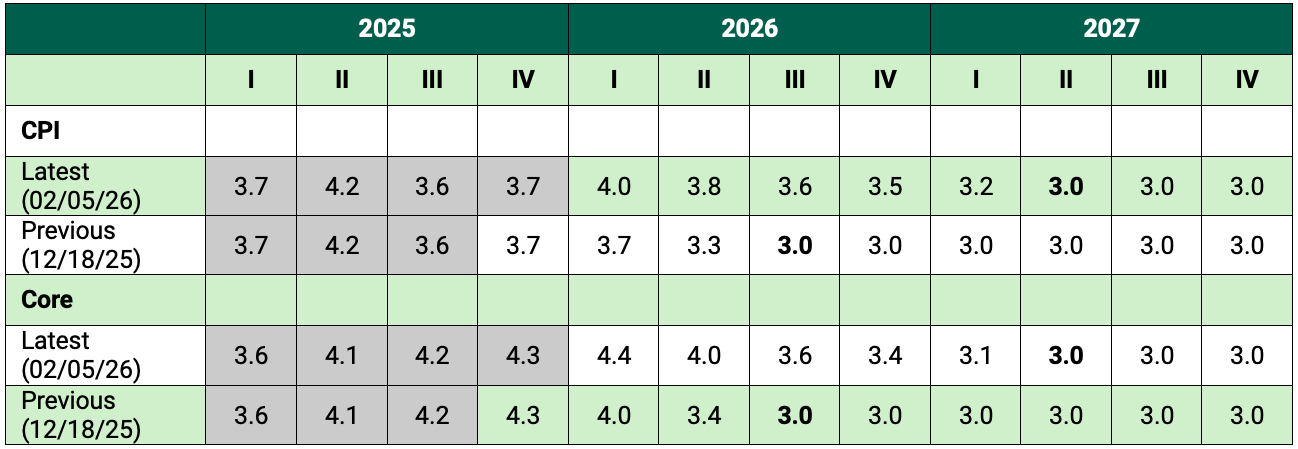

Another point of concern is the declining credibility of Banxico’s forecasts and its autonomy, as their projections have proven overly optimistic by postponing the expected timeline for reaching the 3% inflation target nine times (Table 2). As per the latest Banxico forecast, inflation is expected to reach that goal by the second quarter of 2027. However, outcome is far from guaranteed, as stated by Banxico’s Deputy Governor Jonathan Heath.

The persistence of inflation above the 3% target along with Banxico’s perceived tolerance of the current inflation rate have shifted private sector expectations. According to Banxico’s Survey of Private Sector Forecasters for January 2026, the market does not foresee a near-term convergence to that target, with median annual inflation rate estimated at 3.75% for the 1–4 year horizon and 3.60% for the 5–8 year horizon. Deferring the expected convergence date, coupled with highly optimistic official forecasts, suggests monetary policymakers’ tolerance for elevated inflation readings.

It is important to note that Banxico’s 3% target includes a variability range of plus or minus 1% to accommodate natural fluctuations of annual inflation, and it is not a tolerance range for sustained deviation.

The erosion of Banxico’s credibility could become a structural headwind to economic activity in Mexico due to two factors: 1) the inability to actively address inflation leads to higher tolerated inflation levels, and 2) the inflation expectations channel is one of the most critical monetary policy transmission mechanisms in Mexico. Therefore, the loss of confidence in reaching the inflation target could weaken monetary policy’s overall effectiveness.

Table 2 — Banxico’s Headline and Core Inflation Forecasts by Annual Percentage Change of Quarterly Average Indices, 2025–27

Note: CPI refers to Consumer Price Index. The shaded areas indicate observed data.

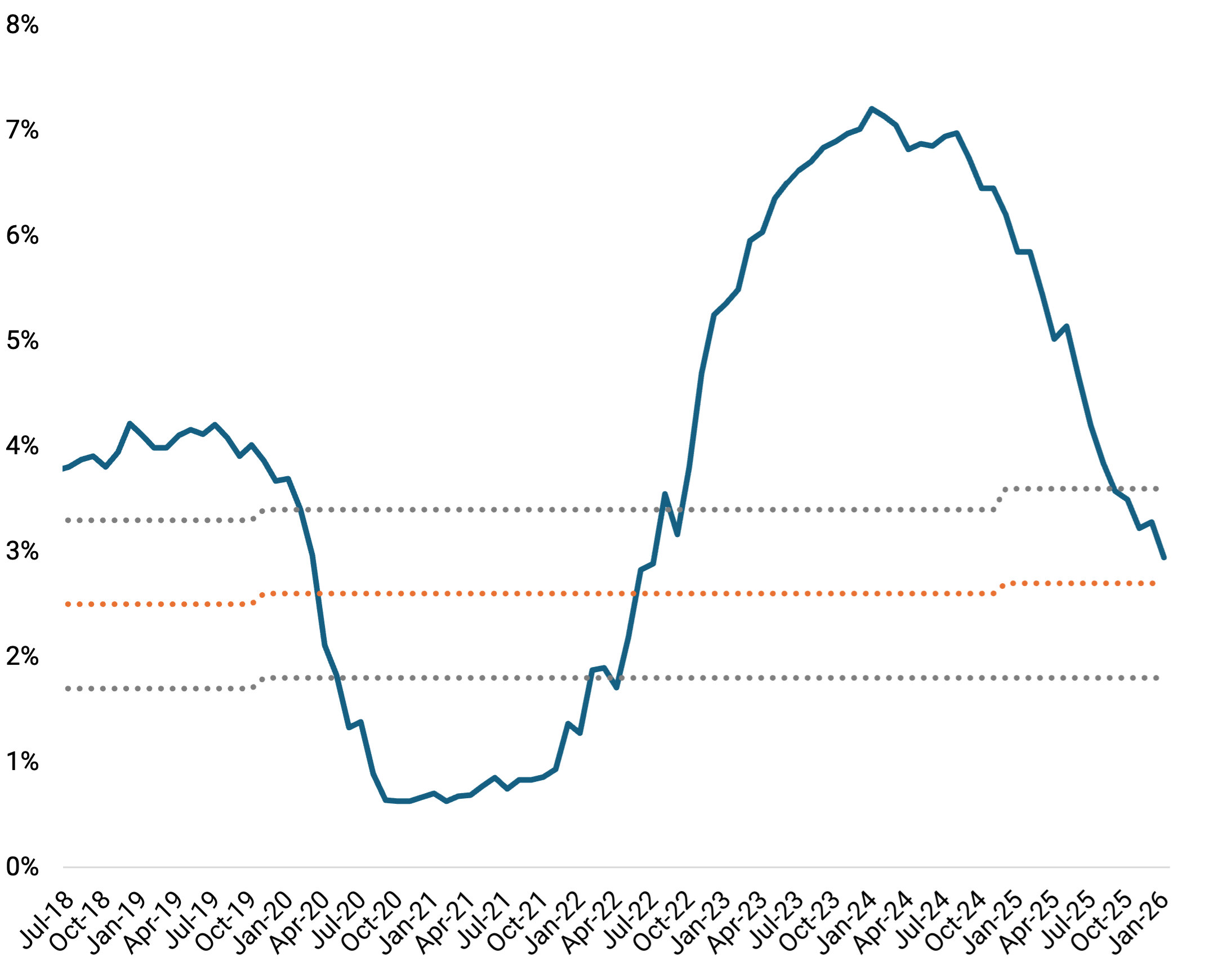

The real ex-ante interest rate — the nominal interest rate minus the expected inflation rate — offers a way to measure the current monetary policy stance, and per Banxico’s reports, this rate stood at 2.94% in January 2026, residing within the neutral range of 1.8% to 3.6% (Figure 14). This indicates that monetary policy is not actively addressing inflationary pressures, especially as inflation is rising to 3.92% year-over-year in the first half of February 2026, well above the 3% target. At the same time, core inflation rose to 4.52%, driven by beverage and food prices with an annual inflation of 6.28%, the highest since the first half of December 2023. Rising inflation is contributing to restricted consumption and, thus, is likely another limitation on short-term economic growth.

Figure 14 — Short-Term Real Ex-Ante Interest Rate, 2018–26

Note: Author utilized the Fisher equation calculation.

Moreover, Mexico’s government has not sought to reform its tax system since 2019, relying instead on aggressive revenue collection methods and maintaining or increasing excise taxes on certain products with low elasticity, such as cigarettes, sugary drinks, gasoline, etc. These excise taxes also contribute to inflation, as they are generally passed onto the consumer at the point of sale.

Impact of Structural Changes: Judicial and Regulatory Reforms

Over the course of the López Obrador and Sheinbaum administrations, Mexico has undergone a series of constitutional, legal, and regulatory reforms that have likely further locked the country into low-growth gear.

One of most extensive changes is the reshaping of the judicial system. The entire judiciary — from Supreme Court justices, circuit court magistrates, to federal judges — is now popularly elected rather than appointed through promotions, competitive examinations, and congressional confirmations. This shift has three primary implications:

- The government’s ruling party gained dominance in the judiciary following the elections, and thus, the judiciary is expected to decide on constitutional and legal matters and their effects on potential complainants based on the executive branch’s political program.

- Political interests have largely supplanted technical expertise, as all judges are now required to run for office, which has relatively few barriers to entry. This change could also open the judiciary to organized crime influence.

- Companies are excepted to increase spending to avoid litigation, instead opting for arbitration or mediation. This would tighten operating margins and, consequently, leave less capital available for investment and hiring. Under these conditions, businesses — particularly mid-sized firms — would experience more vulnerability and could be driven to exit the market or migrate to the informal sector.

The second structural change is the dissolution of several regulatory agencies. The regulation of broad economic sectors is now in the hands of various government ministries, which are largely comprised of economic actors, regulators, and dispute settlers. Thus, complainants will be required to engage with influential cabinet secretaries who are tasked with regulatory decision-making, while in the past, independent regulatory agencies would review and determine outcomes.

This significant shift in regulatory policy could also be used by the executive to direct investment toward sectors that it considers strategic and also exclude investment from other ventures. This is particularly notable in a context where the executive branch could select to invest in economic sectors owned by the government, such as energy and other infrastructure.

These changes have not fully ensured a level playing field for all investors. Under these reforms, the expectation that legislative, executive, and administrative decisions can be appealed effectively and fairly with an experienced judiciary or independent regulatory apparatus has weakened. Both the judiciary and regulatory changes have introduced considerable uncertainty for investors, which has likely reduced the flow of capital into the country.

The Sheinbaum administration has also recently introduced an electoral reform that could alter the rules of proportional representation and protocols for political parties’ public financing. While specific details remain fluid, there is a risk that this reform could challenge democratic processes.

Trade and Investment Uncertainty

The uncertainty generated by President Donald Trump’s tariffs and intentions to influence the direction of the trade system has directly affected Mexico. While this policy may change in the next U.S. administration, policy shifts under the Trump administration has clarified Mexico’s overexposure to U.S. commercial policy.

Given the Trump administration’s tariff schedule, Mexico is one of the least affected countries. However, one of their significant effects has been on the slowing of investment in Mexico, as most companies appear to be in a holding pattern to understand tariffs’ effects and then calculate the differentials among countries and potential changes in future tariff schedules. The recent U.S. Supreme Court decision regarding the Trump administration’s tariffs has likely increased this uncertainty.

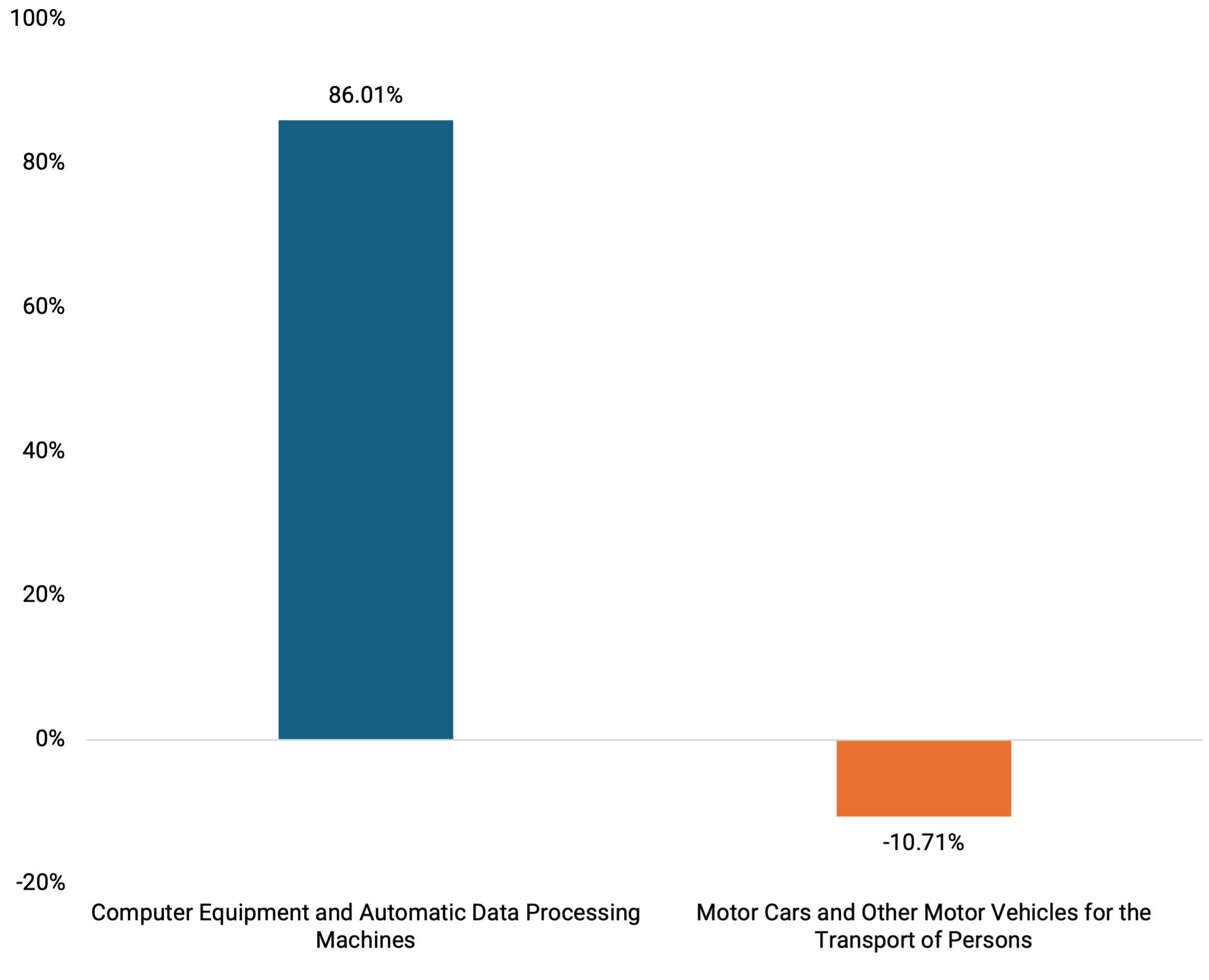

For Mexico, this uncertainty has largely driven brownfield investment, with minimal greenfield investment entering the country. This dynamic is thrown into sharp relief when industries are compared. While exports of computers — computer equipment and automatic data processing machines — and medical equipment have risen, automotive exports have declined in 2025 and appear to be awaiting the outcome of the 2026 USMCA review and any potential revisions (Figure 15).

Figure 15 — Annual Growth of Computer Equipment and Automobiles Exports, 2025

Note: Computer equipment falls under the Harmonized System (HS) Code of 8471, and motor cars and other motor vehicles fall under HS 8703.

Importantly, the decline in fixed investment is not solely attributable to uncertainty surrounding the USMCA review. Risk perception in Mexico began to shift prior to trade-related concerns, instigated by structural reforms. As of November 2025, private investment in machinery and equipment has fallen by 15.68% compared to August 2024 — the period immediately preceding the approval of the judicial reform.

While computer equipment exports prevented a decline in total exports in 2025, this growth is at risk in 2026 due to high-capacity utilization. The subsector for computer equipment and electronic components is operating at 94.6% capacity. Additionally, the computer equipment branch specifically has reached 99.4% utilization, suggesting that any further expansion in production or exports will largely depend on new investment.

Export Strengths and Trade-Offs

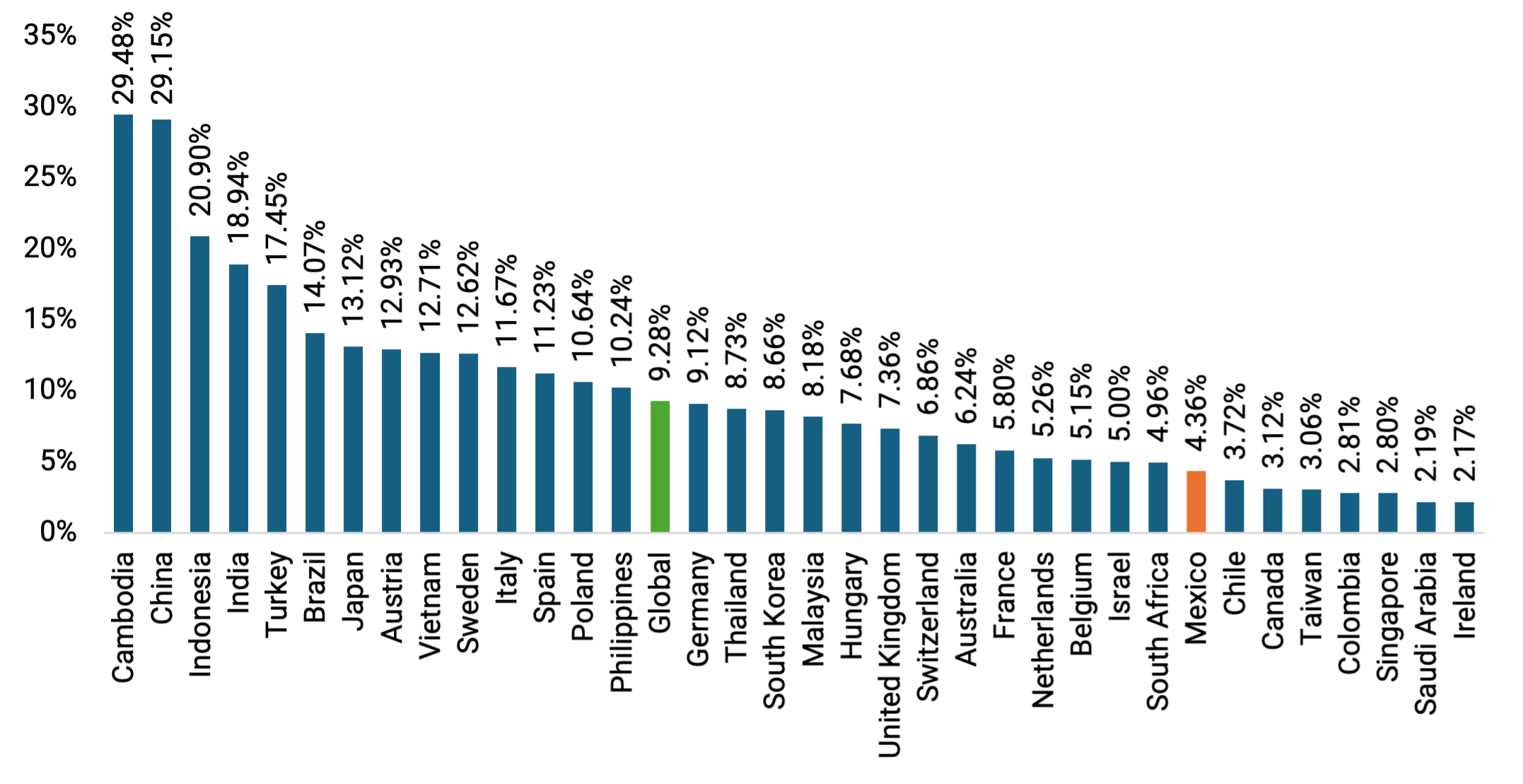

As of late, Mexican’s export sector has helped sustain the economy. Tariffs imposed by the Trump administration have been exempted for USMCA-compliant exports, giving Mexico an advantage over other countries, especially one of its main competitors — China (Figure 16). This largely explains why Mexican exports to the United States have remained robust.

Pending the status of the Trump administration’s tariff policy, the gap in tariffs between Mexico and other major exporters is likely to remain in the near future. At the same time, Mexico’s structural trade advantage also signals its structural dependence on access to U.S. capital and markets. Thereby, these economic factors may increase Mexico’s exposure to U.S. pressure in several policy areas.

Figure 16 — US Tariffs by Country of Origin as of December 2025

Note: The figure includes the top 35 source countries, accounting for 92.88% of total global imports.

Mexico’s export growth is increasingly driven by electronic goods and computers, including servers and automatic data processing machines, and continues to expand. However, the uncertainty generated by the Trump administration’s tariff and trade policies has significantly impacted the automotive industry — historically Mexico’s most important manufacturing sector.

Until 2024, the automotive industry accounted for the largest share of Mexico’s exports to the U.S., with both light and heavy-duty vehicles serving as the top export products. This trend ended in 2025, as automotive exports fell to second place, overtaken by computer equipment. While this shift may initially appear to be a transitory development with limited implications, this is likely not the case because the trade-offs in employment and investment do not directly correspond.

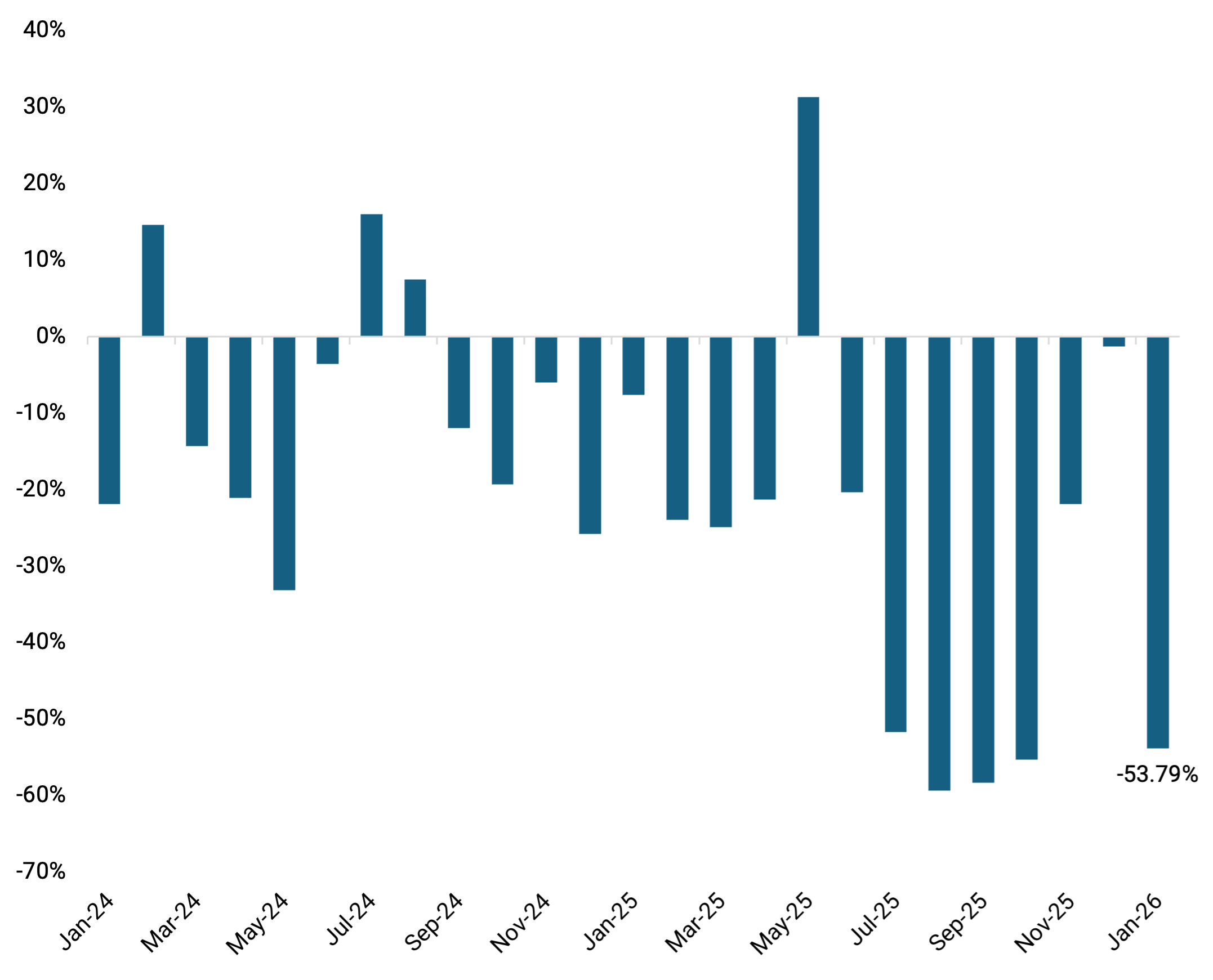

The Mexican automotive industry is deeply integrated into the U.S. supply chain, driving job creation and capital expenditure, which translates into higher productivity. Conversely, a significant portion of the computer equipment sector involves transshipment, which generates a smaller economic spillover than the automotive industry. Thus, the computer equipment sector does not stimulate growth in fixed investment or job creation at the same rate as the automotive industry. Additionally, total exports of heavy-duty vehicles have recently declined, slowing what could be a productive sector without the current tariff environment (Figure 17).

Figure 17 — Annual Growth of Heavy-Duty Vehicle Exports, January 2024–January 2026

Weak Internal Market and Diversification

Mexico’s economy, like many others, relies on domestic consumption for much of its economic activity. In 2025, domestic consumption was roughly 71% of GDP. However, while private consumption in Mexico has shown some resilience, it has been volatile.

Particularly, fluctuations in the service sector reflects relatively subdued consumer confidence, despite robust cash transfer programs, which should, in theory, lead to higher consumption. Most Mexican households are unable to raise their consumption levels, not only because income and wealth is unevenly distributed but also because credit is relatively scarce and most subsidies and remittances are used to maintain basic household consumption. To an earlier point, the export economy has improved and is able to consume at greater levels than the economy focused on the domestic market.

The economic model implemented by the Mexican government in the early 1990s, integrating the Mexican and U.S. economies through the North American Free Trade Agreement — which then became the USMCA — produced significant benefits for regional trade. Over the last three and a half decades, Mexican exports to the United States have grown to compete with those of any other country, such as China and Canada. However, under the U.S.’ current protectionist and fluctuating trade policy, the strength of this policy has weakened.

While Mexico has sought to diversify its economy and trade relations — as currently 83% of goods exports are sent to the U.S. — it has not effectively managed to do so despite numerous trade agreements. Instead, its economy has increased its dependence on U.S. capital and markets; for example, over the last 10 years, 39.7% of Mexico’s total FDI has depended on the U.S and is likely to remain so. At the same time, Mexico’s economic integration with the U.S. increases its exposure to shifts in U.S. trade policy, especially as the uncertainty from tariffs has prevented investors from committing to long-term investments.

Moreover, to mitigate Washington’s pressure on China’s investments in the Mexican market — especially the possibility of China using Mexico as a way to indirectly access U.S. markets — as of Jan. 1, 2026, Mexico imposed a 50% import tariff on more than 1,400 goods from countries without a trade agreement, which includes China. These tariffs were also seen as a revenue-raising mechanism.

For various reasons, including companies increasing stocks of Chinese imports between the announcement in early September and the tariffs in January, the expected costs to Mexican consumers have not yet been reflected in inflation rates. However, these tariffs are likely to affect the Mexican industry, since a large portion of these imports are not consumer goods but rather intermediate industrial inputs. While also potentially discouraging fixed investment, this move will likely increase Mexico’s vulnerability to U.S. trade policy changes in the near future.

Main Economic Challenges Ahead

Mexico is unlikely to experience an economic recession, yet its economy across nearly all sectors seems to be locked in low gear. This condition should be understood as the product of two forces:

- Increasingly competitive international environment, which has largely occurred without fundamental adjustments to Mexico’s economy, as well as alongside the uncertainty introduced by the Trump administration into the world trade system.

- Reconsideration of the fundamentals of the country’s economy, which is a manageable prospect for Mexico.

Many of the challenges facing the Mexican economy stem from domestic factors, particularly its recent structural reforms. By significantly altering important scaffoldings of its modern economy — reversing an education reform, eliminating independent regulatory agencies, and transferring key strategic sectors such as energy and other infrastructure, to state ownership, among others — the country has locked itself into a constrained position.

Moreover, by restructuring its judiciary into an arm that could be influenced by the executive, along with the reforms to Amparo Law, challenging governmental acts has become more difficult. This is particularly the case for investors, as little recourse may occur in cases of investor disagreements with government rules, regulations, and administrative decisions.

Policy Recommendations

The Mexican economy’s structural issues locking it in low-growth gear are difficult to solve along current policy paths.

Addressing these issues should include substantial constitutional and legislative changes to incentivize investment, such as:

- Reconsider the judiciary reform.

- Open energy and other infrastructure markets to encourage private and foreign investment.

- Restore independent regulatory agencies.

- Revise budget priorities.

More specifically, Mexico’s fiscal budget should aim to limit cash transfer programs and pensions as well as channel further resources to strategic sectors that would increase future productivity, including education and skilling programs, science, technology, critical infrastructure, and health care. These revisions should be made alongside efforts to reduce the deficit and ensure the national debt remains under 60% of GDP to maintain the country’s investment-grade status.

Another solution for Mexico lies in FDI — a driver that was prominent until 2022, when new investment accounted for 50% of the total inflow (Figure 10). If new investment returns to that proportion and profit reinvestment remains steady, it would directly trigger a 1.5% point increase in GDP growth. Achieving this would require the following:

- Promote Mexico abroad, tasks formerly managed by ProMéxico and currently by several individual state governments.

- Upgrade public infrastructure, specifically highways and electricity generation.

- Establish a climate of legal and economic certainty, particularly regarding labor costs, fiscal policy, and the rule of law.

Finally, while trade relations are not easily diversifiable for Mexico, the country can continue to seek additional commercial partners. This can be accomplished while maintaining a policy of economic complementarity with the United States, as its asymmetric interdependence is unlikely to change. The pursuit of new partners should extend beyond trade agreements. A viable path forward for Mexico involves increasing export complexity to foster global reliance on its economy, mirroring Taiwan’s strategic dominance in semiconductors.

While this shift may not entirely offset the asymmetric interdependence with the United States, it would yield significant long-term benefits and reduce trade risks. However, growing its industrial and export complexity will require Mexico to address its current low-gear economic status through institutional changes, strategic planning, and high and sustained levels of fixed investment over the coming years.

This publication was produced by Rice University’s Baker Institute for Public Policy. Wherever feasible, the material was reviewed by outside experts prior to release. Any errors or omissions are solely the responsibility of the author(s).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author(s) and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s) and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.