Author(s)

Recent Developments in Cryptocurrency Tax Reporting

In several congressional hearings, IRS Commissioner Charles Rettig emphasized the magnitude of tax underreporting associated with cryptocurrencies. In one testimony, he pointed to the lightly regulated cryptocurrency sector as a major culprit in the growing tax gap: the difference between tax owed and actually paid on time amounts to a whopping $1 trillion per year.

Although some were stunned by the sheer size and increase of the $1 trillion amount — after all, the latest IRS estimates for 2011 to 2013 showed a tax gap of $441 billion per year — Commissioner Rettig’s message is clear: to deter cryptocurrency tax evasion, Congress needs to grant IRS more authority so it can provide better guidance and request more disclosure on cryptocurrency-related transactions. This blog post reviews three recent developments of cryptocurrency tax compliance: IRS modification of Form 1040, the agency’s enforcement actions through the use of John Doe summonses, and the reporting requirements in the Senate-approved infrastructure bill.

2019, 2020 and 2021 Tax Returns

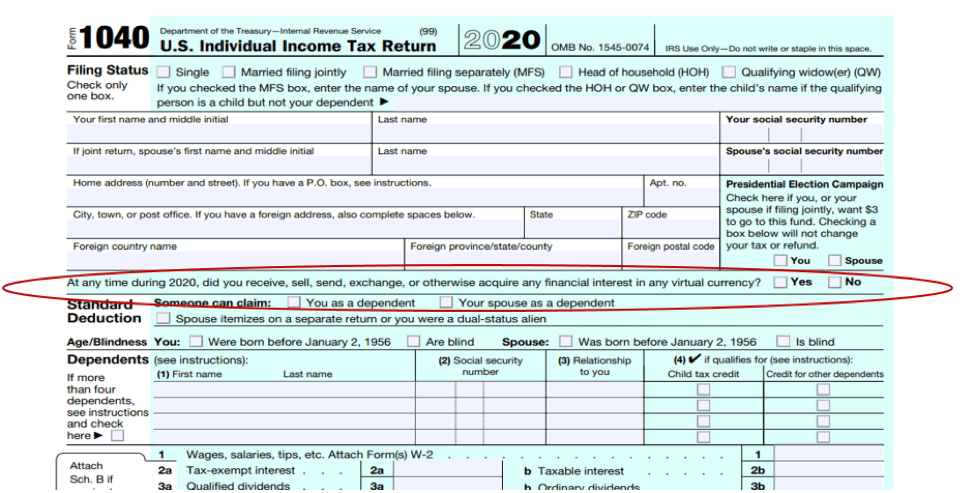

The IRS has acted against cryptocurrency tax noncompliance for several years; one of the most notable is the modification of Form 1040. In 2019, the IRS included a question on Schedule 1 of Form 1040 for the first time, asking taxpayers if they received, sold, sent, exchanged, or otherwise acquired any financial interest in virtual currency during the year. This question, seemingly innocuous to non-cryptocurrency investors, shows that the IRS is aware of the importance and prevalence of cryptocurrency transactions, and is beginning to address the issue within its authority.

The following year, the IRS moved the same question to Form 1040 itself. Some practitioners found the new location fascinating: because the agency puts the cryptocurrency question immediately below the taxpayer’s name and address, it almost seems to indicate the IRS cares more about the taxpayer’s cryptocurrency trading than other income-generating activities. Others applauded moving the question to Form 1040: because taxpayers who do not report income using Schedule 1 may accidentally skip the cryptocurrency question, the new location brings the item to the front and center of taxpayers’ attention. Regardless of how one views the change, it was clear to taxpayers that the IRS wanted to know whether they engaged in cryptocurrency-related transactions in 2020.

Figure 1 — IRS Form 1040

In the draft Form 1040 for 2021 tax returns, released in July, the cryptocurrency question remains on the first page of Form 1040, but the wording is slightly different. It asks taxpayers: “Did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency?” The word “send” was removed and “otherwise acquired” became “otherwise dispose.” This change indicates that the IRS is narrowing its inquiry to taxable events, consistent with its position described in the FAQ on Virtual Currency Transactions (Question 5, updated in March 2021).

Tweaking a question on Form 1040 across three consecutive years shows that cryptocurrency tax compliance is a priority for the IRS. Depending on the level of additional authority the agency obtains from the legislators, this question and the associated reporting rules may continue to evolve.

A recent pending court case may further refine the taxability of cryptocurrency. A couple who is engaged in cryptocurrency mining, the process of creating new crypto assets through verifying information, claimed their income associated with mining should not be taxable until they sell the tokens. Because the IRS views cryptocurrency as property in most cases, mining cryptocurrency “is comparable to an author writing a book or a baker making a cake,” the plaintiffs argued.

Enforcement Through John Doe Summonses

From the IRS’ perspective, a typical summons is issued when the agency knows the name of a specific taxpayer. However, a John Doe summons is used to obtain records from third parties about unnamed taxpayers in a certain group without alleging anyone of wrongdoing. Specifically, the IRS has reasonable basis to believe these taxpayers “may have failed to comply with any provision of any internal revenue laws.”

In 2016, the IRS issued a John Doe summons and requested that Coinbase, a U.S.-based cryptocurrency exchange, turn over information about U.S.-based customers whose transactions exceeded $20,000. As a result, Coinbase submitted data from 13,000 customers to the IRS in 2018 — and the IRS subsequently indicated that it received more than 1,100 amended tax returns and collected $13 million in taxes from these cryptocurrency holders, plus another $12 million from others, such as non-filers.

In the first two quarters of 2021, the agency served John Doe summonses to Circle Internet Financial Inc., a digital currency exchange located in Boston, and Kraken, a California cryptocurrency exchange, hoping to get similar results.

In large part, the IRS targets cryptocurrency exchanges because it is more cost-effective to focus on them than many taxpayers who may each owe varying tax amounts. However, an enforcement gray area is that the exchanges typically do not issue Form 1099-B, which is commonly used when taxpayers sell stocks, bonds, derivatives or other securities through a broker. Form 1099-B includes a range of information such as gross proceeds, cost basis (to calculate capital gains or losses), and the date on which a certain security was acquired or sold (to determine whether the capital gains or losses are long- term or short-term in nature) that taxpayers can readily use for tax filing.

Instead of Form 1099-B, some exchanges issue Form 1099-MISC, which reports a gross amount of income but not the cost basis. Other exchanges provide Form 1099-K, which is typically used by third party settlement organizations such as PayPal and certain sharing economy platforms. Similar to Form 1099-MISC, Form 1099-K reports gross income only; taxpayers need to keep track of their own tax basis to ensure proper compliance. Still others do not provide any tax form at all.

Several governmental studies identify the lack of third-party information reporting as a key reason that IRS cryptocurrency enforcement efforts are hampered. And they generally recommend additional information reporting and data gathering – not only about cryptocurrency tax compliance but also the transactions themselves so that regulators can better manage the evolving industry.

The 2021 Infrastructure Package

These recommendations were manifested in the infrastructure bill most recently passed the Senate in early August 2021. A provision in the $550 billion package requires cryptocurrency brokers to report digital asset transactions to the IRS. In addition, businesses that receive more than $10,000 in cryptocurrency in a single transaction must also disclose the transactions to the IRS by filing Form 8300. According to the Joint Committee on Taxation (JCT), the provision is estimated to raise $28 billion over a decade.

The broker reporting requirement expands the definition of broker in Section 6045 of the tax code to include any person “responsible for regularly providing any service effectuating transfers of digital assets on behalf of another person.” This essentially tasks brokers of crypto assets with the same reporting responsibilities as brokers of stocks and bonds.

The cryptocurrency industry strongly criticized these requirements after the draft first appeared in late July 2021. Industry practitioners indicated the scope of “broker” is overly broad and practically includes anyone who is paid a fee to facilitate transfers of cryptocurrency between third parties on a regular basis. For instance, miners who help verify and support cryptocurrency transactions typically do not possess the information needed to complete certain IRS forms, but will have reporting responsibilities under the proposed language. Industry leaders claim that crypto traders who wish to remain anonymous and cryptocurrency exchanges that do not want to bear these burdens may simply move offshore.

Several Senators shared the concern and pushed for amendments to limit the scope of “broker” prior to the Senate vote. Several versions of amendments that exclude different groups of crypto participants (validators, hardware or software sellers) were initiated but none was included due to procedural rules. The Senate passed the bill on August 10, and the House of Representatives will vote on the measure in the coming months.

Other Senators do not think the current wording will be as harmful as the industry expects. They believe that when the U.S. Treasury writes the regulations to implement the law, it will consider legislators’ intent and refrain from overreaching. Treasury concurred and clarified that it does not plan to go after non-broker entities that do not have transactional information.

Conclusion

Cryptocurrency tax issues were once a niche subject. However, with an estimated $2 trillion market size, it has become a popular topic and too big to avoid regulatory oversight. Some practitioners worry that a series of additional tax reporting and regulatory requirements will push the industry over the tipping point, which may deter potential investors from participating and limit the industry’s growth. Others view these as positive developments because clear rules provide legitimacy to the industry, which is critical given the industry’s unfavorable reputation in its early years. These regulatory measures may instead help to attract investors.

Cryptocurrencies, like other disruptive technologies, have evolved rapidly and will continue to evolve. It is critical for regulators, including the Treasury, to maintain open dialogues with the cryptocurrency industry to ensure a balanced regulatory environment — one that is rigorous enough to sustain an equitable tax system, but not so overly burdensome that it stifles innovation. Current developments are early steps toward establishing a solid regulatory environment. Additional issues such as the coordination of reporting rules with Foreign Account Tax Compliance Act (FATCA) and the clarification of wash sale rules for cryptocurrency may be the next agenda items.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.