Backdrop

Since January, the daily price of WTI has peaked at $63.27/barrel and troughed at $14.10/barrel. In fact, WTI was at $46.78 on March 2, finishing the month at $20.51 on March 31, representing a decline of just over 56% in a month. The precipitous decline was triggered by a combination of factors; namely, the dramatic economic collapse induced by the COVID-19 pandemic and the Saudi-Russia price war.

The COVID-19 pandemic has had a devastating effect on oil consumption. The International Energy Agency and other observers have estimated that an unprecedented 20 million b/d or more of global consumption could be temporarily lost, due to dramatic reductions of transportation and other sources of oil use. To be clear, the impact of COVID-19 on consumption began to manifest prior to March, as could be seen as price declined from $63.27 on January 6 to $44.28 by February 28, representing just over a 29% decline in the first two months of 2020. Much of this was evident in the demand drop in China, with a large fraction of the decline in price occurring after the lockdown in Wuhan on January 23.

Matters were exacerbated significantly heading into March. To begin, COVID-19 spread outside of China, and began to take a significant toll on demand in Europe, the US and elsewhere as economies moved into a self-induced coma in effort to slow the spread of the disease. Compounding the issue, at the OPEC+ meeting in early March, where it was largely believed that a production cut would be agreed, Saudi Arabia and Russia failed to reach an agreement on production restraint, which resulted in a price war. The rationale for the decision has been the subject of intense analysis and debate, but the end result has been a sizeable contribution of additional output (roughly 3 million b/d) to an already massively oversupplied market.

It is useful to disentangle the drivers of the collapse in price to understand how the market, and price, will adjust. Without doubt, the massive oversupply to the market is threatening the ability of storage capacity to absorb the excess production.1 If global storage capacity is exhausted, there will be continued downward pressure on price, and economic pressures will ultimately drive the shut-in of higher cost production. Of course, there are regional constraints that will exert pressures on local prices and production as well. These constraints will emerge on a case-by-case basis, affecting local pricing and hence the commercial viability of continued production. Regardless, markets reveal this through pricing signals, which must remain unimpeded if efficient short run operating and long run investment decisions are desired.

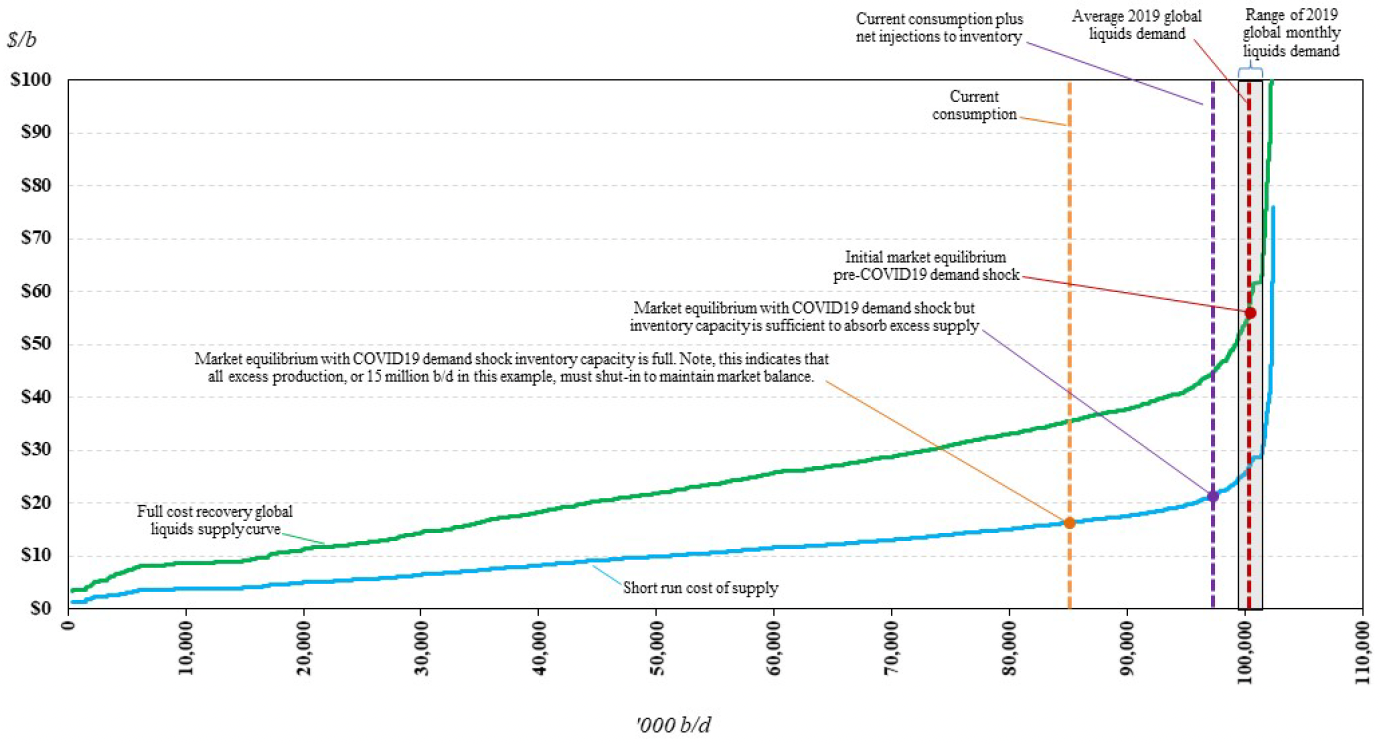

The global liquids supply curve depicted in Figure 1 illustrates the depth and severity of the COVID-19 demand shock. Before the COVID-19 virus struck, the global liquids supply curve indicated full cost recovery market equilibrium in the range of $50-$65/b, depending on the level of consumption, which fluctuated monthly around the annual average (as indicated) throughout the year. If Saudi Arabia and Russia boost output as promised (an additional 3 to 3.5 million b/d, that supply would reflect levels in line with a competitive, inframarginal producer. From Figure 1, we can infer that – if sustained – such an increase in supply from low cost producers would drive a new long run market equilibrium in the $40-$45/b window, although prices would almost certainly dip lower in the short term as higher cost supply is chased out.

Figure 1 — Global Liquids Market Equilibrium in the Presence of an Extreme Demand Shock

But that’s not the whole story. The dramatic, unexpected collapse in oil consumption has placed the market in a very different short run situation. The extreme oversupply to the market is, in fact, largely a demand story. As the chart shows, this will drive price down to a point that still indicates market clearing, but under very different circumstances. Specifically, the demand level at which the market clears reflects consumption plus net injections to inventories. In a “normal” year, net injections roughly balance to meet seasonal demand fluctuations. Today, however, with so much surplus oil being produced, it’s going into inventories. If storage fills, prices will fall even more to shut in higher cost production.

Of course, there are regional constraints that will exert pressures on local prices and production, but Figure 1 is meant to reference the global benchmark equilibrium rather than regional prices. But, even in the case of regional market clearing, equilibrium will reflect short-run production costs and the ability of local storage and take-away capacity to soak up excess supply. Lack of ability to move crude oil either into regional storage or to the broader market will drive local prices down until production is shut-in so that the market balances.

The overall magnitude of production that shuts in will depend on how far consumption falls relative to contemporaneous production and how rapidly storage fills. Regardless, the combined effects of these simultaneous stresses—COVID-19 demand destruction and increased output from Saudi Arabia and Russia—places immense pressure on storage capacity and the global oil market.

What is the Remedy?

American oil and gas companies and their employees have been hit hard. The federal government and oil-producing state governments are struggling to find a policy response. The pain to companies, workers, and families is significant and very real. However, it is important for the long run health of the industry and the country that first principles not be abandoned. The system of free enterprise that is a hallmark of the United States is based on open markets and honest competition. The system is what drove the shale revolution2 and made the US the envy of the world. It is what put the US in the position of being the world’s largest oil and gas producer. It wasn’t a national champion that did that; it was independent companies, working determinedly for a competitive advantage. It would be profoundly short-sighted and ultimately counterproductive to abandon that system by colluding with OPEC or propping up the US oil sector with tariff intervention or other government interdiction. Similarly, pro-rationing would run counter to competitive market economics by impacting efficient operators along with less competitive players.

To be clear, there are times in which policy intervention will raise market efficiency, but those periods typically coincide with the realization of a market failure, or when there is a non-priced externality associated with the activities of market participants. An oversupply condition is not such a case. Rather, the condition results in market signals that culminate in a price collapse; hence the market actually provides the signal that begets a reallocation of resources toward an efficient outcome. In other words, lower prices will disadvantage higher cost producers and drive a reduction in output, even without any policy intervention. So, while especially painful in the short run for producers at the margin, market forces will drive an outcome that is most efficient, leaving the participants in a position to respond rapidly when the market turns.

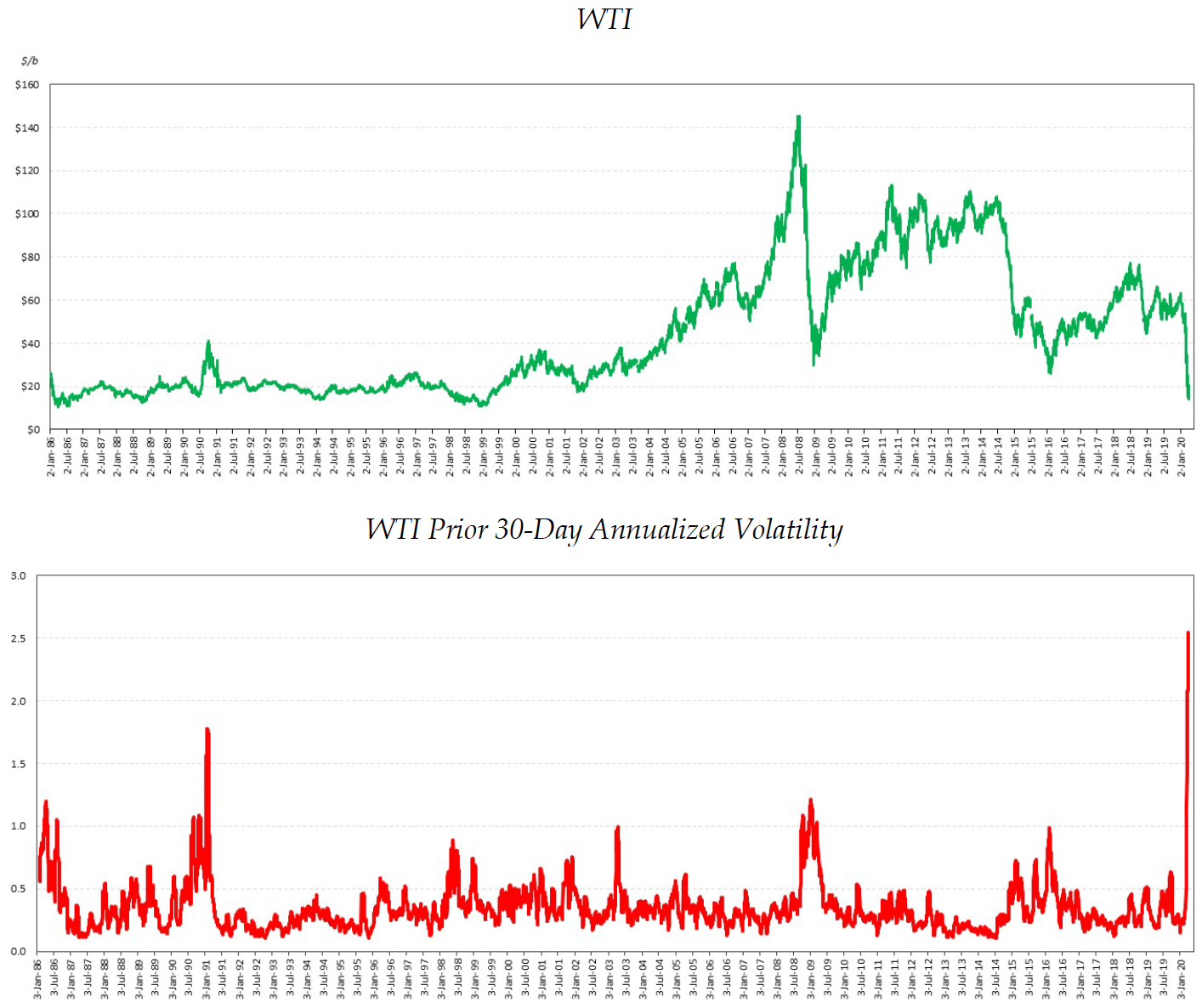

In the US system, investors take risks in the hope of earning a profit. As such, owners of companies have an opportunity to succeed, but also the opportunity to fail. The decision to enter the market through investment is determined by price and cost, with variation in each dictating the risk-reward calculus. Risk and reward are two sides of the same coin. Figure 2 indicates the daily price of oil (WTI) from January 2, 1986 through April 1, 2020 along with a measure of volatility calculated as the standard deviation of the log returns of price over the previous 30 days multiplied by the square root of 252 (the number of trading days in a year). As can be seen, the price of crude oil is anything but stable, with several episodes of extremely high volatility that coincide with periods of heightened oil market and/or economic instability (such as the collapse of oil price in 1985/86, the events surrounding the Iraqi invasion of Kuwait in 1990/91, the Global Financial Crisis of 2008/09, and the collapse of oil price in late 2014 through 2016 when OPEC did not come to agreement on quotas, to name a few). However, this does not indicate a failure of competition; rather, it indicates precisely the opposite.

Figure 2 — Oil Price and Annualized Oil Price Volatility (Daily, 1/2/1986 - 4/1/2020)

Many factors influence price signals to the global market, which is significantly larger now than it was in 1986 and 2003. Global petroleum and other liquids consumption has risen from 61.5 million b/d in 1986 to 79.6 million b/d in 2003 to 100.6 million b/d in 2020. The scale of the increase in demand has required new sources of supply to enter the market, periodically stressing traditional suppliers. In turn, this has created opportunities for new entrants, especially over the last decade, which producers in the US have captured with spectacular success. The competitive nature of the US oil and gas upstream has facilitated the ability to rapidly capture profit opportunities when they presented themselves, something US policy was keen to address when the long-standing crude oil export ban was lifted in December 2015.

In general, competition reveals winners and losers, and it is effective at driving, and rewarding, efficiency and innovation. The rise of US crude oil and natural gas production over the past decade is emblematic of the US system. Of course, there are also risks, and the reality of the global market is that the conventional resources in Saudi Arabia and Russia are cheaper to produce.

Hence, seeking government support to mitigate risks, regardless of how large the black swan event that precipitates, risks setting a precedent that invites future interventions that may cut the other way or adversely impact the future investment climate. Of course, it is central to the US oil and gas industry that we not tolerate anti-competitive behavior at home or abroad any more than we do for other industries. But there are already well-established processes for bringing and judging such cases.

This begs the question, are there cases when other factors should be considered? Of course. Like the hollowing out of US manufacturing capacity a generation ago, the potential damage to the domestic oil and gas industry has economic, strategic, environmental and military implications. All of those are fair game for policymakers to consider. For example, environmental policy may seek to limit greenhouse gas emissions as well as waste by regulating the excessive flaring of natural gas co-produced with oil. In turn, this could effectively limit oil production by forcing producers to either develop gathering and take-away capacity, which raises cost and could be economically prohibitive, or simply not produce those barrels at all.

But other considerations must clearly outweigh the broader benefits of a competitive system before any government intervention is considered. How would the US look differently today if the horse-drawn carriage industry had asked for government protection from Henry Ford’s Model T, with better performance, cost, and environmental impacts, and succeeded? There’s plenty of experience from our own industry—for example, how coal benefitted in the 1970s and 1980s when the government restricted the use of natural gas in the power sector.

In a changing competitive environment, which the recent events affecting the global oil market clearly represent, a greater focus on ensuring and maintaining fair and open competition is critical to the long-term health of the market. Some companies will succeed while others fail, but overall, firms and investors will adapt to new realities; they – and all of us – will be better off as cost efficiency and capital discipline will be rewarded. Indeed, the ability to fail is one of the secret weapons of our system. The geologic conditions that are requisite for production do not disappear if a producer fails; when the market picks up, surviving companies and/or new entrants can produce those resources when price warrants it.

But with failure, we need heart. There are lots of things government and companies can do to help the workers manage in these difficult times. Making sure that affected workers have access to a social safety net isn’t socialism; it’s how we make sure the benefits of capitalism work for all of us. And getting the economy back up and running should be the focus of policy remedies – especially since this is a demand-driven crisis. It is critical to us all, and is germane to the success of the oil and gas industry.

Endnotes

1. See, for example, https://www.reuters.com/article/us-oil-prices-kemp-column/column-global-oil-storage-to-fill-rapidly-as-consumption-plunges-kemp-idUSKBN21E2BR.

2. See https://www.bakerinstitute.org/media/files/files/94020ec4/CES-Pub-EnergySecurity-060214.pdf.