Author(s)

Introduction

As the world pivots toward a new normal in the wake of the COVID-19 pandemic, a strong sense of macroeconomic uncertainty remains. In 2022, a surge in post-pandemic inflation prompted an aggressive monetary contraction by the Federal Reserve. The corresponding rise in the cost of capital, combined with diminishing fiscal stimulus and supply-side constraints, is expected to slow economic growth. How rapidly the economy decelerates could result in either a slow convergence back to trend growth — a so-called “soft landing” — or, in the case of a rapid economic deceleration, a recession.

This issue brief gauges the likelihood of an impending recession by broadly examining both the frequency and nature of recessions throughout U.S. history. Several of the historical events that triggered major recessions exposed the sensitivity of the U.S. economy to certain types of shocks, soliciting policy responses and changes to the regulatory environment that helped insulate the economy against future shocks. This brief discusses these policy responses, posing them as a possible explanation for observed business cycle patterns over time, and evaluates the current state of the economy in light of these insights.

The Cadence of Recessions

Economists and professional forecasters search extensively for leading indicators of recessions. Some research has pointed to certain macroeconomic and financial variables like the unemployment rate, the Treasury yield curve and credit spreads that change course in the months and weeks preceding the start of a recession.[1] In addition to these indicators, historical patterns in the durations of economic expansions — the time elapsed between the end of one recession and the start of the next — suggest that time itself may be a reasonable predictor of recessions.

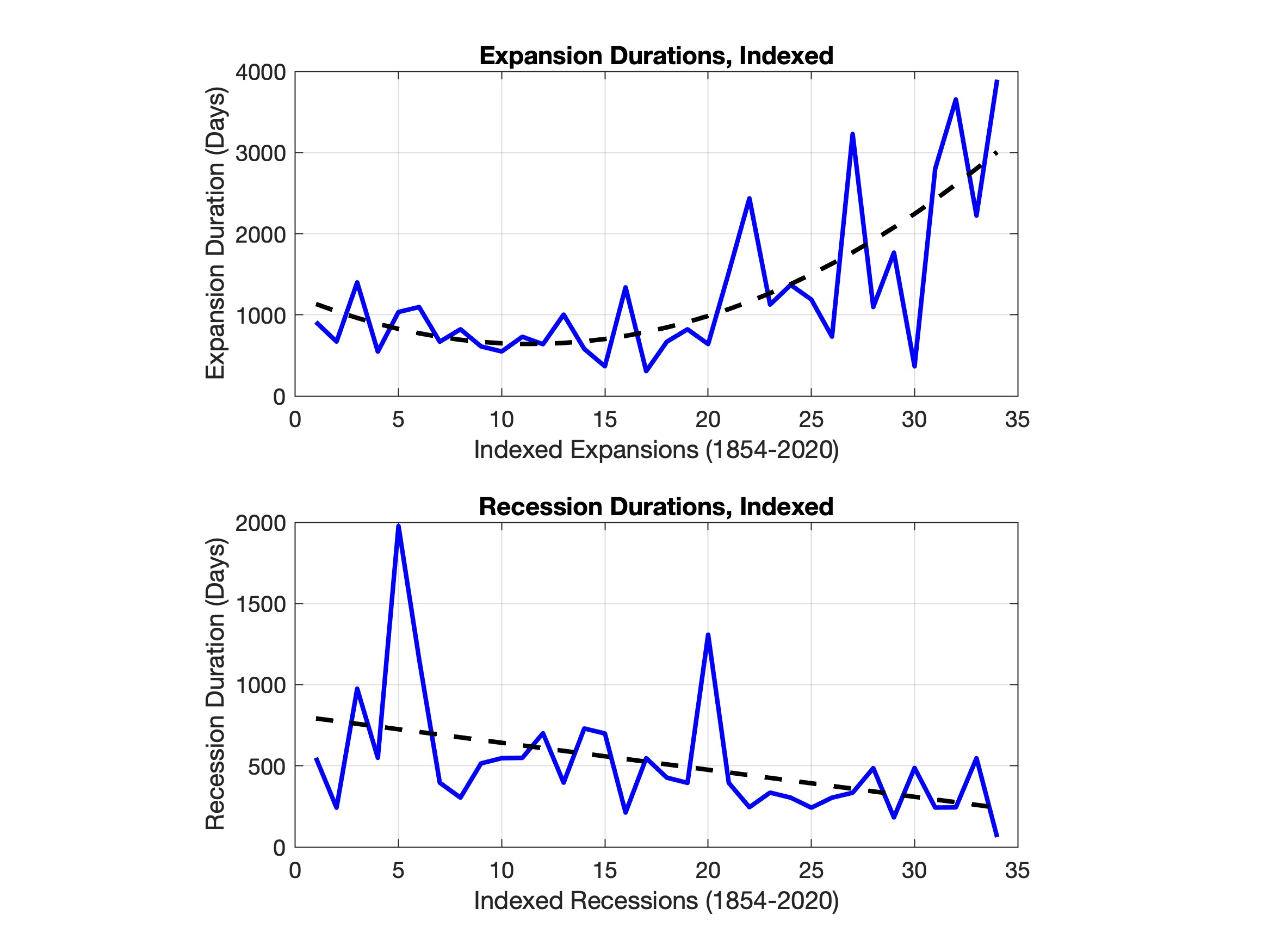

The National Bureau of Economic Research — the arbiter of U.S. recession identification — has observed 35 recessions since 1854.[2] Recessions have happened for several reasons, including financial market crises, macroeconomic imbalances and other shocks like the COVID-19 pandemic.[3] If we study the history of business cycles, we generally find that expansions have gotten longer or, equivalently, that recessions have become more infrequent. In Figure 1, the top graph orders the duration of every expansion on record, with the expansion beginning in 1855 indexed at 1 and the expansion beginning 2009 indexed at 34. The bottom graph shows the same metric for recession durations. Together, the graphs indicate a pattern of increasing expansion durations and declining recession durations over time. If the trending increase in expansion durations were to continue, the expansion starting in May 2020 would be expected to last nearly nine years. Although this trend has become somewhat more volatile over time, it is at least cause for doubt that a near-term recession three years into an expansion is a foregone conclusion.

Figure 1 — Indexed Expansion Durations (a) and Recession Durations (b)

Note R-squared for (a) is 0.545 and for (b) is 0.174.

Over time, recession durations have also gotten shorter. Although this relationship is generally weak, each recession has lasted on average approximately 17 days fewer than the previous recession. In other words, this suggests that the economy generally tends to recover faster over time. The combination of longer expansions and shorter recessions indicates a general improvement in the resiliency of the economy against adverse economic impacts.

The Role of Policy

To a large extent, the reduced frequency and duration of recessions highlights the success of past policies that were designed to mitigate or even prevent certain types of macroeconomic shocks. Several features of the U.S. financial system’s regulatory and institutional framework, for example, were designed in response to financial crises. The bank runs that plagued the financial system in the late 19th century and the early 20th century led to the establishment of the Federal Reserve in 1913 and the Federal Deposit Insurance Corporation (FDIC) in 1933. These institutions served the financial system well until the financial crisis of 2008 exposed further weaknesses in the underlying regulatory environment. The Dodd-Frank Wall Street Reform and Consumer Protection Act imposed restrictions meant to contain financial institutions’ exposure to aggregate risk and limit speculative activity, making the broader economy more impervious to financial crises.[4]

In the early 1970s, extreme volatility in oil prices created an energy crisis and a corresponding macroeconomic downturn. In response, the U.S. government commissioned the Strategic Petroleum Reserve (SPR) to dampen energy price volatility and supply disruptions.[5] This measure helped to insulate the U.S. economy from energy price shocks that could lead to recessions. Since the establishment of the SPR, the U.S. has periodically stabilized domestic energy prices, most recently in response to the energy crisis triggered by the Russia-Ukraine war.[6]

COVID-19 highlighted the exposure that the U.S. economy faced regarding pandemic risk. Although this pandemic itself may have been unexpected, a historical account of the 1918 Spanish flu pandemic provides a quantitative precedent for its macroeconomic consequences. Estimates of the 1918 pandemic suggest an average cross-country decline in GDP of around 6%,[7] while the COVID-19 pandemic led to a contraction in the U.S. of around 2% to 3% GDP on an annual basis in 2020.[8] The brevity of the recession in 2020 is due in large part to the fiscal and monetary response, as well as advances in technology that dampened the disruptions to various economic activities. The rapid development of the COVID-19 vaccine and other treatments also played a major role in reducing the macroeconomic consequences of the pandemic. The vaccine’s development started in early 2020, and its delivery began in December of the same year — far exceeding the previous development record of four years.[9] Although the vaccine was developed by private sector institutions, policy and fiscal support created preparedness before the pandemic and ensured an expedited delivery thereafter.[10] Such rapid development, combined with continued research support, indicates that advancements in medicine and technology could dampen future macroeconomic risk resulting from pandemics.

Studying historical monetary policy-tightening cycles, in which the Federal Reserve increases the federal funds target rate, could also provide insights into the likelihood of an impending recession. The literature is somewhat mixed on the probability of recessions following tightening cycles. In particular, there is historical evidence of both a recession happening and not happening following a tightening cycle, although instances of the former exceed the latter.[11] Moreover, it is unclear whether the historical recessions resulted from natural disruptions or from the adverse economic effects of contractionary monetary policy. For example, did the tightening cycle that ended in December 2018 cause the recession of 2020? A monetary contraction could have plausibly made the economy more susceptible to a recession, but it certainly did not cause the COVID-19 pandemic.

Emergent Macroeconomic Risk

Financial Market Risk

While policy responses can mitigate macroeconomic risk corresponding to past events, an ever-changing world will always introduce new risks. For example, recent growth in cryptocurrencies may pose an emerging threat to the stability of the financial system. A significant devaluation of cryptocurrencies in late 2022 and instability in crypto exchanges had a lesser impact on broader financial markets than they may have had otherwise because of their limited interconnection with the traditional financial system.[12] However, growth of the digital asset ecosystem under the current regulatory environment could eventually contribute to broader financial instability, as these assets generally circumvent the very types of regulations that promote financial stability.

In the months after the start of the COVID-19 pandemic, a combination of factors, including monetary and fiscal stimulus and a surge in household savings, contributed to a sharp decline in various types of consumer and business loan delinquency rates. Historically, delinquency rates have risen during recessions and have often been a leading indicator of an impending recession. While the delinquency rate on all loans at commercial banks remains low — an optimistic indication of financial stability — delinquency rates on credit card loans have risen steadily from their post-pandemic lows.[13] Whether this indicates a reversion to the pre-pandemic trend or a deterioration of household finances leading to a recession remains uncertain. Some increase in credit card delinquencies, however, could reasonably be expected as a natural consequence of rising interest rates and heightened inflation.

Another recurring risk corresponds to the U.S. government’s method of financing expenditures. The legal limit on federal debt accumulation, commonly known as the debt ceiling, prevents the federal government from servicing expenditures by increasing its outstanding debt. Without raising the debt ceiling to finance ongoing expenditures, the government begins cycling through increasingly severe levels of fiscal austerity. In the extreme case, if the government was unable to service its existing debt obligations, it would be in default. Moreover, failure by the government to sustain existing transfer payments and programs, like Social Security, would disrupt households’ finances, likely exacerbating any financial and macroeconomic distress. Without a historical precedent for this level of default, it is difficult to gauge the extent of the risk, but some findings highlight the risk it presents for a recession.[14] Moreover, the rising possibility of default drives up the credit premium on federal debt and could adversely impact Treasury-based collateral in private debt markets.[15] Federal policymakers can fully mitigate this risk by resolving budgetary disputes through alternative means.

Restructuring Risk

Recessions often bring with them a wave of destruction to specific industries and professions. If this type of destruction leads to a subsequent efficiency improvement through resource reallocation to new and growing industries, it is considered a form of “creative destruction.”[16] These transitions could be the result of changes in consumer preferences or technological advancements that render certain professions and industries obsolete. Employment trends during recessions reveal patterns of disruption that may indicate whether the economy is at risk of another wave of destruction.

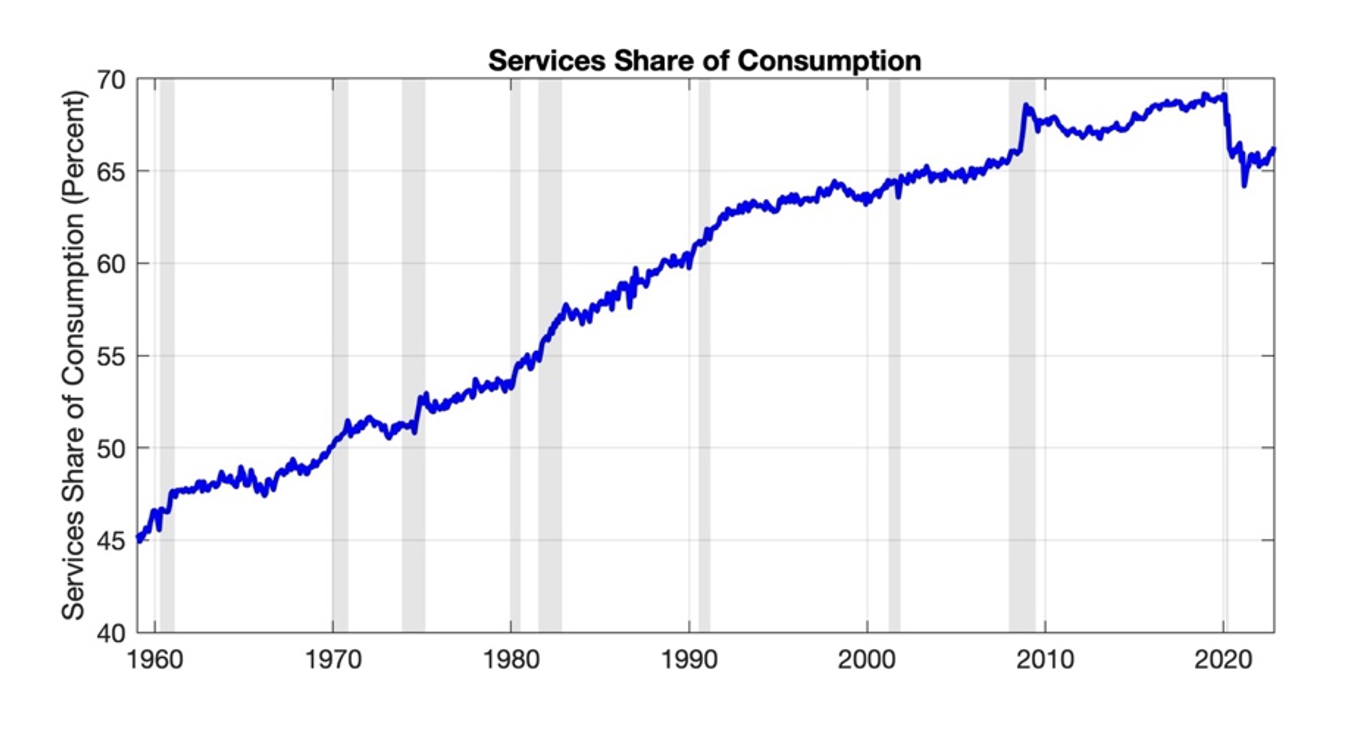

Figure 2 — Services Share of Total Consumption

Note Goods share of consumption equals 100 minus the graphed values.

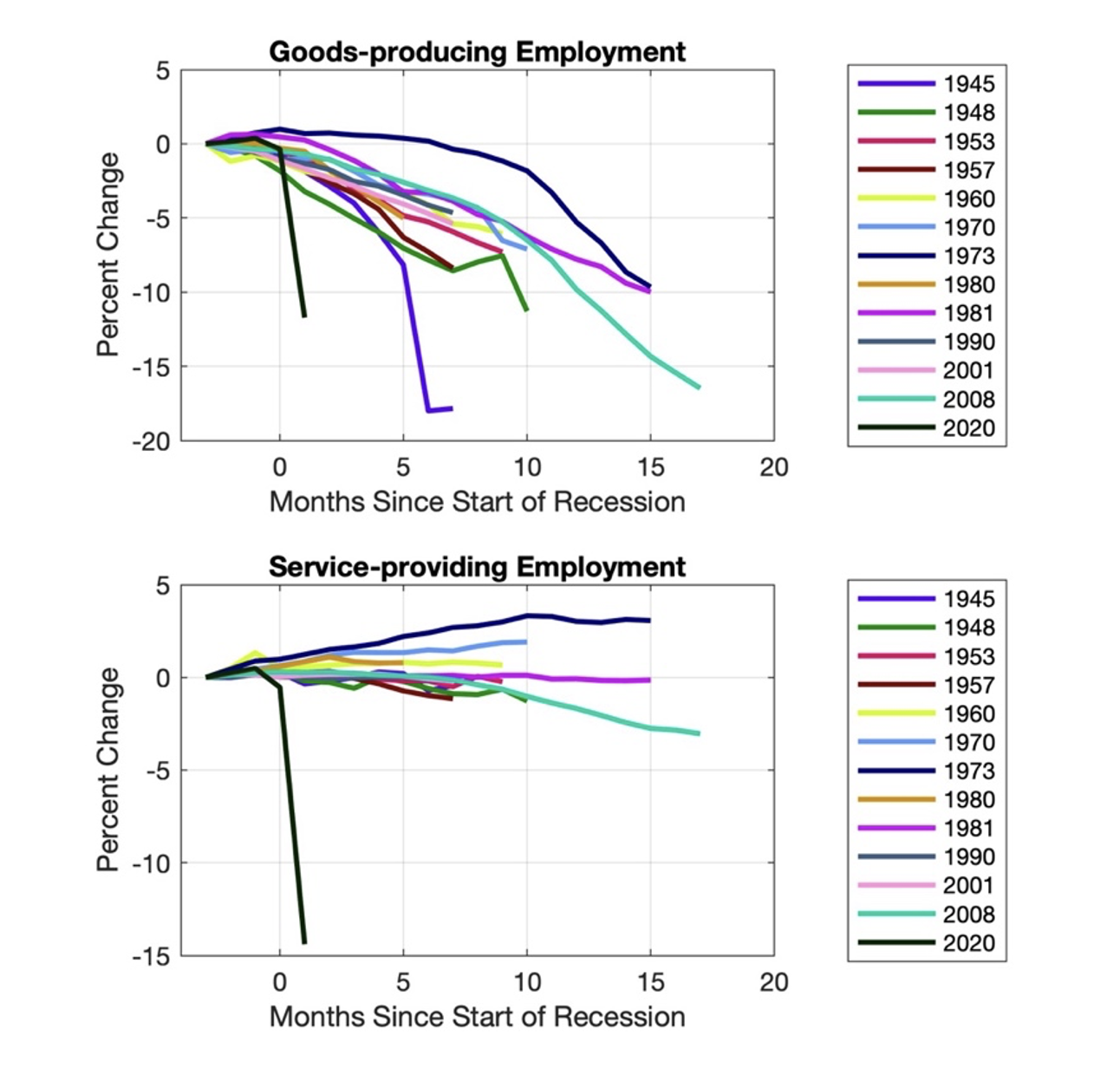

Figure 3 — Employment Trends Following Past Recessions

Note Values are indexed to three months before the start of each recession.

For several decades, shares of consumer demand steadily shifted from goods toward services, as shown in Figure 2. This trend generally accelerated during nearly every recession before the 2020 recession induced by the pandemic. Goods-producing employment fell in nearly every recession, while service-providing employment usually remained stable or even grew, as shown in Figure 3. One exception was the financial crisis of 2008, which caused job losses in both goods-producing and service-providing employment, largely driven by the decline in the financial services sector. Despite this decline in service-providing employment, relative demand for services rose sharply during the 2008 recession and continued trending upward thereafter.

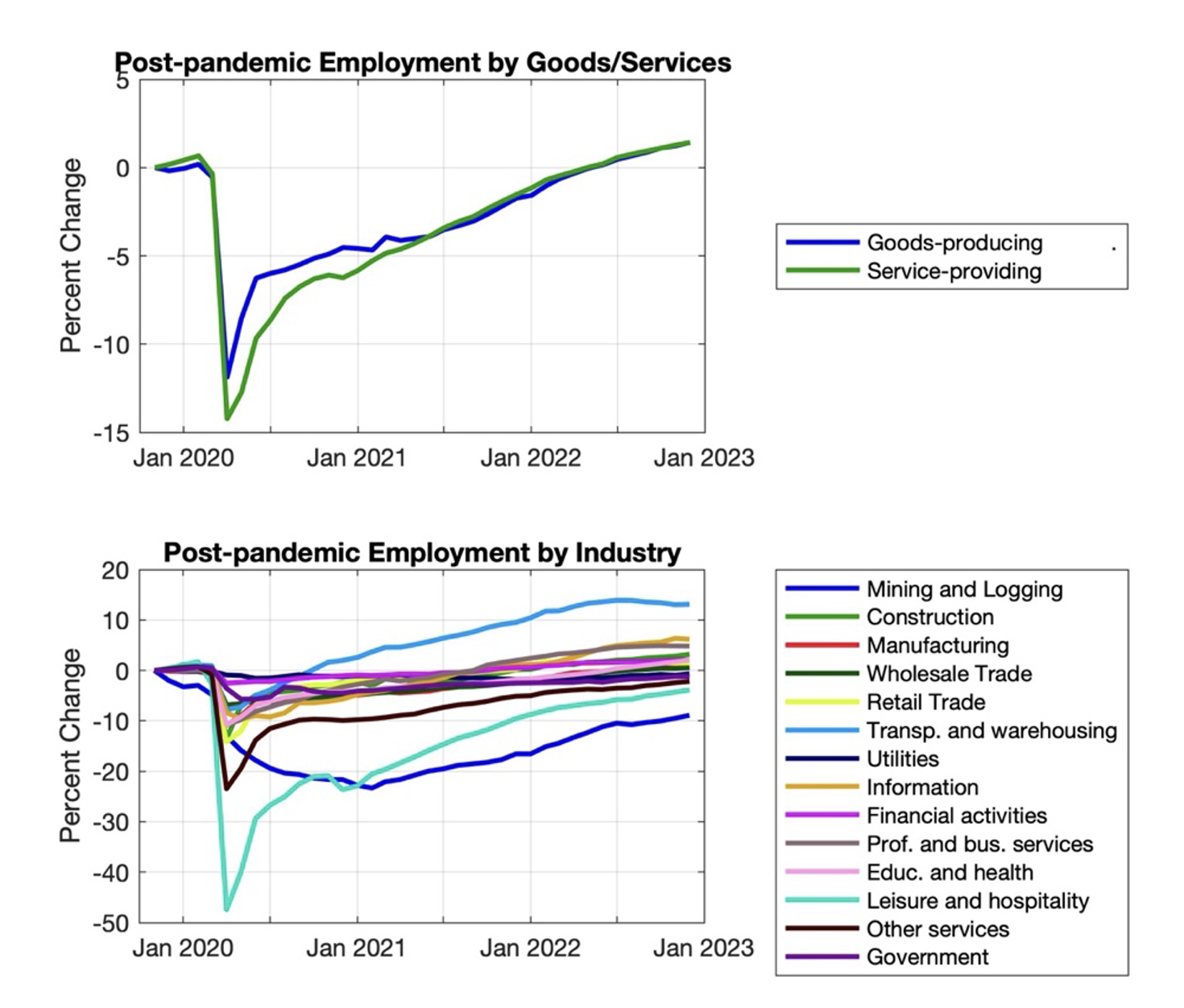

The recession of 2020 reversed this decades-long trend, as relative demand for services suddenly fell sharply and remained relatively low as a share of total consumption. Goods-producing and service-providing employment both fell during the recession, with the latter reasonably falling by a larger share. Despite the lasting change in consumption composition, however, total employment growth for each group has been nearly identical relative to pre-pandemic levels, as shown in Figure 4. As a result, service-providing employment is likely at higher risk for a restructuring wave, similar to those observed in the past. The recent surge in job losses across nearly every industry, however, creates room for doubt that a restructuring wave is eminent or likely. Moreover, further industrial granularization of employment changes since the post-pandemic recovery fails to clearly indicate significant disruptions.

Figure 4 — Employment Trends Following the 2020 Recession

Note Values are indexed to three months before the start of the recession.

Other Factors

As the aftermath of the COVID-19 pandemic began to reach an optimistic turning point in early 2022, global security regressed with the start of the Russia-Ukraine war. Global energy prices soared, sending several regional markets into crisis. The U.S. began withdrawing from the SPR to stabilize domestic prices, limiting the impact of the war on the broader economy. Although the resulting economic risk of supply disruptions in various markets seems contained as of early 2023, global security risk is likely to remain elevated until war tensions subside.[17] Even if the overall likelihood is low, an escalation of the war could have a severe impact on the global economy.

While some factors pose cyclical risks to the U.S. and global economies, others may pose longer-term risks. For example, research indicates that climate change may introduce weather-related risks to the U.S. economy, including instability in the financial sector.[18] In addition, a sharp decline in fertility rates following the pandemic will likely contribute to slowing long-term economic growth and increased financial risk in pay-as-you-go pension programs, such as Social Security, that rely on a stable or growing population.[19] Just as these risks to long-term macroeconomic stability may take several years or decades to materialize, mitigation efforts may also require prolonged periods of implementation and effectiveness.

Conclusion

The COVID-19 pandemic caused a deep and lasting disruption to the U.S. and global economies. Three years later, several macroeconomic values show a convergence to pre-pandemic trends. Based solely on the historical expansion duration trend, a near-term recession seems unlikely. Furthermore, the historical recession duration trend indicates that any recession would likely be short-lived. These observations likely reflect the success of mitigation policies that, over time, have insulated the U.S. economy from various types of shocks. Continued economic disruptions, however, indicate that more research is necessary to predict emergent threats to the economy and to find ways to mitigate their impact. Such efforts could continue the trend of longer periods of economic expansion and shorter, less severe recessions.

Endnotes

[1] Michael T. Kiley, Financial and Macroeconomic Indicators of Recession Risk (Washington, D.C.: Board of Governors of the Federal Reserve System, 2022), https://www.federalreserve.gov/econres/notes/feds-notes/financial-and-macroeconomic-indicators-of-recession-risk-20220621.html.

[2] “US Business Cycle Expansions and Contractions,” National Bureau of Economic Research, last updated July 17, 2021, https://www.nber.org/research/data/us-business-cycle-expansions-and-contractions.

[3] Mark Labonte, What Causes a Recession?, (Washington, D.C.: Congressional Research Service, 2019), https://crsreports.congress.gov/product/pdf/IN/IN10853.

[4] Baird Webel et al., The Dodd-Frank Wall Street Reform and Consumer Protection Act: Background and Summary, (Washington, D.C.: Congressional Research Service, 2017), https://crsreports.congress.gov/product/pdf/R/R41350/10.

[5] International Energy Agency, United States’ Legislation on Oil Security, July 31, 2020, https://www.iea.org/articles/united-states-legislation-on-oil-security.

[6] “History of SPR Releases,” Office of Petroleum Reserves, U.S. Office of Cybersecurity, Energy Security, and Energy Response, https://www.energy.gov/ceser/office-petroleum-reserves.

[7] Robert J. Barro, José F. Ursúa, and Joanna Weng, “The Coronavirus and the Great Influenza Pandemic:

Lessons from the ‘Spanish Flu’ for the Coronavirus’s Potential Effects on Mortality and Economic Activity,” NBER Working Paper Series 26866, National Bureau of Economic Research, Washington, D.C., April 2020, https://www.nber.org/system/files/working_papers/w26866/w26866.pdf.

[8] Bureau of Economic Analysis, “Gross Domestic Product for the U.S. Virgin Islands, 2020,” news release no. BEA 22—07, March 4, 2022, https://www.bea.gov/news/2022/gross-domestic-product-us-virgin-islands-2020.

[9] Phillip Ball, “The Lightning-fast Quest for COVID Vaccines — And What It Means for Other Diseases,” Nature, December 18, 2020, https://www.nature.com/articles/d41586-020-03626-1.

[10] Richard G. Frank, Leslie Dach, and Nicole Lurie, “It Was the Government That Produced COVID-19 Vaccine Success,” Health Affairs Blog, May 14, 2021, https://doi.org/10.1377/forefront.20210512.191448.

[11] Kevin L. Kliesen, “A Look at Fed Tightening Episodes Since the 1980s: Part I,” On the Economy (blog), Federal Reserve Bank of St. Louis, April 14, 2022, https://www.stlouisfed.org/on-the-economy/2022/apr/fed-tightening-episodes-since-1980s-part-one.

[12] Financial Stability Oversight Council, 2022 Annual Report, https://home.treasury.gov/system/files/261/FSOC2022AnnualReport.pdf.

[13] Mia Taylor, “Credit Card Delinquencies Are Expected to Spike to Their Highest Level in a Decade—But Americans Are Opening More Credit Cards Than Ever,” Fortune Recommends, December 14, 2022, https://fortune.com/recommends/article/consumer-credit-debt-forecast-2023/.

[14] Eric Engen, Glenn Follette, and Jean-Philippe Laforte, Possible Macroeconomic Effects of a Temporary Federal Debt Default (Washington, D.C.: Board of Governors of the Federal Reserve System, 2013), https://www.federalreserve.gov/monetarypolicy/files/FOMC20131004memo02.pdf.

[15] U.S. Government Accountability Office, Debt Limit: Market Response to Recent Impasses Underscores Need to Consider Alternative Approaches, GAO-15-476, July 9, 2015, https://www.gao.gov/products/gao-15-476.

[16] Muriel Dal Pont Legrand and Harald Hagemann, “Retrospectives: Do Productive Recessions Show the Recuperative Powers of Capitalism? Schumpeter’s Analysis of the Cleansing Effect,” Journal of Economic Perspectives 31, no. 1 (Winter 2017): 245–256, https://doi.org/10.1257/jep.31.1.245.

[17] Amy J. Nelson and Alexander Montgomery, “How Not to Estimate the Likelihood of Nuclear War,” Order from Chaos (blog), The Brookings Institution, October 19, 2022, https://www.brookings.edu/blog/order-from-chaos/2022/10/19/how-not-to-estimate-the-likelihood-of-nuclear-war/.

[18] Office of Financial Research, “Climate Change Risk,” in Annual Report to Congress 2021, https://www.financialresearch.gov/annual-reports/files/OFR-Annual-Report-2021.pdf#page=95.

[19] Barro, Jorge. 2021. The Macroeconomic Scars of the Pandemic. Issue brief no. 02.25.21. Rice University’s Baker Institute for Public Policy, Houston, Texas.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.