Author(s)

Introduction

In December 2022, the Australian government passed a law imposing a price cap on domestic natural gas for 12 months, with the possibility of the cap becoming permanent after that. Australia exports most of its natural gas, and extremely high international prices — triggered by the market turmoil in Europe over the last year — have caused its domestic prices to soar. Although the intention of the natural gas price cap is to provide relief to industrial gas users, this policy brief argues that the cap will reduce investment and production by natural gas producers — hurting not only the nation’s economy, but its citizens as well.

Australians expect to share in their country’s resource wealth, but price caps are not a good way to achieve this. Forcing companies to sell on the domestic market at a lower price reduces the value of Australia’s gas resources — an opportunity cost that ultimately does more harm than good. Instead, it would be better to maximize the value of the resource and then choose a tax policy that does not affect investment.

Price Cap Might Become Permanent

The price of natural gas sold in Australia has been capped at AU$12 per gigajoule (GJ) for 2023. At current exchange rates, that is equivalent to US$7.90 per million British thermal units (MMBtu),[1] which is much lower than the Asian price of around US$30 per MMBtu late last year.[2] The domestic price cap has a relatively narrow scope — it applies to gas supplied by producers in eastern Australia during 2023, under agreements signed after Dec. 23, 2022.

More importantly, the government has proposed permanent price controls in the form of a “reasonable pricing provision.” The aim is for domestic gas prices to match production costs, where costs include exploration expenses and a return to capital.[3] So far, we know that the government currently considers AU$12 per GJ to be a reasonable price.

To ensure that producers do not avoid the price cap by simply re-directing gas to the export market, producers would be required to make offers broadly available to the domestic market. The timing for issuing expressions of interest would be regulated, and binding arbitration would be available to parties that cannot form an agreement. However, the government cannot force producers to explore for — or produce — more gas.

How Did We Get Here?

Let’s take a quick overview of recent market history. During 2015 and 2016, three liquefied natural gas (LNG) export terminals started operation on the east coast of Australia. Since then, domestic gas prices have risen, together with Australia’s collective eyebrows. Real gas prices averaged AU$4.21 per GJ between 2010 and 2015 and then doubled to AU$8.55 per GJ between 2016 and 2021.[4]

The LNG projects produce large amounts of gas in Queensland, some of which is sold on the domestic market. The LNG projects have substantial bargaining power because they have an outside option to export at the Asian price. As such, they offer prices to the domestic market that are linked to the Japan Korea Marker (JKM).

Large industrial gas users have struggled to cope with the higher gas prices, with several closing down. Following the turmoil in Europe, contract prices as high as AU$30 per GJ have been offered for domestic supply in 2023.

The influence of the export price in the domestic market has increased over time as gas supply in southern states has declined. State governments in New South Wales, Victoria and South Australia share responsibility for this, with bans on new developments contributing to the decline in gas production. If produced, southern gas could be sold at a discount to the LNG export price, because southern gas would be further from the export plants and closer to demand centers. Indeed, if gas supply was large enough that LNG export plants were at capacity, the domestic price would again de-couple from the export price.

Price Caps Discourage Investment

Some have argued that the LNG industry never expected prices to be as high as current levels, so imposing price caps would not affect investment incentives. I disagree.

Although a war in Europe was unexpected, high LNG price events are not. Global LNG supply is inherently inflexible, because increasing liquefaction capacity is costly and slow, and the market remains illiquid, particularly in Asia.[5] Investors know that small increases in demand can create large increases in price. (The converse is also true, small declines in demand create large price falls.)

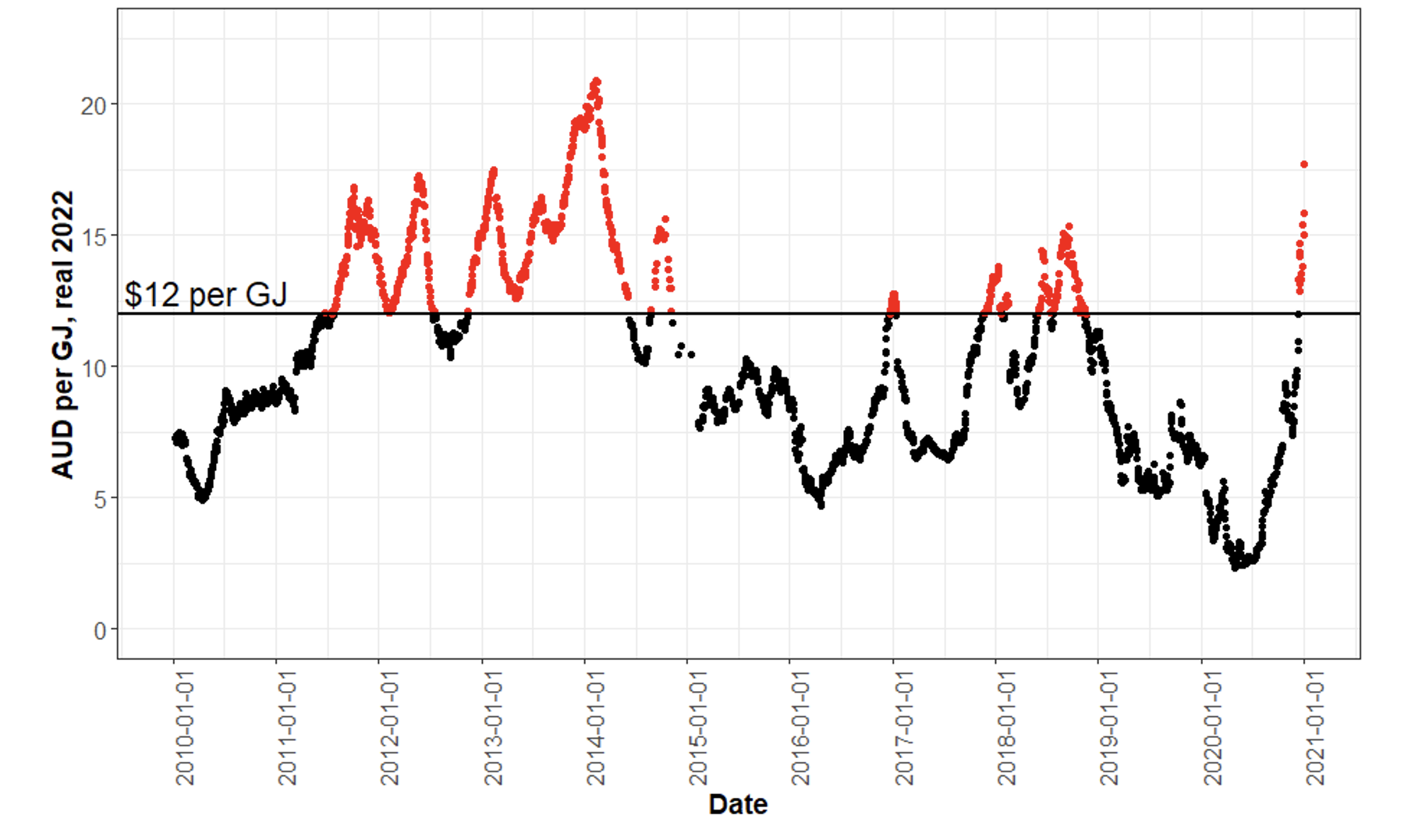

Figure 1 shows the Australian netback price, before the turmoil in Europe. This is the Australian domestic gas price that is equivalent to the prevailing export price (calculated as the spot JKM price, converted to Australian dollars and units, subtracting liquefaction and shipping costs).[6] During the time that the Queensland LNG projects made their investment decisions, the LNG price was well above $12 per GJ for a sustained period. That high price event was a result of the tsunami that hit Fukushima in 2011.

Figure 1 — JKM: Australian Netback Price

Investors in eastern Australia surely recognized the potential for high LNG prices, certainly above $12 per GJ. They deliberately left some room to participate in the spot market, rather than selling their full capacity to Asian buyers under long-term contracts. That is, the decision to invest in Queensland gas fields was made on the basis that large volumes would be sold under long-term contracts to Asian buyers, with some upside opportunity from the spot market.

If the Australian government limits LNG profits in the good times but does not help producers during the bad times, companies are left with all of the downside risks and reduced upside risks. They will be less willing to invest in natural gas exploration and development, reducing longer-term production levels.

In the short to medium term, LNG projects can respond to reduced profitability by producing less from their existing fields. The government argues that the price cap covers the life-cycle costs of gas and would not affect production. However, within any field, there are always wells that have low productivity and would only be drilled at high prices. The lower the price cap, the fewer of these wells that would be drilled.

Production is flexible enough to respond in the short term. Indeed, production volumes in Australia already respond to seasonal fluctuations in demand. However, in Queensland, gas is produced from coal seams, which require more frequent investment in drilling activities, and will therefore be more responsive to prices.

This means that a price cap will almost certainly lower production.

Price Caps Reduce Australia’s Resource Wealth

Most importantly, Australia now has the option to export gas at prices much higher than AU$12 per GJ. By forcing gas companies to sell to the domestic market at lower prices, the gas industry foregoes revenue. However, the value that domestic users get out of the gas is currently not high enough to make up for this loss borne by the LNG producers. We know that the value of gas to domestic users is currently less than the export price, because otherwise they would be willing to pay the export price.

Fundamentally, this policy will reduce the value of Australia’s natural gas, because it is not sold to the users that value it highest. This loss is on top of the loss from reduced exploration, development, and production.

A Better Option: Sharing Resource Profits & Losses

Policymakers wish to ensure that the domestic wholesale gas market “delivers for Australians.” Australians own the country’s natural resources (through their governments), and as such are entitled to benefit from their extraction.

To maximize their benefits from natural gas, Australians should first seek to maximize the resource’s value, by exporting it. Then, they can share in this value using a tax similar to the existing Petroleum Resource Rent Tax (PRRT).

The PRRT currently applies to offshore oil and gas projects, and it attempts to replicate a situation where the Australian government is a silent shareholder in each resource company. Under a well-designed version of this tax, the government shares in resource profits when prices are high. Importantly, it also shares in the investment costs and any losses when prices are low. In theory, the tax does not change the risk profile of the project; it only reduces the company’s share of the project. As a result, investment incentives are not reduced. A project that is marginally profitable without the tax is still marginally profitable with it. It does not become unprofitable.

The current design of this tax is not perfect, as highlighted by the Callaghan Review in 2017. However, it is far better than the ad-hoc interventions in the market currently being considered.

To tax gas extracted by LNG exporters, the Rudd and Gillard governments extended the PRRT to onshore gas projects in 2012. However, significant grandfathering concessions were made, and at the time no revenue was expected to be earned from the LNG export projects. In 2019, onshore projects were exempted from the tax by the Morrison government.

Australian voters currently feel that they deserve a greater share of their resource wealth, particularly from the gas industry. This momentum should be channelled into designing a better longer-term mechanism for Australians to share in their resource wealth. It should not be wasted on counter-productive price caps.

Endnotes

[1] On Jan. 17, 2023, the exchange rate was 0.6973 and an MMBtu is 0.947817 of a GJ.

[2] Japan Korea Marker (JKM).

[3] This will be implemented via a mandatory code of conduct, which requires producers to offer their gas domestically at “reasonable” prices, and binding arbitration for pricing disputes.

[4] Spot prices in the Victorian “Declared Wholesale Gas Market,” adjusted to real terms (2022) using the producer price index.

[5] International Energy Agency, Gas Market Report (Q1-2022), 19.

[6] The netback method follows the ACCC, but extends it backward to include a longer history.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.