Author(s)

I. Introduction

On August 25, 2022, the Center for Energy Studies at Rice University’s Baker Institute for Public Policy and the King Abdullah Petroleum Studies and Research Center hosted a workshop at the Baker Institute in Houston, Texas. The workshop was held under Chatham House rules. Participants in the workshop included representatives from major integrated oil and gas companies, large independent oil and gas producers, the banking and financial service sector, the US Energy Information Administration, OPEC, energy consultants and academia. These experts convened to consider the future of US shale oil and gas production and discussed, among other topics, shale’s role in global oil markets and the impact of environmental concerns and investor sentiments on the industry’s future development.

In introductory remarks, the “three phases” of the US upstream renaissance, driven by shale oil and gas production, were described. In phase 1, significant expansion was fueled by a period of high oil prices from 2010 through 2014. This was followed by a contraction, when prices declined through 2016, and a subsequent rise in production from 2016 through 2019, as prices recovered (phase 2). The infamous collapse of prices in 2020, coinciding with the onset of the COVID-19 pandemic, was the start of phase 3. As global demand recovered in 2021, supply chains became stressed, and prices moved upward dramatically. Now, a lack of sufficient investment combined with global demand recovery, general inflation pressures, policy uncertainty and the war in Ukraine have created a very high commodity price environment. Given these factors, the future direction of phase 3 was a key focus of the day’s discussions. Is a new shale renaissance on the horizon, or will environmental and investor concerns temper production?

In the first session of the workshop, “Shale’s Part in Global Oil Markets,” the discussion focused on the large swings in oil prices over the last 20 years, the emergence of environmental, social and governance (ESG) priorities in investment flows, and uncertainties about the timeframe of energy transitions. Given recent commodity inflation and geopolitical turbulence that has pushed the topic of energy security back to the top of policy discourse, questions about the near-term future of energy markets and the role shale plays in defining the short-to-medium term energy market balance were discussed.

In the second session of the day, “Defining the Future of Shale,” the discussion shifted to focus on several key questions that will shape the medium-to-long-term future of shale. These included:

- Have the “sweet” spots in shale been exhausted?

- Will new approaches improve recovery and drive greater value?

- What are the constraints for growth?

- How does infrastructure development impact the opportunity for growth?

- How will environmental concerns — methane emissions, flaring, water use and disposal, seismicity, etc. — impact future development?

- How will access to capital evolve, and what role will investor sentiment play?

The deliberations of session 2 led directly to a more focused discussion in session 3, “Investor Sentiment, ESG and Shale.” Over the last few years, oil producers have generally recognized the importance of ESG considerations to investors, and many have begun to promote solutions that would sustain oil production while advancing emissions mitigation. Session 3 also addressed inadequate returns in the oil and gas sector over the last decade, and it was put forth that a decade-plus of inadequate returns have contributed to increased investor emphasis on ESG criteria for performance evaluation. More recently, energy security considerations and the provision of reliable and affordable energy services have begun to dominate energy-related discourse. As economies rebound from COVID-induced shutdowns and geopolitical stresses mount, energy commodity prices have increased. This has significantly improved the financial health of firms across the oil and gas sector, thereby attracting investors who seek high returns. But will this influx of interest drive another boom in production that could erode future returns? And, how does this align with ESG-conscious investors?

In what follows, we offer more a more detailed overview of each session, beginning with the overall context that was provided to open the workshop. The rest of the paper is organized according to key issues that participants raised, in no particular order, throughout the day’s deliberations.

II. Framing the Discussion

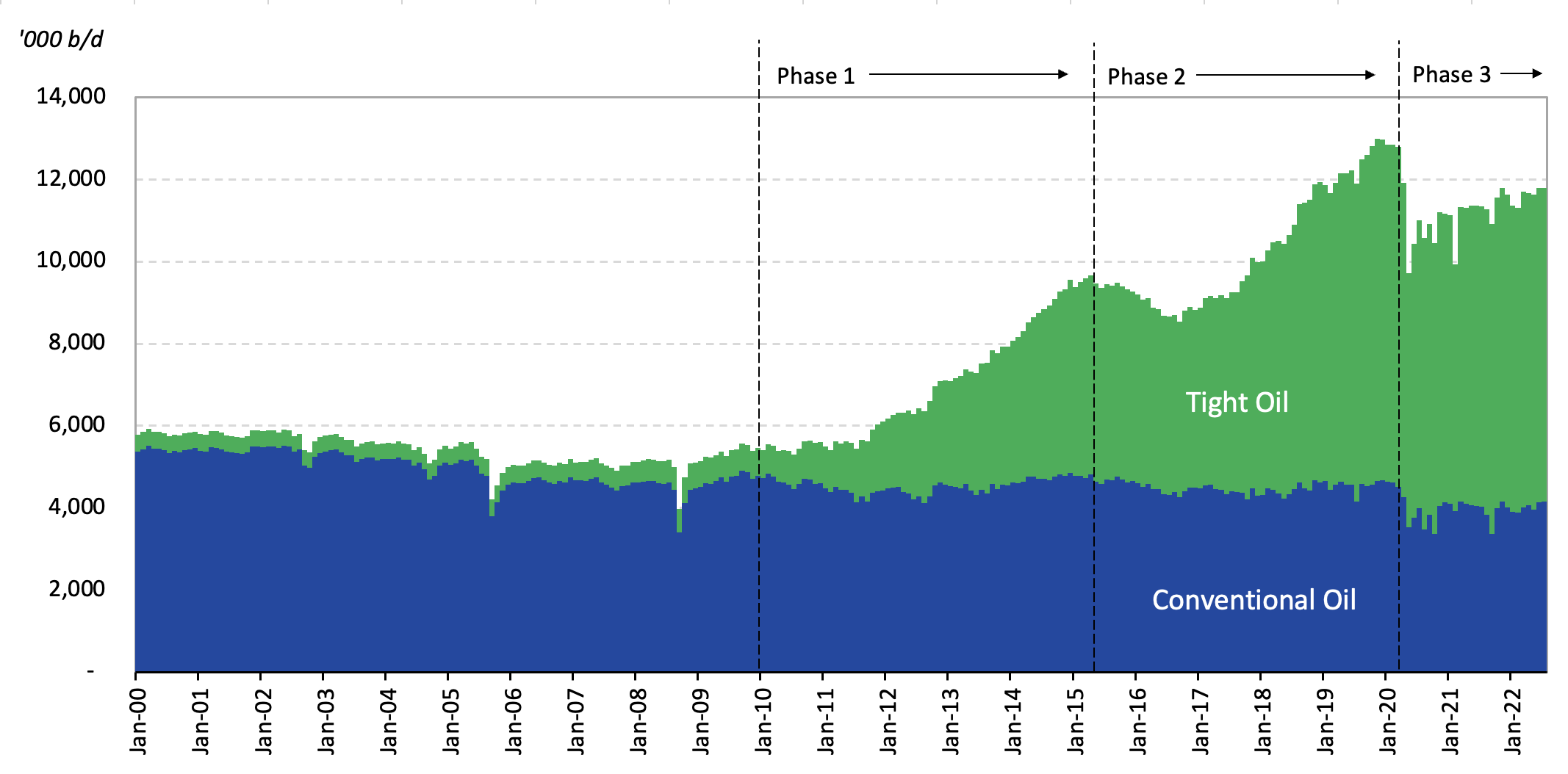

The shale revolution has been one of the most transformative events in global energy markets in the last two decades. Production of oil and gas from shales was once commercially infeasible, but innovation in hydraulic fracturing and horizontal drilling changed the upstream fortunes of US oil and gas producers. The US currently produces more than 11 million barrels per day (b/d), with shale (tight oil) accounting for over 7 million b/d — a remarkable feat given that fewer than 20 years ago, shale accounted for virtually nothing (see Figure 1). Moreover, the US has gone from being the world’s largest oil importer to being a significant exporter of crude oil and petroleum products. This dramatic shift of fortune was largely driven by technological advances that radically improved productivity. In fact, the shale revolution, along with a significant increase in demand in Asia, together represent the two most significant sources of transition in global energy markets over the last two decades.

In the 2000s, the US oil and gas industry enjoyed favorable market conditions earmarked by high oil prices, an abundance of available capital, access to resources on private lands and a robust supply chain for upstream oil and gas production. This, alongside technological innovations such as horizontal drilling and hydraulic fracturing, enabled the astounding production growth seen in the US over the last 15 years. In fact, the shale revolution drove the US to a point where it is now the largest oil-producing country in the world. The global landscape was changed even more when the US lifted its oil export ban in December 2015.

Despite the overwhelming shift of fortune in the US upstream, the shale renaissance has passed through different phases — both boom and bust. The first boom was fueled by innovation and rising oil prices from 2010 to early 2015, as domestic tight oil production increased from 0.6 million b/d to just over 4.8 million b/d, driving total US production to over 9.5 million b/d.

As oil prices fell from over $100 per barrel in late-2014 to $30 per barrel in early-2016, the industry saw total US production fall to about 8.5 million b/d in mid-2016. The industry responded by cutting costs, high-grading acreage, applying lessons learned in existing shale assets and improving operational efficiency; some may even call this phase the adaptation phase. As prices began to rise in 2016, the second boom cycle began. Total US production grew from 8.5 million b/d to 13.0 million b/d in late 2019.

The COVID-19 pandemic shocked global markets in 2020, and US oil production fell to 9.7 million b/d in just six months. The industry responded by seeking further operational efficiencies and fully engaged capital discipline favoring a new modus operandi of focusing on returning value to shareholders over increasing volume. Layering in industry-announced climate targets, caution by the banking and finance industry, and ESG-motivated investors, the oil and gas industry now has a self-proclaimed focus on generating strong returns to improve investor confidence and access to capital. Although US production has rebounded to almost 12 million b/d, it still stands at one million b/d below its peak just prior to the pandemic, even with oil prices rising in excess of $100 per barrel in 2022. There remains a sense of capital discipline across the industry — which is bolstered by perceived short-term risks of the economy falling into recession and long-term concerns over the pace of energy transitions. Many questions about the future of shale and US oil production therefore remain: Could the industry be entering a new shale renaissance as geopolitical pressures for energy security mount? Or could the next phase of shale oil and gas production be tempered by investor sentiments and the need to meet global climate goals?

Figure 1 — US Oil Production (Monthly, Jan. 2001-Jul. 2022)

Source: US Energy Information Administration.

III. The Future of Tight Oil Production: Views and Drivers

Many of the views expressed during the workshop indicated an expectation for US production to rise to 13 million b/d or more by year-end 2023. This view is largely driven by an expectation that prices will remain elevated moving into 2023, before moderating as the year progresses. However, the production outlook is fraught with uncertainties that extend beyond just potential price paths.

a. Near-term Production, Constraints and Uncertainties

Several short- and long-term structural trends were noted by participants when discussing current production trends. In the short-term, supply chain constraints continue to drive up costs and disrupt the availability of supplies and equipment — such as pipes, cement, casing, sand and chemicals, to name a few. Shortages in personnel for drilling and wellhead services are also being experienced. One participant even noted a recent survey by the Federal Reserve Bank of Dallas in which 90% of industry respondents stated that supply chain issues negatively affect their firms and that they expect these disruptions to last at least throughout 2023. This, it was argued, has had a tangible negative effect on the industry’s ability to boost production. It was also noted by multiple participants that even with these factors in play, drilling activity is rising, especially in the Permian Basin, but completions are lagging. This was pondered by one participant as a possible restocking of the drilled but uncompleted (DUC) well inventory — which was drawn down considerably during 2020 and 2021 as producers sought low-cost ways to keep production flowing, while capital dried up in response to the COVID-induced commodity crash and economic uncertainty.

As economies have recovered in the post-COVID era, demand for oil has accelerated back to pre-COVID levels. It was noted by several participants that this has triggered some unforeseen but predictable outcomes. For one, a lack of investment in new production capability has driven commodity prices up. Much of the capital restraint, it was argued, was driven by significant losses on balance sheets in 2020, government rhetoric about oil having reached its peak and “building back better,” ESG-motivations and investor sentiments for higher returns. In addition to tightening investment, fiscal stimulus provided by governments around the world to cope with the economic malaise wrought by COVID-induced shutdowns has provided a boost to demand as economies emerge from the pandemic. Taken together — restraints on investment in supply and demand stimulated by fiscal and monetary policy — economies around the world are set for an extended period of high inflation. This matters for the upstream oil and gas industry, it was argued, because inflationary pressures also manifest through increased capital requirements for personnel and equipment, thus raising the cost of drilling.

Compounding matters is a linkage between interest rates and production. As a response to rising inflation, the US Federal Reserve has been raising interest rates. In turn, access to capital is reduced by higher interest rates because borrowing costs increase, and expanding production requires capital. Thus, a combination of factors — supply chain difficulties, capital discipline, inflation and rising interest rates — has slowed growth in drilling and well completion, while rapid demand recovery and global supply disruptions have accelerated the need for new supply. Supply and demand must always balance in a market, so the near-term pressures are largely about the timing of various shocks. However, uncertainty remains, especially in light of mounting concerns about a global recession, making a rapid production response a risky proposition.

Going forward, it was expressed by several participants that as costs escalate, operators would prefer to maintain high earnings in the short- to medium-term as they weather current uncertainties in the marketplace. One participant even noted a long-standing piece of academic literature on “investment under uncertainty,” in light of these concerns. Regardless of the views expressed about robust, near-term uncertainties, there was a general, although not universal, positive stance on the medium to longer term. Several participants viewed current structural issues as likely continuing — or even worsening given pervasive economic and geopolitical uncertainties — for the next several months, before moving to a more stable situation. This will eventually lead to a “new normal” in total spending, but activity will continue to emphasize shareholder return rather than volume growth. This was a sentiment that was not debated by participants, as the shift in investor sentiment over the last couple of years has driven both private and public firms to emphasize returns and financial sustainability.

Even given the general tendency to emphasize returns, several participants highlighted a significant difference between public and private exploration and production firms. It was shared by one participant that public firms are expected to grow 5%-6% to approximately 300,000 barrels/year by 2023. Private firms, however, are expected to grow 20%-30% to 400,000-600,000 barrels/year on the back of a 35% increase in capital spending. The difference between the investment and expected growth of public and private firm production was attributed to private firms having more flexibility because shareholder pressures are not present — which allows them to be more agile as market conditions change. It was also noted that this is not new, as large public companies typically move more slowly than private companies. But this difference between public and private firms has significant bearing on near-term production trends given the current market uncertainties as well as political and shareholder pressures. Whether or not private firms actually expand production as expected remains to be seen, and some participants were skeptical they would.

b. Long-term Production and the Importance of Infrastructure

As noted above, despite the near-term uncertainties, several participants, but not all, shared a general optimism that US crude oil production would grow to more than 13 million b/d by the end of 2023, averaging more than 12.5 million b/d for the entire year. Notably, the anticipated growth assumes a significant production backlog that simply “hasn’t come online” yet.

Despite modest production growth, US crude oil exports have been incredibly strong in recent months. Several participants recognized that this growth in exports is a result of both higher global prices, especially for refined products, and the disruption of Russian supplies. It also highlights the importance of US oil for global market balance. However, the need for new infrastructure to access both domestic and international markets for further expansion was stressed. Infrastructure needs were cited as critical by several participants, for both crude oil and natural gas. Indeed, a scarcity of natural gas pipeline infrastructure, especially from tight oil developments with associated gas production, presents a challenge for oil production growth. If associated gas volumes cannot be flared, then they must find a marketable outlet, but that requires pipeline take-away capacity or onsite demand. Both options are being explored, depending on the location, but an inability to move gas volumes can compromise oil production, especially as flaring rules tighten.

Many participants also underlined that shale producers have generally become more resilient to lower oil prices, thanks to improved productivity. As such, if infrastructure impediments can be overcome, then US producers are likely to remain a vital component of the global oil supply portfolio for the long term. Nevertheless, a few participants contemplated that a peak in global oil demand within the next decade or so would challenge the long-term US production outlook. Such uncertainty calls into question the scale of investment needed for long-term supplies and makes it difficult to assess a potential return to capital over the next 20 years. This tends to leave long-term infrastructure investments in an environment of high uncertainty.

Participants also connected infrastructure to energy security, both domestically and abroad. In particular, they pointed out the energy security dimensions of the ability to access markets, which has implications for both buyers and sellers of energy. The European market, in particular, was singled out as an excellent opportunity for US exports, as European nations seek to diversify their sources of imported supplies. Of course, take-away capacity is a critical driver of future growth. One participant noted that, in addition to difficulties in permitting and construction, the proposed rule by the US Securities and Exchange Commission to include scope 3 emissions in climate commitments could put an additional constraint on pipeline capacity and export facility development.

c. Productivity in Shale

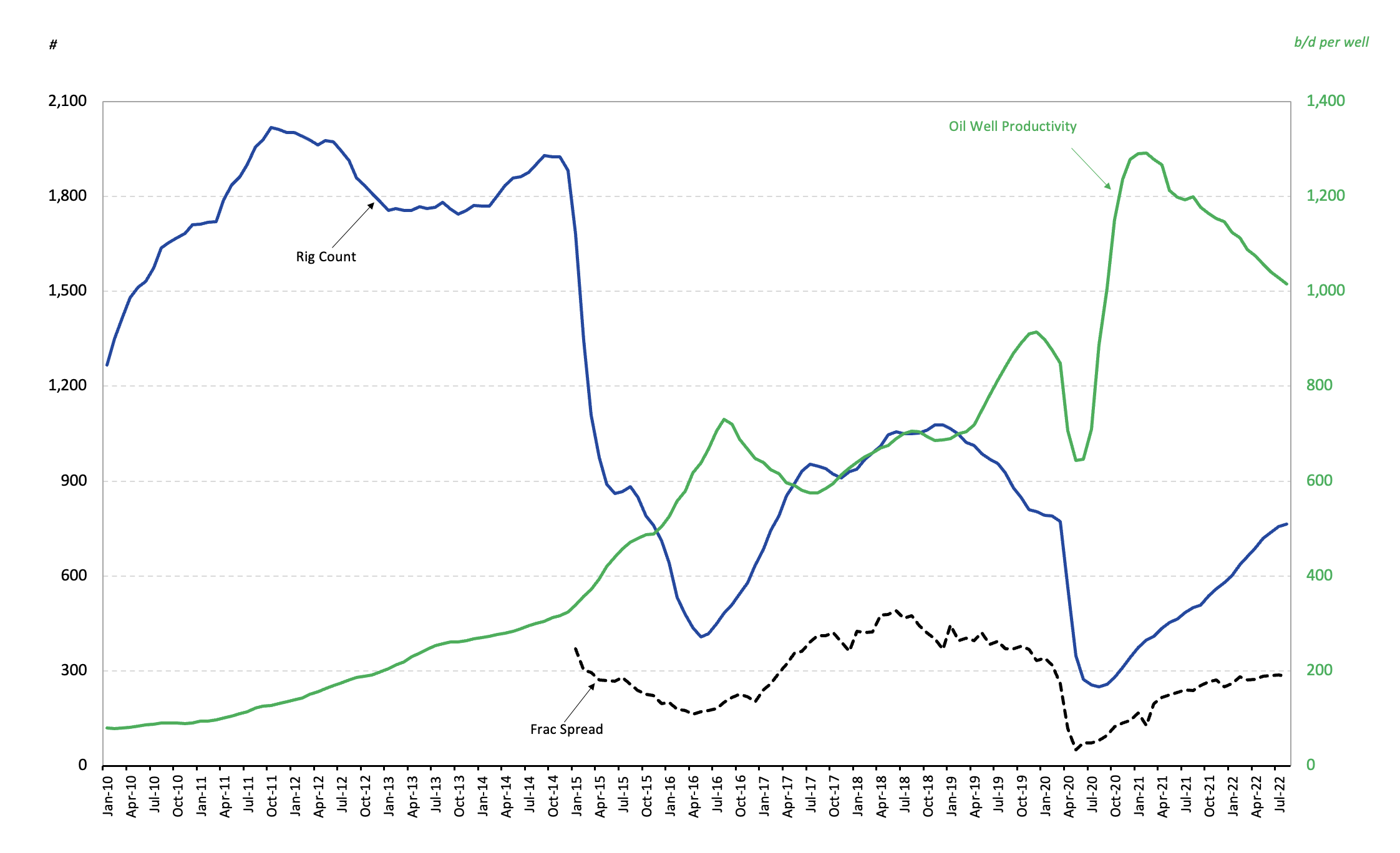

Participants generally expressed that they expected much higher upstream drilling and production activity at the current price level. Since the beginning of 2021, rig counts have more than doubled, and since January 2022, they have increased by 27%. The “frac spread” — or “frac fleet” — has increased by a smaller amount over the same time periods, 70% and 10%, respectively (see Figure 2). Frac spreads are generally a better indicator of how much production will come online in the near term, because they indicate active frac fleets engaged in well completion.

Notable from Figure 2 is the general trend of increasing productivity. This persistent trend was noted by several participants as indicative of the long-term success of shale. While there is a tendency for measured productivity to rise when rig counts and frac spreads fall, which tends to occur when prices weaken, this was attributed to producers high-grading acreage during times of tightening margins. Of course, productivity tends to decline when prices rise and drilling activity increases, but long-term rising productivity has persisted through these transitory shifts.

On the point of productivity, several participants postulated that the industry could sustain production at current levels for about 10 to 15 years in the most productive (tier 1 or tier 2) acreage in the so-called “sweet spots.” It was also noted the best prospects are being drilled first, meaning the industry will have to drill into lower-quality prospects as time progresses. It is worth noting that this is a basic tenet of the “economic theory of the mine.” However, the implication is that productivity will need to continue to increase if the remaining inventory of prospects is to be developed profitably. Given that 67% of active land-based rigs in North America are currently in the Permian and Eagle Ford regions, this also means that productivity gains in those shale basins will drive the foreseeable future of US oil production.

Figure 2 — Rig Counts, Frac Spreads and Oil Well Productivity (Monthly, Jan. 2010 - Aug. 2022)

Inevitably, as high-quality prospects in existing shale basins are developed, upstream focus will shift to other shales in places such as Utah and Wyoming to find new sweet spots. Some participants questioned whether the productivity gains seen to date will fully translate to new areas. For instance, drilling 15,000-foot laterals in some locations is possible, but it may not be in others, depending on the formations themselves. There is a countervailing factor, however, that favors continued productivity growth. It was noted that the intense pressure to improve cash flows and profitability has driven the industry to do more with less. For example, the ability to target deeper formations, stack laterals, drill longer laterals and drill more laterals from a single pad-site have been revolutionary. Innovations in downhole sensing, the use of artificial intelligence and improvements in field and reservoir simulation have all enabled significant improvements in productivity. These factors are transferable regardless of the shale formation.

In sum, productivity improvements are critical for growth in shale production. They are also important for maintaining existing production levels. As producers move into lower-quality acreage, productivity gains will be necessary to avoid declining production. Moreover, this all must balance against industry and firm-specific targets to reduce methane and other greenhouse gas emissions. Other issues such as water handling and disposal — including efforts to recycle produced water in field activities — and induced seismicity from waste water injection were also raised. To these ends, more than one participant noted how important productivity gains are to meeting all of these objectives, and commented that the objectives themselves are actually driving firms to continually improve productivity.

d. Energy Security and Prospects for New Shale Development

The war in Ukraine in February 2022 marked a turning point in discussions about energy security. The risk of geopolitically-motivated supply disruptions has renewed interest in new sources of supply. It has also highlighted the importance of oil and gas over the medium to long term, even as economies transition to lower-carbon energy sources. Thus, as long as the industry can generate solid and sustainable financial returns, there was a general consensus that capital will return to the sector. Of course, as noted by participants, strong returns will need to be balanced with investor and societal environmental preferences.

Shale development requires the buildout of a robust and well-functioning service industry. This is an advantage the US has above all others. In fact, the US shale revolution is unique. Although shale resources have been assessed globally, development has only seen significant advancement, so far, in the US. Participants agreed that the scale of the US shale revolution is unlikely to be replicated anywhere else. This was attributed to the depth of the supply chain — oil field services, for example — that supports upstream operations in the US. Another important factor is the ownership of subsurface resources in the US, which are largely held by private landowners, as opposed to the state/government. The US ownership model, rooted in the legal treatment of property rights, creates incentive for landowners to seek pathways for monetization that do not exist when mineral rights are owned by the state. This model cannot be replicated, absent a change in law, in most other places around the world.

Participants noted that although countries like Argentina and Australia have significant assessed shale resources, they also have constraints due to relatively thin oil field service sectors that lack the depth to respond quickly and at low cost to the demands of shale development. Moreover, given the need for new infrastructure and a growing international emphasis on environmental issues — such as methane emissions, flaring, and water treatment and handling — the likelihood of near-term robust shale development outside the US is low. Several participants did suggest, however, that the most exciting future shale developments could come from prolific oil-producing and exporting countries such as Saudi Arabia.

Given the low near-term prospects for shale development in other regions, a focus on US shale is understandable. It plays a major role in the global oil market balance and has significant foreign policy and energy security benefits for the US and, by extension, allies of the US. There was some discussion by participants regarding the potential for shale to serve a spare capacity function. However, it was also argued that shale is not appropriately characterized as spare capacity because (i) it is not a government-controlled asset, (ii) it is not accessible absent capital investment, and (iii) producers do not coordinate activity (by law), responding instead to commercial motivations. Even during the oil price crash of 2020, when WTI famously traded in negative territory, there was little political appetite to institute production quotas, despite hearings at the Texas Railroad Commission. Instead, producers responded by cutting back their drilling and completion programs (see Figure 2), thus allowing production to fall dramatically (see Figure 1). This re-emphasizes the point that commercial incentives are the primary driver of US production.

It was also noted that any ability for US shale to act as inventory has been further diminished as the DUC well inventory in the US has been drawn down substantially over the last two years. In fact, according to the Energy Information Administration, the DUC inventory has been cut in half since June 2020 (falling from 8,803 to 4,283 in August 2022) as firms sought ways to produce additional volumes from existing inventories rather than ramping up drilling activity. One participant noted that as firms continue to exercise capital discipline in their production programs, it is unlikely that the DUC inventory will grow in the near term.

Several participants raised the notion that the energy security benefits of tight oil and shale gas production in the US are limited by existing logistical constraints to accelerate production (i.e., supply chain constraints) and difficulties in expanding export capabilities (i.e., infrastructure and transport needs). Limited capacity to move oil and gas within US markets was noted as another challenge, as recent debates on the Jones Act demonstrate. This links directly back to the importance of infrastructure to move produced volumes to market, and it highlights the fact that US shale’s energy security implications are largest for the US. It was also noted that although US shale could offer greater energy security benefits in other regions with future investment in infrastructure, this is unlikely to change in the near term.

The current situation in Europe presents an opportunity for US oil and gas production. Specifically, exorbitant energy prices in Europe have been exacerbated by the interruption of flows of Russian supplies, thereby creating an opportunity to export greater volumes of US LNG and petroleum products to Europe. The current desire by European countries to reduce reliance on Russian energy supplies going forward may cement a longer-term relationship between US fuel suppliers and European buyers.

IV. Investor Sentiment and Shifting Producer Behaviors

The continued production of oil from shale in the US needs significant and stable capital investment. In an era of uncertain oil prices, tightening environmental policy and increasing costs due to inflation, this point is more salient than ever. To explore potential sources of capital, one participant shared some insights on historical investment trends for shale.

The historical investment trends were divided into phases. Following the global financial crisis in 2008, when oil prices bottomed out in December 2008 at below $40/barrel, oil prices (Brent) increased steadily, eclipsing $100/barrel in early 2011 and remaining above that level for 42 consecutive months. Appetite for oil-directed investment was strong, and US oil production increased from 5.1 million b/d in December 2008 to over 9.3 million b/d in November 2014, with tight oil production rising from 0.6 million b/d to 4.6 million b/d over the same time period, accounting for almost all of the increase in output.

After September 2014, oil prices declined after dropping below $100/barrel for the first time in 42 consecutive months. In January 2016, prices reached $30/barrel before stabilizing in the $40-$50/barrel range for the next 19 months. The US shale sector responded with cost cutting and innovation to maintain production, and the period experienced relatively flat production until early 2017. Production rebounded in 2017, as prices increased into the $50-$60/barrel range, and continued to expand as prices recovered and stabilized around $60-$70/barrel in early 2019. During this time, an urgency was expressed by investors to move away from a growth strategy and focus on positive free cash flows. Even before the COVID-19 pandemic, investors began to exit a sector that had generated sub-par financial returns. The rapid and large collapse in demand wrought by the COVID-induced, economy-wide shutdowns accelerated this evolution.

Producers in the US shale patch have since gained a sense of capital discipline, where operators now focus more on generating returns for investors rather than on growth. The decade of the 2010s highlighted a sector that reinvested more than 100% of its cash flow to drive growth rather than fortifying balance sheets and distributing returns to shareholders. This trend culminated in the worst equity performance in the market over the past decade. The recent emphasis on capital discipline coupled with a higher price environment have led to the oil and gas sector substantially outperforming the S&P 500 over the last 18-24 months and generating significant positive free cash flow. One participant noted that this has shifted sentiment among investors, particularly those focused on returns, and driven strong equity performance. Notably, however, this has not motivated a rapid increase in capital spending. Rather, as noted by one participant, firms have embraced ESG considerations to motivate a more deliberate approach to field development and operations. In turn, this has driven greater capital discipline and promoted stronger returns in the sector.

Participants agreed that a model with emphasis on higher free cash flow, more disciplined reinvestment and a focus on investor returns is a better, more financially sustainable model for oil and gas producing firms. In turn, the new strategy, as argued by one participant, has made such firms more attractive for investment opportunities to equity investors. That stated, some remaining skepticism among investors was recognized, particularly given previous poor performance coupled with tightening environmental requirements. Reestablishing credibility with investors was seen as an important step toward attracting substantial capital for any sustainable growth.

Several participants emphasized that the investor community is also urging an increased focus on ESG principles. It was argued that firms that incorporate sustainability metrics into their operations and strategic planning and adopt protocols for better measurement and transparency on environmental performance, will also become more attractive to a broader suite of investors. However, it was also noted that ESG metrics are still evolving, and uncertainty about what to emphasize could slow firms’ adaptation to a new investment environment.

Nevertheless, ESG considerations are impacting firm behavior. Many oil and gas firms are focused on delivering a robust financial performance while also working to reduce the environmental impact of their operations. This is a distinct shift from the previous decade where production growth was the emphasis. Investors are now asking companies about long-term climate risks, the risk of demand erosion due to energy transitions, the risk of stranded assets and the potential future costs assigned to carbon emissions. In fact, it was noted that oil and gas firms have had to address these issues in their investor relations calls, which has reinforced their emphasis on generating strong financial returns through exercising capital discipline and focusing on higher productivity.

Several participants also noted that a constantly shifting political environment makes it difficult for the industry to attract capital. In effect, political uncertainty is very high in the US. Even so, confidence was expressed that the industry, with a measured approach, can generate positive returns even as they take steps to address emissions, in-line with self-administered net-zero targets. Moreover, even if the demand for oil declines, participants expressed that continued investment would be needed to ensure that production remained robust enough to offset declines and keep the market in balance. In fact, if investment in new supply lags, the concomitant increase in prices will promise higher returns and attract capital. Hence, firms must remain capable of meeting global production needs in an environmentally responsible manner while also generating positive returns.

V. Closing Remarks

The story of US shale development is one of peaks and valleys — successes and failures. After over a decade of poor financial returns, the shale industry is striving to reestablish credibility and present an attractive proposition for potential investors. Thus, it is important to generate strong returns while also reducing environmental impacts.

Workshop participants agreed that oil is critical for economic activity in today’s societies. This makes all technically and commercially viable resources, such as those in US shales, important for the global supply portfolio. Significant and sustained investments are therefore needed to ensure there are sufficient supplies to meet global energy demands, even in future scenarios where global demand declines in the medium to long term.

However, even with the generally accepted assessment of the need for new oil supplies, uncertainty remains about the future of US shale production. Various factors — ranging from supply chain difficulties and shifting investor preferences to ESG considerations and the reprioritization of firm behaviors (i.e., emphasizing returns over volume) — contribute to this uncertainty. Participants also stressed that ESG concerns are here to stay. As such, the industry must meet the challenge of ensuring progress on environmental obligations as well as producing enough to ensure market balance and allay energy security concerns. To that end, it is critical to engage in a balanced dialogue about energy to achieve a sustainable future that recognizes the needs and concerns of all members of society.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.