“Washington is a city of Southern efficiency and Northern charm.” —John F. Kennedy

The announcement of a new BRICS bank displays the emerging economies’ desire to move away from Washington, DC-style lending institutions. But between India’s bureaucratic efficiency and China’s indifference to humanitarian, environmental, and regional concerns, they may come to resemble Kennedy’s tart characterization of the very place they hope to leave behind. Much work lies ahead for the creators of these new multilateral financial institutions before the first loan can be made.

How Were They Able to Agree?

Simply reaching sufficient agreement to announce the new BRICS bank represents a significant achievement for the six-year-old BRICS group, which includes Brazil, Russia, India, China, and South Africa. While it may seem silly to organize a serious international grouping based on a clever acronym, the BRIC countries are the four largest economies in the developing world.1 They have economic heft, but do they have much in common?

Unlike OPEC, for example, their economic fundamentals differ dramatically. Russia, Brazil, and South Africa export different commodities, while China exports manufactured goods and India exports services. Two are current account surplus and three are deficit countries.

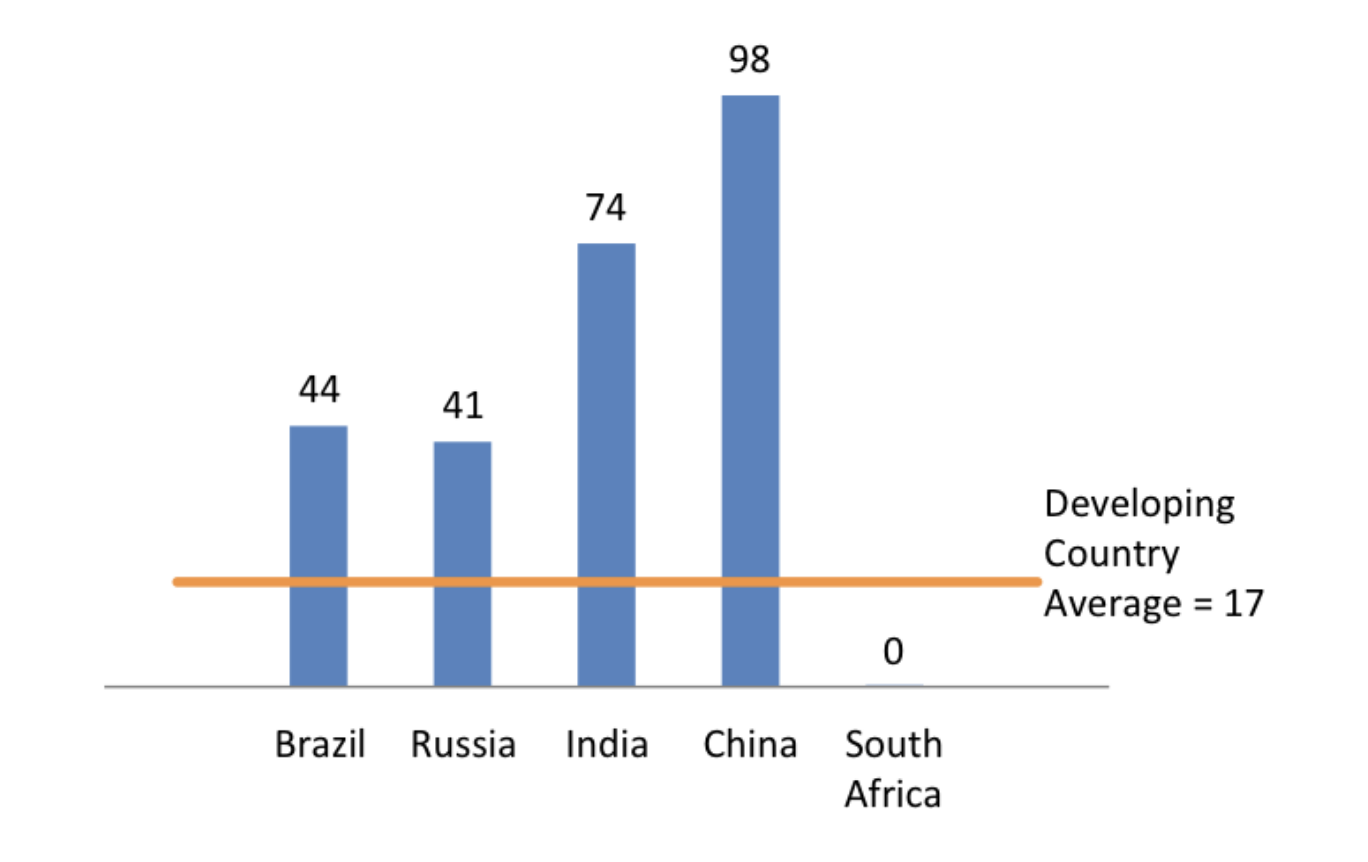

Common ground does exist. All but South Africa have serious enthusiasm for state-led lending in their own economies, though most have financial development plans that aim to reduce it (see Figure 1). All but China have infrastructure gaps—some more serious than others—and none have infrastructure gaps caused by lack of adequate financing.

What they most need to succeed is trust. Russia and India have long histories of conflict with China. Brazil and Russia are not famous for being creditworthy. South Africa is a solid neutral party, but also, frankly, a lot less significant than the other members.

Apparently, their joint desire to plant a flag on the global economy sufficiently overcame mutual differences. With no small amount of postcolonial pique, they all want to demonstrate their capacity for tangible contributions to global economic stewardship, independent of the Western-dominated established, multilateral institutions.

In Fortaleza, Brazil, the countries agreed on the broad outline for two new institutions. Formally, they pledged to establish the New Development Bank, which could resemble the World Bank, and the Currency Reserve Arrangement (CRA), which could resemble the IMF. Each will contribute $10 billion initially and have equal vote on the board.2

Figure 1 — State-owned Bank Assets, % of Total, 2010

Escaping Western Hegemony Over Lending Policies

What does it mean for a development bank to be freed of the dominance of developed economies? Where have these countries disagreed with developed countries on World Bank policy, for instance?

There are politics in any multilateral organization, and certainly some rich countries have a heavy hand from time to time in pushing their peculiar priorities. The US Congress, for instance, restricts by law US support for lending by3 the International Financial Institutions (IFIs, like the World Bank, IMF, or Asian Development Bank) to countries or activities that contravene certain US sanctions programs.

But the preponderance of the friction on lending policy (we will get to institutional governance next) at the IFIs reflects typical lender-borrower conflict. Developed countries, most often net lenders, want high standards to make sure money is used responsibly and repaid. The developing countries, most often net borrowers, resent outsiders imposing conditions on the use of money inside their own country.

The conditions placed on loans are broadly either prudential or values-based. Prudential conditions protect the financial integrity of a loan—ensuring that the money is used wisely and gets repaid. Values-based conditions protect its moral integrity, ensuring that money does not fund unsavory activities.

Two main prudential mandates cause splits in the IFIs.

- Additionality: This strange term is IFI-speak for whether the loan adds value (by solving a market failure or promoting social benefits) that could not be financed otherwise. This prevents the World Bank from using its limited resources on what amounts to corporate welfare.

- Loan-level governance: The IFIs are quick to shut down projects with allegations of sweetheart deals and hold the borrowing country accountable. Imposing developed-world standards for contracts can be painful in countries where things typically run more loosely. This discipline ensures, first, that the money goes only where it should, and, second, that the institution’s reputation remains untarnished. The IMF further imposes difficult reforms as conditions for its loans to help the borrowing nation not just repay but avoid future loans.

Values-based mandates range from the frivolous to the serious.

- Priorities: Rich-world fads influence the World Bank. Borrowing countries can feel pressured to develop more projects in clean energy or financial inclusion, say, than they would prefer, and these priorities are debatable. But by and large, the World Bank responds to borrowing countries’ project requests, not the other way around.

- Social impact standards: World Bank loans include onerous requirements for social impact audits to ensure, for instance, that anyone displaced by an infrastructure project is treated well. Such concerns are not always given equal weight in purely domestically financed projects, as the Three Gorges Dam exemplifies.

- Environmental impact standards: High environmental standards may feel like a luxury that rich countries impose, while borrowers prioritize economic progress. Sometimes these are hypocritical standards, as when the US spearheaded a ban on World Bank lending to coal projects despite having no similar ban on new coal plants at home. Balancing environmental concerns against developmental needs is difficult, but lenders feel the use of “their” money should reflect their values.

By and large, the Western hegemony that the BRICS hope to escape means holding loans to high standards. Often, that is simply good business—making sure loans are repaid and protecting the reputation of the institution. Some of these standards reflect rich-world values that may not be prioritized by the BRICS. They are good, high-minded values that the BRICS do hold, but at what cost?

If the BRICS are comfortable with lowering their lending standards in the new development bank, I do not doubt they will find plenty of projects to fund. If they are, it is best that the existing IFIs are not affiliated with it. If they are not, and are able to maintain high standards, then it is not clear what their comparative advantage is. As Robert Kahn at the Council on Foreign Relations rightly identified, the World Bank and regional development banks largely fill current demand.4

Getting Institutional Governance Right

From what has been announced, the BRICS bank will take a very democratic approach to governance by giving each member equal voting rights. The democratic governments among them have proudly trumpeted this arrangement in contrast to the IFIs, where voting power largely follows financial contribution. Undoubtedly, there is value in such an equal arrangement for symbolic solidarity, as well as to avoid concerns about Chinese domination. But is it practical?

Some consideration rests on the allocation of vetoes. If equal vote means equal veto power, like in the UN Security Council, the institution may be doomed. India’s government famously makes decisions on a consensus basis, resulting in a ponderously slow pace of progress. If India selects a civil servant as the first president, he or she would feel only too at home trying to meet every country’s demands before moving projects forward.

Despite its shortcomings, this arrangement may be the only way to overcome their mutual trust deficit. The rotating right to select the BRICS bank president is an example. The Chinese may have been placed last in line as an incentive to allow institutional independence. If independence has not been established well before their turn comes in 20 years, there may be no bank to lead.

There are good reasons to suspect the Chinese will dominate the BRICS bank. Mihir Sharma has already pinned the bank as a vehicle for the Chinese to commandeer the friendlier public image of the three southern BRICS as a front for China’s foreign economic policy.5 Maybe Russia had the same thought as China. They are the two countries best placed, by virtue of their structural current account surpluses, to provide more funds for institutional growth. But such funds rarely come without strings.

For one, the United States manages to sway the World Bank and IMF significantly with only 15 percent of the vote. This share gives it the only single-country veto on certain board-level decisions, but the biggest source of its influence is the soft power of location. US Treasury officials walk the four blocks back and forth many times a day, allowing them to scrutinize the institutions much more closely than any other government.

In addition, staffing needs (unofficially) allocated to Americans can easily attract highly qualified candidates. It can be much harder to convince Japan’s best and brightest, for instance, to move to Washington and work in an all-English environment. The US cadre is therefore often—of course, not always—the most effective at influencing these institutions from the inside out. While the US government makes no attempt to influence Americans employed at the IFIs, can the same be said of China?

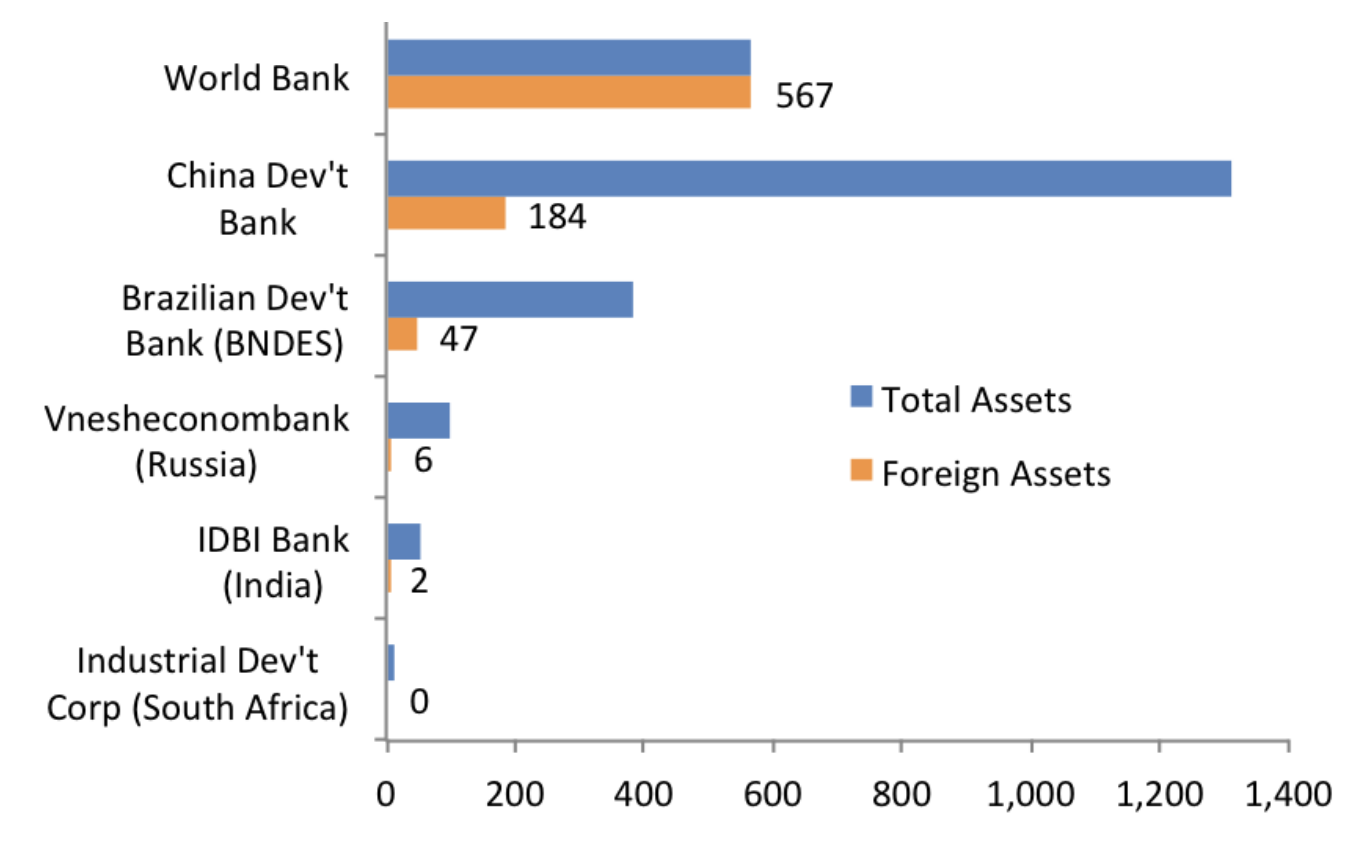

Besides home-field advantage, the Chinese have a head start in experience. The China Development Bank is more than twice the size of the World Bank, with a substantial portfolio of lending to projects overseas. None of the other BRICS come close (see Figure 2).

Imagine, on the other hand, that the institutional arrangements prevent Chinese dominance. Can an institution survive being funded primarily by China and Russia, when their influence is no greater than any other member? But if adequate checks are put in place to prevent Chinese dominance, will China remain interested in this project?

This works as long as the countries with underweighted representation (by IFI standards) see long-term value in the institution. For instance, Sharma cites “Jim O’Neill’s theory, that the BRICS bank is a ‘low-risk rehearsal’ for the global leadership role at the IMF, the World Bank, and the UN that China expects to shortly play.” That would not convince US taxpayers to accept such a bargain, but China and Russia have less need to answer to their own taxpayers.

Figure 2 — Assets of the Largest Development Bank in Each BRICS Country, 2013

Conclusion

The BRICS clearly want something tangible to demonstrate their global prominence and the power of non-Western values. Yet the new BRICS bank faces two critical tensions that the BRICS must navigate. The first pits the desire to be free of the IFI’s constraints on lending that developing countries chafe against, versus the need for prudential lending. The second sets the high-minded desire for equality of governance against the reality that the lack of Chinese dominance may result in institutional neglect by its primary benefactor.

While the BRICS bank project was put together in an impressively short two years, most of the difficult decisions remain unanswered. These tensions will not be easily resolved, and will determine the bank’s viability. I expect it will be several years before the details are sufficiently ironed out for the BRICS bank to open its doors.

Endnotes

1. South Africa was admirably added to Goldman Sachs’ original BRIC acronym sometime before the group began meeting in order to include an African representative, although there are nine larger developing economies, including Nigeria’s.

2. Technically, the CRA will have a separate endowment and board, but its funding structure does not require much of an upfront outlay.

3. “Africa’s new Number One,” The Economist, April 12, 2014, http://www.economist.com/news/leaders/21600685-nigerias-suddenly-supersized-economy-indeed-wonder-so-are-its-still-huge.

4. Robert Kahn, “BRICS and Mortals,” Council on Foreign Relations Macro and Markets Blog, July 15, 2014, http://blogs.cfr.org/kahn/2014/07/15/brics-and-mortals/.

5. Mihir S. Sharma, “BRICS Bank: worthless at best, a disaster at worst,” Business Standard, July 16, 2014, http://www.business-standard.com/article/economy-policy/brics-bank-worthless-at-best-a-disaster-at-worst-114071600571_1.html.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.