Introduction

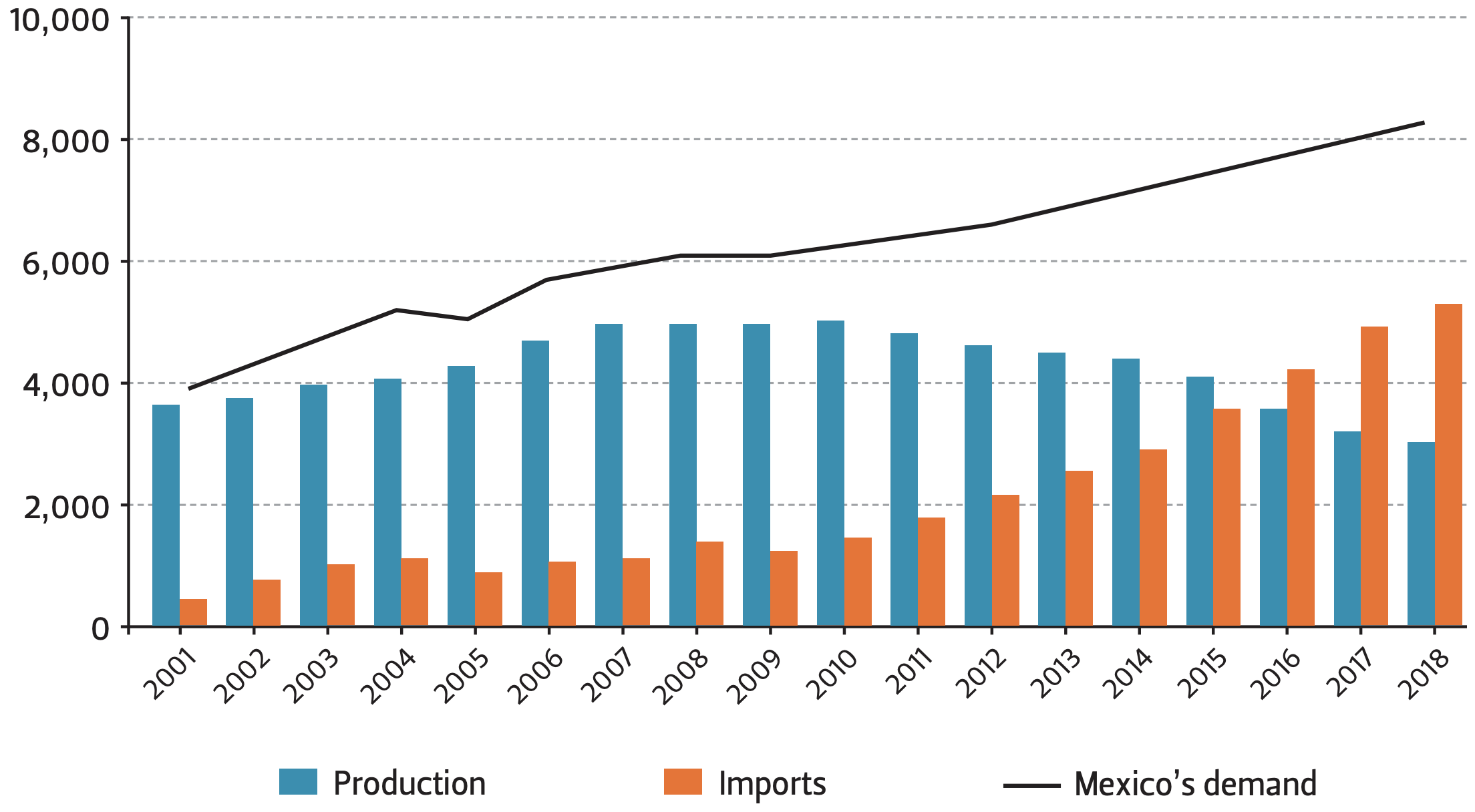

Mexico’s natural gas industry is at a crossroad. While domestic production has been on a downhill trajectory for almost a decade now and consumption has expanded, the resulting gap has been covered by ever-increasing imports (Figure 1).1 In 2018, 71% of the natural gas available locally was sourced abroad.2 As a result, Mexico’s new president, Andrés Manuel López Obrador (AMLO), sees boosting domestic natural gas production as the backbone of his policy agenda to limit Mexico’s import dependency and strengthen energy sovereignty. But while these goals are not controversial per se, the policy direction of Mexico’s president casts doubt on whether the proposed agenda can be realized.

Two main factors lend themselves very well to advancing Mexico’s strategy of increasing domestic natural gas production: 1) the large unconventional (shale) resources Mexico is estimated to hold;3 and 2) the ongoing comprehensive reform that opened Mexico’s oil and gas sector to private investment. However, contradictory statements about whether shale development in Mexico should be banned4 and whether the country should postpone oil and gas auctions have raised a great deal of uncertainty about the future of these two factors. This has made energy pundits wonder what would be an alternative route consistent with AMLO’s aim of energy sovereignty.

Most observers focus on the potential impact on Mexico’s production growth5 should oil and gas auctions be halted under AMLO’s presidency. The effects of a ban on shale development in Mexico have not been discussed as much. Our analysis leads us to posit that whether or not shale development is banned in Mexico, little will change in the near- to medium-term since above-the-ground factors such as limited access to water6 and a lack of infrastructure are likely to stall shale development. Nonetheless, in the long run, a ban on shale—even if it only stands for the six years of AMLO’s presidency—may have adverse consequences in the absence of an effective scheme to diversify Mexico’s gas supply sources. This is because beyond retarding new production, a ban would shelve the establishment of regulatory and legal frameworks that could encourage shale development—e.g., exploratory drilling, pipelines and other infrastructure, and the creation of a local workforce and a base for equipment and supplies. A ban would also impede foreign and domestic investment and innovation, which are both central to shale’s success in the United States.7

To Ban or Not to Ban

Those intimately familiar with Mexico’s energy issues, including Rocio Nahle,8 AMLO’s own secretary of energy, have hinted at the necessity to assess—from an environmental and technological standpoint—the viability of a variety of extraction techniques as potential methods for domestic natural gas production.9 But AMLO does not seem to share that line of reasoning. On several occasions, the president has claimed—as he did as a candidate—that fracking would be banned under his tenure.

Figure 1 — Mexico’s Natural Gas Balance, 2001–2018 (in Million Cubic Feet per Day)

Despite the president’s vow to abandon shale development and forbid fracking, the AMLO-controlled lower house of Mexico’s Congress earmarked 3.35 billion MXN (approximately US$170 million) in the 2019 budget for the evaluation of shale formations in various Mexican basins.10 Also, purportedly acting in compliance with existing regulations,11 Mexico’s National Hydrocarbons Commission (CNH) sanctioned PEMEX’s use of hydraulic fracturing in four exploration blocks in the Tampico–Misantla basin, in the state of Veracruz.

These actions are inconsistent with AMLO’s previous statements and suggest, since they come from government institutions, that the fate of shale is not yet settled. Instead, AMLO may be keeping the option to abandon his campaign promise if shale extraction could, for example, address his other promises, including decreasing Mexico’s dependence on foreign energy sources.

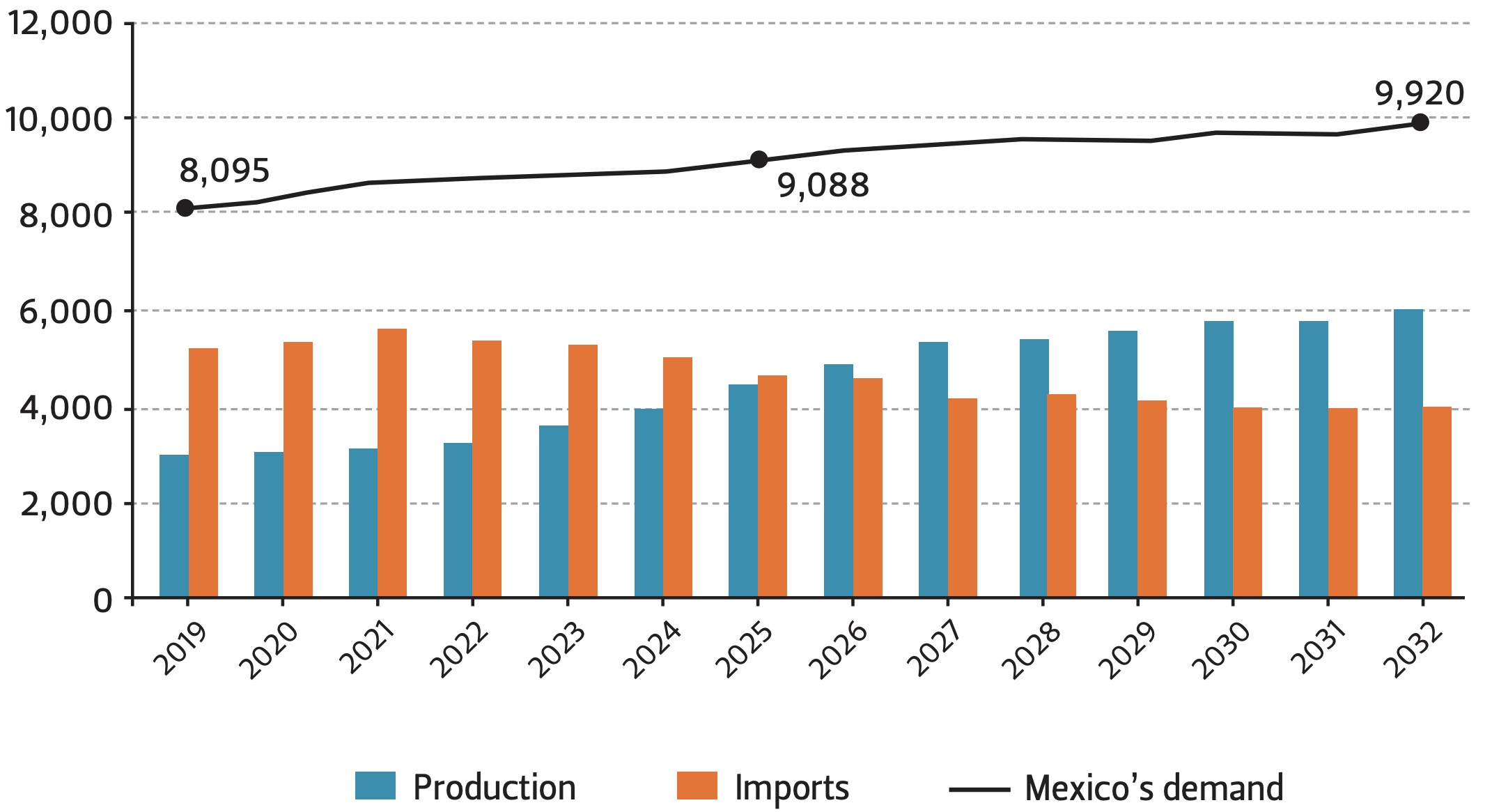

For its part, Mexico’s Secretariat of Energy (SENER) appears to be optimistic in its assessment of the country’s domestic energy potential.12 Bearing in mind past bidding rounds and PEMEX’s onshore and offshore resources, SENER forecasts in its most recent outlook that between 2019 and 2024 (which will be AMLO’s last year in office) domestic production may expand by around 31% and imports may decline by 3.3% (Figure 2).13 Hence, the gap between production and imports may start to narrow. And while in 2024 U.S. imports will still satisfy 56% of Mexico’s demand,14 shortly after that time—in 2026—SENER forecasts that domestic production will exceed all natural gas imports. This is four years earlier than SENER estimated in its 2017 outlook.15 The energy outlook prepared by the U.S. Energy Information Administration (EIA)16 is somewhat less positive, but it still anticipates that Mexico’s domestic production will start to displace U.S. imports by 2030.

Auctions, Investment, and Debt

The administration of Enrique Peña Nieto (2012-2018) instituted constitutional changes in the Mexico’s energy sector in 2013, allowing the participation of private firms in activities where PEMEX had long been the sole player. Through auctions, Mexico’s goal was to increase by 2018 crude production to 3 million barrels per day (MMbd) and natural gas production to 8 billion cubic feet per day.17 Although these targets were not met, the point is that 4-5 years into the implementation of reforms, Mexico’s energy sector has started to change gradually, owing to ongoing investments in areas such as fuel storage and commercialization, renewable energy, and natural gas pipelines. Nonetheless, the largest share of investment will come from past oil and gas auctions (exploration and production), the outcomes of which in terms of production will materialize in the long-term. In this regard, investment is expected to reach $161 billion as a result of nine completed auctions at which 107 contracts were awarded to 73 firms from 20 different countries between 2015 and 2018. According to projections by SENER, production18 from these contracts is expected to amount to 0.816 MMbd by 2030, with 74% of the profits feeding the government’s coffers.19

Despite these gains, Mexico’s lagging production, its need for investment, and AMLO’s vow of energy sovereignty, the president has halted new bidding rounds.20 Round 3.2 and Round 3.3, which were scheduled to take place after last year’s presidential election, have been postponed indefinitely until the companies that hold contracts from previous auctions show significant results. This decision is viewed as a blow not only to the energy reform, but also to Mexico’s prospects for producing more natural gas since both auctions were meant to target both conventional and unconventional hydrocarbon resources, with many of the areas adjacent to shale formations in Texas. Now the pressure is on private operators to ramp up drilling on previously auctioned properties and prove to AMLO that their participation is necessary. Less than four years after awarding the first contracts, CNH reports that—as of January 2019—the contract holders are producing 0.072 million barrels per day (MMbd) of oil, or 4.4% of Mexico’s daily oil production, and 175.6 million cubic feet per day (MMcfd) of natural gas, or 3.8% of Mexico’s daily natural gas production.21 It is still too early to assess whether these numbers represent success given the long-term nature of exploration and production activities.

Figure 2 — Forecast of Mexico’s Natural Gas Balance, 2018–2032 (in Million Cubic Feet per Day)

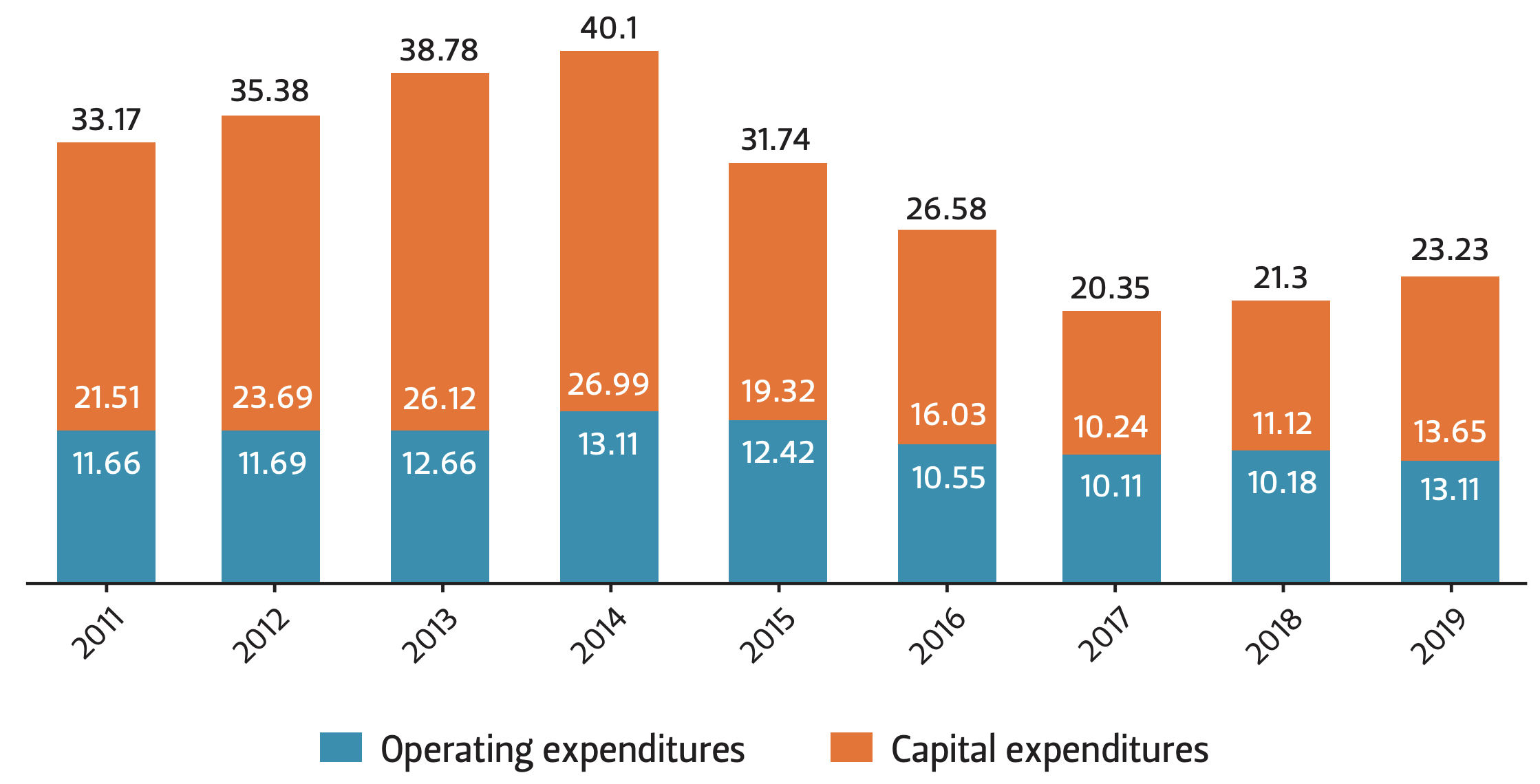

Meanwhile, AMLO is considering a greater role for PEMEX in exploration and production and sees value in restoring the company’s ability to invest into new production and areas like refining. To this end, the government has boosted the company’s 2019 budget for operations and capital expenditures to the equivalent of US$23.23 billion, which is a 9% year-on-year increase. Looking at capital expenditures alone, the change in 2019 is even greater, with a 23% increase over 2018.22 PEMEX’s 2019 budget may be an increase over 2017 and 2018 (Figure 3) but it is a far cry from the company’s expenditures during previous years. PEMEX’s capital expenditure totaled US$26.99 billion in 2014, almost twice the amount suggested by AMLO in his first year in office.23

Figure 3 — PEMEX Operating and Capital Expenditures, 2011–2019 (in $U.S. Billion)

It seems, however, that AMLO’s attempts to boost PEMEX’s exploration and production activities may not be successful enough to make up for abandoning auctions. This is because the economic damage inflicted by decades of insufficient investment and heavy reliance on PEMEX profits as source of budgetary revenue is now taking a toll on today’s efforts to strengthen Mexico’s largest firm. PEMEX is the world’s most indebted oil and gas firm,24 and recent credit rating downgrades illustrate that additional capital injections25 will be required if the objective is to ameliorate the company’s structural problems of falling production and excessive debt.26 If PEMEX cannot meet AMLO’s production goals, the president’s administration could be swayed to resume oil and gas auctions, including those for unconventional oil and gas resources.

Mexico’s Shale Gas: What Can and What Cannot Be Done

Even if it is not clear whether AMLO’s proposed ban on shale development will come to pass, it is useful to consider what a potential ban could mean for Mexico’s energy market.

First, development of shale in Mexico will not be an easy task, even though the Burgos basin shares geological features with the prolific Eagle Ford in the U.S. This is because the success of shale development in the U.S. is tied to a unique mixture of on-the-ground infrastructure and regulatory and legal factors that, as a whole, cannot be found currently anywhere else in the world.

So what are the elements that could make shale development less feasible in Mexico than in the U.S.?

Regulatory and Legal Environment

The obstacles start with the ownership of subsurface minerals. As opposed to the U.S., in Mexico the government rather than the landowner owns subsurface rights. And since it is too early to predict how attractive the system of royalties and fees will be, it remains to be seen whether the economic incentive for the landowner is enough to offset the disruption to his land caused by drilling. Moreover, the process to acquire drilling rights is also notably slower and more bureaucratic since firms must wait for federal regulators to auction acreage. In contrast, in the U.S. this process is much faster and easier as firms can approach landowners directly. Likewise, the U.S. has developed a robust body of state- and federal-level legislation and regulations concerning drilling and hydraulic fracturing standards, water use and disposal, and other environmental concerns related to shale drilling. These institutional capacities have yet to be developed or strengthened in Mexico.

Sector Development and Infrastructure

Mexico lacks a well-developed private sector that could provide specialized oil and gas services. Of course, given Mexico’s proximity to the U.S. and U.S. shale development in the Permian and Eagle Ford basins, some service companies may be willing to come across the border to work. However, those companies would still lack the locally or regionally based service and equipment companies and workforce that exist in U.S. shale regions. There is also the issue of pipeline infrastructure that would have to be built to deliver any shale oil and/or gas from the scarcely populated Mexico’s shale regions to processing plants and centers of demand. Similarly, the current road and rail infrastructure may not be sufficient to bring in the sand, water, and equipment necessary for hydraulic fracturing activity. Additionally, a considerable increase in truck traffic could wreak havoc on the existing local roads.

Other On-the-Ground Factors

There are several issues that will additionally complicate shale development in Mexico. These include the limited availability of water, the sparsely populated areas around shale plays, and security problems.

Mexican states with shale potential—such as Coahuila, which neighbors the Eagle Ford basin—are under significant levels of water stress.27 Since hydraulic fracturing processes use considerable amounts of water, the water shortage will definitely create barriers to shale development there.

Areas with shale formations are also sparsely populated, which poses logistical challenges for industry and government. For example, there is the challenge of ensuring room and board for the temporary workers who move across states from one rig to another. In the U.S., the problems of enough housing and other necessary services associated with the rapid growth of a mobile population have been quite significant in lightly populated areas of North Dakota. As a result, housing prices have skyrocketed and local communities have experienced a weaker than expected economic boost, as some of the new oil and gas revenues had to pay for new housing and infrastructure, including new roads.

Lastly, there is the issue of the security and safety of workers, equipment, and infrastructure that are subject to drug cartel activity and violence in the shale regions of Mexico.

Conclusion

The legal and regulatory, infrastructure and other above-the-ground factors discussed in this brief are more than likely to slow any potential development of shale and increase its cost in Mexico. And since there is ample and more affordable shale oil and gas right across the northern border, the economic calculus does not favor prospects for Mexico’s shale production, particularly in the absence of strong government incentives for industry in the form of taxes and landowner royalties, for example. But with safer investments like offshore and conventional development already established and in-demand from foreign firms, there is no incentive for the cash-poor Mexican government to provide incentives to drill or invest in as-yet untouched shale resources.

As such, government and non-governmental actors are more likely to concentrate on other, more attainable ways to expand Mexico’s natural gas supply. These could include 1) gas associated with crude production, including reducing flaring; 2) a more efficient way of extracting non-associated gas from current conventional sources; 3) pipeline development; 4) nitrogen rejection; and 5) improved efficiency, including optimizing the operation of natural gas processing plants.

Considered in this light, the potential decision by the AMLO administration to ban shale activity may not have an immediate or even medium-term impact on Mexico’s energy prospects. Mexico will continue to focus its exploration on shallow waters and to rely on the U.S. for natural gas. However, in the long-term, a ban means that Mexico would miss the opportunity to start implementing the regulatory and royalty/taxing regimes that would support the development of shale resources, which are estimated to be significantly more abundant than the country’s conventional energy resources. As a consequence, Mexico is likely to deepen its dependency on imports. And ironically, much of those imports will come from shale.

Also in the long-term, closing the door to shale development deprives Mexico of the potential economic benefits of this unconventional energy resource, including increased employment and investment. In addition, domestically available shale gas could provide cheaper feedstock for power generation, chemicals, including nitrogen fertilizers, or refining.

Even if the shale ban is short-lived, it will postpone institutional capacity-building and industrial development. In addition, Mexico’s import dependency may grow through the build-up of long-term infrastructure, such as cross-border pipelines. Once in place, these are likely to discourage domestic production, which is already bound to be challenged. The ones to profit will be the shale producers who work in the U.S. section of the Eagle Ford and Permian basins and are happy to dispatch the gas associated with their oil production to Mexico.

Endnotes

1. Mexico’s Energy Information System (SIE), “Dry natural gas balance,” http://sie.energia.gob.mx/bdiController.do?action=cuadro&subAction=applyOptions.

2. When PEMEX demand is discounted, imports represent 99% of the natural gas available domestically. Source: Mexico’s National Hydrocarbons Commission (CNH), “Natural gas balance,” December 2018, https://hidrocarburos.gob.mx/media/1975/balance-gas-natural.pdf.

3. In 2013, it was estimated that Mexico’s unproven technically recoverable shale resources amounted to 545.2 trillion cubic feet. Source: U.S. Energy Information Administration (EIA), World Shale Resource Assessments, https://www.eia.gov/analysis/studies/worldshalegas/.

4. “No habrá fracking en México, reitera López Obrador,” El Financiero, February 4, 2019, https://www.elfinanciero.com.mx/economia/no-habra-fracking-en-mexico-reitera-lopez-obrador.

5. “Delays of Mexico oil, gas auctions will slow revenue, production growth: commissioner,” S&P Global Platts, March 5, 2019, https://www.spglobal.com/platts/en/market-insights/latest-news/oil/030519-delays-of-mexico-oil-gas-auctions-will-slow-revenue-production-growth-commissioner.

6. “Mexico opens door to hydraulic fracturing, but water a worry,” Bloomberg Environment, February 20, 2019, https://news.bloombergenvironment.com/environment-and-energy/mexico-opens-door-to-hydraulic-fracturing-but-water-a-worry.

7. For more on the U.S. natural gas industry, see Ken Medlock, The impact of the shale revolution (PowerPoint presentation, Baker Institute’s Center for Energy Studies, March 26-27, 2019), https://eneken.ieej.or.jp/data/6750.pdf.

8. “Discuten fracking in tercer foro energético,” Energía a Debate, March 4, 2019. https://www.energiaadebate.com/petroleo/discuten-fracking-en-tercer-foro-energetico/.

9. “Secretaría de Energía analiza fracking sustentable,” El Economista, March 4, 2019, https://www.eleconomista.com.mx/empresas/Secretaria-de-Energia-analiza-fracking-sustentable-20190304-0151.html.

10. See Secretariat of Finance and Public Credit (SHCP), Mexico’s expenditures budget, 2019, “Investment projects of PEMEX Exploration & Production,” https://www.ppef.hacienda.gob.mx/work/models/PPEF2019/docs/52/r52_t9g_pie.pdf.

11. This is according to Gaspar Franco, at the time a CNH commissioner who voted in favor of the PEMEX proposal; he has since resigned from his post. See 8th Extraordinary Session of CNH Governing Body, February 11, 2019, https://www.gob.mx/cnh/documentos/8-sesion-extraordinaria-del-organo-de-gobierno-de-la-cnh-2019.

12. It is worth observing that the 2018 natural gas outlook is based on SENER’s maximum scenario, which comprises all the awarded contracts in auctions organized by CNH since the approval of reforms and PEMEX resources.

13. Prospectiva de gas natural 2018- 2032 (Ciudad de México: Secretaría de Energía, 2018), http://base.energia.gob.mx/Prospectivas18-32/PGN_18_32_F.pdf.

14. Ibid.

15. Prospectiva de gas natural 2017-2031 (Ciudad de México: Secretaría de Energía, 2017), https://www.gob.mx/cms/uploads/attachment/file/325639/Prospectiva_de_Gas_Natural_2017-2031.pdf.

16. U.S. Energy Information Administration (EIA). Annual Energy Outlook 2019, https://www.eia.gov/outlooks/aeo/pdf/aeo2019.pdf.

17. México, Gobierno de la República. Resumen ejecutivo de la reforma energética, https://embamex.sre.gob.mx/suecia/images/reforma%20energetica.pdf.

18. It hinges on the extent of exploration success.

19. Secretariat of Energy (SENER) (press release 065, September 26, 2018), https://www.gob.mx/sener/prensa/licitaciones-petroleras-atraeran-inversiones-por-cerca-de-161-mil-millones-de-dolares-al-pais-pjc?idiom=es.

20. “AMLO call for bid oil hiatus until companies show results,” Bloomberg, December 5, 2018, https://www.bloomberg.com/news/articles/2018-12-05/amlo-calls-for-oil-tender-hiatus-until-companies-show-results.

21. Mexico’s National Hydrocarbons Commission (CNH), Board of Crude and Gas Production, https://portal.cnih.cnh.gob.mx/dashboards.php.

22. See Petróleos Mexicanos (PEMEX), Operating and capital expenditures, 2011- 2019, http://www.pemex.com/ri/finanzas/Paginas/InversionCifras.aspx.

23. However, AMLO’s government has hinted that PEMEX is set to receive additional capital injections during 2019.

24. As of November 2018, PEMEX’s debt amounted to US$103.4 billion, with debt obligations to cover of $25.5 billion between 2019 and 2021. See Petróleos Mexicanos (PEMEX), 2019 Financial and operating outlook, http://www.pemex.com/en/investors/investor-tools/Presentaciones%20Archivos/2019%20 NY%20Roadshow.pdf.

25. PEMEX’s capital expenditure budget may surge as the Secretariat of Finance and Public Credit (SHCP) is contemplating additional capital injections to PEMEX during 2019. See “Preparan más apoyo a PEMEX,” El Heraldo de México, March 9, 2019, http://bit.ly/2VMUcLr.

26. “The measures announced today do not solve PEMEX’s structural problems,” BBVA Research, February 15, 2019, https://externalcontent.blob.core.windows.net/pdfs/190215_PemexMedidasAnunciadas_eng.pdf.

27. “Water scarcity could deter energy developers from crossing border into northern Mexico,” Circle of Blue, June 24, 2015, https://www.circleofblue.org/2015/world/water-scarcity-could-deter-energy-developers-from-crossing-border-into-northern-mexico/.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.