Author(s)

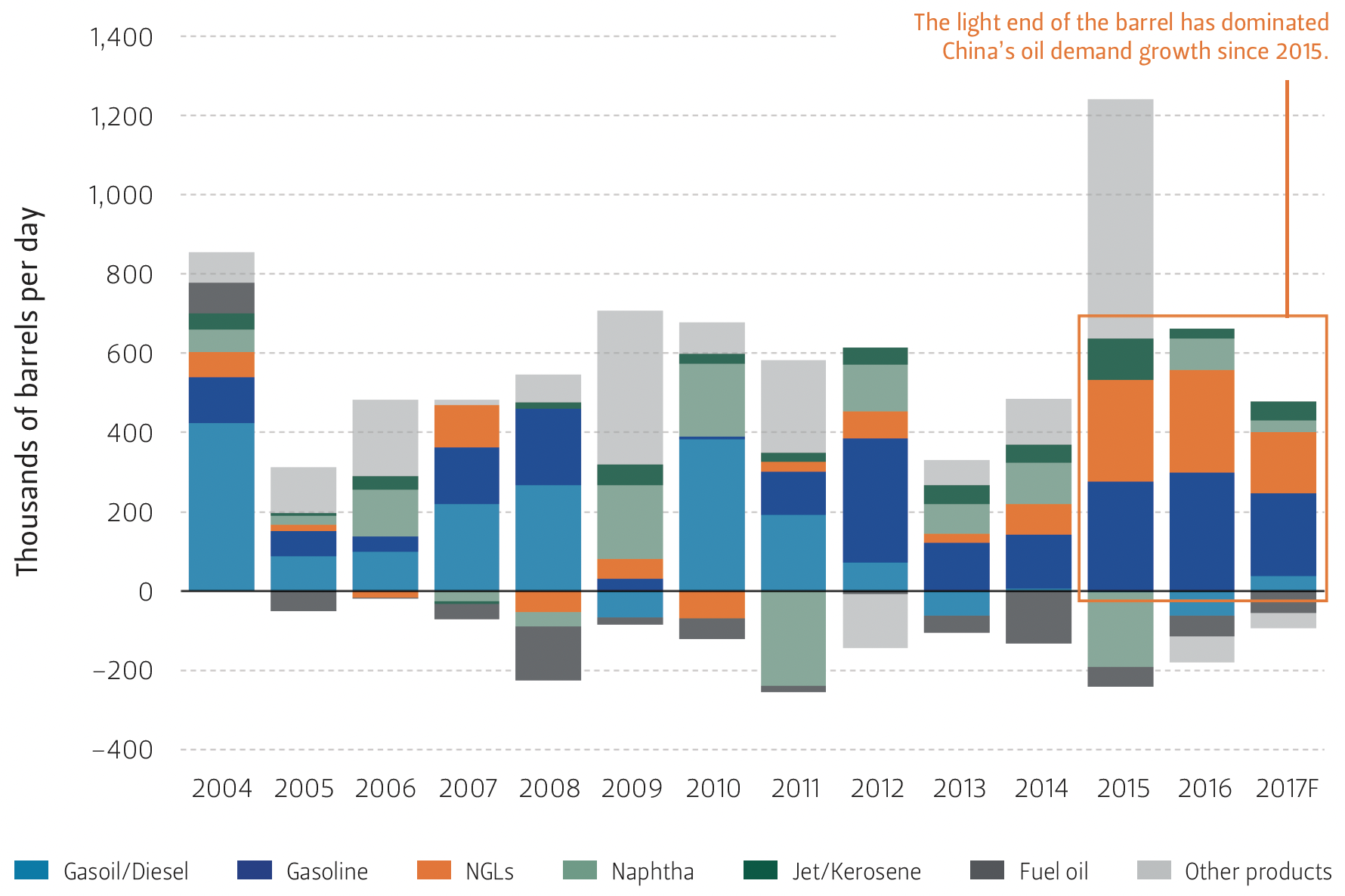

China’s oil products demand growth over the past several years has been dominated by the light end of the barrel. In 2015, gasoline and natural gas liquids (NGLs) together accounted for 53% of net incremental oil products demand growth in China (Figure 1).1 By 2016, light ends accounted for such a significant proportion of this demand that without gasoline and NGL demand growth, oil product consumption in China would have actually declined, as consumption of diesel fuel and residual fuel oil fell year-on-year.

Figure 1 — China Oil Products Demand Growth by Category (2004–2017)

As China’s demand for light oil products continues to drive incremental consumption growth, an interesting theme is becoming apparent: commodities that are framed as “oil products” are increasingly not actually made from crude oil. The methanol and derivatives being blended into the Chinese gasoline supply generally come from coal, while a meaningful portion of NGLs entering China are produced in US shale plays and never see the inside of a refinery distillation tower.2 This could pose an emerging demand-side risk for crude oil prices, since molecules of methanol and its derivatives—along with shale-sourced NGLs—are effectively displacing compounds formerly created by refining crude oil.

Methanol Blending and Derivatives Injecting Coal Into China’s Gasoline Pool

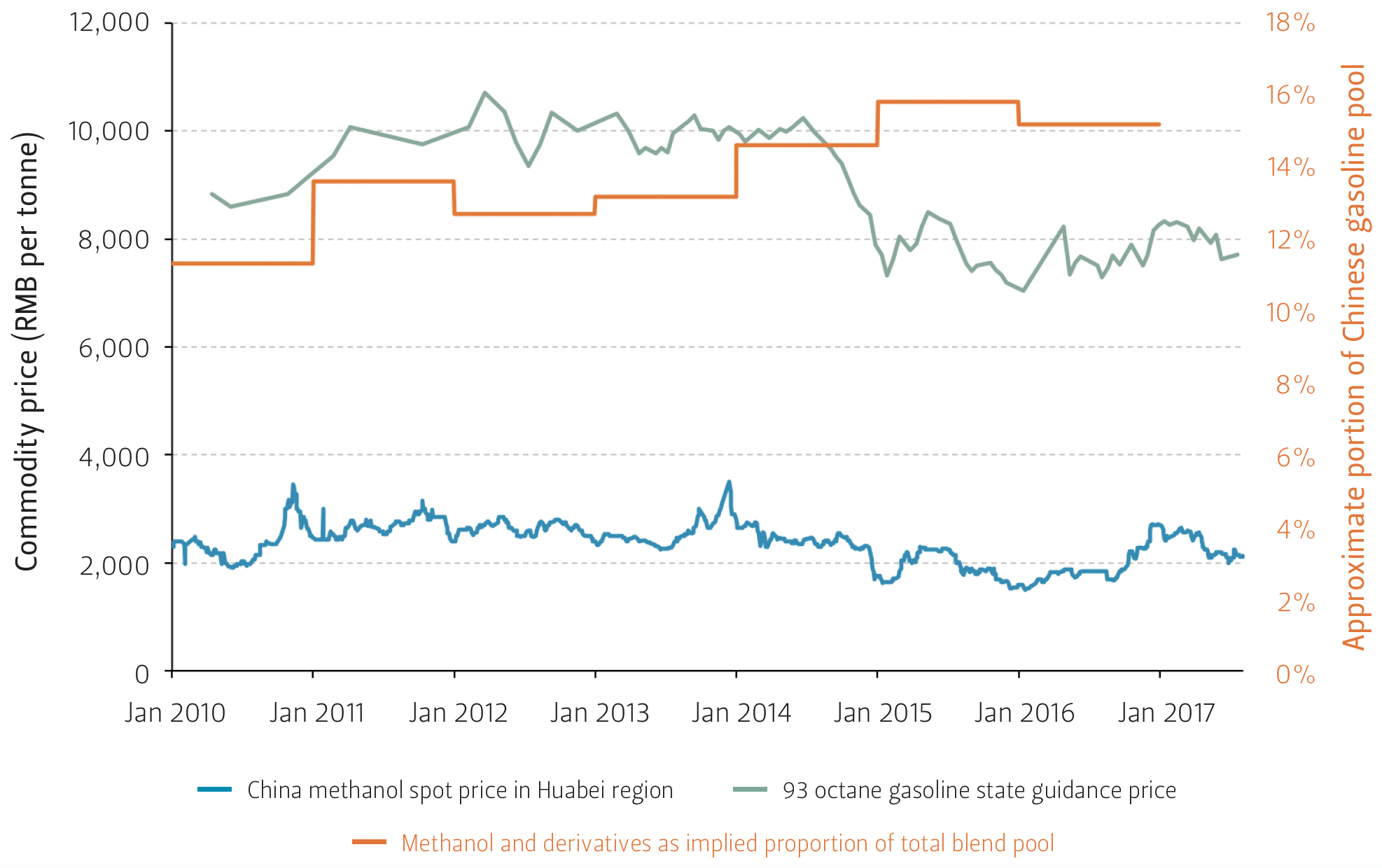

Figure 2 — Methanol and Derivatives Offer Cost Advantages to Gasoline Blenders in China, Now Account for Approx. 15% of Gasoline Pool

While the lion’s share of China gasoline supply comes from refining crude oil, an increasing proportion effectively comes from China’s coalfields in the forms of methanol and chemicals produced using methanol as a feedstock. Indeed, data from Argus Media suggest that more than 400,000 barrels per day (bpd) of China’s gasoline pool—which is currently about 3 million bpd in size—comes from methanol and its derivatives.3 Expressed in share terms, this means at least 15% of the country’s gasoline comes from methanol and methanol-derived compounds such as methyl tertiary butyl ether (MTBE) (Figure 2).

Methanol’s growing role as a gasoline constituent in China raises questions about possible new cross-commodity price relationships, since two-thirds of China’s domestic methanol production—which dominates overall supply—comes from plants using coal feedstock. The remainder comes from facilities that use coking gas (17% of total capacity) and natural gas (15% of total capacity) as feedstock.4

The rise in methanol blending appears primarily driven by (1) increasing octane ratings and decreasing gasoline sulfur content to meet new national quality standards in a cost-effective manner, (2) reducing oil import needs, and (3) providing an additional domestic industrial value-added activity by sustaining coal demand, as apparent consumption declines at the national level.

Regulatory changes are also facilitating increased use of methanol in gasoline across China. Sixteen Chinese provinces have issued local standards on methanol-blended fuel since 2004, the bulk of which focus on lower concentration blends such as M10 and M15 (i.e., 10% and 15% methanol by volume, respectively).5 The provinces with local methanol rules now include Fujian, Jiangsu, Liaoning, Shandong, Shanghai, and Zhejiang. These provinces contain roughly 30% of China’s entire private car fleet and are located on the coast, where they can potentially access price-advantaged methanol imports made from low-cost U.S. natural gas. Inland, together with those in Sichuan, drivers in the “coal patch” of Shanxi, Shaanxi, Ningxia, Gansu, and Qinghai own roughly 16 million private passenger cars. In all of these provinces, either methanol-gasoline blends are already for sale, or policymakers are seriously considering incorporating methanol into the local gasoline pool.

Data from Argus Media suggest that in 2016, roughly 200,000 bpd of methanol were blended into the Chinese gasoline stream, with another 200,000 bpd of methanol derivatives such as MTBE also being incorporated.6 As such, if we assume a baseline Chinese gasoline demand of approximately 3 million bpd, actual methanol accounts for 6–7% of the gasoline pool, with methanol derivatives contributing another 7% to total pool volume. As such, on a national level, the M15 era is already essentially here in the Chinese gasoline market, albeit in a derivative sense.

Moving forward, it is unclear whether the percentage of MTBE in Chinese gasoline will remain at current levels, if more of the Chinese population begins to have the same environmental and health concerns about MTBE that led to it being banned from the US market in 2006.7 If MTBE was to fall out of favor and be substituted with methanol— thus keeping the proportion of methanol and its derivatives in the gasoline pool closer to the current level—the crude oil demand displacement effect would likely be relatively muted. If, on the other hand, MTBE remains heavily used and blenders inject a large volume of neat methanol into the Chinese gasoline system, much more crude oil use could be displaced—especially if gasoline demand growth slows or stalls.

Two key factors will greatly influence the ultimate answer to these questions: First, how much more methanol can the Chinese car fleet accommodate without inducing maintenance problems that could prompt a driver backlash against higher-concentration gasoline-methanol fuel formulas? And second, can the areas in China with low-cost coal feedstocks— which are also often afflicted by water shortages—muster sufficient water supplies to accommodate additional methanol production? From a raw materials perspective, China’s coal reserves are more than capable of supporting a significant increase in methanol production, but water intensity poses tougher challenges. Researchers in China estimate that producing one tonne of methanol from coal requires 8.3 tonnes of water.8 In other words, it takes about 6.6 barrels of water to produce one barrel of methanol from coal.9

In contrast, data from Valero—the largest independent U.S. refiner and operator of one of the world’s most complex set of refining assets—show that processing a barrel of crude oil requires 0.4 to 1.2 barrels of water, depending on refinery complexity and on-site hydrogen production activity.10 Sinopec, which has the largest and arguably most sophisticated refinery footprint in China, refined 236 million tonnes of crude oil (approximately 4.72 million bpd) and produced 56.36 million tonnes of gasoline (approximately 1.30 million bpd) in 2016.11 As such, it can reasonably be assumed that China’s large refiners process 4 barrels of crude oil for every barrel of finished gasoline produced. Using the Valero data, this suggests each barrel of gasoline in China likely requires in the neighborhood of 5 barrels of water to produce. This is approximately 25% less water per unit of fuel than the amounts coal-based methanol plants will typically use.

China’s largest refineries tend to be located in water-abundant coastal areas, whereas the central Chinese coal patch (a likely location for methanol producers seeking proximity to coal feedstock) is generally much drier. If the Chinese leadership seeks to promote the use of methanol but reduce competition for scarce inland water resources, one possible solution would entail building coal-to-methanol plants in wetter coastal areas and transporting the coal to those plants, since water is the greater limiting factor. To boot, with the exception of Sichuan, China’s largest gasoline markets are located in the populous, wealthier coastal zones such as Guangdong, Jiangsu, Shandong, and Zhejiang.

China’s Petrochemical Makers Tap U.S. Shale Boom

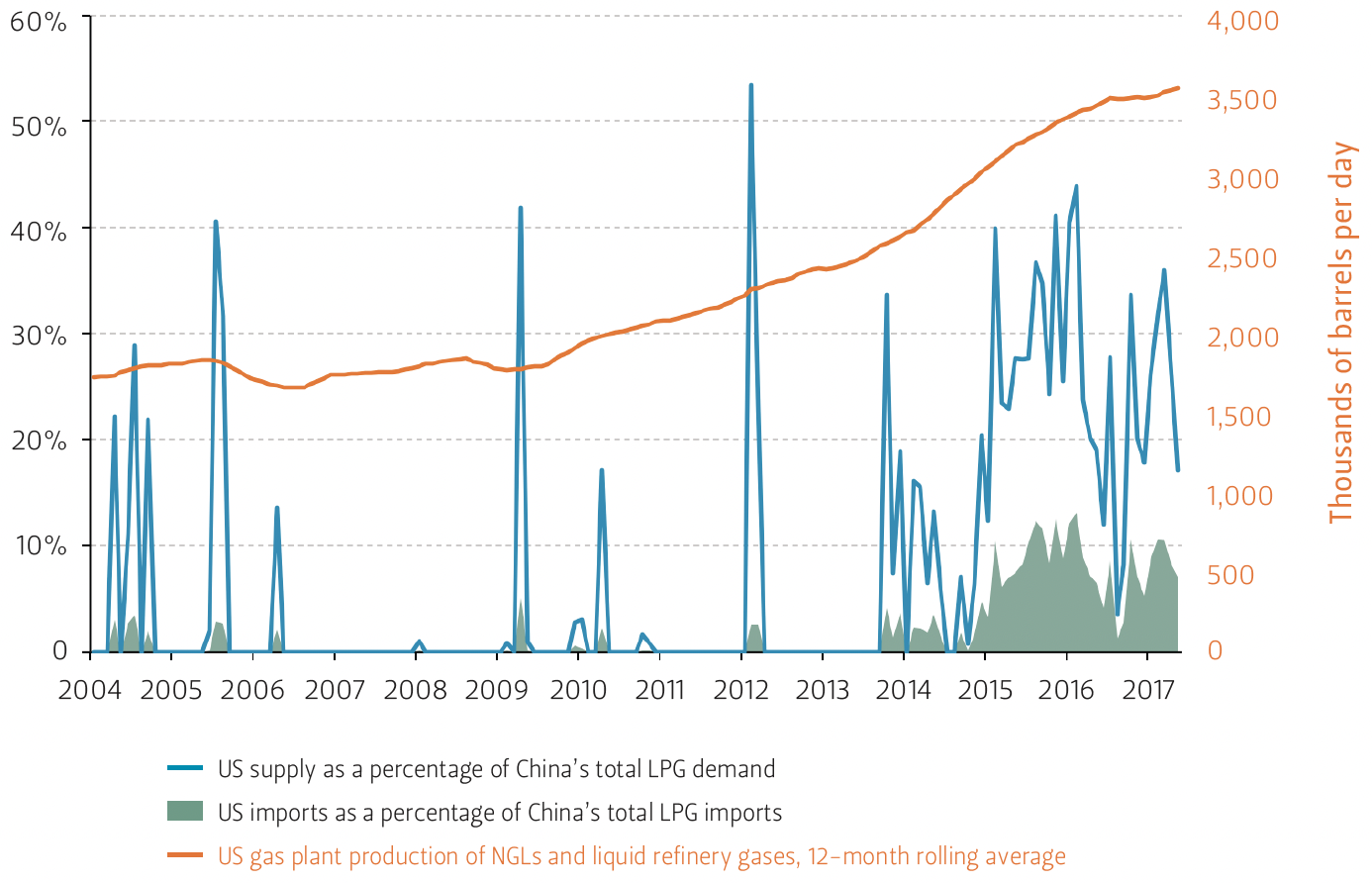

Figure 3 — China LPG Imports From the U.S.

In a twist that vividly illustrates how the US shale boom has reshaped global NGL and gas procurement strategies, the United States now accounts for a significant portion of China’s liquefied petroleum gas (LPG) imports, sometimes exceeding 40% of the country’s total imports in a given month (Figure 3). Much of the country’s LPG supply used to come from domestic refinery operations and was derived from crude oil.

LPG supplies from the US, however, come directly or indirectly from shale plays and thus bypass the refinery. Large-scale exports of LPG from the US only became possible with the advent of shale gas production. This means US NGL producers across plays such as the Marcellus, Utica, and Permian now effectively underwrite a significant portion of China’s imported petrochemical feedstock, as well as some degree of gasoline-blending components.12 And the entire process happens with the exported hydrocarbons bypassing the distillation towers of a traditional oil refinery.

Much of China’s LPG imports from the US come under term deals, such as the one Sinopec signed with Phillips 66 in early 2014.13 Chinese petrochemical plants’ willingness to bind themselves to multiyear contracts with parties from the US is notable because it is occurring despite rising geopolitical tensions between Beijing and Washington, D.C. To illustrate a potential contrast, consider the recent upswing in purchases of US crude oil made by PetroChina and Sinopec, which are being conducted primarily through spot market deals and generally appears to be an opportunistic move to capitalize on ample global supplies.14

Most likely, the disparity between China’s crude and LPG sourcing approaches reflects two fundamental factors: (1) the US market is structurally long on LPG while the country remains a large net crude oil importer, making long-term supply agreements more feasible; and (2) even if LPG supplies were to be disrupted by political events, the resulting problems would tend to be issues of private economic losses rather than threats to core national security, since plastic production for consumer goods is generally a much less strategic activity than the production of liquid fuels.

Strategic Implications

Oil producers—whether in Riyadh, Moscow, or the Permian Basin—should take stock of how China’s growing use of “oil products” that do not actually come from crude oil and instead bypass the refinery may translate into effective reductions in demand and prices for the crude oil they produce.

There is an increasing risk that petroleum products that bypass the refinery may coincide with political factors to drive China’s crude oil demand toward the low-demand scenario the author posited in a previous paper published in September 2016: average annual demand growth of 1.9% between 2016 and 2020.15 As expressed in that study, “China has simultaneously become a core driver of global oil demand growth while also fueling this growth through the construction of a debt-based, increasingly unsustainable economic structure.”16 If Chinese drivers fill their tanks with more methanol and Chinese petrochemical plants use more shale-sourced NGLs, global benchmark oil prices could be trapped between $45 and $55 for at least 24 months to come, because no other consumer country can currently deliver consistent incremental crude oil demand growth on the same scale as China.

Endnotes

1. NGLs are important feedstocks for China’s burgeoning petrochemical industry, as they are used to make ethylene and propylene—the building blocks of polyethylene and polypropylene, the world’s two most widely consumed plastics. China’s demand for propane has been especially robust, with the activation of multiple propane dehydrogenation plants that produce propylene for use as a petrochemical and polymer feedstock. Butane, another NGL, is also increasingly in demand as a gasoline-blending component, as China implements its National Phase 5 gasoline quality standard. See, for instance, “Chinese propane imports to rise in Q4 on startup of two PDH plants,” S&P Global Platts, September 21, 2016, https://www.platts.com/latest-news/oil/singapore/chinese-propane-imports-to-rise-in-q4-on-startup-27672803; and “China LPG imports may reach 20 mil mt in 2017 on strong petrochemical demand: Sinopec,” S&P Global Platts, March 21, 2017, https://www.platts.com/latest-news/petrochemicals/singapore/china-lpg-imports-may-reach-20-mil-mt-in-2017-26690201.

2. The raw associated gas stream from producing wells is generally first processed at plants located in or near the producing basin to remove methane (i.e., what most people think of as “natural gas”). The mix of compounds left over after methane is removed is referred to as “y-grade” or “raw make” and consists of heavier molecules such as ethane, propane, butane, and natural gasoline. Raw make is typically transported by pipeline to centralized fractionation plants often located along the Gulf Coast, where the mixed NGLs are isolated into each component fraction using absorption with a solvent (to capture heavier NGLs) and cryogenic expansion (to capture ethane). See, for instance, “Operations,” Targa Resources, accessed August 21, 2017, http://www.targaresources.com/operations/logistics-marketing/storage-terminaling/fractionation-and-treating-facilities; and “Oil & Gas: Natural Gas Processing: NGL Processing,” Maverick Engineering, Inc., accessed August 21, 2017, http://www.maveng.com/index.php/business-streams/oil-gas/natural-gas-processing/ngl-extraction-fractionation.

3. “China’s use of methanol in liquid fuels has grown rapidly since 2000,” Energy Information Administration, February 23, 2017, https://www.eia.gov/todayinenergy/detail.php?id=30072.

4. Peter Gross, “China’s use of fuel methanol and implications on future energy trends,” Washington Methanol Policy Forum, June 13, 2017, http://www.methanol.org/wp-content/uploads/2017/06/Peter-Gross-Global-Methanol-Fuel-Blending-Initiatives-Panel.pdf.

5. “Methanex Investor Presentation,” Methanex, June 2017, https://www.methanex.com/sites/default/files/MEOH%20June%202017%20single%20slide% 20per%20page.pdf.

6. “China’s use of methanol in liquid fuels has grown rapidly since 2000,” Energy Information Administration, February 23, 2017, https://www.eia.gov/todayinenergy/detail.php?id=30072.

7. “TIMELINE: A very short history of MTBE in the US,” ICIS, July 5, 2006, https://www.icis.com/resources/news/2006/07/05/1070674/timeline-a-very-short-history-of-mtbe-in-the-us/.

8. Jin Yong, Yan Binhang, Chu Bozhao, and Cheng Yi, “Develop Coal Chemical Industry In A Moderate And Orderly Way Under The Principles Of High Efficiency, Clean Conversion And High Added-value” (research paper, Department of Chemical Engineering, Tsinghua University, Beijing, China, 2012), 1-6, http://en.cnki.com.cn/Article_en/CJFDTOTAL-MHGZ201205002.htm.

9. Calculated as follows: (333 gallons of methanol per tonne) / (42 gallons per barrel) = 7.93 barrels of methanol per tonne. 8.3 tonnes of water to produce 1 tonne of coal-derived methanol = 1.05 tonnes of water per barrel of methanol. Water mass = (8.3 pounds per gallon) * (42 gallons per barrel) = (348.6 pounds per barrel) / (2204 pounds per tonne) = 0.16 tonnes per barrel of water, or 6.32 barrels of water per tonne. Finally, (6.32 barrels of water per tonne) * (1.05 tonnes) = 6.62 barrels of water. See “Methanol FAQs,” Southern Chemical Corporation, http:// www.southernchemical.com/wp/safety-environment/frequently-asked-questions; see also Han Hao, Zongwei Liu, Fuquan Zhao, Jiuyu Du, and Yisong Chen, “Coal-derived Alternative Fuels For Vehicle Use In China: A Review,” Journal of Cleaner Production 141 (2017): 774-90, https://doi.org/10.1016/j.jclepro.2016.09.137.

10. “Water Reuse/Recycle…What does it mean for Refiners?” Valero, July 18, 2014, http://www.weat.org/Presentations/2014WRA_B-11%20GARRISON.pdf.

11. See Sinopec’s 2016 Form 20-F Report, available at http://www.sinopec.com/listco/en/Resource/Pdf/2017042601.pdf. Crude oil tonnage was converted to barrels at a ratio of 7.3 barrels per tonne; gasoline data was converted at 8.45 barrels of gasoline per tonne (http://www.cmegroup.com/tools-information/calc_refined.html).

12. Between 2008 and 2016, OPEC producers added 1.8 million bpd of incremental NGL supplies, while US producers increased NGL output by 1.7 million bpd during that same time period. However, between 2014 and 2016, OPEC producers brought only 200,000 additional bpd of NGL onto the market, while US producers added 500,000 bpd of NGLs as unconventional output accelerated. See OPEC 2011 and 2014 Annual Reports, available at http://www.opec.org/opec_web/en/publications/337.htm; OPEC August 2017 Monthly Oil Market Report, available at http://www.opec.org/opec_web/static_files_project/media/downloads/publications/OPEC% 20MOMR%20 August%202017.pdf; and “U.S. Gas Plant Production of Hydrocarbon Gas Liquids,” EIA, accessed September 6, 2017, https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MNGFPUS2&f=A.

13. “Sinopec Buys LPG from Phillips 66 as Chinese Tap U.S. Shale Boom,” Reuters, March 14, 2017, http://www.reuters.com/article/sinopec-phillips-66-lpg-idUSL3N0MB3FT20140314.

14. “Analysis: China's record US crude imports to give OPEC more sleepless nights,” S&P Global Platts, July 27, 2017, https://www.platts.com/latest-news/oil/singapore/analysis-chinas-record-us-crude-imports-to-give-27860829?ito=793&itq=260a0437-5934-408e-98ab-d1a413d5f3cf&itx%5bidio%5d=63749.

15. Gabriel Collins, “China’s Evolving Oil Demand: Slowing Overall Growth, Gasoline Replacing Diesel as Demand Driver, Refined Product Exports Rising Substantially” (working paper, Rice University’s Baker Institute for Public Policy, Houston, Texas, September 30, 2016), https://www.bakerinstitute.org/media/files/files/e0b5a496/WorkingPaper-ChinaOil-093016.pdf.

16. Ibid.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.