In 1999, small business was growing at around 5% per year in real terms.1,2 The small business sector accounted for about 40% of the overall U.S. economy and was contributing 2% to U.S. gross domestic product (GDP) growth.3 This growth is achievable again today.

Small business owners have repeatedly said that the lack of debt financing is preventing their growth.4 At the same time, community banks—which have the closest relationships with small business and are best able to assess their risks and returns—have suffered disadvantages under regulation for decades and were disproportionately hit by the 2008 financial crisis. Changing community banking regulation could unleash the power of free enterprise and put America back on the path to prosperity.

What Is a Small Business?

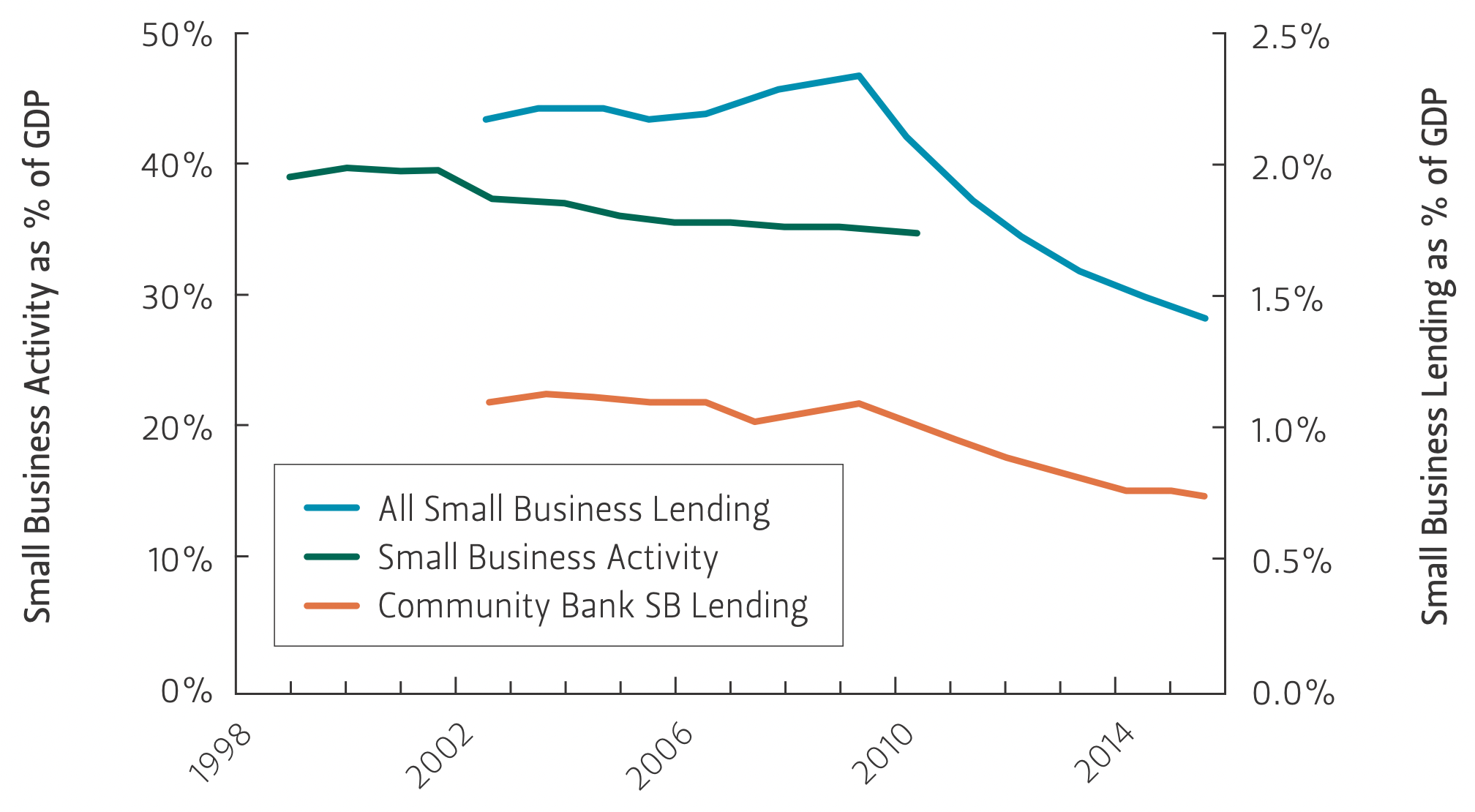

Figure 1 — Small Business and Its Lending as a Percentage of U.S. GDP

A small business is a firm with fewer than 500 employees.5 In 2011, the United States 40% 2.0% had almost 5.7 million small businesses, representing 99.7% of all U.S. employer firms.6 These firms employed 48% of the nation’s labor force. Most small businesses are truly small: Over 60% have zero to four employees, and more than 90% have fewer than 20 employees. Small business has a 10% 0.5% meaningful representation in every sector of the U.S. economy except for mining and utilities. Any American can become a small business entrepreneur.

Small Business in Decline

Before the turn of the millennium, small business produced a greater contribution to U.S. GDP than large business. In the seven years leading to the 2008 financial crisis, small business GDP contribution fell to around 46% of non-farm private sector economic output. In real terms, small business GDP went from just under $5.2 trillion in 2000 to just over $5.4 trillion in 2007.7 Annual average real growth was around 1% during these 7 years.

The 2008 financial crisis made matters considerably worse. The average real growth rate of small business from 2008 to 2010 was -1.5%. Data is not available for the past five years.8

Uncompetitive Banks

The loan market share of the top 10 banks increased from 30% in 1980 to 50% in 2010.9 It may now exceed 60%. In 2002, 9,466 banking institutions were lending to small business.10 This year there are just 6,058, and the vast majority—more than 92%—are community banks. Only 456 other banks are active in small business lending in the U.S. today.

Community banks do not have the economies of scale or the diversity of scope of large banks. They have been in decline for decades.11 As a consequence, the small business loan market has dramatically decreased in real terms. This year’s $286 billion of loan activity is 30% below the value of the market a decade ago adjusting for inflation.

The Small Business Administration

The Small Business Administration (SBA) was founded in 1953. Enabling access to capital for small business is a crucial part of its core mandate. The SBA requested a total budget of $860 million in 2016. Of this amount, just $3.3 million was set aside to subsidize small business loans provided through private banks under the 7a loan guarantee program.12 SBA reform should be a priority for the new administration.

Less Taxes vs. More Lending

Lowering corporate tax rates would likely stimulate small business growth. However, increasing access to loans is a more effective solution:

- A tax reduction is more of today’s money tomorrow, whereas a loan is tomorrow’s money today. Debt capital allows immediate investment in growth.

- Professionally assessed loans pay for themselves. The government does not need to forgo spending, or increase the deficit, to finance them.

- Universal corporate tax reductions do not target growth from small business. Constraints on tax reductions may create perverse incentives that undermine growth.

- 100% of a loan is often used to capitalize a firm for growth. A reduction in corporate taxes may lead to increased dividends, one-off consumption, etc.

- Competitive loans provided by knowledgeable local professionals will flow to small businesses that offer the best risk-return trade-off first; loans select for growth.

The federal government will need a nuanced approach to properly stimulate small business growth. However, a core focus should be on creating a level playing field for community banks to compete to provide small business loans. With growth- oriented investment coming from local, knowledgeable professionals, the U.S. could see 2% GDP growth from its small business entrepreneurs again.

Endnotes

1. Research assistance provided by Dylan Dickens.

2. Small business economic data from SBA. Urban, unchained CPI data from the Bureau of Labor Statistics.

3. U.S. GDP data from the World Bank.

4. See, for example, Bank of America (2015), “Small Business Owner Report”; Wells Fargo (2016), “Small Business Survey”; and Federal Reserve Banks of New York, et al. (2014), “Joint Small Business Credit Survey Report.”

5. U.S. Department of Commerce

6. Small business size, sector data from the Small Business Administration.

7. Real amounts in 2010 U.S. dollars.

8. There is no up-to-date data on small business GDP contributions. The Bureau of Economic Analysis has requested funds from Congress to address this.

9. D. Corbae, P. D’Erasmo, “A Quantitative Model of Banking Industry Dynamics,” 2013.

10. Small business lending data from FDIC.

11. Since 1994, changes to banking regulation have almost all favored large banks.

12. FY2016 Congressional Budget Justification, SBA. Note that $153 million will be used in the 7a program’s administration.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.