Houston is experiencing renewed interest in fostering a high-growth, high-technology (HGHT) entrepreneurship ecosystem.1 Venture capital—typically associated with equity-based investments into nascent startups—is a crucial component of any HGHT ecosystem. In this issue brief, we explore the extent and nature of venture capital in Houston as compared to investment at the national level, and explain why one particular type of venture capital is vital to Houston’s future.

What Should Count as Venture Capital?

Venture capital (VC) activity is frequently measured in three ways: total amount of investment, number of investment rounds, and number of deals made. In the academic literature,2 a deal means the first venture capital investment into a startup firm. Once a startup receives venture capital funding, it is said to be venture capital backed (VC-backed). While some startups fail after the first or second round of investment, a successful startup will receive multiple rounds of investment from a broad array of investors. A successful startup stops being VC-backed at its liquidity event, which is typically an initial public offering (IPO) or a lucrative acquisition.

Houston by the Numbers

By our calculation, Houston VC-backed startups received a total of $72 million across 18 rounds of investment in 2016, but only six of these were new deals.3 For 2015, we estimate that $92.7 million was invested across 17 rounds and eight deals.

A report released by Accenture in 2017 estimates that $161 million in venture capital was invested in Houston in 2015 across 29 rounds, of which 21 were classified as seed, early, or late-stage startup rounds.4 Despite the differences between Accenture’s numbers and our own, each could be considered correct: we are each counting different things.5 The stage of development of companies at the time they received their investment and the rationale for the investment, as well as, to an extent, the source of the investment, matter. Below, we examine these issues and why they are important for Houston, Texas.

Growth vs. Transactional Venture Capital

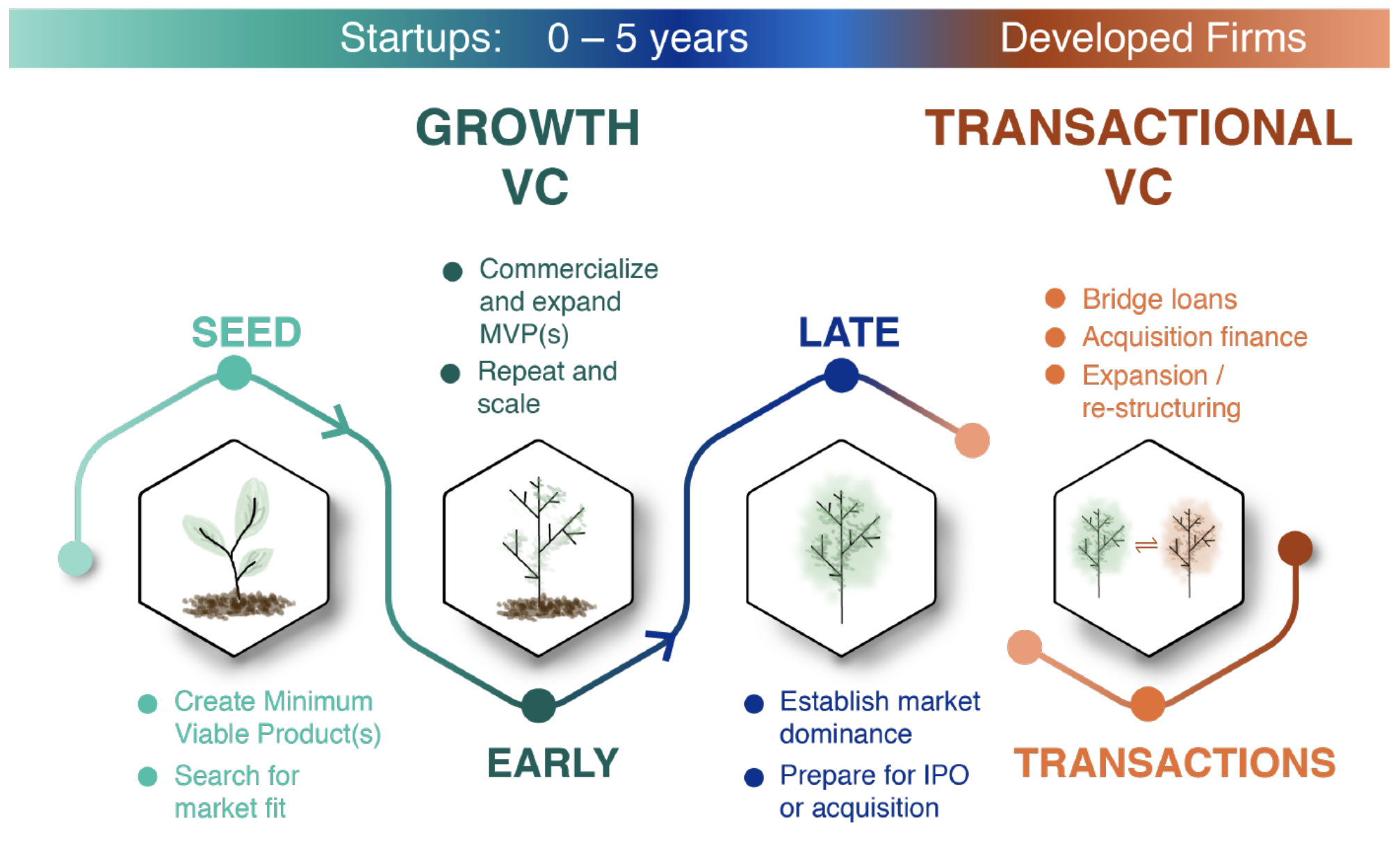

Venture capital investments can be classified as either growth VC or transactional VC investments.

Growth VC is an investment made at the seed, early, or later stages of an HGHT startup’s lifecycle. This investment is made with the objective of growing a firm from an idea to one capable of being listed on a stock exchange or bought by an established incumbent. New ventures that are capable of this kind of rapid growth are concentrated in a small number of industries, particularly information technology (IT) and biotechnology.

Beginning in the early 2000s, venture capitalists started using their expertise to provide transactional investment to non-HGHT firms as well as startups. Transactional VC is a private equity investment in companies in need of funding for expansion, new-market entry, operations restructuring, or other large-scale corporate finance needs, including bridge loans before an initial public offering or investment to complete or undergo an acquisition. Many recipients of transactional VC have never received growth VC. For example, venture capitalists participated in more than 95 percent of all U.S. IPOs and acquisitions by publicly traded firms in 2015, but did not invest growth VC in the vast majority of them.6 Including transactional investments with growth investments overestimates the finance flowing into HGHT entrepreneurship ecosystems. Figure 1 illustrates the differences between growth and transactional venture capital.

Figure 1 — Growth vs. Transactional Venture Capital

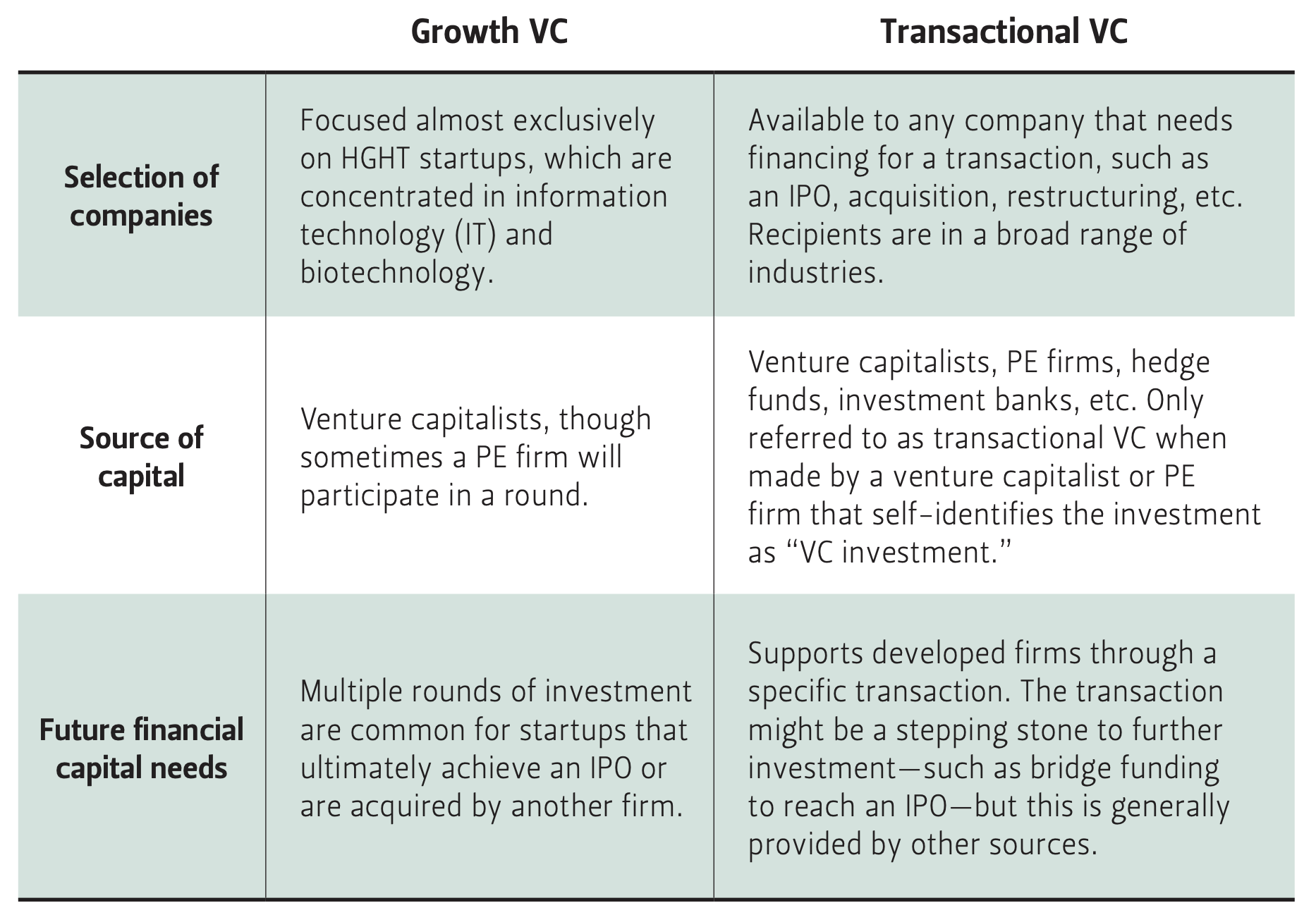

Private Equity vs. Venture Capital

Private equity (PE) firms further complicate the differentiation between growth and transactional capital, particularly because some data sources mix private equity and venture capital investments together.

Traditional private equity firms focused on leveraged or management buyouts of publicly traded firms. In the 1980s, PE firms would provide capital to buy listed firms off of stock exchanges with the intention of restructuring and refocusing them, before making a new public offering under new management or with a new ownership structure. But modern PE firms primarily invest in privately held firms instead.7 These investments are seldom in HGHT companies; their target companies tend to be large and established, and in traditional sectors like energy, real estate, manufacturing, transportation, and retail.

However, private equity firms also make investments on the secondary market, buying stock from other PE firms and from venture capitalists. And they sometimes make direct (generally later stage or transactional) investments into privately held companies, some of which are VC backed. In such cases, they are most likely to participate as co-investors or for a single round. When they do participate in HGHT startups, they mostly provide transactional investment. Table 1 summarizes the differences between growth and transactional “venture” investments.

Growing an HGHT Ecosystem

Simply put, growth venture capital is crucial to an HGHT startup ecosystem, and transactional venture capital is not. Transactional VC may assist mature HGHT startups, but startups can, and frequently do, go from later stage VC directly to liquidity events. In addition, cities that have large amounts of transactional VC and little to no growth VC cannot sustain HGHT ecosystems. In these cases, the transactional VC is either going to non-HGHT firms, or the ecosystem only has HGHT firms that are at the end of their lifecycle and features little new startup activity.

We assess Houston through this lens: we analyze growth venture capital and transactional venture capital in the city using data from 1998 to 2016, and compare Houston’s results to national trends.

Table 1 — Differences Between Growth VC and Transactional VC

National Growth VC

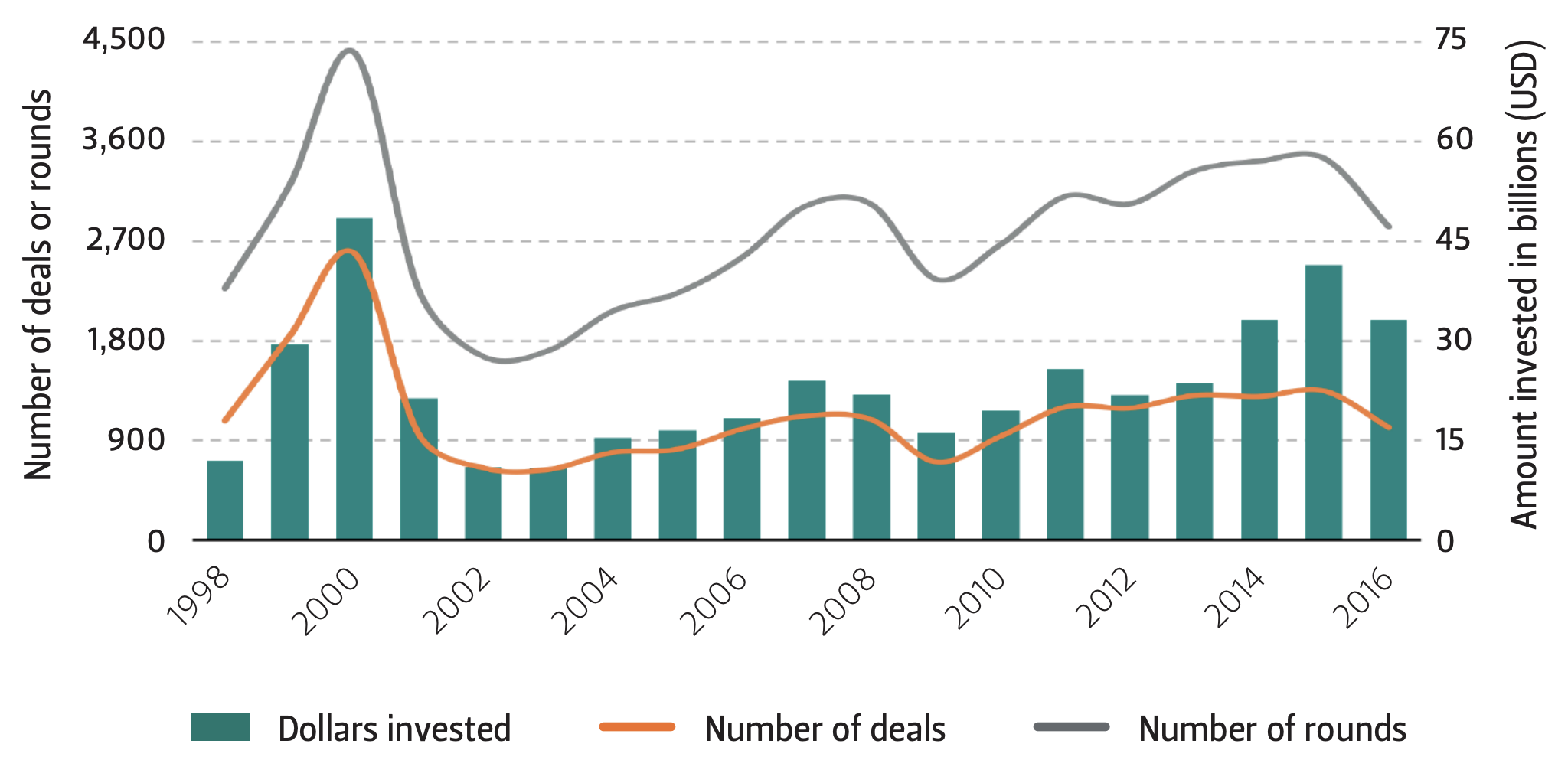

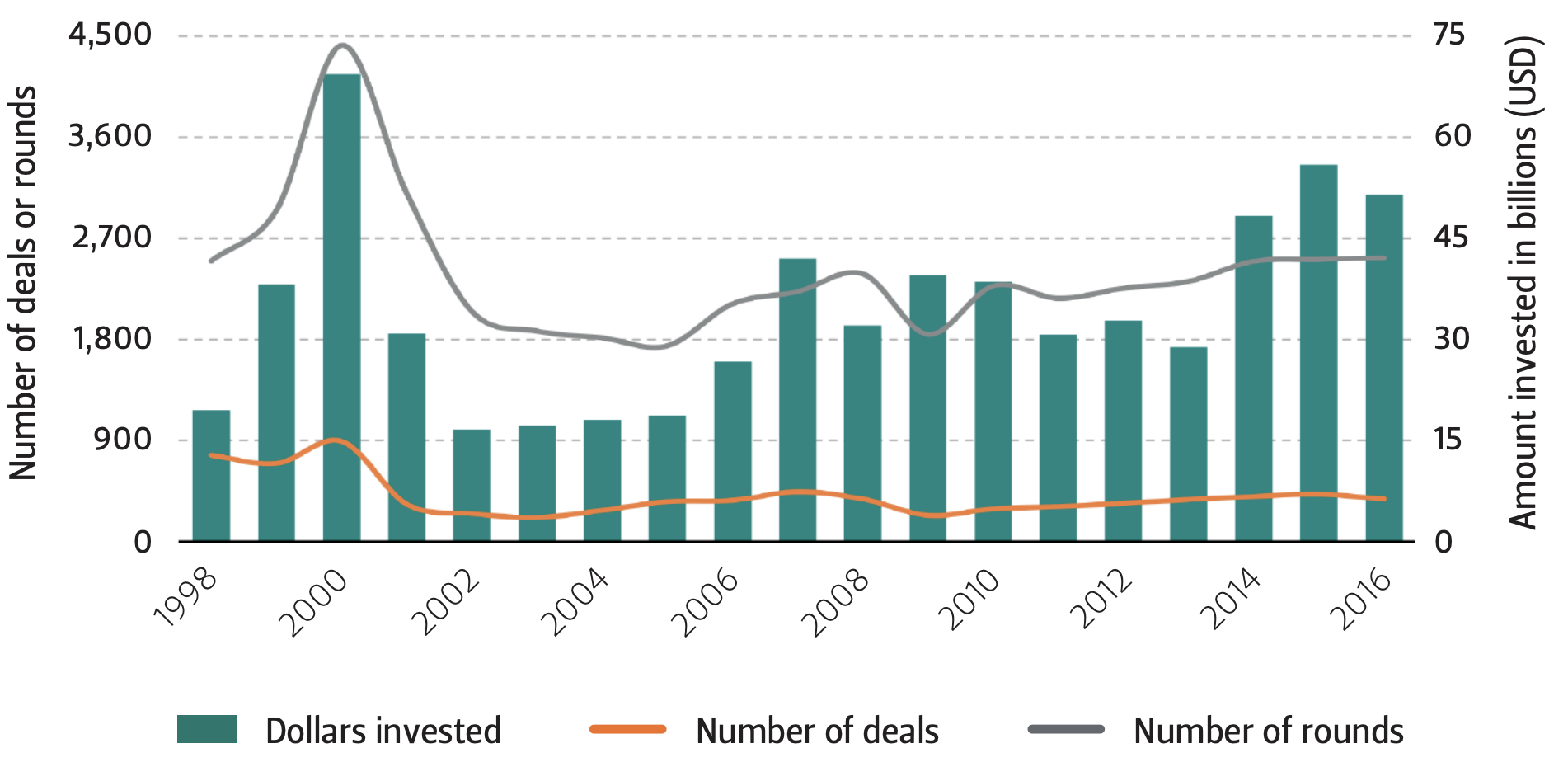

Figure 2 shows growth VC investment into venture-backed startups in the United States from 1998 to 2016. The green bars represent the total dollars invested in nominal amounts (i.e., not adjusted for inflation), the grey line shows the number of rounds of investment, and the orange line shows the number of new deals.

The peak of venture capital investment took place in the year 2000, at the height of the dotcom bubble. By the end of 2001, the majority of publicly traded dotcom companies had folded, and trillions of dollars of market capitalization had vanished.8 The unusual peak in 2000 was driven by an oversupply of VC and led to a significant decline of venture capital activity in the years that followed. A steady recovery then took place until declines in 2009 and 2010, which were affected by the 2007 global financial crisis,9 before resuming. VC investment is now approaching year 2000 levels, but with the supply and demand of venture capital in apparent balance.

Despite the great recession of 2007, U.S. growth VC investment nearly doubled from 2006 to 2016, with an 81 percent increase in nominal terms. This overall steep upward trend was marked by two peaks, one in 2011 of $25.6 billion, and one in 2015 at over $41.4 billion. Totals for 2017 appear poised to approach or match 2015 levels.10 The number of rounds also averaged 3,000 per year between 2006 and 2016, and both deals and total number of rounds showed a moderate-to-strong growth trend during that period.

Houston's Growth Venture Capital

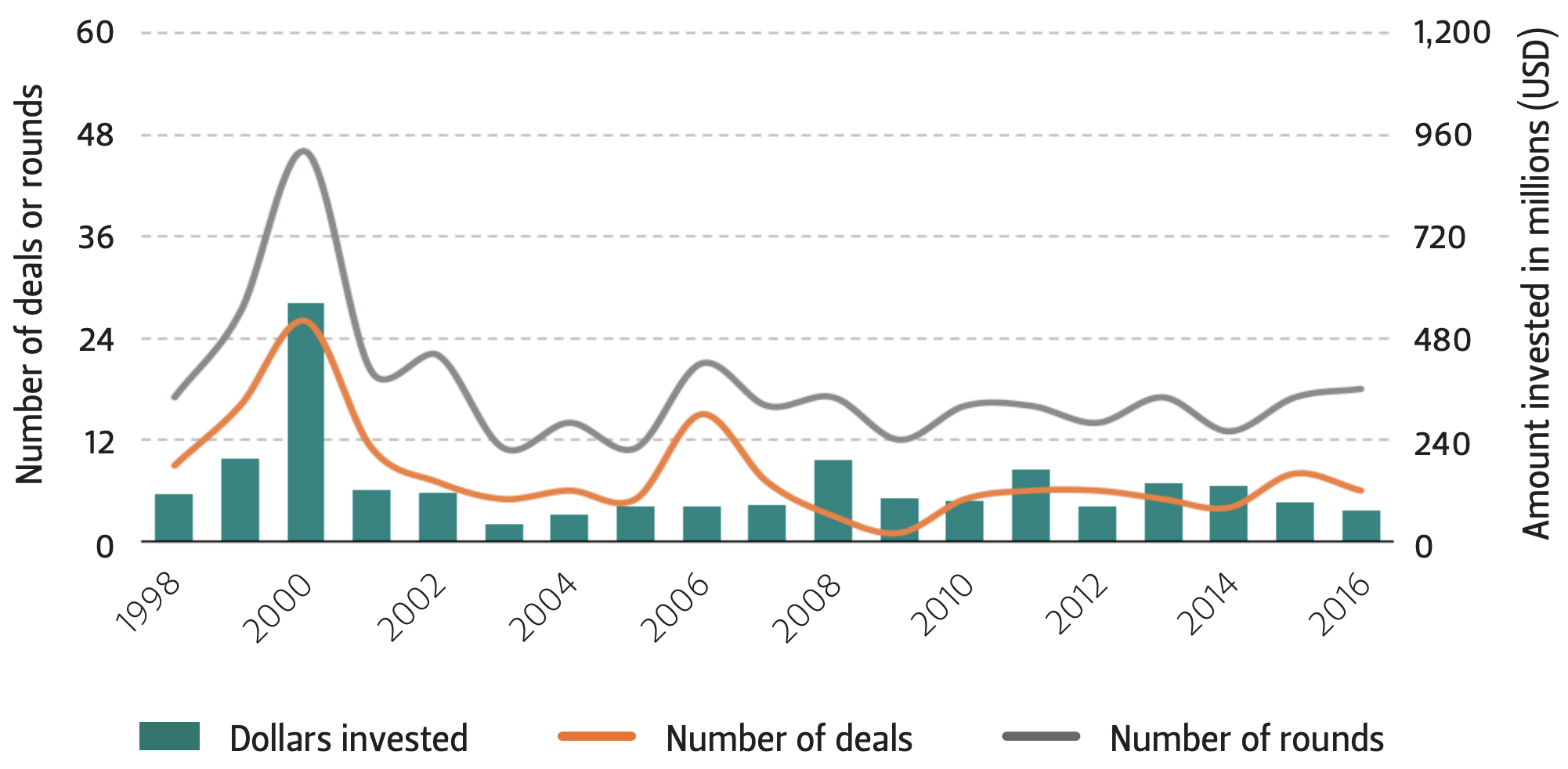

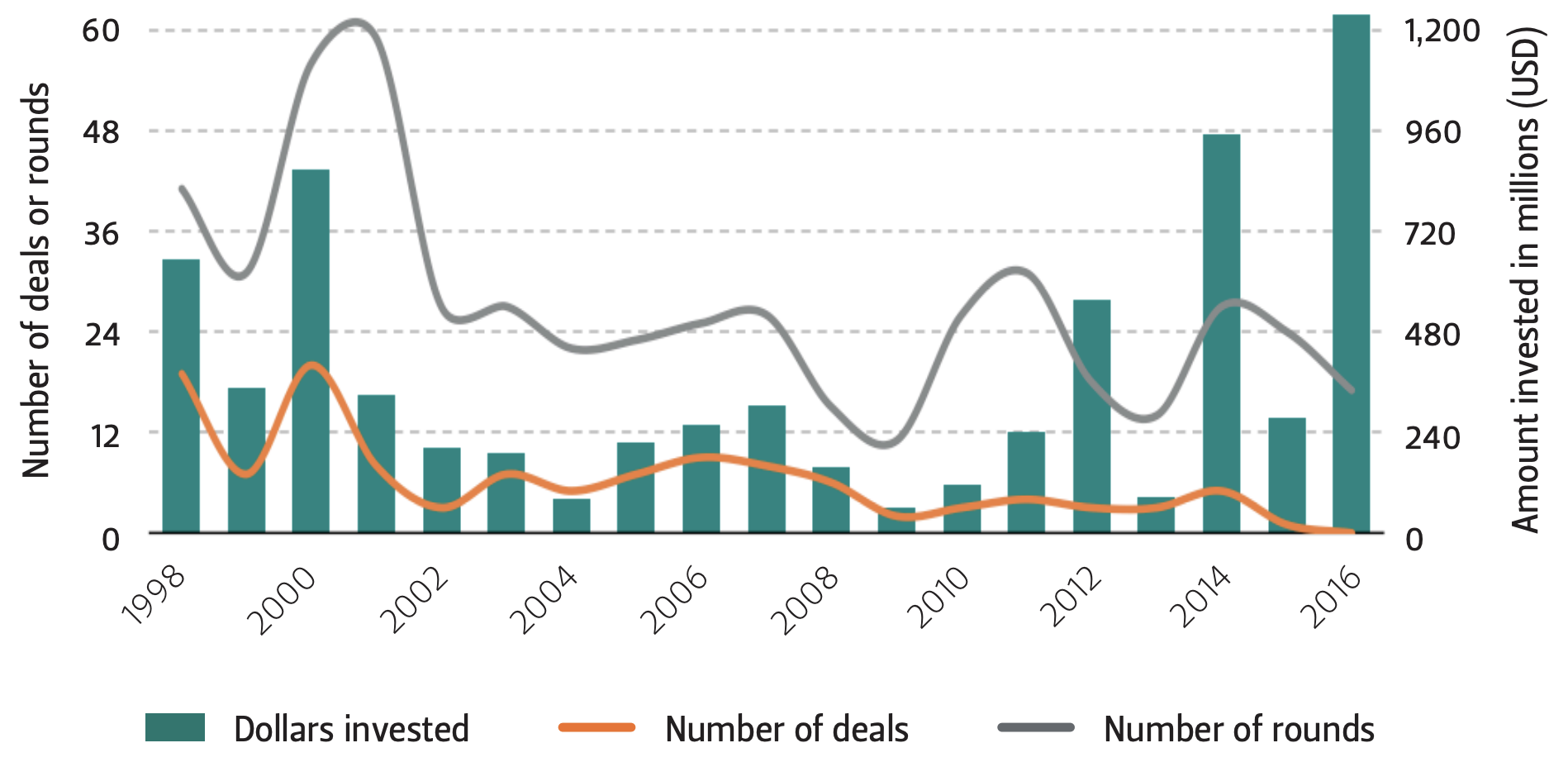

From the late 1990s through the mid2000s, Houston appears to have followed the national trends, albeit on a reduced scale (Figure 3). For the last decade, though, Houston deviated substantially from the national pattern. While venture capital investment across the country is growing back to year 2000 levels, Houston has flatlined.

In 2006, Houston’s total venture capital investment was $83 million. By 2016, there was just $72 million in VC investment; Houston ended the last decade with 13 percent less VC investment than when it started. Moreover, these investment amounts are in nominal dollars. In 2016 dollars, Houston’s venture investment fell from $100 million to $72 million—a 28 percent decrease.11

Figure 2 — U.S. National Growth Venture Capital

Houston’s venture capital investment shows a great degree of volatility, with promising peaks followed by dramatic falls. This is a trend commonly seen in nascent ecosystems that have not achieved a critical mass of startup companies.12 Houston recorded an overall high of $192.7 million in VC investment for 2008, followed by a 46 percent decline the next year to $103.2 million. While this decrease could be partly attributed to the 2007 global financial crisis, the drop in national investment is much more muted.13 Further, Houston demonstrated the same pattern in 2011, with a peak of $168.6 million followed by a 52 percent decrease in 2012 to $81.5 million.

Figure 3 — Houston Growth Venture Capital

Houston’s venture capital investment in 2016 was around half the amount invested in 2013 and 2014. It would be tempting to attribute this to the collapse of oil prices in late 2014,14 as Houston’s economy is heavily focused on oil and gas, but HGHT startups are seldom in the oil and gas sector.15

Shut Out of the Future?

Overall, Houston’s trajectory in venture capital dollars invested is best described as flat or a weak inverted U. The city’s trend in new deals and rounds is similar, ranging between four and eight per year.

Houston ranked 39th in The Top 100 U.S Startup Cities for 2016 Report,16 down from 21st in 2006. Much of this drop comes from the rise of other cities, so Houston’s fall is a relative one. But Houston is still the only former top 25 city to have less venture capital investment today than it did a decade ago.17 With less than 1 percent of U.S. venture capital now flowing into Houston—the fourth-largest U.S. city by population and sixth-largest metro area by GDP—and with HGHT firms driving U.S. economic growth and prosperity,18 Houston risks being shut out of America’s future innovative economy.

National Transactional Venture Capital

There has been a clear upward trend in transactional venture capital at the national level following the dotcom crash (see Figure 4). The total dollars invested have increased by 93 percent in the last decade, rising from nearly $26.6 billion in 2006 to around $51.4 billion in 2016. The fall from $42 billion in 2007 to $32 billion in 2008 might be associated with the financial crisis, and the recent peak of nearly $55.8 billion invested in 2015 came close to levels in 2000.

Transactional VC tends to involve fewer rounds with larger investments than growth VC, since the recipient firms are typically well-established and seeking substantial financing. The greater number of rounds per deal is due to the transactional nature of the rounds. Once a firm builds a relationship with an investor, it may require a bridge loan followed by a convertible note to make an acquisition, and so forth. The number of rounds of growth VC a startup can receive is limited by the duration of a firm’s growth from its inception to its liquidity event.

Transactional VC in Houston

Transactional VC is far more dynamic and sizeable in Houston than growth VC. The average amount of growth VC in the city is around one-third of the average amount of transactional VC for the 10-year period from 2006 to 2016.19

Figure 4 — U.S. National Transactional Venture Capital

Transactional VC investment in Houston totaled $260.2 million in 2006 but rose to a staggering $1.25 billion in 2016 (see Figure 5). Houston’s transactional VC has trended upward, mirroring national results, but Houston’s levels rose 379 percent, compared to 93 percent nationally.

However, Houston’s transactional VC investment shows a great degree of volatility. In recent years, transactional investment has cycled on and off, with peaks in 2012 (at $561.9 million), 2014 (at $958 million), and the highest peak in 2016 (at $1.25 billion).

Figure 5 — Houston Transactional Venture Capital

Houston's Separate Worlds

Transactional VC and growth VC do sometimes overlap—especially when an HGHT startup takes transactional VC rather than a later round investment—but, particularly in Houston, they largely exist in separate worlds. Houston’s transactional VC is, unsurprisingly, prevalent in the oil and gas sector and has little if anything to do with HGHT startups.

Even within a venture capital fund that provides both growth and transactional investment, these different types of deals are usually handled by different partners and associates, as they require specialized expertise. There is, therefore, little hope of spurring growth VC by attracting transactional VC in general, and the transactional VC focus on energy firms makes this even less likely in Houston.20

Conclusion

The City of Houston has set the ambitious goal of joining the nation's top entrepreneurship ecosystems, creating 10,000 new technology jobs, and luring $2 billion in venture capital investment to Houston-based startups by 2022.21 These goals rely on growth venture capital, not transactional venture capital. With 2016 growth VC investment standing at $72 million for the city, Houston would need to increase its nominal investment by 75 percent year-on-year over the next six years to reach its goal. This simply isn’t feasible.22

There are two good reasons to believe that Houston will turn a corner, perhaps even in its 2017 totals: Houston’s pipeline of accelerator or incubator supported startups grew 1,189 percent from 2011 to 2016,23 and its current policy efforts (including various task forces,24 an innovation district,25 Houston Exponential,26 and a fund of funds)27 appear constructive. If these policy efforts work to enhance, rather than undermine, market forces, Houston’s growth VC investment should break out of its current ranges with a clear upward trajectory.

A realistic, but still aggressive, goal for Houston would then be around a 15 percent year-on-year increase in growth VC. This would allow Houston to reach around $170 million in growth VC invested, with perhaps 14 new deals and a stock of almost 80 actively funded VC-backed startup firms, by 2022. Houston would then likely become a top 25 U.S. city for HGHT startups, though its ecosystem would still be emerging and startups would remain a very small part of Houston’s economy. With yet another decade of sustained growth, Houston could finally join the set of other giant metropolises that are harnessing the power of this century’s driving force for American economic growth.

Endnotes

1. See Lydia DePillis, “Houston is Starting to Work on its Startup Problem,” Houston Chronicle, February 23, 2017. Retrieved from http://www.chron.com/business/texanomics/article/Houstonis-starting-to-work-on-its-startupproblem-10951608.php.

2. See, for example, Josh Lerner, “The Syndication of Venture Capital Investments,” Financial Management 23, no. 3 (1994): 16-27. However, from an investor’s perspective, a deal can mean the first investment in a startup firm. See, for example, Thomas Hellmann, Laura Lindsey, and Manju Puri, “Building Relationships Early: Banks in Venture Capital,” Review of Financial Studies 21, no. 2 (2008): 513-541.

3. The primary data used in this report comes from Thomson Reuters Corporation’s VentureXpert database.

4. See “Innovation in Houston: A Study of the Bayou City’s Startup Ecosystem,” Accenture and The Greater Houston Partnership, March 2017. Retrieved from http://www.houston.org/pdf/comm/Innovation-Accenture-Final-Report.pdf. Note that Accenture refers to rounds as deals.

5. Accenture counts some transactional VC and PE investments as late-stage growth VC investments, while this analysis counts transactional VC separately.

6. Data from Thomson-Reuters VentureXpert, SDC Mergers & Acquisitions, and Global New Issues. Weighting by transaction value, venture capitalists on average participated in 90 percent of all IPOs from 2010 to 2015 and in 93 percent of all disclosed mergers and acquisitions by U.S. publicly traded firms from 2006 to 2015.

7. In a sample of private equity recipients that had one or more patents, divisional and private-to-private investment outweighed public-to-private investments by an approximate 5.5 to 1 ratio. See Josh Lerner, Morten Sorensen, and Per Stromberg, “Private Equity and Long-Run Investment: The Case of Innovation,” Journal of Finance 66, no. 2 (2011): 445–477.

8. David Kleinbard, “The $1.7 trillion dot.com lesson,” CNN Money, November 9, 2000. Retrieved from http://money.cnn.com/2000/11/09/technology/overview/.

9. Venture capitalists typically raise 10-year funds and make the majority of their investments in their first five years of operation. This fundraising cycle gives rise to a delayed response to macroeconomic shocks.

10. Based upon the first three quarters of 2017 investment (not shown in the graph).

11. Consumer Price Index data from the U.S. Bureau of Labor Statistics.

12. Edward J. Egan, Anne Dayton, and Diana Carranza, The Top 100 U.S Startup Cities for 2016, Rice University’s Baker Institute for Public Policy, Houston, Texas, 2017.

13. The U.S. recorded nearly $22 billion in VC investment in 2008, followed by a 27 percent decline the next year to $16.1 billion.

14. See, for example, Clifford Krauss, “Oil Prices: What to Make of the Volatility,” New York Times, June 14, 2017. Retrieved from http://www.nytimes.com/interactive/2017/business/energyenvironment/oil-prices.html.

15. SURGE Ventures (an energy-focused Houston accelerator program), schooled 32 cohort companies in four cohorts before closing in April 2016. The Houston Technology Center (HTC) also incubated some energy-focused startups over the course of its 18-year life. The HTC became Houston Exponential in October 2017, and is refocusing its operations.

16. Egan, Dayton, and Carranza, The Top 100 U.S Startup Cities for 2016. Note that a single new deal, worth $3 million, was counted in this report (as growth venture capital from a private equity firm) but not counted in the Top 100 U.S. Startup Cities ranking. Counting it would not change Houston’s rank.

17. See Egan, Dayton, and Carranza, The Top 100 U.S Startup Cities for 2016.

18. See, for example, Edward J. Egan, The Key Driver of Economic Growth in the 21st Century: High-growth, High-tech Entrepreneurship. Rice University’s Baker Institute for Public Policy, Houston, Texas, 2017.

19. Houston's transactional VC averaged $388 million from 2006 to 2016, while the city’s growth VC averaged $113 million over the same period.

20. The flip side of this is that transactional VC probably does not crowdout growth VC.

21. See Andrea Rumbaugh, “Houston Exponential to Harness Startup Potential,” Houston Chronicle, October 24, 2017. Retrieved from http://m.chron.com/business/technology/article/HoustonExponential-to-harness-startup-potential-12300495.php.

22. At the state level, the most dramatic growth on record is New York state, which increased its nominal VC by just over 20 percent year-on-year between 2006 and 2015. The average nominal annual state-level growth rate of VC investment is around 7.5 percent. See Edward J. Egan and Rachel L. Garber, The State of Venture Capital in Texas, Issue Brief no. 03.07.16. Rice University’s Baker Institute, Houston, Texas, 2016.

23. See Edward J. Egan, Benjamin J. Baldazo, and Dylan T. Dickens, Creating a Pipeline for Startups in Houston, Texas, Rice University’s Baker Institute, Houston, Texas, 2016.

24. Houston Technology & Innovation Task Force, June 2017. Retrieved from http://www.houstontx.gov/council/4/Tech-andInnovation-Task-Force.pdf.

25. See Joe Martin, “Mayor Sylvester Turner Outlines Plans for Tech Innovation District,” Houston Business Journal, May 5, 2017, Retrieved from https://www.bizjournals.com/houston/news/2017/05/05/mayor-sylvester-turner-outlines-plans-fortech.html.

26. See “New Organization to Drive Houston’s Innovation Economy,” Houston Technology Center, October 24, 2017. Retrieved from https://www.houstontech.org/latest_news/announcing-houstonexponential/.

27. See “Houston Launches its First Venture Capital Fund of Funds,” Global Newswire, October 24, 2017. Retrieved from https://globenewswire.com/newsrelease/2017/10/24/1152597/0/en/HoustonLaunches-its-First-Venture-Capital-Fundof-Funds.html.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.