Author(s)

This testimony was delivered before the U.S.-China Economic and Security Review Commission on April 4, 2013. Read Lewis' prepared testimony here.

Video of the testimony is available here. Lewis' testimony begins at 4:36:26.

Commissioners Brookes and Tobin, and other commissioners, it is my great pleasure to provide testimony to the US-China Economic Security Commission on the subject of China’s maritime disputes in the East China and SCSs. My name is Steven Lewis, and I am the C.V. Starr Transnational China Fellow in the Baker Institute for Public Policy, and professor in the practice and associate director of the Chao Center for Asian Studies, at Rice University. My colleagues and I in the Energy Forum of the Baker Institute have been studying the development of China’s energy economy since 1998, including hosting international research conferences in Houston, Beijing, Shanghai and Tokyo that bring together academic, government and corporate analysts from many disciplines and many countries to examine the potential for cooperation and coordination in energy policies between the United States, China and Japan. I am happy to share the results of this collective research here in the hopes it will help reveal the energy drivers of the maritime disputes in the East China Sea (ECS) and South China Sea (SCS).

The commission has posed important questions: (1) What roles do oil, gas, minerals, and fisheries play in the development and outcome of the East and SCS disputes? (2) Overall, how closely has China adhered to its long-held policy of “shelving disputes and jointly developing” natural resources? (3) What are the prospects for joint development of resources in the ECS, particularly following the failed outcome of the 2008 China-Japan joint exploration consensus of ECS gas fields? (4) To what extent could joint development of energy resources in the ECS and SCS serve as a cooperative measure? (5) Given the uncertainty of available resources and the potential economic unfeasibility of extraction, could resources be overemphasized as a driver of maritime disputes in East Asia?

In order to adequately answer these questions we must first try to answer the much larger question: what potential roles do the SCS and the ECS play in China’s long-term economic development? China has enjoyed annual growth in the 7 to 10 percent range for more than 30 years, creating a population that is now more than 50 percent urban, an urban middle class numbering in the hundreds of millions, and an economy that is increasingly international and global. How important are the SCS and ECS to keeping this economy growing at the rapid pace to which the Chinese people and government have become accustomed? I argue here that SCS and ECS play critical roles in the transportation of oil and gas imports to China’s economically vibrant localities along the Southern and Eastern China coasts. I also argue that the structure of China’s oil and gas industries, and the geological placement within China of its domestic oil and gas resources, means that in 20 to 25 years it will be importing many times more LNG across the SCS and ECS in order to maintain economic growth in these same localities. Best geological estimates of the recoverable oil and gas resources in the ECS and SCS indicate that they are very small for the ECS and quite substantial for the SCS. Even if China adopted an “imperial” strategy of colonizing its neighbors along the SCS coasts it could at most buy itself a few years of oil imports and a decade or more of gas imports. Baker Institute global gas trade models reveal that even if China were to slow down its economic growth, or to rapidly develop substantial shale gas and other unconventional gas resources (coalbed methane), in 2040 it would still require many times more LNG imports from Malaysia, Indonesia, Australia, Qatar and other major producers. Given China’s long-term energy needs, and the relative inadequacy of oil and gas resources in ECS and SCS, China has very strong incentives to work with its neighbors to cooperate in the joint development of SCS and ECS resources.

East China and South China Seas as Energy Corridors. Here, we should first distinguish between the seas as locations for transportation of trade and as locations for the provision of resources. Both seas play a critical transportation role in the development of China and other Asian economies, especially in the transportation of oil and gas. The United States Energy Information Administration estimates that in 2011 some one-third of global oil trade, totaling some 14 million barrels of oil per day, passed through the SCS, with just over 5.4 million going to China, 3.2 million to Japan and 2.4 to South Korea.2 Approximately 15 percent of the oil moving through the SCS goes on to pass through the ECS, particularly oil destined for South Korea and Taiwan. Since oil is mainly used for transportation, a conflict that disrupts oil tanker flows in the SCS would cripple transportation in three East Asian economies (and Taiwan) equally, but a conflict in the ECS that blocked crude carrier flows would disproportionately disrupt the South Korean and Taiwanese transportation systems, although as a International Energy Agency member country South Korea could call on Japan and other Organization for Economic Cooperation and Development (OECD) and International Energy Agency (IEA) members to release crude and product to help alleviate the shortages there. It is worth noting that as OECD and IEA members, South Korea and Japan are required to maintain crude stockpiles equal to 90 days worth of imports, whereas China currently maintains only some 40 days worth of crude imports. Or in other words, a conflict in the SCS would cause long lines for gas much earlier in China than in South Korea or Japan, and it is possible that a conflict in the ECS would not have a rapid or drastic impact on gas lines in China or Japan. Japan and other OECD countries’ capacity to assist South Korea in the case of a conflict in the ECS is limited, as South Korea consumes a large amount of crude.

In contrast, a conflict in the SCS that stopped the flow of natural gas on ships would quickly cripple much of the Japanese economy, especially after the Fukushima nuclear accident in 2011, which shut down almost all of Japan’s nuclear reactors (providing some 40 gigawatts of power) and forced it to fall back on natural gas for power production. The EIA estimates that in 2011 over 6 trillion cubic feet (Tcf) of liquefied natural gas (LNG) passed through the SCS daily, comprising more than half of the global LNG trade, with 3.4 Tcf (56 percent) going to Japan, 1.4 Tcf (24 percent) to South Korea, and .6 Tcf and .6 Tcf (9.5 percent each) going to China and Taiwan. A conflict in the ECS would disrupt the flow of natural gas to South Korea, Taiwan and East and Northeast China’s coastal cities. Unlike oil, the capacity for long-term storage of gas in the Northeast Asian economies is very limited, and there are no collective response mechanisms set up to deal with gas shortages among IEA members, as there is with oil. A disruption in the SCS mainly shuts down transportation in South and East China, as they rely most on imported oil, and then in South Korea, Taiwan and Japan, which are wholly dependent on imported crude. In the case of gas, disruption in the SCS alone rapidly affects power generation for both home and factory in all of Japan, Korea, Taiwan and certain cities in coastal Southern, Eastern and Northeastern China. A disruption in the ECS alone is less problematic for Japan, even as it also hurts a few localities in North and East China, and all of Taiwan and South Korea, as its LNG supplies need not pass through the ECS.

Simply looking at the global flow of oil and gas resources, then, we can see why China and Japan may be more free to engage in belligerent acts over disputed territories in the ECS than in the SCS. A maritime conflict that shut down the ECS creates enormous problems for South Korea, from transportation to factory and home, especially in the winter heating months, and on a smaller scale for Taiwan. A maritime conflict in the ECS would harm a significant part of China’s oil imports, mainly creating transportation disruption in South and East China, but only a portion of its gas imports would be affected, and those would be to cities which have the potential to fall back on coal and other energy sources. Japan could potentially largely be unaffected in its energy imports by a maritime conflict that was restricted to the ECS. And if its nuclear power plants came back online – at enormous domestic political cost for any Japanese government – Japan could reduce its dependence on LNG imports, but only enough to give it more flexibility and surplus capacity to deal with normal fluctuations in supply and demand, not enough to be free of dependence on sea lanes. Japan has recently announced it has successfully developed offshore methane hydrates, a sign that it is aggressively seeking energy supplies closer to home, as the seas to the south and east of Japan are estimated to contain enormous stores of methane hydrates. The development of these resources will likely take decades.

The long-term energy supply picture for Northeast Asia changes dramatically. In the long-term the critical importance of stability in the SCS and ECS increasingly threatens the import of fuels to power the engines of the Chinese economy, not so much the Japanese and South Korean economies, whose energy demand will grow much more slowly than China’s over the next two decades. Japan’s energy needs in 2035 are projected to be very little more than they are today. To see this, consider the long-term forecasts of the IEA, which project China’s oil imports rising from the current 50 percent of demand to more than 80 percent in 2035, and gas imports rising from less than 20 percent of demand to more than 40 percent.3 Then look at the structure of China’s oil and gas import system – through its three national oil companies, CNPC, Sinopec and CNOOC – and we can see that the bulk of China’s energy imports will come through the SCS and the ECS. China’s onshore oil exploration is largely winding down, with most of its aging fields in the Northeast (Daqing, Shengli) and the Northwest (Tarim) declining rapidly in production. Only with massive investments in new technologies are CNPC and Sinopec capable of keeping domestic onshore production from falling even more rapidly. China’s opportunities for pipeline imports of oil are also very limited, although in a few years it will be importing oil by pipeline from three of its neighbors: Kazakhstan, Russia and Myanmar. Russia and Kazakhstan today provide only some 12 percent of China’s crude imports.

China’s rapidly growing personal automobile population will thus demand many millions of barrels of oil more per day from the Middle East, Southeast Asia and Africa: all passing through the SCS and the ECS. This very dire picture for oil imports helps explain the emphasis in the 12th Five Year Plan (2011-2015) on public transportation, including high-speed rail connections between all cities of more than 1 million population, as well as Chinese central government strategic investments in alternative fuel vehicles. Interviews with Shanghai municipal government strategic energy plan advisers in recent years reveal they are pushing for electric and perhaps natural gas vehicles in order to decrease their dependence on foreign oil. The municipal government of Beijing is also considering making strategic investments in alternative fuel vehicles in order to cut down on the rapidly threatening ozone pollution, which added to the pollution from coal-fired power plants in nearby provinces is creating a choking smog that is scores of times more hazardous to individual health than the pollution permitted in European, Japanese or American cities. Both cities have adopted license plate auction systems in recent years in order to restrict the registration of new automobiles to several thousand each month, seeing the mere registration of a new vehicle cost nearly US $15,000.

If the forecast of rapidly rising oil imports by sea is dire enough for China’s energy security planners, the gas import picture is, in the long-run, even more bleak and alarming. Most Chinese officials, from those in the thousands of small cities that invest in new coal-fired power plants every day to those working in strategic energy planning in the capital, may not have a clear picture of their rapidly increasing LNG dependency, and thus the critical importance of South China and ECS sea lanes in the decades to come. This ignorance is not hard to explain. In response to crippling urban power shortages in the 1980s, China’s localities, especially those in the export-driven economies of South and Eastern coastal China, made huge local investments in coal mining, local railways and long-distance coal trucks in order to avoid the shortages caused by an over-reliance upon the central government’s Ministry of Railways and its ability to move coal from the very large deposits of coal in the North to the power-hungry localities on the coast, many hundreds of miles away. At the time these localities did not have the capital or permission of the central government to invest in LNG imports. This situation turned the majority of China’s local energy planners – those who make the vast bulk of investments in power generation in China – in to experts on coal and coal power plants.4 The Chinese central government wants localities to switch to natural gas, and very large and relatively wealthy municipalities on the coast themselves also want to move power generation over to natural gas in order to decrease their dependency on domestic coal transportation disruptions, as well as to diversify their energy fuels in general, and to reduce harmful emissions. The average Chinese energy official today, however, is still focused on coal.

China’s Economic LNG Imperative. China will need much more natural gas in the decades to come. According to the Energy Information Administration, China’s total energy consumption in recent years has been heavily dependent on fossil fuels: coal (70%), oil (19%), hydroelectric (6%), natural gas (4%), nuclear (1%), and other renewables (.3%).5 China’s government leaders are actively working both to diversify the sources of energy and to find cleaner sources of energy. The 12th Five-Year Plan (FYP) (2011 to 2015) is the first in which China’s central and local economic planners have confronted climate change, establishing national goals and metrics to shift from fossil fuels to renewable sources of energy, and among fossil fuels to transition from coal and oil to natural gas.6 The 12th FYP calls for the reduction of energy consumption per unit of GDP by 16%, and the cutting of CO2 emissions per unit of GDP by 17%. Non-fossil fuels (currently around seven percent) should account for 11.4% of total primary energy consumption by 2015. The central government also plans to set local energy conservation targets which must be met by local governments: “The central government will create energy control requirements for province-level governments and hold them accountable for fulfilling the requirements.”7

During the 11th FYP, the central government implemented the 1,000-Enterprise Plan, in which central government authorities were largely successful in forcing the largest energy intensive industrial users to sign energy efficiency contracts — most likely because many of these enterprises were owned directly by the central government — and under the current FYP it plans to carry the program forward to the lower levels and crack down on local government enterprises that waste energy resources.

The central government has more than sticks to wield, however, as it has a track record of offering carrots to local enterprises and local government leaders who can help it achieve a strategic global advantage in manufacturing and technology. The 12th FYP and supporting documents and policies further detail strategic investments to be made by central and local governments to support “emerging strategic industries”: new-generation information technology, energy-saving and environmental protection, new energy, biology, high-end equipment manufacturing, new materials and new-energy cars. Beijing plans to not only open up its coffers to support enterprises that can clean up its cities and conserve energy, it hopes to turn them in to central state enterprises that can go out and become global leaders, perhaps stealing a march on their slower Western competitors, as was the case with solar panel manufacturers.8 This demonstrated capacity for the central government to support strategically, and even potentially raise to the level of central ownership, enterprises that succeed in global markets is a unique feature of China’s decentralized planned economy, one that makes up for the inability of China’s still-developing stock markets to direct domestic capital toward state enterprises that are competitive in international markets.

Finally, in the months since the release of the 12th FYP, China’s central leaders have made it clear they will continue to support the “going abroad” strategy of its large central owned state enterprises, including the three central national oil companies (NOCs), China National Petroleum Corporation (CNPC), Sinopec and China National Offshore Oil Corporation (CNOOC), to obtain the necessary fossil fuels and the technology and management practices to produce and market them within China and abroad. Top Communist Party leaders reshuffled the top leaders of the three NOCs in 2011, largely to insure the Politburo retained control over these immensely powerful organizational actors in China’s energy economy, including their ability to use the NOCs to forge strategically important gas pipeline ties to Central Asian states, Myanmar and Russia, and equally important LNG ties to Australia, Indonesia, Malaysia, Yemen, Iran, Trinidad, Nigeria and Russia.9 With increasingly interdependent trade and financial ties between China and the United States in recent years, all three Chinese NOCs have even made their way past American political opposition to become partners in natural gas and shale gas projects in the American South and Midwest. Far from being the dinosaurs of the planned economy era, these very large central owned enterprises have proven adept at adaptation and innovation, largely through experiments created by through subsidiaries, and there is little call publicly in China to continue privatization and make them majority private entities.

Although currently providing only four percent of China’s primary energy consumption, natural gas is tipped to become the fuel of choice for China’s localities, growing from the current consumption of around five Tcf/y at five percent per year to reach nearly 12 Tcf/y by 2035, according to the EIA.10 Historically, China’s gas sector grew much as its petroleum sector grew: according to local geological and economic factors, and by the state-owned petroleum and gas enterprises. Except for the Sichuan Oilfield Administration in Southwest China, which created an extensive local ring of pipelines in the 1950s to supply gas to local enterprises and cities, most of China’s gas infrastructure was initially developed to handle associated gas in the major petroleum producing centers of Northeast China (Daqing, Shengli, Liaohe Oilfields). And when it became apparent in the late 1990s that the increasing cost to the central government of moving coal by train and boat from the North to the resource-poor and yet economically prosperous South and Eastern provinces could imperil these export engine localities, these areas and CNPC began to build the first cross-country pipelines, connecting the gas fields of Western China’s Xinjiang Autonomous Region (and later Kazakhstan and Turkmenistan and Uzbekistan) to Shanghai and some ten provinces in between. The second West-East Gas pipeline opened in 2011, work on the third has started, and is expected to be completed in 2015, with plans to run from West China to South and Southeast China and the areas around Hong Kong, Guangdong and Fujian. The first West-East pipeline carries 430 Bcf/y, the second 1.1 Tcf/y, and the third is designed to carry 1.1 Tcf/y. The third line, which is partially financed by private investors, finds an East China market for the Central Asia Gas Pipeline (CAGP) network that China has built connecting neighboring Kazakhstan, Turkmenistan and Uzbekistan. The pipeline has capacity of 1.4 Tcf/y and some 530 Bcf/y came through in 2011, with China signing deals with Turkmenistan to expand to 1.1 Tcf/y, and through additional extensions, an extra 360 Bcf/y each from Kazakhstan and Uzbekistan to enter China after 2015.11 Overall, China is expected to double its 27,000 miles of gas pipelines to 51,000 miles in 2015, and there are plans to increase notoriously low storage capacity of 70 Bcf to 1,010 Bcf by the end of the 12th FYP. CNPC owns most of the cross-country trunk pipelines, with Sinopec recently adding one from Southwestern Sichuan to Shanghai in the East, and local distribution companies own the transmission lines in urban areas.12

Meanwhile, gas from Myanmar will soon tie in to Southwest China’s Yunnan Province through a 1,100-mile 430 Bcf/y pipeline, and Russian Far East gas is expected to enter China through either the Northwest Xinjiang region and a 1 to 1.4 Tcf/y pipeline, or following oil pipelines from Siberia in to the rust-belt economies of the Northeast through a 1.1 to 1.4 Tcf/y pipeline that connects China to gas from Eastern Siberia and Sakhalin Island. China gets little gas from offshore. A small amount of gas flows from offshore in to Shanghai, and from the SCS in to Hainan Province, necessitating the planned siting of both nuclear power plants and LNG terminals and gas power plants in the thriving coastal areas of South, East and Northeast China. China became a net importer of natural gas only in 2007, with LNG, and pipelines in the Northwest, rapidly expanding imports today. There are currently five LNG regasification terminals operating in coastal China, joint-ventures between CNPC and CNOOC and such foreign partners as BP, QatarGas, Malaysia’s Petronas, Australia and Iran, in which some 586 Bcf/y comprised half of China’s gas imports in 2011. Four more terminals are under construction, and six more are planned, with the next regasification capacity doubling from 1 Tcf/y today to 2 Tcf/y by 2015.13 Overall, China does indeed have a large gas pipeline and LNG terminal infrastructure, but it is designed to feed Chinese coastal cities directly from overseas, with only a few longer pipelines connecting the far West and Central Asia to the East, and smaller denser webs of pipelines in the Northern areas around Beijing, and then a more developed ring network in the Sichuan basin of Southwest China.

Worth noting is that the first West-East gas pipeline took more than a decade to build, requiring the creation of an informal “leadership small group” at the highest levels of the Communist Party to coordinate and eliminate obstacles for its development, with the first LNG regasification terminals necessitating similar extraordinary organizational measures. More recent pipelines and terminals have still faced considerable red tape problems in their development, but China appears to have worked out a political and organizational model to coordinate the at-time competing interests of central government, central enterprise (NOCs), local governments and local enterprises, and then in recent years to bring on board domestic private investors as well. It is telling that many cities, provinces and counties in China’s shale gas regions, for example, are forming “shale gas economic development leadership small groups,” a sure sign that they are mobilizing senior cadres in to ad hoc groups capable of overcoming bureaucratic and political obstacles to develop this potentially important fuel.

Most recently China’s central planners have turned their eyes toward developing unconventional gas. Pointing to an estimated 10.2 Tcf of proven coal bed methane (CBM) reserves in 2011, with an estimated 350 Tcf of recoverable CBM reserves, the central government sanctioned the formation of China United Coalbed Methane Corporate (CUCMC) in 1996 by CNPC and China Coal Energy Corporation to develop reserves in the North, Southwest and West, China’s major coal-producing areas. According to the IEA and FACTS Global Energy, CBM production was estimated to be 315 Bcf/y in 2010, and the Chinese government expects that to rise to 1,060 Bcf/y by the end of the 12th FYP in 2015.14 There is currently one CBM pipeline that connects the Qinshui Basin in North China to the West-East Gas Pipeline, and the company and local governments are building several more. In a move presaging later actions to accelerate the development of shale gas, the National Energy Administration in Beijing in 2007 opened up CUCMC’s monopoly on the formation of technical join ventures with foreign partners, ushering in to the field CNPC working on its own, Sinopec and most recently CNOOC. It also began to provide the company with production subsidies. CUCMC, now half-owned by CNOOC, in 2012 signed an agreement with CNOOC to spend US $1.56 billion developing CBM over the next 30 years.15 Most CBM in China is liquefied and sent by truck to local areas for residential use, but FACTS Global Energy estimates that with more pipelines being built by CNPC’s PetroChina it will increasingly be used for power and may rise to 2 Tcf/y by 2020.

Shale gas is widely expected to be even more influential than CBM in China’s future gas economy. The recent US DOE sponsored assessment of global shale gas by ARI (2011) places China’s technically recoverable shale gas resource at over 1,200 Tcf. China’s Ministry of Land and Resources puts domestic shale gas resources at 917 Tcf, and is targeting the development of 10 to 15 “experimental shale development regions” by 2015.16 Facing initial “foot dragging” by the NOCs, whom interviews with reveal consider shale gas to be yet another potentially costly burden that cuts in to their profits -- much as their recent efforts to invest in costly pipelines to Central Asia and long-term contracts and terminals for LNG -- the central government has once again goaded the NOCs by letting more competitors come sit around the policy-making table. With the development of the 15 experimental shale gas development zones, the central government raises the possibility that it will directly step in to appoint local leaders in shale producing regions, and with its declaration in 2011 that shale gas will be priced separately from oil and conventional gas, and that it will support it with price subsidies, the central planners are essentially daring the NOCs to ignore a potential resource that has not just economic value, but political value for energy industry cadres. Historically, whenever the central government makes a major investment in an energy project it raises the nomenklatura ranking within the Communist Party of its leaders. CNPC and Sinopec in particular thus understand the political threat implicit in Beijing’s creation of shale gas development zones: the future leaders of such zones may have competitive Party ranking to the leaders of their own major oilfields and refineries, potentially giving them less comparative Party clout in central government policy-making. Shale gas is thus far a union of central planners who are attracted to its energy security implications, and ambitious local leaders who see it as a potential “helicopter ride” to Beijing.

Shale gas is still an unexplored resource in China, and regardless of the assessment of technically recoverable resource, there is tremendous uncertainty around the economically recoverable shale resource. But even as China’s mega-firms are moving somewhat slowly on shale investment, the National Energy Administration incorporated shale gas into its “National Energy Strategies Toward 2030,” assigning targets for shale gas development in the 12th FYP, and its parent National Reform and Development Commission indicated that it saw price reform as an ultimate necessity.17 To promote rapid development of shale gas, domestic prices must be structured to incentivize large investments. China’s shale resources are thought to be relatively expensive to develop compared to the US and other regions. There are also several other barriers besides pricing to rapid development that must be overcome. These include long distances between shale rich regions and major end-use markets and a lack of existing pipeline infrastructure, in addition to water constraints in some many potentially prolific areas.

American and European companies are also trying to engage in the development of unconventional gas in China. For the most part, Chevron has been focusing on its Chuangdongbei project, the first large-volume sour gas development in China, although it is interested in shale opportunities in China. While first commercial output from Chuangdongbei has been delayed by complex geography, Chevron has found recoverable and proved gas reserves of 6.2 Tcf, which will yield about 4.0 Tcf of marketable gas. Initial output is planned at 740 mmcfd from two large-scale cleaning plants, but will only be achieved late in 2012. A second phase would double output by 2016, but timing and volume will be dependent upon the operating experience gained in initial sustained production. The US firm has considerable experience in handling gas with large volumes of inerts as well as hydrogen sulfide, a gas that is both corrosive and explosive. Chevron hopes to be the partner of choice for developing technically challenging gas finds. Shell has pledged $5 billion to explore the Jingqui and FushunYangchuan shale blocks with CNPC. BP, Statoil, Hess and ExxonMobil also pursuing opportunities in Chinese shale.

So in the long-term can China utilize unconventional gas to become “gas import free” as the United States is set to become in future years? The research of the Baker Institute’s Energy Forum and its partners all around the world in the Rice World Gas Trade Model (RWGTM) suggests that this is very unlikely. A 2011 report by the Baker Institute estimates that in order to continue even moderate levels of economic growth, and to continue using coal resources, China will need to steadily increase its gas use over the next 25 years to some 20 Tcf/y. According to a “status quo” scenario in which China has continued high growth to 2040, and it has relative success in developing shale gas resources (to 3.5 Tcf) and pursues conventional gas (1.5 Tcf) and international pipeline gas (4 Tcf), its LNG imports will still rise from the current .6 Tcf/y to around 11 Tcf. Even in a “high shale gas” scenario, in which China produces domestically some 14 Tcf/y from unconventional gas, it will still need some 3 Tcf/y of LNG (with 2 Tcf/y from pipelines) by 2040. This is so because shale gas – which will be likely be more costly to develop and produce than in the US because it is commonly twice as deep as US shale deposits, and because most Chinese shale plays will require imports of water for hydro-fracturing – will still not be found near the major consumption centers of costal South and East China. LNG from the rest of the world will often be the most economical fuel for industrial and residential power in these vibrant local economies.18

Contrary to the dreams of China’s energy-security-conscious energy planners in Beijing, if China experiences a shale gas revolution similar to America’s, in which nearly half of all gas consumption comes from shale and other unconventional gas production, it is unlikely to obtain the ability to be free of either pipeline gas or LNG from overseas. America’s vast gas pipeline network allows most localities to switch at low cost between domestic shale, conventional gas and imported LNG and piped gas sources across its regions. China’s underdeveloped network means that North, Northeast, Central and Western China benefit disproportionately from any boom in shale gas production. The future economic growth of China’s most prosperous cities and provinces is one heavily tied to massive fleets of LNG carriers (with four or five times the number of vessels used today) sailing toward them across the SCS and the ECS. Or, in other words, the long-term economic growth of China’s most developed local economies is unquestionably dependent on the safe flow of LNG across the two bodies of water.

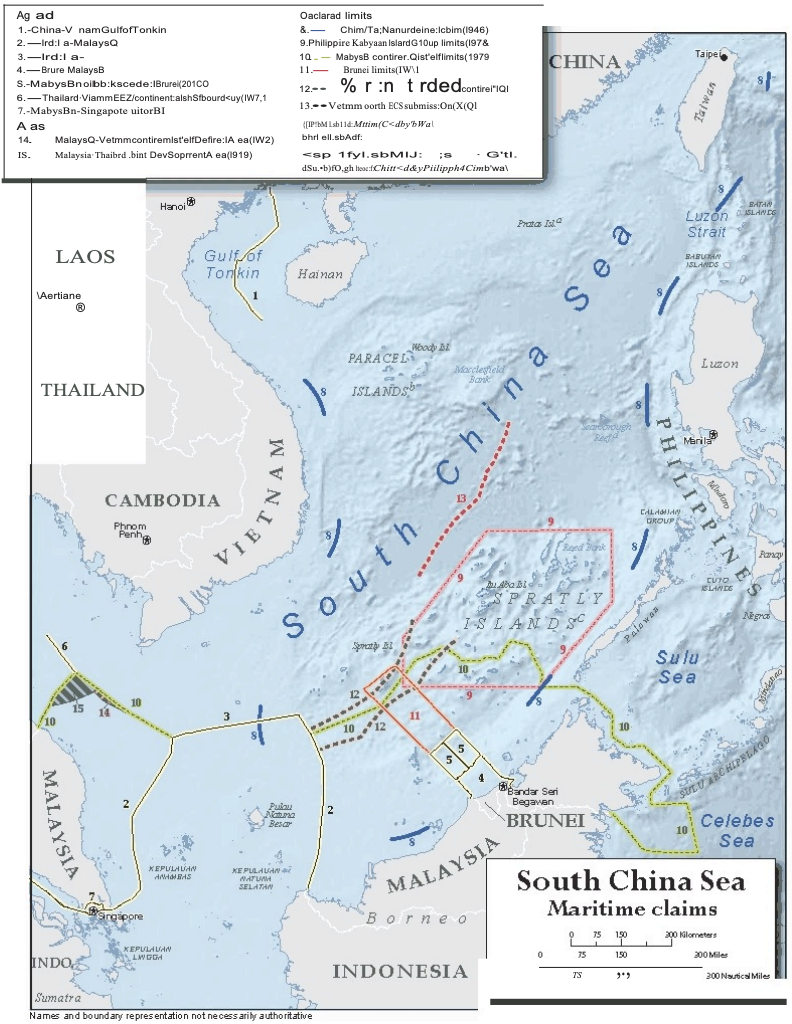

East China and South China Seas as Energy Supplies. Given that there is an economic LNG imperative that will in the long-term drive China to make very large LNG imports through the SCS and the ECS, can the discovery and production of energy resources underneath the ECS and SCS themselves make China more energy independent? In stories too numerous to cite, the state media of China, and occasionally Western media as well, routinely cite estimates that the SCS in particular contains enormous stores of petroleum and natural gas. The problem with these unattributed and unexplained statistics is that they do not delineate the boundaries of the SCS. Chinese media reports typically assume the energy resources of the SCS include all of those of the countries and regions bordering the SCS: Taiwan, Philippines, Malaysia, Brunei, Indonesia, Vietnam and Thailand. Most Western energy analysts, however, distinguish between the nearoffshore resources and the far-offshore resources. Here, the SCS can be said to have the energy resources of a “donut”: much on the periphery, with no proven resources in the middle.19 Map A in the appendix uses US State Department and EIA data to map out the competing claims among these countries, many of which belong to the Association of South East Asian Nations (ASEAN).20 Looking more closely, USGS estimates of undiscovered oil and gas resources in SCS map out much of these sections of the “donut”, estimating oil and gas resources for nine basins. The Pearl River Basin just offshore South China is estimated to hold 608 million barrels of oil (MMBO) and 9,035 billion cubic feet of gas (BCFG), or about four month’s imports of oil, and four-year’s imports of gas.21 If China can manage to persuade or intimidate Taiwan, Philippines, Malaysia and Vietnam to give up their occupation of the Spratley Islands it might be said to hold the entire claim to the basin known to USGS as South China Sea Platform, which is estimated to contain 2,522 MMBO of oil and 25,519 BCFG. Or, in other words, if China can retain control of the Pearl River Delta Basin and also exert itself diplomatically and militarily to control the South China Sea Platform it could potentially develop several year’s worth of current oil imports and a dozen year’s gas import needs. This is the most that an aggressive China could hope to achieve without seizing large islands that are part of its Southern neighbors.

But what if China were to turn imperial and take the entire SCS donut, including the shorelines that sit above the basins that run offshore? The largest parts of the donut would be those controlled by Malaysia and Brunei, and the smallest parts would be those controlled by Taiwan, Philippines and Vietnam. To take the parts of offshore and onshore basin facing the SCS currently held by Malaysia and Brunei (the Greater Sarawak Basin and Baram Delta/BruneiSabah Basin) would gain approximately 4,921 MMBO and 64,448 BCFG. Even these rich assets would only provide China with enough oil to offset several years of current oil imports, and perhaps 15 years of current gas imports. The Philippines controlled Palawan Shelf Basin might yield 270 MMBO and 1,408 BCFG. The Vietnamese controlled Song Hong Basin running along its northern shore, and the Phu Kanh Basin running along its southeastern shore, would together yield 427 MMBO but 25,306 BCFG. If Vietnam were to also control the Cuu Long Basin and Nam Con Son Basins along its southwest shore, and out in to sea close to Malaysia’s, Thailand’s and Indonesia’s claims just beyond the western boundaries of the SCS, then Vietnam could also control an additional 2,420 MMBO and 18,997 BCFG.22 If China were to seize control of these basins, all of which lie within several hundred miles of Vietnamese shore, it could possibly gain itself another two year’s worth of oil imports and a decade of gas imports. A new imperial China that was capable of seizing control of the oil and gas resources of its southern neighbors would still only gain a few years of oil imports, but several decades of potential gas imports, assuming it had the technical ability to develop these.

The East China Sea has far fewer estimated resources than the SCS. The EIA and CNOOC estimates are that there are perhaps 18 million barrels of oil there, and 1 to 2 TCF of natural gas, most of it in a geologically difficult trench claimed by both China and Japan, and capable of being explored through a joint production agreement never put in to operation. Politics in the form of nationalist protests over the Diaoyu/Senkaku Islands has intervened, but economics is also harsh, considering the small amounts and the high cost to construct lengthy pipelines to Chinese and Japanese gas markets. Interviews with both Chinese and Japanese company officials suggest that even if there were no political disputes there would be not much incentive to develop these projects. Nevertheless, it is likely that if protests diminish the Chinese and Japanese companies will resume, as both have been told to jointly develop projects with each other.

A full accounting of resources in the SCS and ECS would include fisheries and methane hydrates. I leave the fisheries to relevant experts to detail, and note that any potential commercial exploration and production of methane hydrates is likely to occur decades from now, and it would certainly first proceed onshore before moving offshore, especially to contested waters.

Conclusions and the Potential for Cooperation and Conflict in ECS and SCS. How important are the SCS and ECS to keeping this economy growing at the rapid pace to which the Chinese people and government have become accustomed? I argue here that SCS and ECS play critical roles in the transportation of oil and gas imports to China’s economically vibrant localities along the Southern and Eastern China coasts. I also argue that the structure of China’s oil and gas industries, and the geological placement within China of its domestic oil and gas resources, means that in 20 to 25 years it will be importing many times more LNG across the SCS and ECS in order to maintain economic growth in these same localities. Best geological estimates of the recoverable oil and gas resources in the ECS and SCS indicate that they are very small for the ECS and quite substantial for the SCS. Even if China adopted an “imperial” strategy of colonizing its neighbors along the SCS coasts it could at most buy itself a few years of oil imports and a decade or more of gas imports. Baker Institute global gas trade models reveal that even if China were to slow down its economic growth, or to rapidly develop substantial shale gas and other unconventional gas resources (coalbed methane), in 2040 it would still require many times more LNG imports from Malaysia, Indonesia, Australia, Qatar and other major producers. Given China’s long-term energy needs, and the relative inadequacy of oil and gas resources in ECS and SCS, China has very strong incentives to work with its neighbors to cooperate in the joint development of SCS and ECS resources, or risk serious harm to its economy. Interviews with Chinese international security advisers to the central government suggest that they will seek to find ways to bring the United States, and the OECD nations, in to broader negotiations over the full range of “ocean commons”, linking SCS discussions with Polar Sea discussions, for example. Here, the work of American and Chinese scholars looking at building umbrella treaties and organizations to deal with maritime resources and transportation disputes might be useful.”23 Discussions with Chinese officials also suggest that bilateral USChinese discussions on other “commons”, such as cyberspace, space, and the terrestrial atmosphere, might also be welcome.

Endnotes

1. This testimony would not be possible without the assistance of many, especially colleagues Ken Medlock, Peter Hartley, Joe Barnes and Ron Soligo of the Baker Institute, Amy Myers Jaffe of UC Davis, Meghan O’Sullivan of Harvard’s Belfer Center, and particularly Al Troner of APEC Energy Consulting. Invaluable help was provided by research assistants Ying Zhang, Devin Glick, Benjamin Chou, Yuanzhuo Wang, Neeraj Salhotra, Andy Wang, Julian Yao, Simon Wu, Ran Chen, Jay Yusheng Chen and David Liou.

2. [http://www.eia.gov/countries/regions-topics.cfm?fips=SCS] (Accessed 3/28/2013).

3. [http://www.worldenergyoutlook.org/] (Accessed 3/28/2013).

4. See Steven W. Lewis, “China and Energy Security in Asia,” published by the Korean Economic Institute Policy Forum, May 2008, at [bakerinstitute.org/publications/ASIA-EnergySecurity-050608.pdf].

5. http://www.eia.gov/countries/cab.cfm?fips=CH (Accessed 3/28/2013).

6. For English summary see http://news.xinhuanet.com/english2010/china/2011-03/05/c_13762230.htm (Accessed 3/28/2013) and for Chinese full text see http://news.xinhuanet.com/politics/2011-03/16/c_121193916.htm (Accessed 3/28/2013).

7. http://news.xinhuanet.com/english/china/2013-01/24/c_132125842.htm (Accessed 3/28/2013) and for a useful analysis see “Energy and Climate Goals of China’s 12th Five-Year Plan” by Joanna Lewis of C2ES at http://www.c2es.org/international/key-country-policies/china/energy-climate-goals-twelfth-five-year-plan (Accessed 3/28/2013).

8. See Edward Steinfeld’s Playing Our Game: Why China's Rise Doesn't Threaten the West (Oxford, 2010).

9. On the 2011 reshuffle see Erica Downs and Michael Meidan’s “Business Politics in China: The Oil Executive Reshuffle of 2011,” in China Security, 2011, Issue 19, pp. 3-21, at http://www.chinasecurity.us/index.php?option=com_content&view=article&id=489&Itemid=8 (Accessed 3/28/2013) and for a history of the NOCs see Steven W. Lewis, “Chinese NOCs and World Energy Markets: CNPC, Sinopec and CNOOC,” Baker Institute Energy Forum, 2007, at http://www.bakerinstitute.org/programs/energy-forum/publications/energy-studies/docs/NOCs/Papers/NOC_CNOOC_Lewis.pdf (Accessed 3/28/2013) and for an analysis of the current political role of the NOCs see Steven W. Lewis, “Carbon Management in China: The Effects of Decentralization and Privatization,” Baker Institute Energy Forum, December 2011, at www.bakerinstitute.org/publications/EF-pub-RiseOfChinaLewis-120211-WEB.pdf (accessed 3/28/2013).

10. http://www.eia.gov/countries/cab.cfm?fips=CH (Accessed 3/28/2013).

11. See http://www.eia.gov/countries/cab.cfm?fips=CH (Accessed 3/28/2013).

12. See http://www.eia.gov/countries/cab.cfm?fips=CH (Accessed 3/28/2013).

13. See http://www.eia.gov/countries/cab.cfm?fips=CH (Accessed 3/28/2013) for US data and analysis, and for Japanese data and analysis see Yoshikazu Kobayashi of IEEJ’s “Natural Gas Situation and LNG Supply/Demand Trends in Asia Pacific and Atlantic Markets,” 2010, at http://www.eneken.ieej.or.jp/data/2940.pdf(Accessed 3/28/2013).

14. For IEA see http://www.eia.gov/countries/cab.cfm?fips=CH (Accessed 3/28/2013) and for FACTS Global Energy see Alexis Aik and Christopher Gascoyne, “Unconventional Gas and Implications for the Global LNG Market,” at National Bureau of Asian Research 2011 Pacific Energy Summit, http://nbr.org/downloads/pdfs/eta/PES_2011_Facts_Global_Energy.pdf (Accessed 3/28/2013).

15. See Reuters, “CNOOC Signs 1.56 bln Domestic Coalbed Methane Deal,” August 5, 2012, at http://www.reuters.com/article/2012/08/06/cnooc-coalseam-idUSL4E8J603Q20120806 (Accessed 3/28/2013).

16. For the ARI report, “World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States,” see http://www.eia.gov/analysis/studies/worldshalegas/(Accessed 3/28/2013).

17. See National Energy Administration website and “页岩气发展规划(2011-2015 年)” at http://www.nea.gov.cn/zwhd/wszb20120316/index.htm (Accessed 3/28/2013).

18. See Kenneth B. Medlock III and Peter R. Hartley, “Quantitative Analysis of Scenarios for Chinese Domestic Unconventional Gas Resources and their Role in Global LNG Markets,” paper presented at The Rise of China and Its Energy Implications, Baker Institute Energy Forum, December 2, 2011, at http://www.bakerinstitute.org/programs/energy-forum/publications/energy-studies/the-rise-of-china-and-its-energy-implications [Accessed 3/28/2013). Scholars from the Baker Institute Energy Forum and the Belfer Center at Harvard University have applied the model to explaining global gas trade under a wide range of scenarios, with the results of this research to be released in September 2013.

19. I am indebted to Al Troner of Apec Energy Consulting for this analogy.

20. US Energy Information Administration, using State Department data: http://www.eia.gov/countries/regions-topics.cfm?fips=SCS [Accessed 3/28/2013).

21. See USGS, “Assessment of Undiscovered Oil and Gas Resources of Southeast Asia, 2010,” at pubs.usgs.gov/fs/2012/3042/fs2012-3042.pdf (Accessed 3/28/2013).

22. See USGS, “Assessment of Undiscovered Oil and Gas Resources of Southeast Asia, 2010,” at pubs.usgs.gov/fs/2012/3042/fs2012-3042.pdf (Accessed 3/28/2013).

23. See a summary of these and the idea of a “global maritime partnership” in Andy Wang, “Calming the Seas: China, The United States and Transforming Maritime Rivalries in to Partnerships,” The Rice Cultivator, Vol. 3, 2012, pp. 62-87, http://www.bisf.rice.edu/research/currentandpastissues/ (Accessed 3/28/2013).

Map A